Stefan Lenz/iStock via Getty Images

Stefan Lenz/iStock via Getty Images

It will be a big week for the NASDAQ 100 and the broader market in more ways than one. It won't be because the dollar or rates are on the cusp of breaking out. Or due to skyrocketing inflation expectations or the nervousness around the Fed. No, it will be because the company that has delivered nearly 35% of the index's gains this year will be reporting earnings.

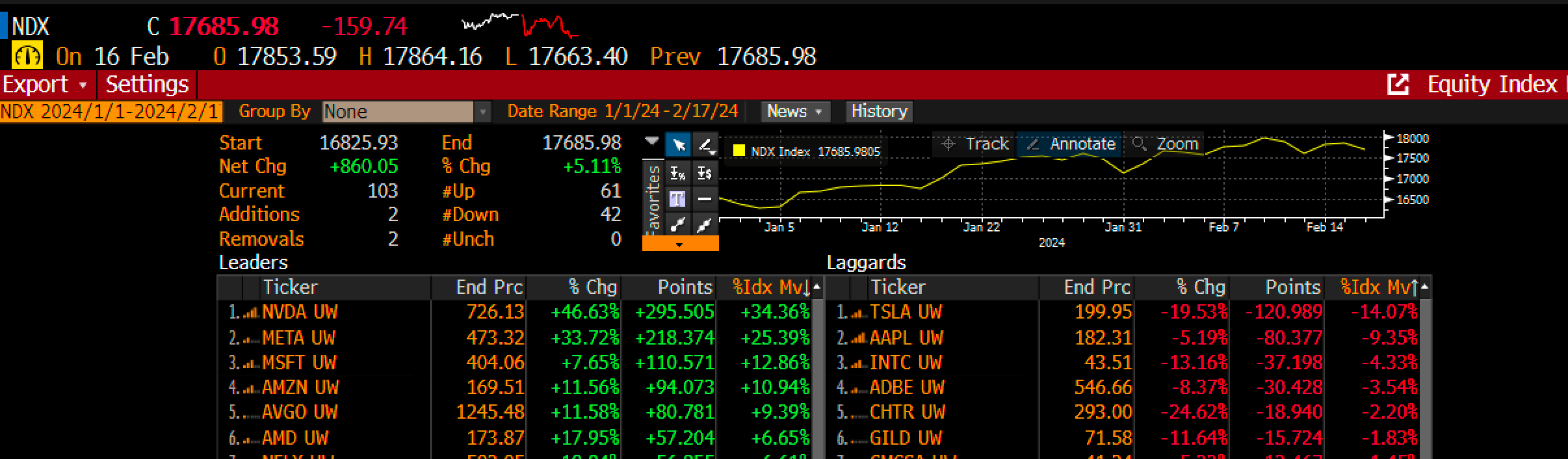

The NASDAQ 100 is up over 5% this year, and the biggest reason is that Nvidia (NVDA) is up over 46% and has delivered 34.4% of the index's gains. That's right, Nvidia alone has delivered 295 points of the 860 points that the Nasdaq 100 has increased by in 2024. The entire fate of where the NASDAQ 100 goes from here may rest on Nvidia's quarterly results and, more importantly, how the market reacts.

