DKart

DKart

Earlier this quarter, Qorvo (NASDAQ:QRVO) reported results for the third quarter of FY24 and its outlook for next quarter; I'm unconvinced of Qorvo's growth story for 4Q24 and 1HFY25 due to smartphone weakness. I recommend investors take advantage of the stock's current price to explore exit points or trim their exposure.

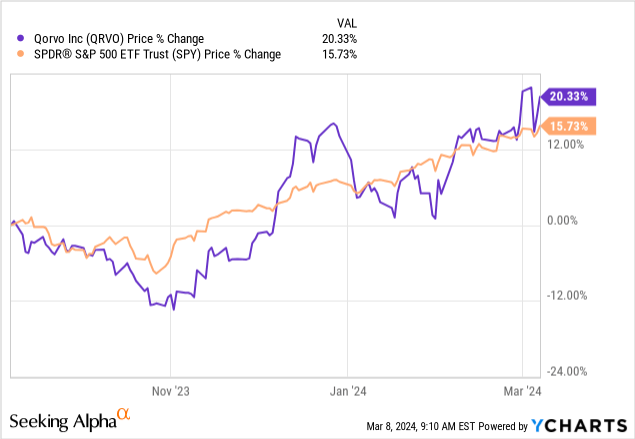

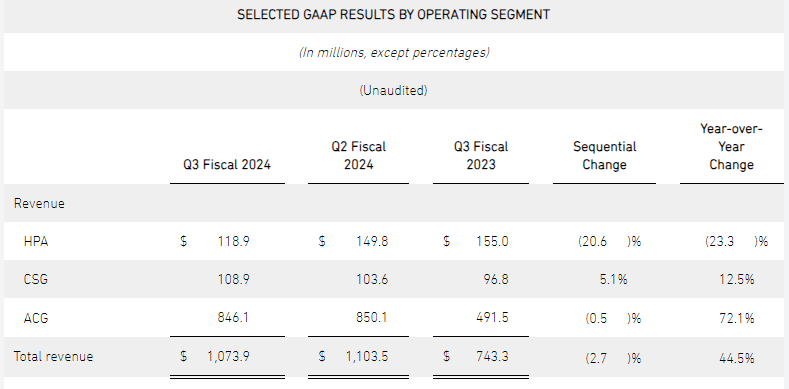

The wireless connectivity chipmaker's stock is up ~20% over the past six months and ~18% over the past three months, outperforming the S&P 500 by ~16% and 12% during the same period (as shown in the graph below). My less optimistic outlook on Qorvo is due to smartphone weakness in 2024. Qorvo is highly exposed to smartphone demand dynamics. The way I see it, the company has three main segments that require our attention: HPA, CSG, and ACG. The company gets its sustenance from its Advanced Cellular Group sales, which came in flat sequentially in the third quarter. ACG sales made up $846M of the total sales of $1,073.9M for the quarter. This translates to roughly 79% of all total sales. I think Qorvo's ACG sales will likely suffer this year due to a lack of smartphone recovery; hence, I would recommend that investors trim their positions substantially before the downside plays out.

YCharts - Seeking Alpha

Semis are trading at all-time highs, but this does not reflect the health of real end demand, and that's where most retail investors can get lost. Qorvo is a great company bringing RF and power tech and solutions "to mobile, infrastructure, the IoT, defense/aerospace and power management markets." Basically, the company "makes radio-frequency chips used in 5G base stations, as well as for cellular and Wi-Fi connectivity in smartphones and other gadgets." My issue with Qorvo in the current environment is its hefty exposure to mobile sales. Not to mention its exposure to IoT (Internet of Things) and power management markets, which are now seeing weakness due to inventory correction cycles.

The company's high-performance analog sales dropped double-digit percentage sequentially by 21% and 23% year-over-year to $119M. I am seeing some positives for the company's connectivity and sensor group, with sales growing slightly by 5% sequentially and 12% year-over-year, but I don't think that's enough reason to be bullish on the stock. I don't believe this growth will be able to offset weakness in Qorvo's core market, ACG. I outline the company's third-quarter results in comparison to 1HFY24 in the image below, taken from Qorvo's press release.

