Instants

Instants

Quipt Home Medical (NASDAQ:QIPT) is recognized as the 5th largest home medical equipment provider in the United States, serving nearly 300k patients with a focus on clinical respiratory care. The attraction here is the company's acquisitions-based expansion strategy in what remains a highly fragmented market primed for consolidation.

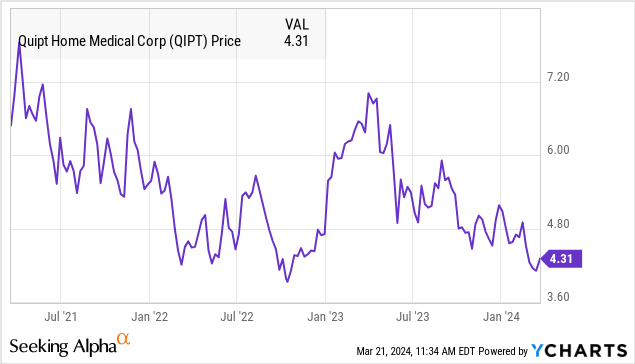

Despite impressive growth in recent years, the stock has struggled to gain momentum amid more volatile earnings. That said, the latest quarterly report was highlighted by improving margins setting the stage for an expected ramp-up in profitability.

While we can keep QIPT in a speculative category considering its micro-cap profile, we are bullish on the stock which appears undervalued and supported by overall solid fundamentals.

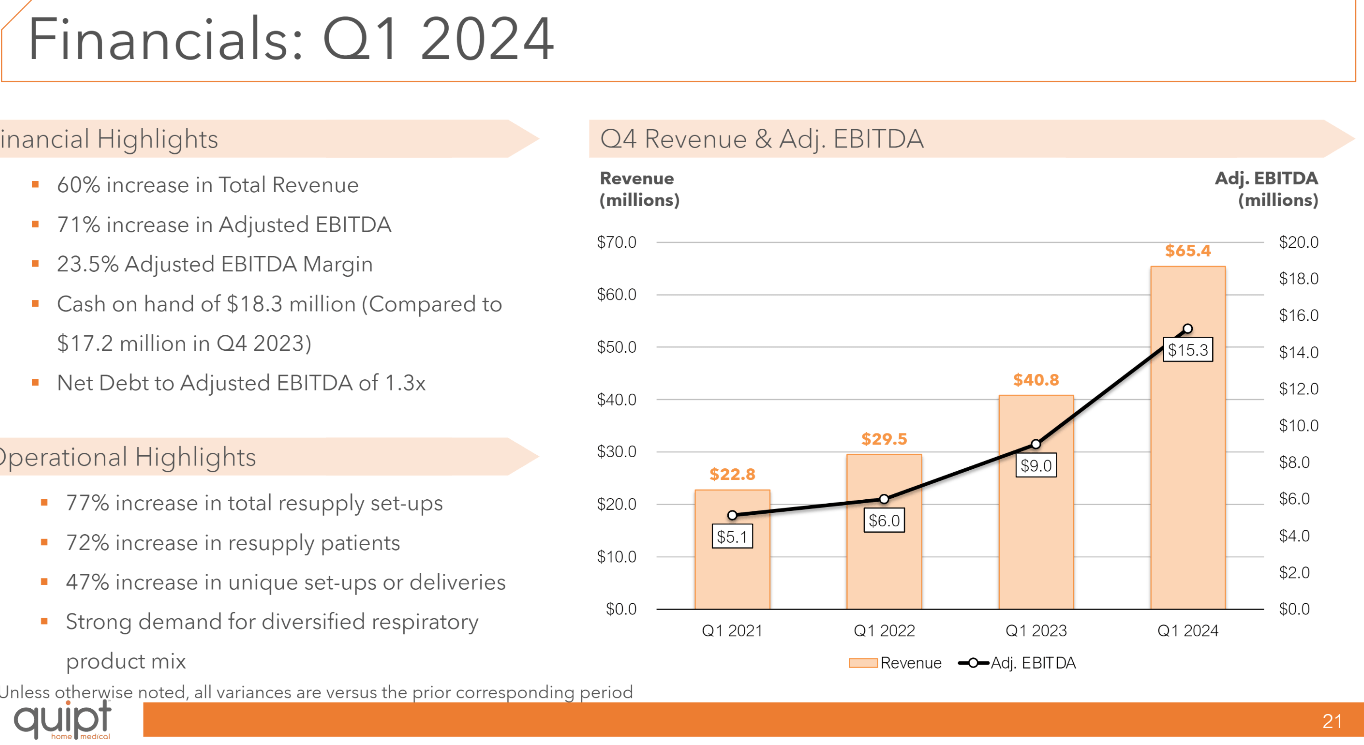

QIPT reported its fiscal 2024 Q1 earnings back in February with an EPS loss of -$0.01, favorably coming in $0.01 ahead of the estimate. Revenue of $65.4 million was 60.3% higher year-over-year and also above expectations.

