airdone

airdone

With a market capitalization as of this writing of $45.39 billion and an estimated enterprise value of $70.11 billion, Realty Income (NYSE:O) is one of the largest publicly traded REITs on the planet. The company experienced a bit of a boost to its size earlier this year when management completed the acquisition of another REIT called Spirit Realty Capital at what was initially valued as a $9.3 billion deal. Since the completion of the transaction, management has come out with more fundamental data. This allows us to get a glimpse into what the picture looks like today and what the future might hold for the company and its investors. Because there are some holes in the data, holes that will be filled eventually, it's difficult to get a picture-perfect view of matters. But what data does exist suggests that Realty Income, post-merger, still remains an attractive prospect for investors.

Back in November of 2023, I wrote a bullish article regarding Realty Income. That particular article was dedicated to exploring the announced transaction between it and Spirit Realty Capital. At that time, I talked about how the transaction would help the company diversify further while simultaneously allowing it to become the fourth largest REIT, by enterprise value, in the S&P 500. At the end of the day, my findings led me to rate the company a ‘buy’ but the picture since then has not been the best. In a short window of time, shares have seen upside of 10.9%. But this has paled in comparison to the 19.8% increase achieved by the S&P 500 over the same window of time.

Author - SEC EDGAR Data

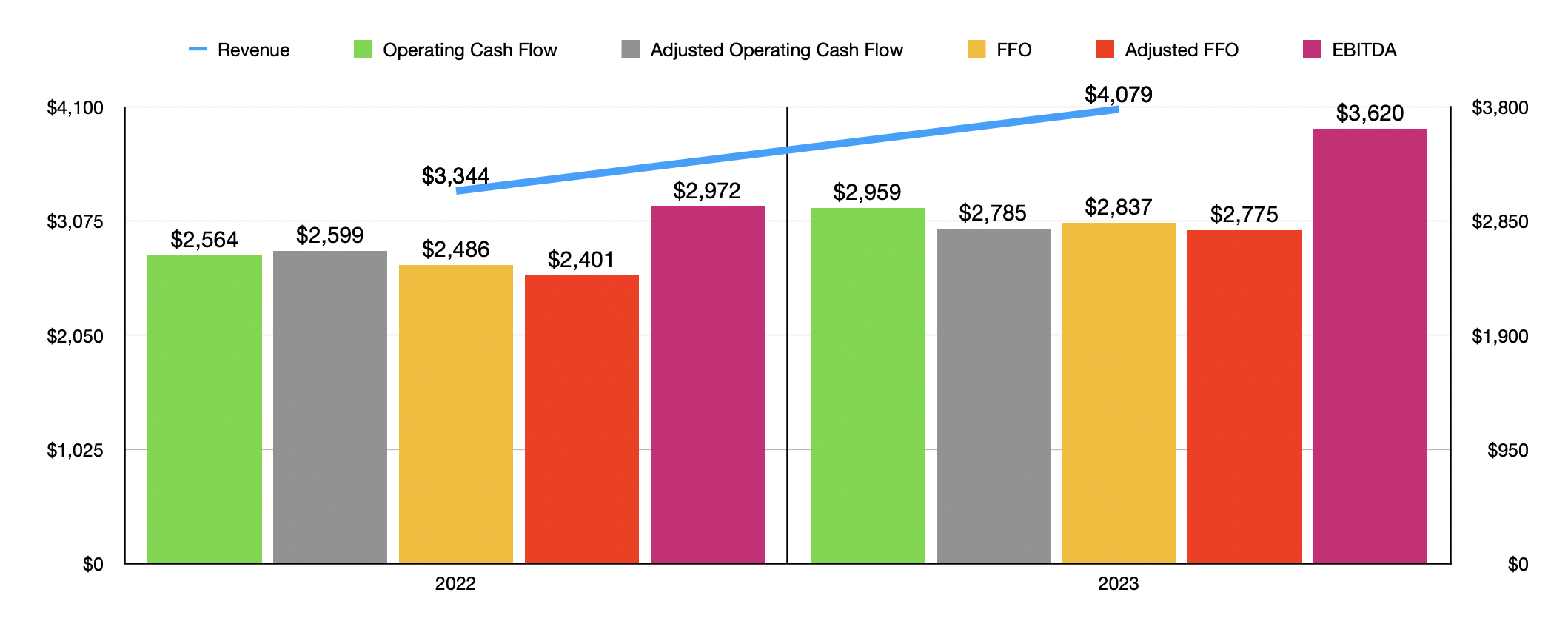

Because of the transaction between the two companies, a historical review of Realty Income and its performance is not terribly significant at this time. But it's not a bad idea, for reference, to at least touch on financial results from the past two fiscal years. In the chart above, you can see revenue for the company, as well as certain profitability metrics. Thanks to significant investments made in growth initiatives, namely $9.5 billion allocated toward various investments, including outright asset purchases and investments in unconsolidated entities, the firm saw its revenue jump from $3.34 billion to $4.08 billion. Such a significant increase in revenue came about because of an increase in the number of properties owned from 12,237 to 13,458. This resulted in an increase in square footage from 236.8 million to 272.1 million. And none of this includes the aforementioned acquisition.

With revenue rising, cash flows rose nicely as well. As you can see, operating cash flow as well as adjusted operating cash flow both rose nicely from 2022 to 2023. FFO, or funds from operations, as well as adjusted FFO, managed to rise. Even EBITDA increased for the company, rising from $2.97 billion to $3.62 billion. All things considered, this is a very impressive showing freight company that is already large and that operates in mature markets.