Bloomberg

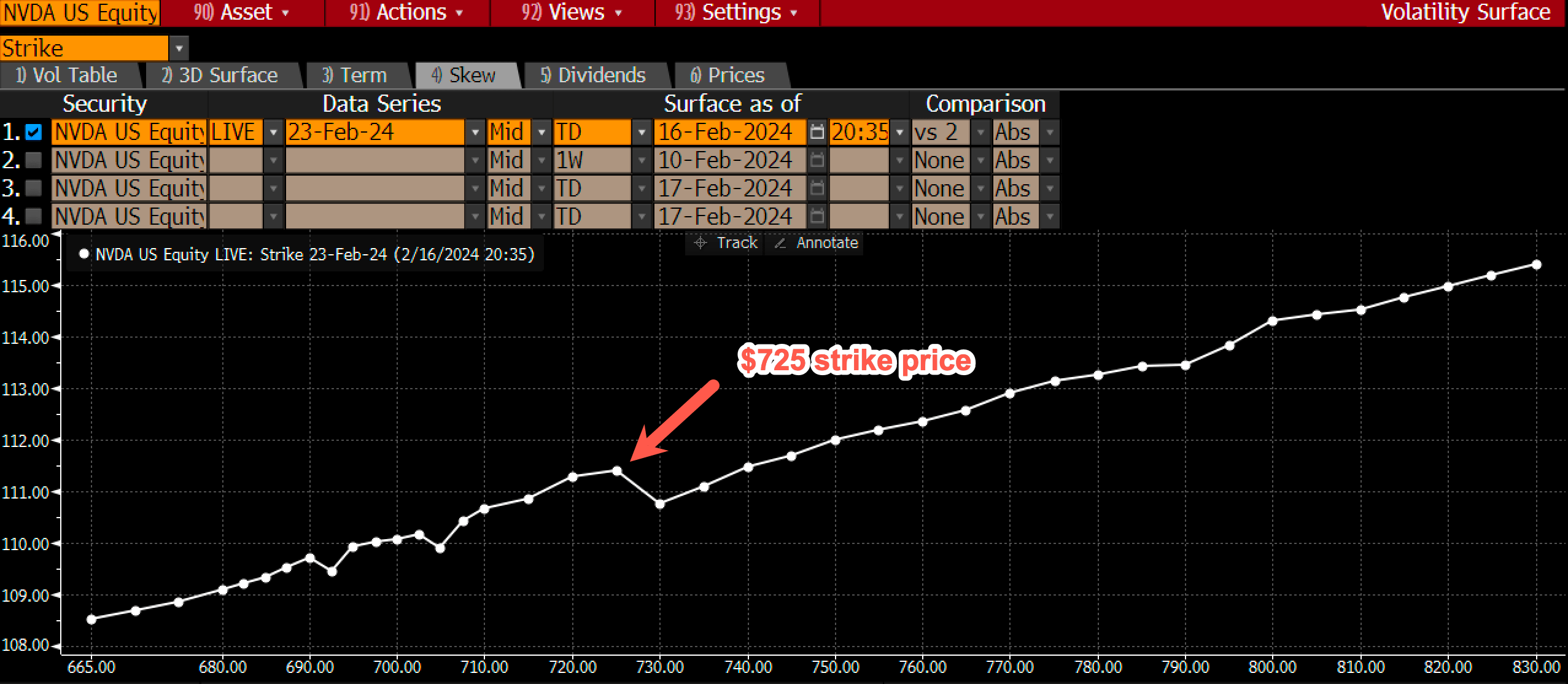

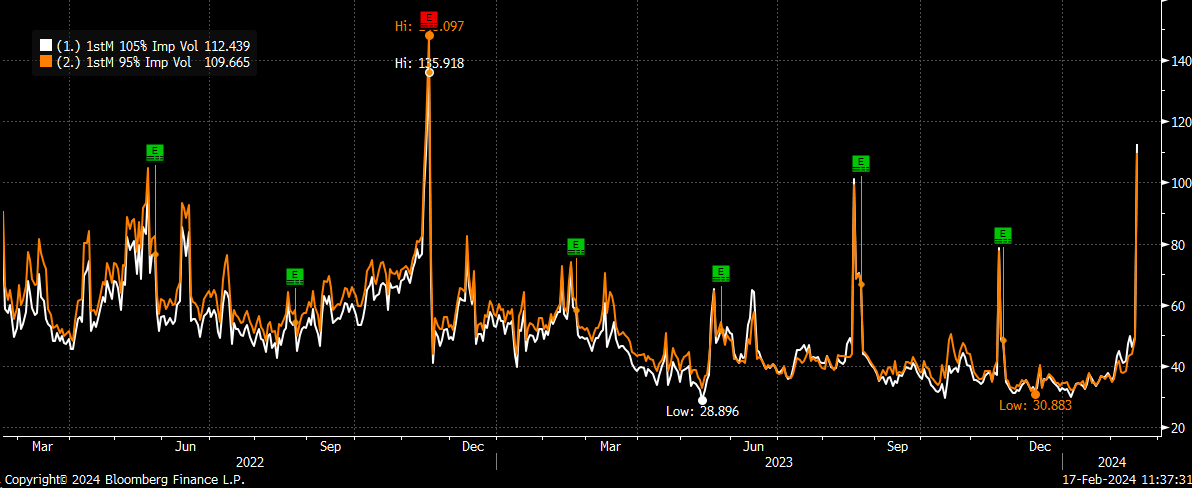

The problem is that the market is so bullish on Nvidia, and the prospects of the stock rising after it reports results that it could almost be considered bearish. The implied volatility for Nvidia at the $725 strike price for expiration on February 23, 2024, is 111%. Worse is that the implied volatility rises as the strike prices rise and falls as the strike prices go lower. It is a sign that investors are very bullish on Nvidia and that the calls are more in demand than the puts.

