Leon Neal

Leon Neal

Despite reporting an impressive Q4 2023, Roblox Corporation (NYSE:RBLX) is still down 10% YTD. I believe the current valuation is an opportunity to add shares of Roblox, given that bookings are expected to grow at least 20% annually until 2027. While the company expects to report losses for the foreseeable future, the company’s bookings growth has outpaced the growth in developer exchange fees and infrastructure and trust and safety costs for 2 straight quarters for the first time, which is a sign of prudent cost management. Moreover, I expect advertising to represent a major revenue stream for the company, with the potential to add around $1.3 billion in revenues annually. As such, I’m rating Roblox as a strong buy with a price target of $101.13 by the end of 2027.

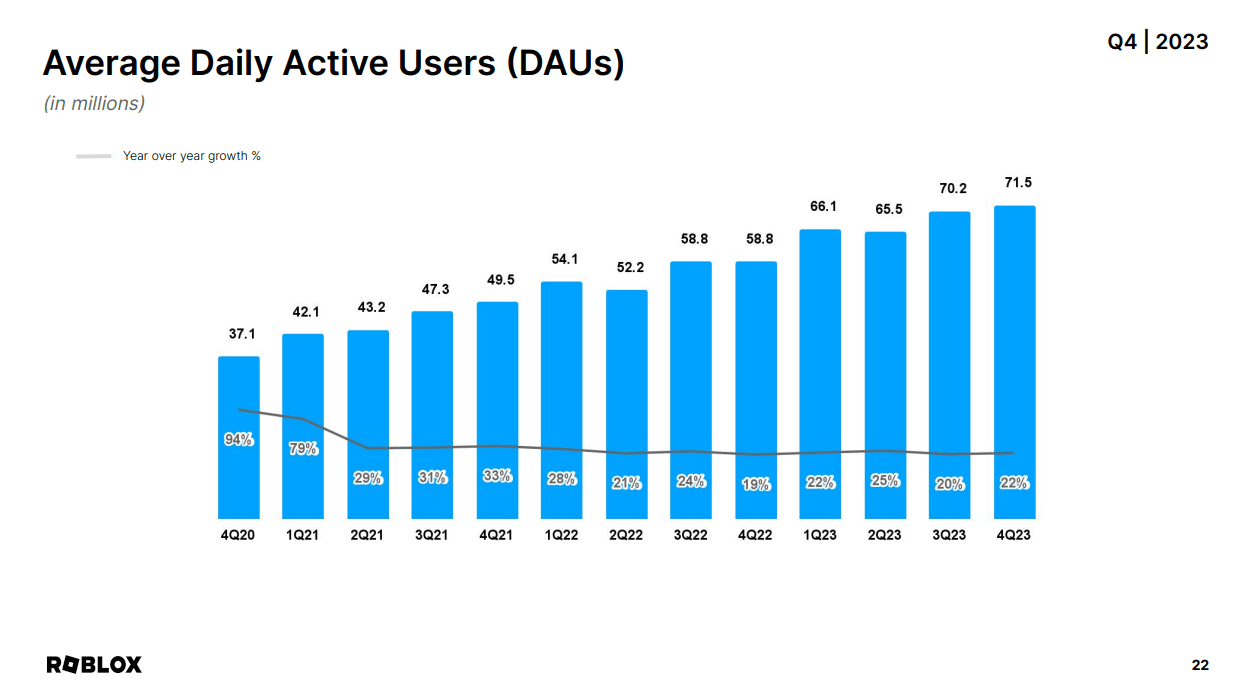

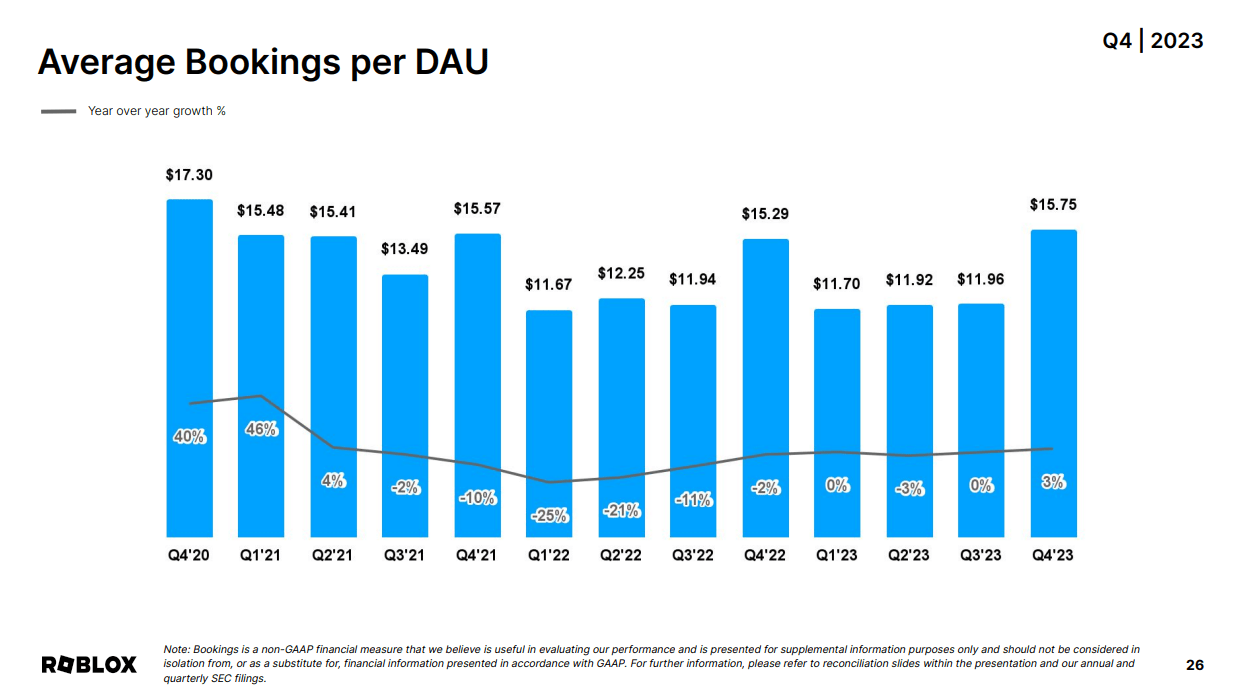

The highlight of Roblox’s Q4 2023 report is the impressive DAU growth of 22% YoY to a record 71.5 million. This DAU growth was accompanied by a 3% YoY increase in average booking per DAU (ABPDAU) to $15.75, its highest since Q4 2020.

Roblox's Q4 Investor Presentations Roblox's Q4 Investor Presentations

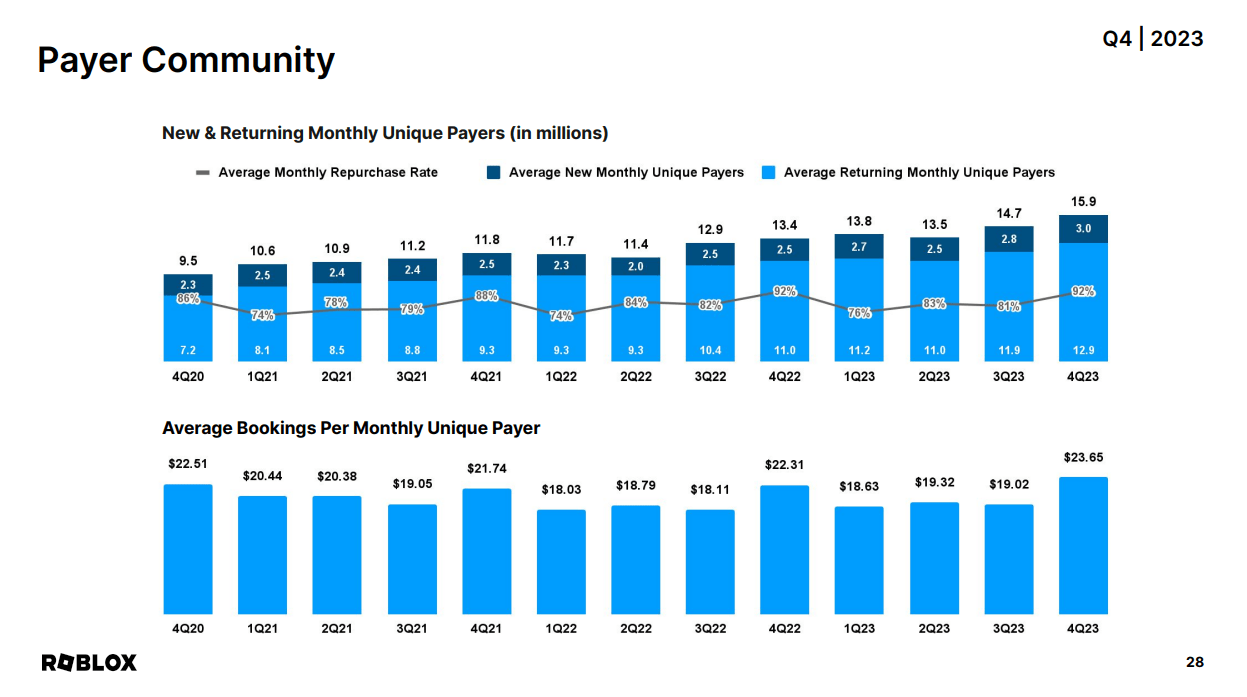

This tells me that the company is successfully monetizing its user base. As is, Roblox’s paying users spent an all-time high $23.65 per month in Q4, a 6% increase YoY.