Realty Income

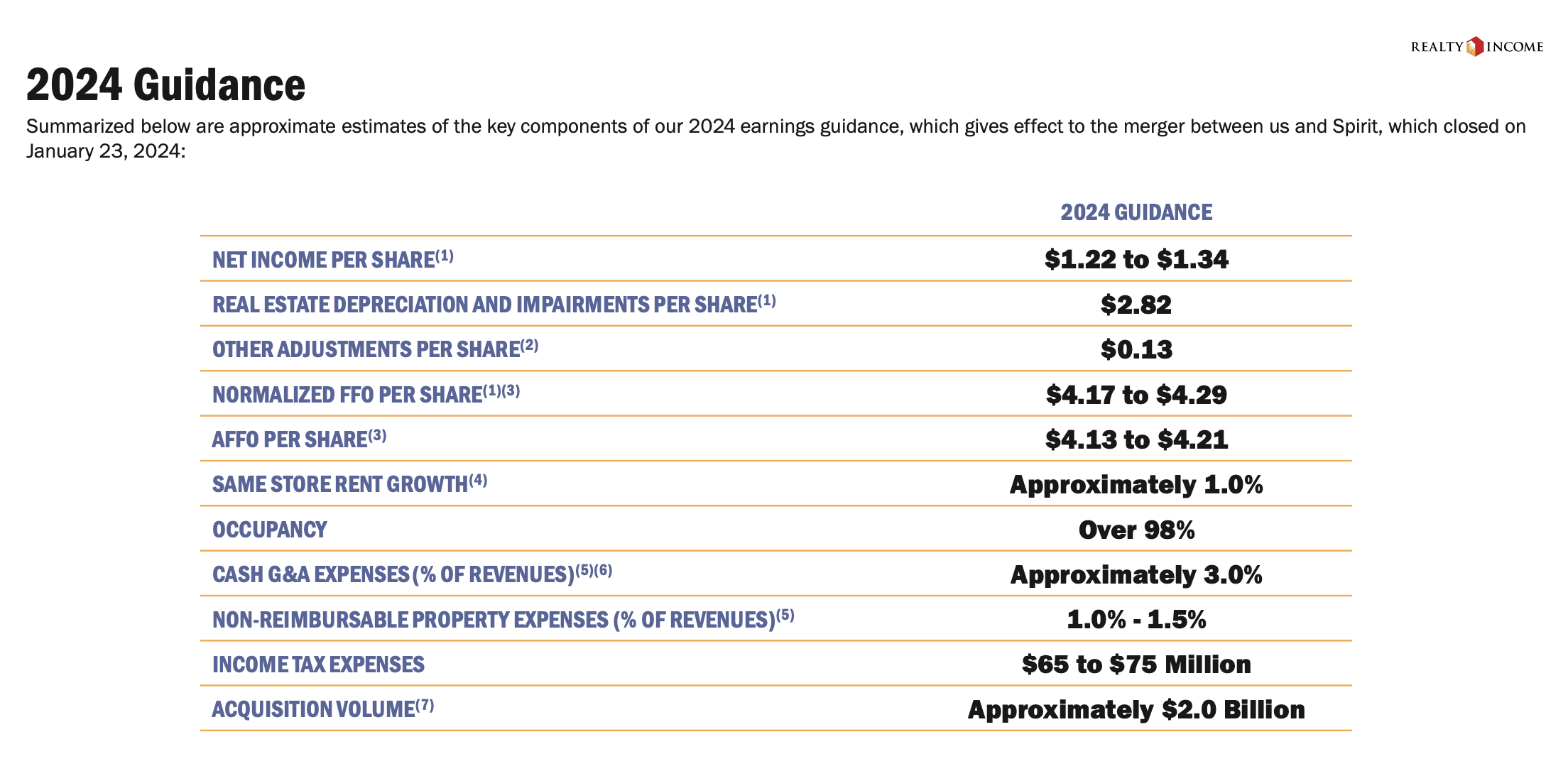

Thanks to the acquisition of Spirit Realty on January 23rd of this year, the business now looks a great deal different than it did previously. That's because the deal brought with it ownership over another 2,018 properties. One of the great things about management is that they have been very open about what investors should expect moving forward. For this year, for instance, they are forecasting normalized FFO per share of between $4.17 and $4.29, while adjusted FFO per share should be between $4.13 and $4.21. As part of the acquisition of Spirit Realty, the number of shares outstanding for the company exploded. However, that wasn't the only complication in terms of figuring out what these per share figures should ultimately amount to. You see, we knew exactly how many shares would be issued as part of the transaction. But in addition to this, the firm has ATM (at-the-market) forward agreements to sell up to 10.8 million shares of stock that it has been using to fund continued growth. We know that, in January of this year, the company received net proceeds for 4.6 million of these units. Ultimately, the company expects $605 million worth of net proceeds from these sales. So to make things simple, immediately added on the full 10.8 million shares and the expected cash from the transactions into my figures.