Bloomberg

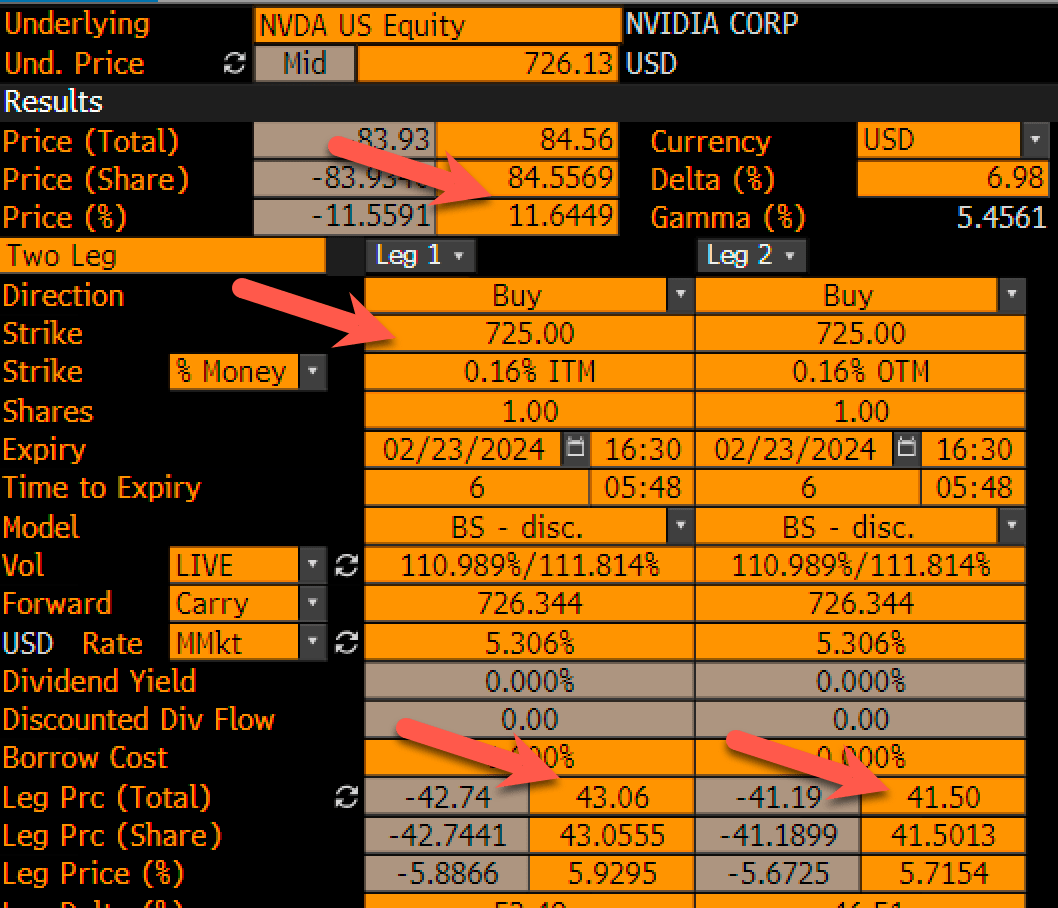

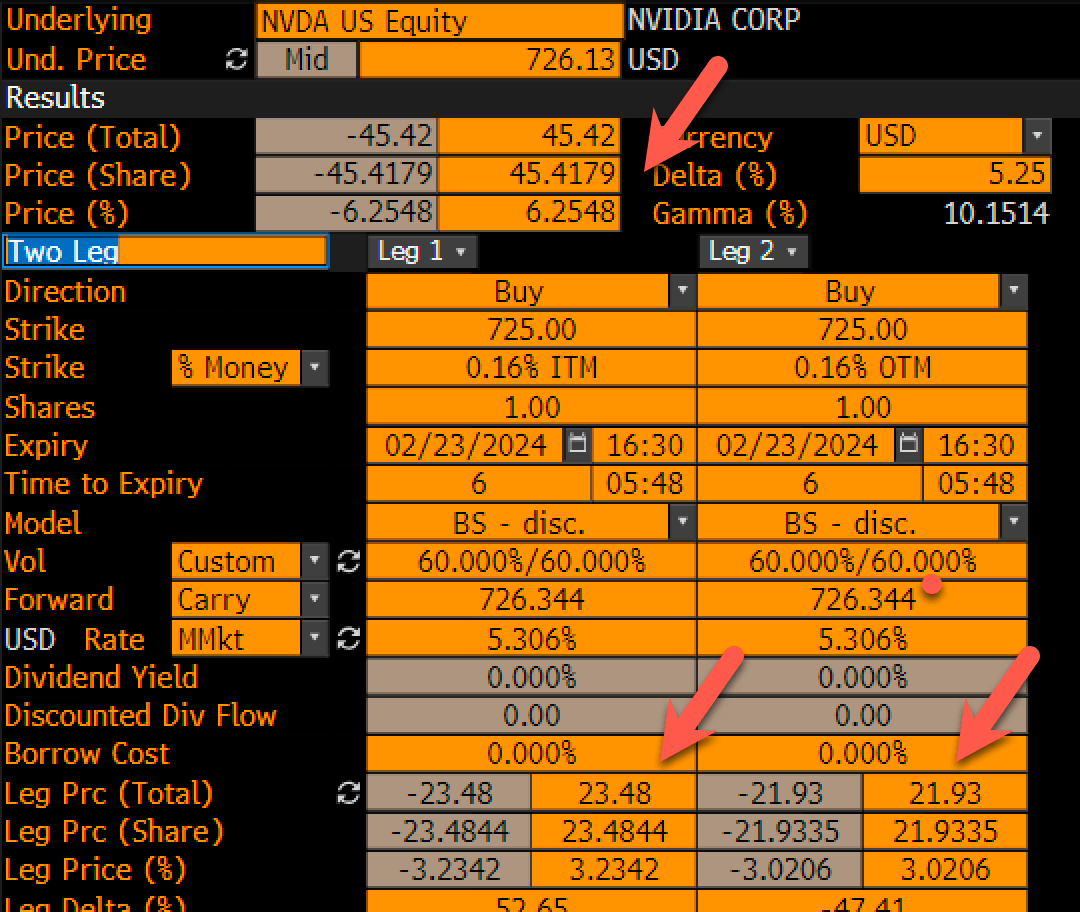

Meanwhile, a long straddle, which is the purchase of a put and call option at the same strike price for the same expiration date, suggests the stock needs to move by 11.6% from the $725 strike price in either direction of the straddle to pay off, which is a massive move for a stock with a nearly $1.8 trillion market cap.

