Nemes Laszlo/iStock via Getty Images

Nemes Laszlo/iStock via Getty Images

The science of today is the technology of tomorrow. - Edward Teller

Today, we put Arcus Biosciences, Inc. (NYSE:RCUS) in the spotlight. The company was recently in the news after drug giant Gilead Sciences (GILD) paid just over $300 million to up its stake in this developmental firm to 33%, paying some $21 a share to do so. Gilead upped its members on the board of Arcus from two to three. However, the shares are trading approximately 25% under what Gilead just paid to increase its holdings in Arcus. Is an opportunity for investors to get the stock at a discount? An analysis follows below.

Seeking Alpha

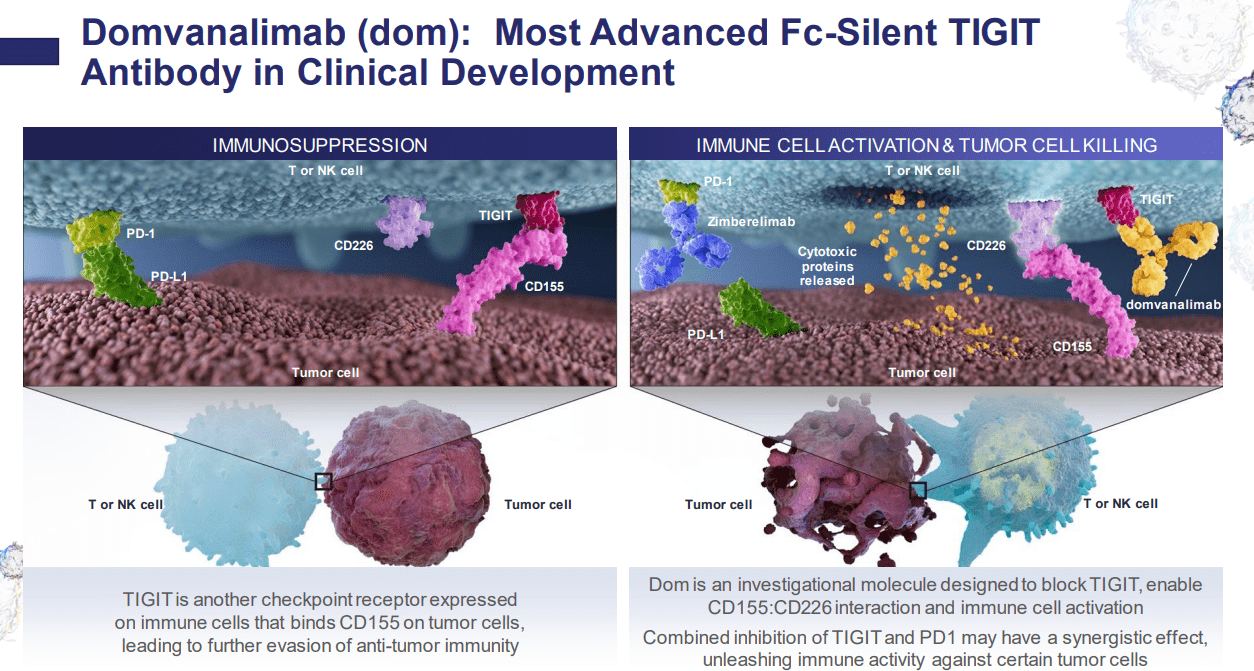

Arcus Biosciences, Inc. is headquartered just outside of San Francisco in Hayward, CA. The clinical-stage biopharmaceutical concern is focused on developing and commercializing cancer therapies. The company's lead product candidate is called Domvanalimab, which is an anti-TIGIT investigational monoclonal antibody.

January Company Presentation

It has several other compounds in development as well. The stock currently trades just north of $16.00 a share and sports an approximate market capitalization of $1.5 billion.