Author - SEC EDGAR Data

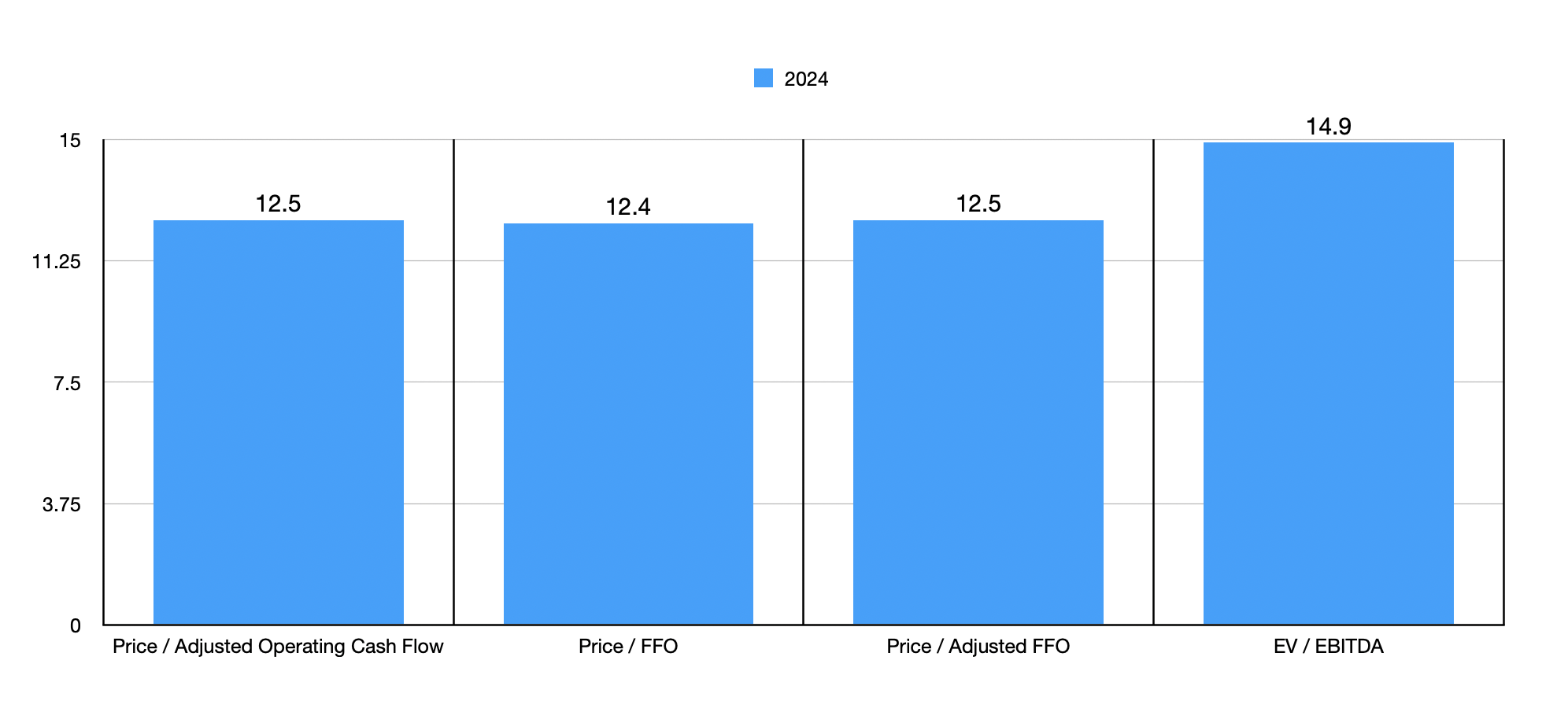

What we get for 2024 is FFO of $3.67 billion and adjusted FFO of $3.62 billion. If we assume that other profitability metrics will rise at the same rate, we would anticipate adjusted operating cash flow of $3.63 billion and EBITDA totaling $4.72 billion. Using these results, we can value the company as shown in the chart above. In the table below, meanwhile, we can stack up the company against similar firms. On a price to operating cash flow basis, two of the five companies ended up being cheaper than Realty Income, while one of the five ended up being cheaper when it came to the EV to EBITDA approach.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Realty Income | 12.5 | 14.9 |