Qorvo press release

The main basis for my concern about Qorvo's ACG sales is Apple (AAPL). Apple is easily Qorvo's largest customer, representing 37% of the company's total sales in FY23. Apple and the broader smartphone market have already been showing signs of trouble and muted end demand for the year, even though management claims inventory correction cycles are mostly over. The IDC's outlook for the smartphone market is mixed, with some analyst reports estimating a low single-digit 2.8% year-over-year growth and others expecting a 0-5% growth, which is very low. Apple sales in China are suffering; Apple's iPhone sales dropped 24% in China, with Counterpoint Research reporting that Apple is facing increased competition with Huawei and local smartphone firms. I think these data points show that smartphone demand remains weak, and it'll be more difficult for Qorvo to outperform as long as its core market and biggest customers suffer.

Aside from Qorvo's exposure to weaker smartphone demand in China through Apple, the company is also exposed to China directly through its geographical sales, as shown in the following graph. I think this is another red flag, given that China is going through a macro slowdown that might not get worse for the semi-players but is showing no near-term sign of getting better.

Qorvo's geopolitical exposure

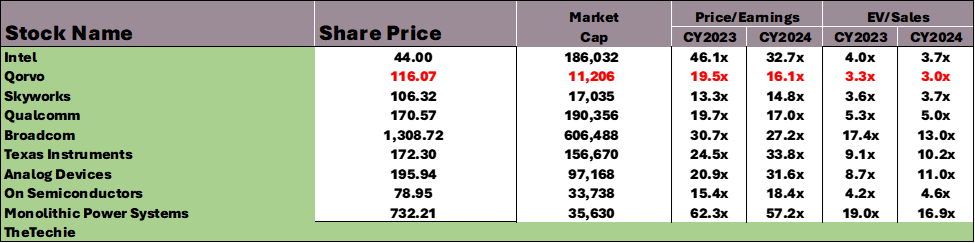

Using a relative methodology of valuing stocks within Qorvo's peer group, the stock is visibly undervalued. Qorvo stock trades at a ratio of 3.0x for CY2024 on an EV/Sales basis. In comparison, the peer group is trading at a ratio of 7.9, as shown in the table below, generated with data from Refinitiv. The stock's P/E ratio also indicates the same undervalued nature. Qorvo's P/E ratio is 16.1x, compared to the group average ratio of 27.6. I understand the attractiveness of Qorvo's valuation, but I don't think it makes up for the fact that the company's main source of revenue is under pressure this year. I don't see a favorable risk-reward scenario for Qorvo in 1H24.

Image created by The Techie with data from Refinitiv

Of course, there's a scenario in which my negative thesis of Qorvo underperforming does not play out, and that is if the smartphone total addressable market rebounds significantly this year, which I don't see happening based on the reasons I highlighted above. I am using Apple as a window into the market to better understand current demand levels. So far, particularly after this week's news of Apple's shrinking sales in China, I stand by my pessimistic outlook for Qorvo. The bulls are arguing that the Android market is seeing an earlier recovery than the iPhone market, and while Qorvo's results do reflect seasonal demand from Android markets, I don't think we're at the infliction point where true demand is there, neither in iPhone nor Android markets. Samsung is also confirming the weaker smartphone end demand, with reports saying, "Samsung expects smartphone demand to drop..." I think that the biggest risk to my bearish sentiment is if the smartphone market recovers ahead of 2025.

I'm not too optimistic about Qorvo's ability to outperform consensus expectations in 2024 because of the weaker smartphone outlook for the year. I think the company is at higher risk as we head deeper into 1H24. Management is now guiding for revenue to drop again sequentially next quarter by 14% to $925M, compared to Street estimates of $913M. I think the weakness is getting priced into the outlook, but I haven't seen it priced into the stock yet. When the smartphone weakness is priced into the stock, that's when I believe Qorvo would provide a more favorable risk-reward scenario. I would recommend investors trim their positions substantially, if not entirely, and explore entry points down the line when the stock is in the high $80s.