January Company Presentation

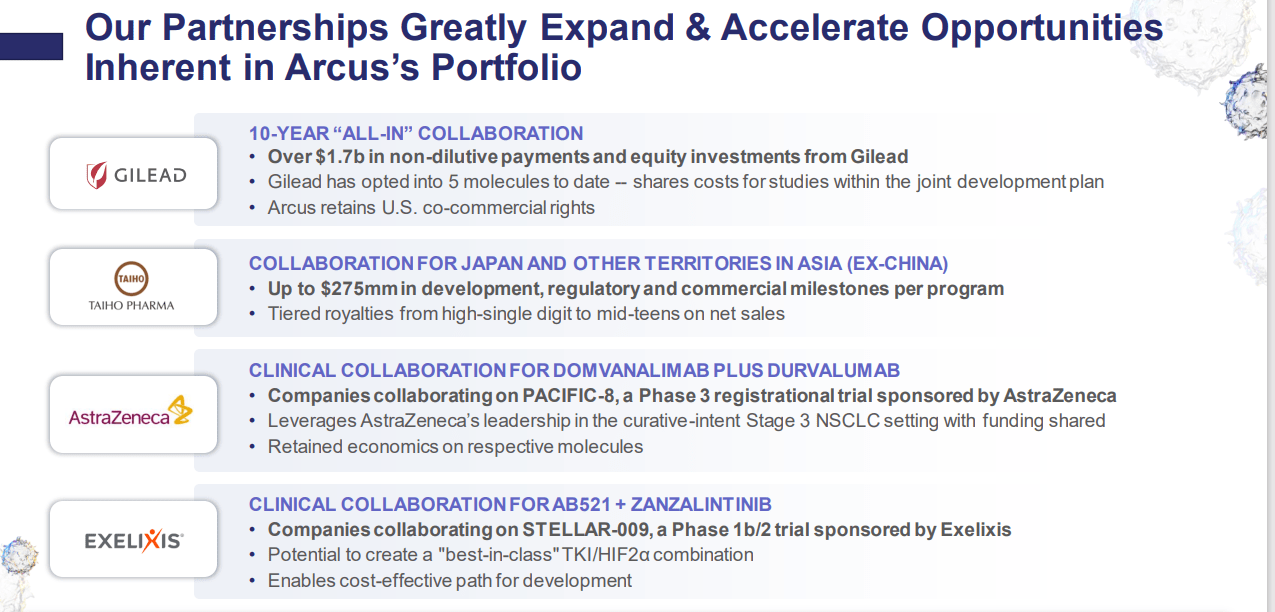

The recent additional funding/equity investment from Gilead is not surprising as it just part of approximately $1.7 billion Arcus has received from the drug giant in recent years. It is also just one of several developmental partnerships Arcus has with larger pharma concerns. Arcus recognized some $117 million in revenue from these partnerships in FY2023 up from $112 million in FY2022. The company also gets reimbursed for significant trial expenses through these partnerships (more on that in a later section).