Bloomberg

So not only will the results and, more importantly, the immediate market reaction have a big impact on the NASDAQ 100, but the results will have a bigger impact on the market in the future because much of the hope for earnings growth for the index comes from just one stock, Nvidia.

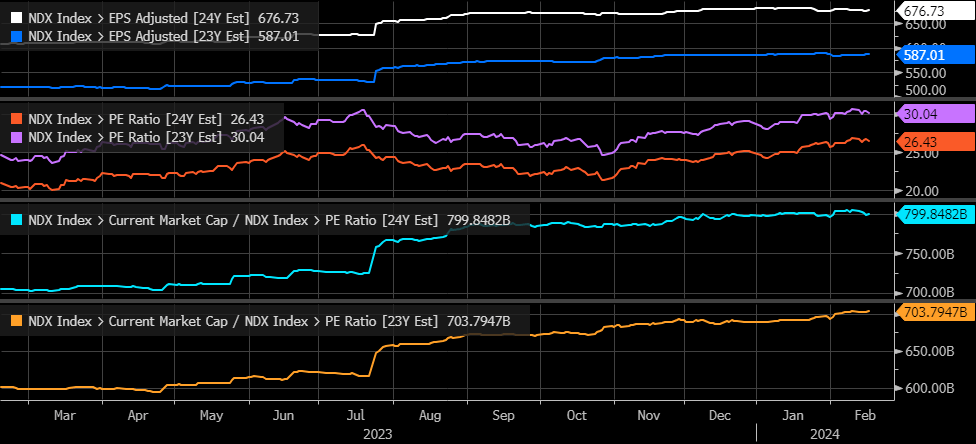

Earnings for the NASDAQ 100 are expected to grow roughly 15% in 2024 to around $675 per share from $585 in 2023. This means, using a back-of-the-envelope approach, that if the Nasdaq is currently trading at 30 times 2023 earnings and 26.5 times earnings estimates and the current market cap of the NASDAQ is about $21 trillion, that Nasdaq should earn about $700 billion in 2023 and almost $800 billion in 2024.

Bloomberg

Meanwhile, Nvidia is expected to grow its earnings from $12.39 in fiscal 2024 to $21.35 in fiscal 2025. Nvidia operates on a fiscal calendar one year ahead of the current calendar, so fiscal year 2024 equals calendar year 2023, and fiscal year 2025 equals calendar year 2024. Assuming that Nvidia has 2.47 billion shares outstanding, that means that Nvidia's earnings will grow by $22.1 billion in calendar 2024, which accounts for roughly 20 to 25% of the NASDAQ 100 entire forecasted earnings growth.

This would suggest that the Nasdaq 100 rally has been predicated on one stock delivering a 1/4 of all of the growth in 2024. This means that if Nvidia should slip or doesn't provide the street with what is expected for some unknown reason when it reports results this week, it won't just be an Nvidia problem but a NASDAQ 100 problem.

So, not only has the options market gone all in on Nvidia, but the entire market has gone all in on Nvidia, whether it realizes it or not. If Nvidia's results and guidance come in as expected because the options market is so heavily weighted to the stock rallying, all those calls will lose value quickly.

Bloomberg

Generally speaking, the IV falls dramatically following results, so the current implied volatility of Nvidia at over 100% is likely to be back in the 40 to 60% range the day after the company reports. Therefore, the value of those calls will go from roughly $42.50 to about $23. The stock must trade around $770 after the results to keep those calls from crashing. Meanwhile, the puts will need the stock to trade down to about $685 to keep the put value from crashing.

Bloomberg

However, there will be a ripple across the options chain because IV is elevated across the entire complex. There is more open call delta than open put delta, meaning market makers will likely have stock to sell once the company reports results. So, if the company doesn't blow out results and deliver a META-like performance, getting this stock moving higher post-results will be tough.

Bloomberg Bloomberg

So Nvidia's results matter greatly because if the company doesn't deliver versus the wildly elevated expectations, it isn't just Nvidia that will suffer; it will take the entire market down with it, or up for that matter.