Roblox's Q4 Investor Presentations

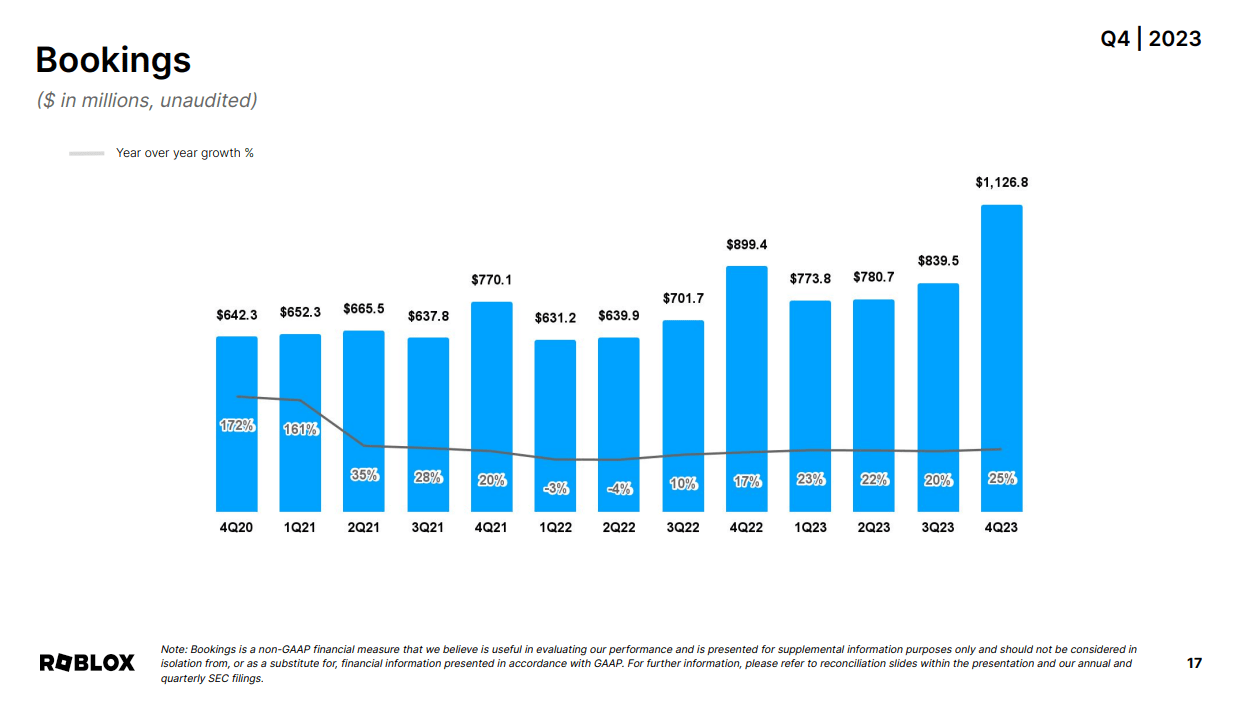

As a result, Roblox’s bookings grew 25.8% in Q4 2023 to $1.1 billion compared to $899.4 million in Q4 2022, the first time bookings topped the $900 million mark in a quarter. Overall, bookings grew 22.6% YoY to a record $3.5 billion in 2023 compared to $2.8 billion in 2022.

Roblox's Q4 Investor Presentations

At the same time, fixed costs of developer exchange fees and infrastructure and trust and safety costs grew at a slower pace than bookings in Q3 2023 and Q4 2023. Those 2 quarters are the only quarters in Roblox’s history where bookings growth outpaced both costs at the same time.