January Company Presentation

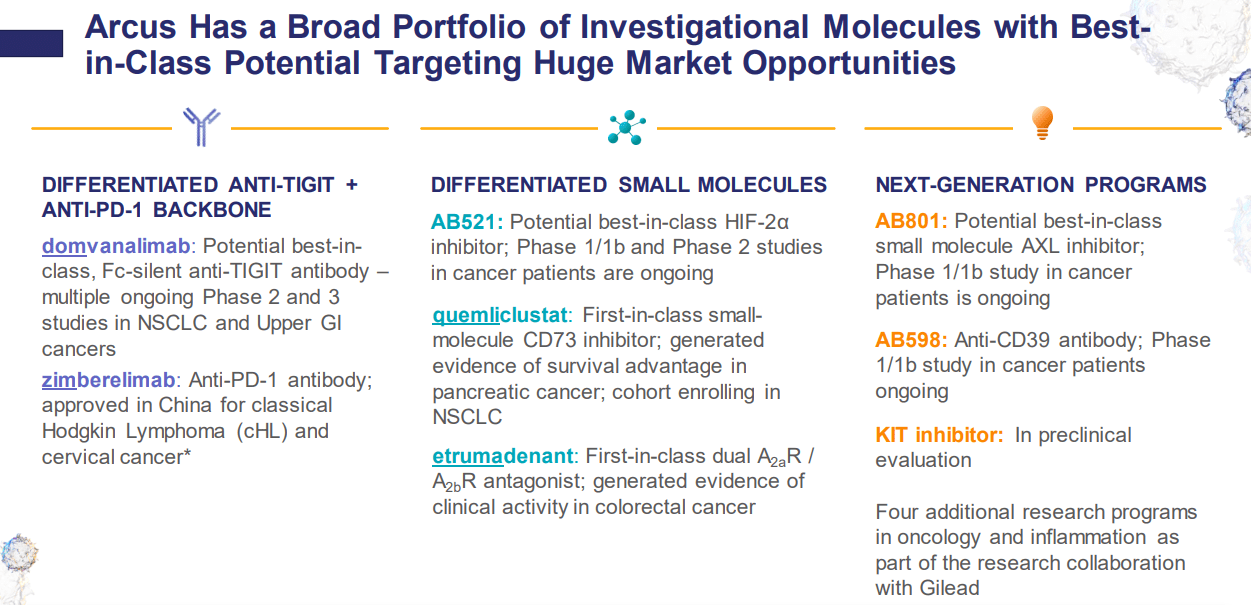

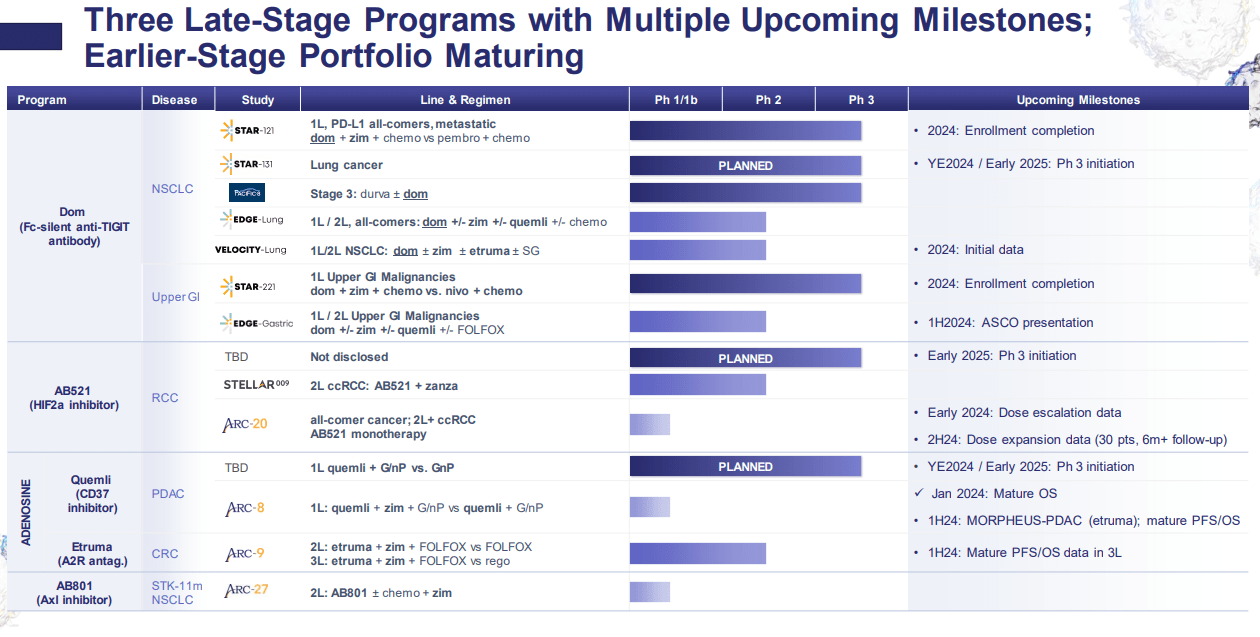

This has allowed the company to build a diverse and large pipeline with three late-stage programs.

January Company Presentation

This is led by the development of Domvanalimab which is currently being evaluated in a half dozen Phase 2 and Phase 3 studies to treat NSCLC and upper GI cancers. Most of these are within a combination therapy with its in-house anti-PD-1 antibody called zimberelimab. If any of these are successful, this could lead to a large potential market.

January Company Presentation

Arcus is also developing Quemliclustat, which is a highly selective and potent small molecule CD73 inhibitor. Quemliclustat has demonstrated encouraging mid-stage data to treat pancreatic cancer. This compound is partnered with Gilead and a Phase 1b study should good results, that were disclosed in January. The company is in the process of setting a pivotal phase 3 study against this indication.