| Simon Property Group (SPG) | 12.7 | 15.1 |

| Kimco Realty (KIM) | 11.3 | 14.2 |

| Regency Centers (REG) | 15.4 | 18.0 |

| Federal Realty Investment Trust (FRT) | 14.9 | 17.7 |

| NNN REIT (NNN) | 12.4 | 15.0 |

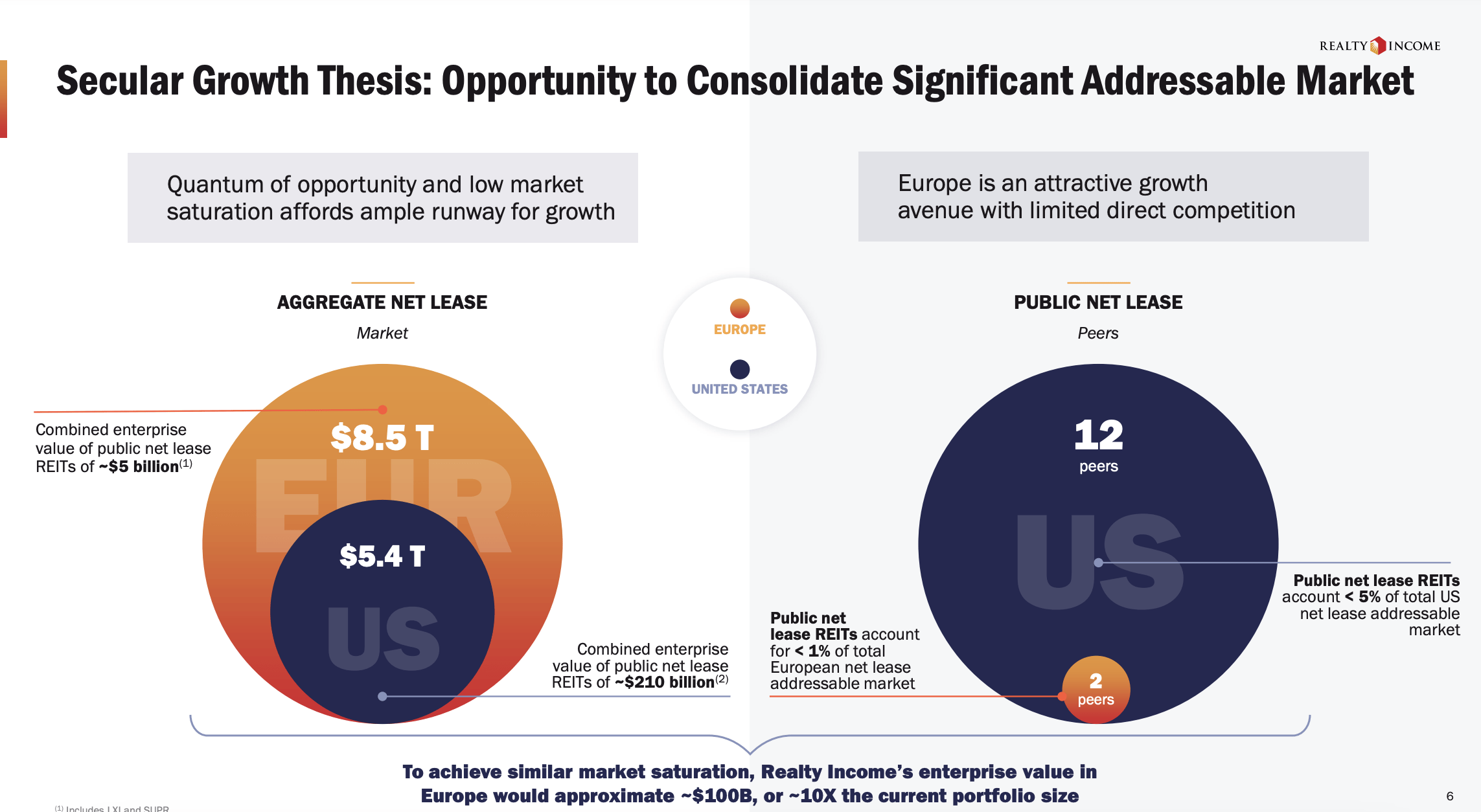

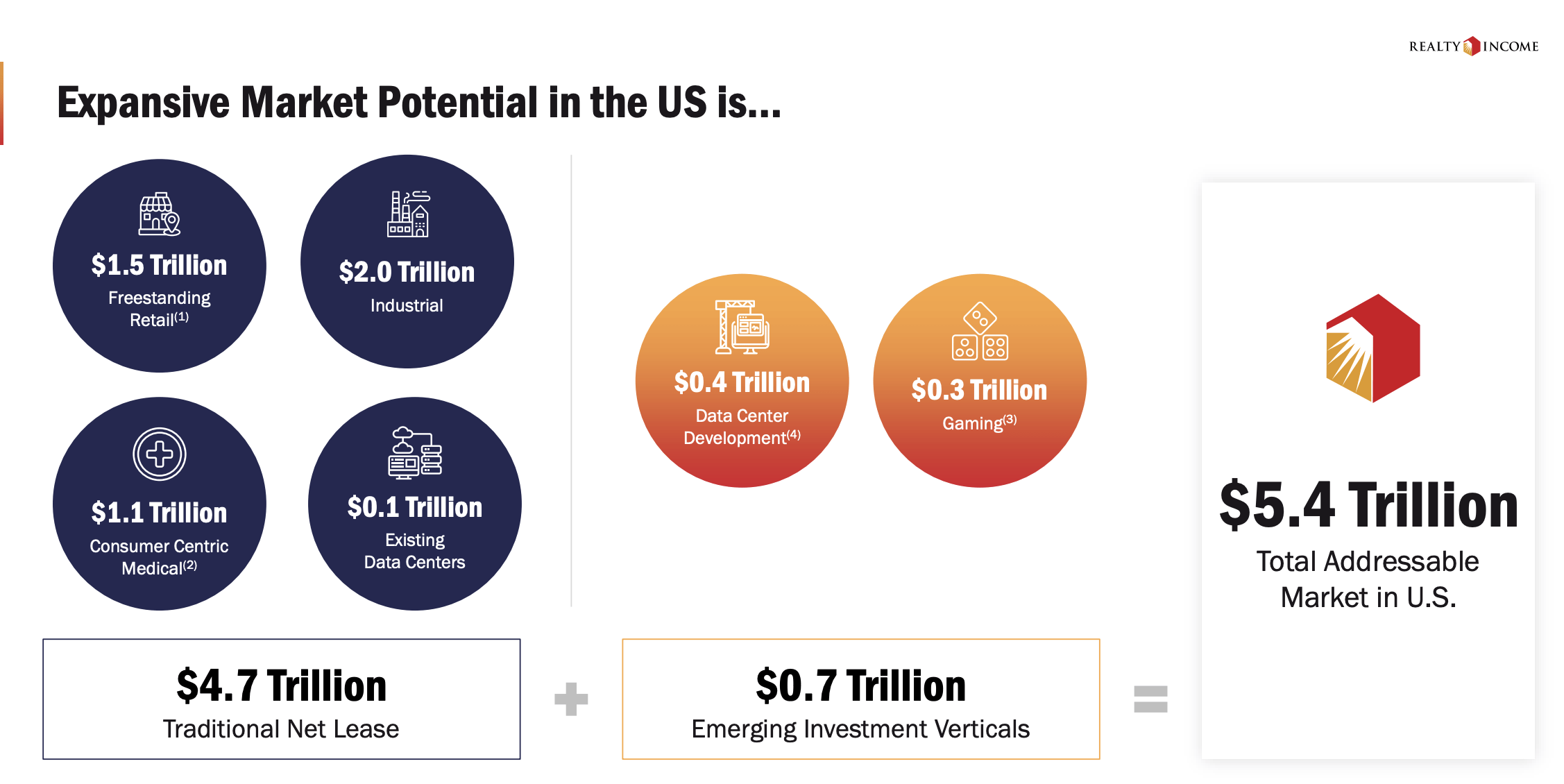

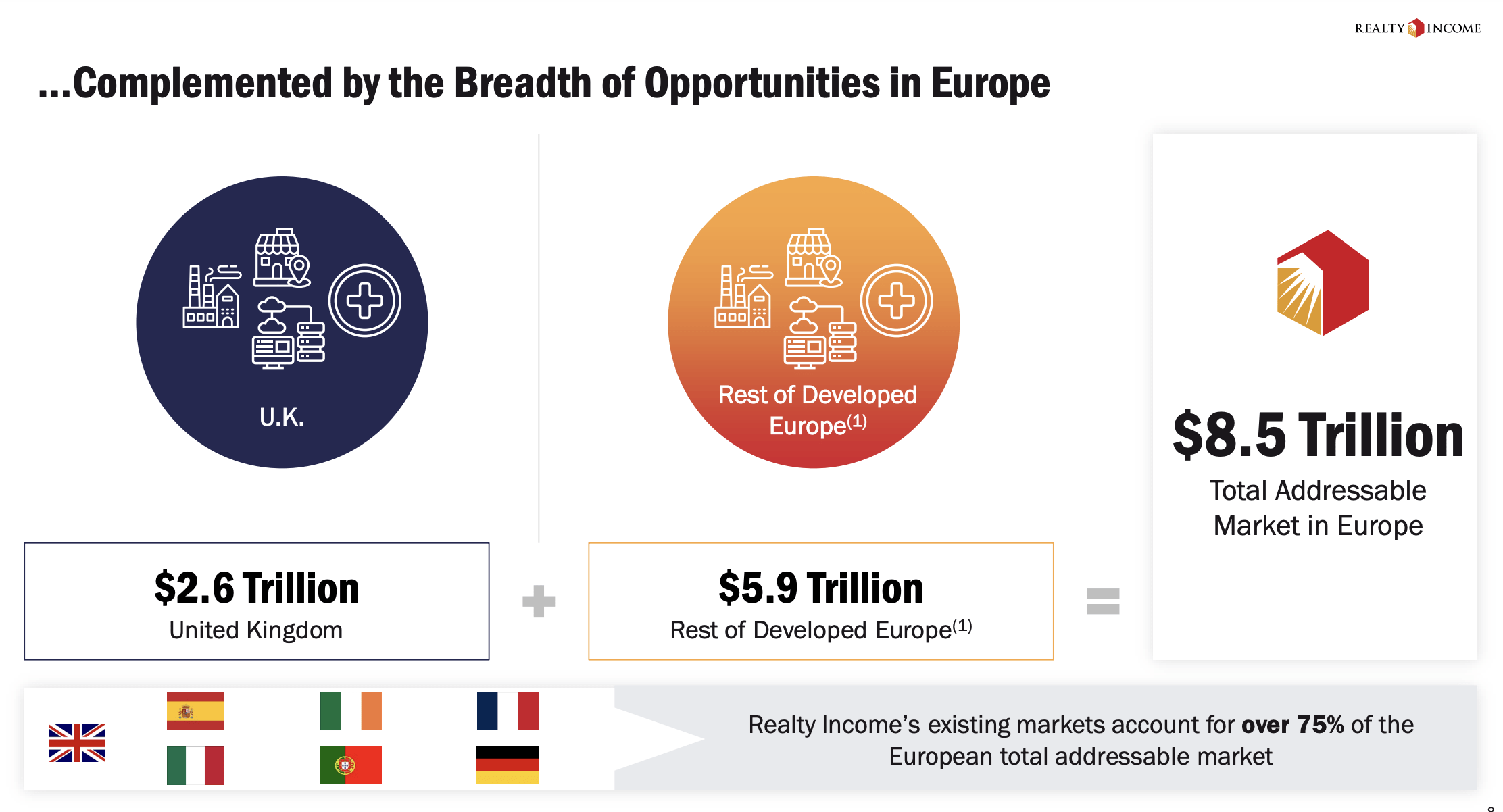

In addition to being attractively priced, Realty Income also has a lot going for it. As large as the company is, its growth potential is truly massive. But don't take my word for it. Management has even provided a great deal of insight into just how large this market potential is. In the US alone, the net lease market that Realty Income focuses on is estimated to be worth about $5.4 trillion. This dwarfs the $210 billion in estimated enterprise value of the publicly traded