Quarter | Bookings | YoY Growth | Dev Ex Fees | YoY Growth | IT&S | YoY Growth |

Q1 20 | $249,600,000 | $44,499,000 | $52,620,000 | |||

Q2 20 | $494,200,000 | $85,052,000 | $61,853,000 | |||

Q3 20 | $496,500,000 | $85,475,000 | $71,405,000 | |||

Q4 20 | $642,300,000 | $113,714,000 | $78,348,000 | |||

Q1 21 | $652,300,000 | 161.34% | $118,938,000 | 167.28% | $94,136,000 | 78.90% |

Q2 21 | $665,500,000 | 34.66% | $129,714,000 | 52.51% | $108,986,000 | 76.20% |

Q3 21 | $637,800,000 | 28.46% | $129,952,000 | 52.04% | $117,381,000 | 64.39% |

Q4 21 | $770,100,000 | 19.90% | $159,717,000 | 40.46% | $135,995,000 | 73.58% |

Q1 22 | $631,200,000 | -3.23% | $147,122,000 | 23.70% | $141,355,000 | 50.16% |

Q2 22 | $639,900,000 | -3.85% | $143,148,000 | 10.36% | $158,235,000 | 45.19% |

Q3 22 | $701,700,000 | 10.02% | $151,470,000 | 16.56% | $190,986,000 | 62.71% |

Q4 22 | $899,400,000 | 16.79% | $182,115,000 | 14.02% | $198,505,000 | 45.96% |

Q1 23 | $773,800,000 | 22.59% | $182,440,000 | 24.01% | $211,044,000 | 49.30% |

Q2 23 | $780,700,000 | 22.00% | $165,843,000 | 15.85% | $225,039,000 | 42.22% |

Q3 23 | $839,500,000 | 19.64% | $170,719,000 | 12.71% | $218,968,000 | 14.65% |

Q4 23 | $1,126,800,000 | 25.28% | $221,750,000 | 21.76% | $223,310,000 | 12.50% |

*Author compilation from earnings reports.

This is significant since both costs are fixed costs, which Roblox can’t do business without them. As a result, they eat up a significant portion of the company’s gross profit which is why Roblox continues to report large losses despite improving its topline.

This makes me bullish on Roblox’s outlook, given that management reiterated their target of bookings growth of 20% annually until 2027 and expanding margins by 100 to 300 basis points each year by managing growth in fixed costs.

This has been evident in developer exchange fees being flat YoY as a percentage of bookings at around 21%. Infrastructure and trust and safety costs were also flat YoY as they represented 24% of bookings in 2022 and 25% of bookings in 2023.

Quarter | Bookings | Dev Ex Fees | % of Bookings | IT&S | % of Bookings |

Q1 20 | $249,600,000 | $44,499,000 | 17.83% | $52,620,000 | 21.08% |

Q2 20 | $494,200,000 | $85,052,000 | 17.21% | $61,853,000 | 12.52% |

Q3 20 | $496,500,000 | $85,475,000 | 17.22% | $71,405,000 | 14.38% |

Q4 20 | $642,300,000 | $113,714,000 | 17.70% | $78,348,000 | 12.20% |

Q1 21 | $652,300,000 | $118,938,000 | 18.23% | $94,136,000 | 14.43% |

Q2 21 | $665,500,000 | $129,714,000 | 19.49% | $108,986,000 | 16.38% |

Q3 21 | $637,800,000 | $129,952,000 | 20.38% | $117,381,000 | 18.40% |

Q4 21 | $770,100,000 | $159,717,000 | 20.74% | $135,995,000 | 17.66% |

Q1 22 | $631,200,000 | $147,122,000 | 23.31% | $141,355,000 | 22.39% |

Q2 22 | $639,900,000 | $143,148,000 | 22.37% | $158,235,000 | 24.73% |

Q3 22 | $701,700,000 | $151,470,000 | 21.59% | $190,986,000 | 27.22% |

Q4 22 | $899,400,000 | $182,115,000 | 20.25% | $198,505,000 | 22.07% |

Q1 23 | $773,800,000 | $182,440,000 | 23.58% | $211,044,000 | 27.27% |

Q2 23 | $780,700,000 | $165,843,000 | 21.24% | $225,039,000 | 28.83% |

Q3 23 | $839,500,000 | $170,719,000 | 20.34% | $218,968,000 | 26.08% |

Q4 23 | $1,126,800,000 | $221,750,000 | 19.68% | $223,310,000 | 19.82% |

*Author compilation from earnings reports.

With that in mind, Roblox stated in its 2023 annual report that it intends to increase its developer earnings and expects to increase the dollar amount of its infrastructure and trust and safety costs. However, with the expected bookings growth in the coming years, these costs should decrease as a percentage of bookings, which will be key to Roblox’s profitability in the future.