January Company Presentation January Company Presentation

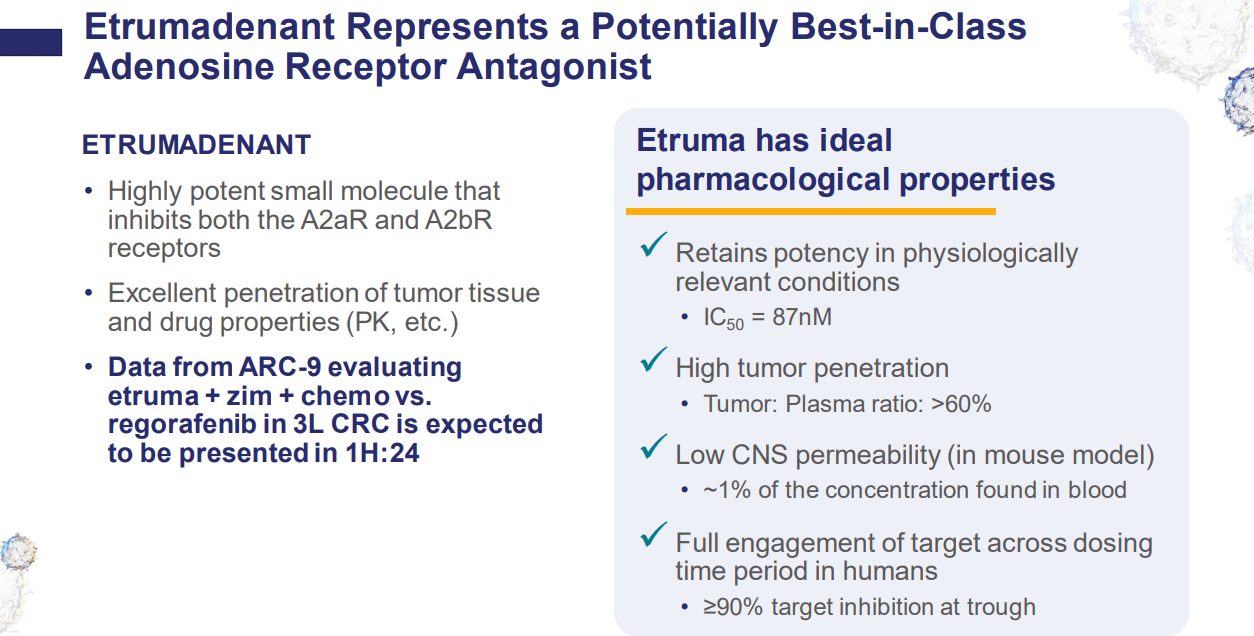

Arcus Biosciences is also pursuing development of an adenosine receptor antagonist called Etrumadenant to treat colorectal cancer within a combination therapy. The company has some other earlier stage compounds in development that will not be germane to this analysis.

January Company Presentation

Since Arcus posted its Q3 numbers on November 7th, eight analyst firms including BTIG, Barclays and Wedbush have reiterated/assigned Buy/Outperform ratings on ACUS. Price targets proffered range from $30 to $70 a share. Bank of America maintained its Hold rating and $25 price target on ACUS.

Approximately 12% of the outstanding float in the shares is currently held short. Company insiders sold approximately $2.5 million worth of shares collectively in 2023. So far in 2024, they have disposed of just over $180,000 worth of equity. Arcus ended the third quarter with approximately $950 million in cash and marketable securities on its balance sheet, providing funding for all planned activities into 2026.

The boost from Gilead pushed pro-forma cash to approximately $1.2 billion and funding in place into 2027. On their fourth quarter press release that came out after the bell yesterday, Feb. 21, management stated that Arcus should end the fiscal 2024 with between $850 million to $920 million of cash on hand. The company listed no long-term debt on its third quarter 10-Q.

For the FY2023, Arcus had G&A expenses of $117 million compared to $104 million in FY2024. R&D expenses ran $340 million during the 2023 fiscal year compared to $288 million in FY2022. Of which, $162 million was reimbursed via partnerships in FY2023.

Arcus Biosciences seems a solid 'sum of the parts' investment at current trading levels. To get an even more complete picture of the developmental story at Arcus Biosciences, I suggest the company's recent investor presentation and portfolio update. The company certainly has multiple 'shots on goal', several partnerships with larger drug development concerns, upcoming trial milestones and is quite well-funded. The shares currently trade far under most analyst firm price targets and at a significant discount to what Gilead just paid to own a third of the company. Therefore, I have taken a small position in RCUS via covered call orders pending further developments.

Reality provides us with facts so romantic that imagination itself could add nothing to them. ― Jules Verne