net lease REITs that are out there. In Europe, the opportunity is even larger than that at roughly $8.5 trillion. Some of the more interesting growth categories that the company is focusing on when it comes to the US market would be gaming, which is estimated to be worth around $300 billion, and data center development, which is estimated to be worth around $400 billion. This still pales in comparison to more traditional opportunities like the $1.5 trillion that exists in freestanding retail and the $2 trillion in industrial opportunities.

Realty Income

When it comes to the European market, a big emphasis is placed on the UK. It, in particular, has a disproportionate share of the net lease opportunities, with an estimated value of $2.6 trillion. That leaves another $5.9 trillion, however, for the rest of the developed nations on the continent. This list includes Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Poland, Portugal, Spain, Sweden, and Switzerland.

Realty Income

Management is also open to other interesting opportunities. It has been focusing, for instance, on the $1.6 trillion of corporate sale lease back potential that exists amongst S&P 500 companies. The firm believes that the $1.5 trillion or so in debt that comes to maturity at those companies between 2024 and 2028, especially if interest rates remain high, will prompt many of them to look to offload their real estate assets. But there are other interesting initiatives as well. One of these is the joint venture that Realty Income entered into with Digital Realty Trust (DLR) dedicated to the aforementioned data center opportunity. And another involves the sale leaseback transaction that the company locked in with Decathlon, a global leader in retail sporting goods that resulted in Realty Income picking up 82 retail properties spread across five different countries in exchange for €527 million.

Realty Income

Fundamentally speaking, Realty Income has never been larger and has likely never been healthier than it is today. Shares look attractively priced at this point in time and the company is operating in a market that has significantly more potential for growth than most might imagine. Alternately, when you combine these factors, it's difficult to be anything other than bullish about the business. And because of that, I've decided to keep it rated a ‘buy’ for now, even as shares have underperformed the market over the past few months.