Another reason I’m bullish on Roblox is its venture into advertising, which I believe will be a major revenue stream in the future. This is mainly due to the impressive DAU growth in the over 13 age cohort, which represented an all-time high 58% of total DAUs in Q4 2023. With that in mind, North American users typically have much higher ARPUs in terms of social media advertising compared to other geographies. Assuming the percentage of the over 13 age cohort is similar across geographies, Roblox core ad market would be just more than 9 million users, or 12.6% of Roblox’s DAUs.

While that may seem like a small market, it could substantially boost Roblox’s revenues and act as a major revenue stream in the future. In 2020, the average Facebook user clicked at least 12 ads per month. If we assume a similar rate to Roblox, the platform could generate more than 1.3 billion clicks per year.

With that in mind, the average cost per click of social media ads can range from $0.38 to $5.26 per click. Assuming Roblox charges $1 per click, it could generate more than $1.3 billion in ad revenue per year without taking into consideration any future growth in the above 13 age cohort. This would also boost Roblox’s margins due to the high margins of ad revenues, which should improve its profitability prospects in the future. That said, the company’s ad segment is still in its early stages as the company is currently working with 69 brands, with plans to scale up this year, per the Q4 earnings call.

Given that Roblox is a growth company, I believe looking at its future bookings is a good way to value the company. Based on management’s target of 20% annual bookings growth until 2027, we can project the company’s bookings as follows.

Year | Bookings | Growth Rate |

2023 | $3,520,800,000 | |

2024 | $4,224,960,000 | 20% |

2025 | $5,069,952,000 | 20% |

2026 | $6,083,942,400 | 20% |

2027 | $7,300,730,880 | 20% |

As such, Roblox is trading at the following P/Bookings ratios.

Year | Bookings | P/Bookings |

2024 | $4,224,960,000 | 6.04 |

2025 | $5,069,952,000 | 5.03 |

2026 | $6,083,942,400 | 4.19 |

2027 | $7,300,730,880 | 3.49 |

I believe such growth in bookings would justify a 10 P/Bookings multiple. However, it should be noted that stock-based compensation has resulted in significant dilution to shareholders as the company’s shares outstanding increased by 18.7 million from 2021 to 2022 and 26.5 million from 2022 to 2023. As such, my price targets for Roblox will be based on an average increase of 22.6 million shares per year until 2027.

Year | OS | Increase |

2021 | 585,878,000 | |

2022 | 604,674,000 | 18,796,000 |

2023 | 631,221,000 | 26,547,000 |

2024 | 653,892,500 | 22,671,500 |

2025 | 676,564,000 | 22,671,500 |

2026 | 699,235,500 | 22,671,500 |

2027 | 721,907,000 | 22,671,500 |

Based on my projections for Roblox’s outstanding shares, my price targets for the stock are as follows.

Year | Bookings | P/Bookings | Price Target | Upside |

2024 | $4,224,960,000 | 6.04 | $64.61 | 60% |

2025 | $5,069,952,000 | 5.03 | $74.94 | 86% |

2026 | $6,083,942,400 | 4.19 | $87.01 | 115% |

2027 | $7,300,730,880 | 3.49 | $101.13 | 150% |

That said, these projections could be conservative as they don’t take into account the potential growth in the advertising segment.

Since DAU growth is at the core of my bullish thesis on Roblox, a risk to consider is a potential TikTok ban in the US, as the House recently passed a bill that would force ByteDance to sell its US operations of TikTok or face a nationwide ban on the app. As is, TikTok is a main platform for developers to promote their Roblox games and banning the social media platform would eliminate this promotion channel, making it harder for creators to attract new players to the Roblox platform.

Moreover, Roblox is unprofitable and management expects the company to remain that way for the foreseeable future. As such, Roblox’s valuation is highly dependent on speculative aspects such as potential bookings growth and advertising revenues, so any change in investor sentiment could cause the stock’s value to decline.

Given Roblox’s record bookings and management’s expectations of growing bookings by 20% annually until 2027, I’m rating the stock as a strong buy. The expected increase in bookings could improve Roblox’s profitability prospects in the future, as fixed costs like developer exchange fees and infrastructure and safety and trust costs should represent a lower percentage of total bookings. Moreover, I expect advertising to represent a major revenue stream in the future, with the potential to generate $1.3 billion annually. Considering the high margins of ad revenue, this segment should boost Roblox’s profitability prospects. In light of Roblox’s anticipated bookings growth, I believe a 10 price to bookings multiple would be justified, which is why my price target for Roblox is $101.13 by the end of 2027.