RBC Bearings Incorporated Just Missed EPS By 17%: Here's What Analysts Think Will Happen Next

Last week, you might have seen that RBC Bearings Incorporated (NYSE:RBC) released its third-quarter result to the market. The early response was not positive, with shares down 3.5% to US$266 in the past week. It was not a great result overall. While revenues of US$374m were in line with analyst predictions, earnings were less than expected, missing statutory estimates by 17% to hit US$1.39 per share. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on RBC Bearings after the latest results.

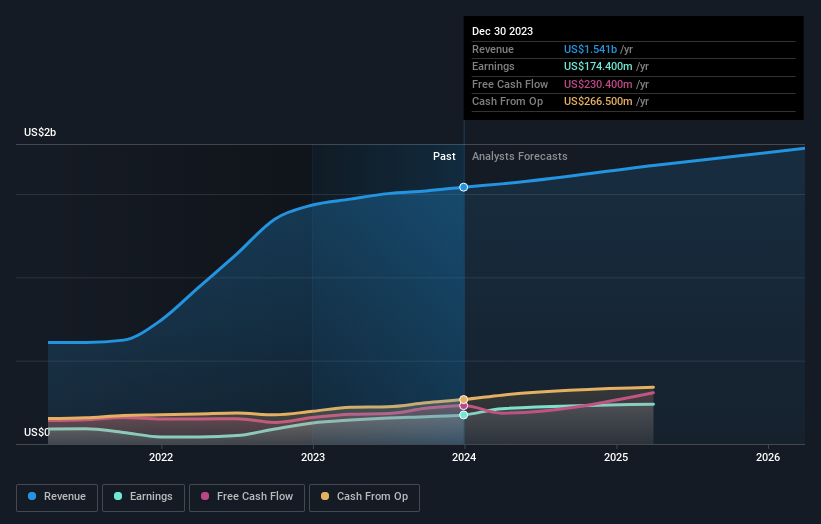

See our latest analysis for RBC Bearings

Taking into account the latest results, the consensus forecast from RBC Bearings' seven analysts is for revenues of US$1.67b in 2025. This reflects a decent 8.5% improvement in revenue compared to the last 12 months. Per-share earnings are expected to bounce 36% to US$8.20. In the lead-up to this report, the analysts had been modelling revenues of US$1.68b and earnings per share (EPS) of US$8.37 in 2025. The analysts seem to have become a little more negative on the business after the latest results, given the minor downgrade to their earnings per share numbers for next year.

It might be a surprise to learn that the consensus price target was broadly unchanged at US$280, with the analysts clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on RBC Bearings, with the most bullish analyst valuing it at US$310 and the most bearish at US$250 per share. The narrow spread of estimates could suggest that the business' future is relatively easy to value, or thatthe analysts have a strong view on its prospects.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that RBC Bearings' revenue growth is expected to slow, with the forecast 6.7% annualised growth rate until the end of 2025 being well below the historical 21% p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 3.3% annually. So it's pretty clear that, while RBC Bearings' revenue growth is expected to slow, it's still expected to grow faster than the industry itself.