The context for the top-line strength considers the impact of 19 acquisitions completed in the calendar year 2023. Nevertheless, organic growth was positive with the company citing a 2% sequential increase from Q4 2023.

More favorably, Q1 adjusted EBITDA reached $15.3 million, an increase of 71% y/y better describing the underlying earnings story. In this case, the 23.5% adjusted EBITDA margin climbed from 22.1% in the prior year quarter capturing ongoing operating leverage as the business scales nationally.

source: company IR

The implementation of a unified technology platform for providers to manage orders and maintain records is seen as adding to organization and financial efficiencies.

There is typically a process for integrating home care acquisitions into the ecosystem with an expectation that synergies and cost savings are generated over time. This dynamic provides some visibility for further earnings momentum.

A major operating theme has been efforts at cross-selling and "expanding the continuum of care" where patients being treated with certain products may also onboard into other equipment and consumables within a recurring revenue model. Keep in mind that the primary payers here are private insurance companies along with Medicare and Medicaid.

The company has targeted sales efforts toward areas with a high prevalence of chronic obstructive pulmonary disease "COPD" that can be served with the company's full range of end-to-end respiratory solutions.

source: company IR

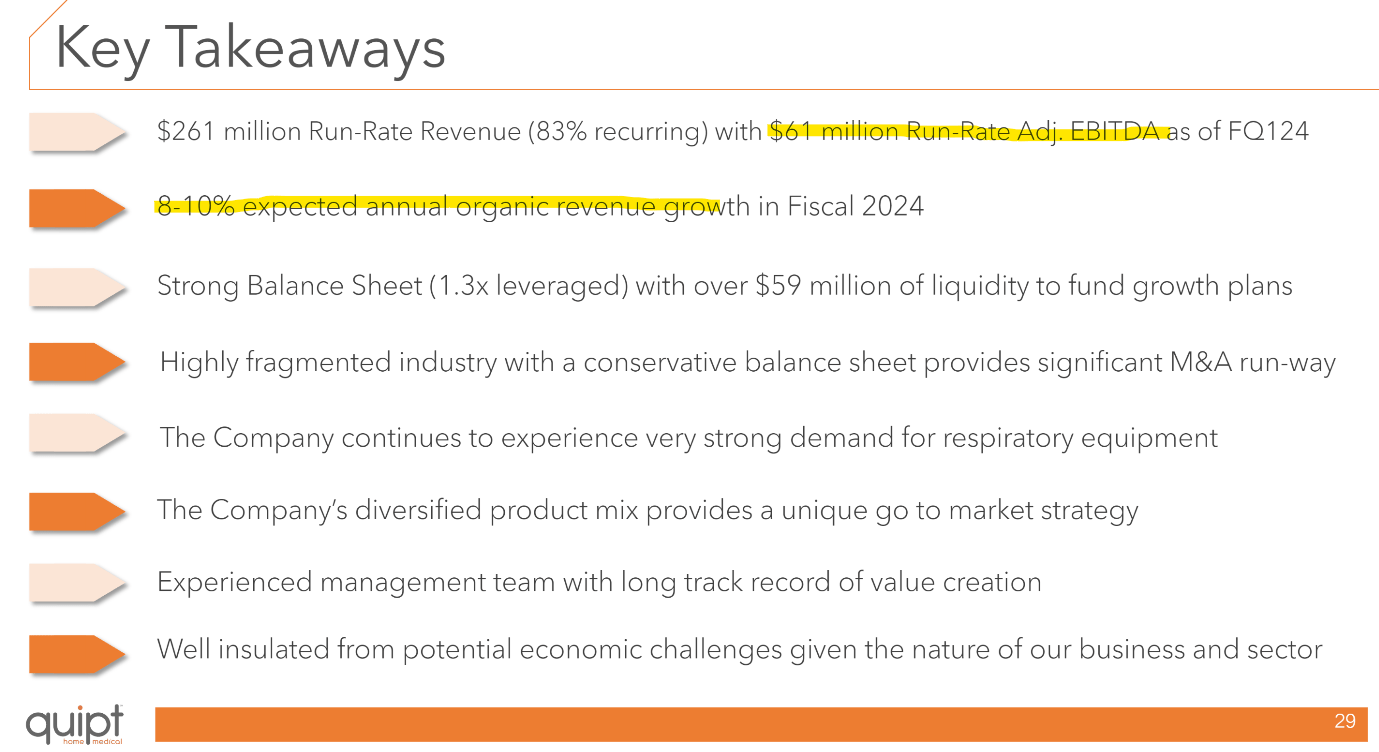

In terms of guidance, Quipt Medical is targeting 8-10% organic annual growth this year while citing its strong balance sheet providing the flexibility for further strategic acquisitions.

The company ended the quarter with $18.3 million in cash and cash equivalents, against $97.6 million in long-term debt. Considering the $61 million run-rate for adjusted EBITDA from the latest quarterly results, a net leverage ratio of 1.3x is stable, in our opinion, with additional liquidity.

source: company IR

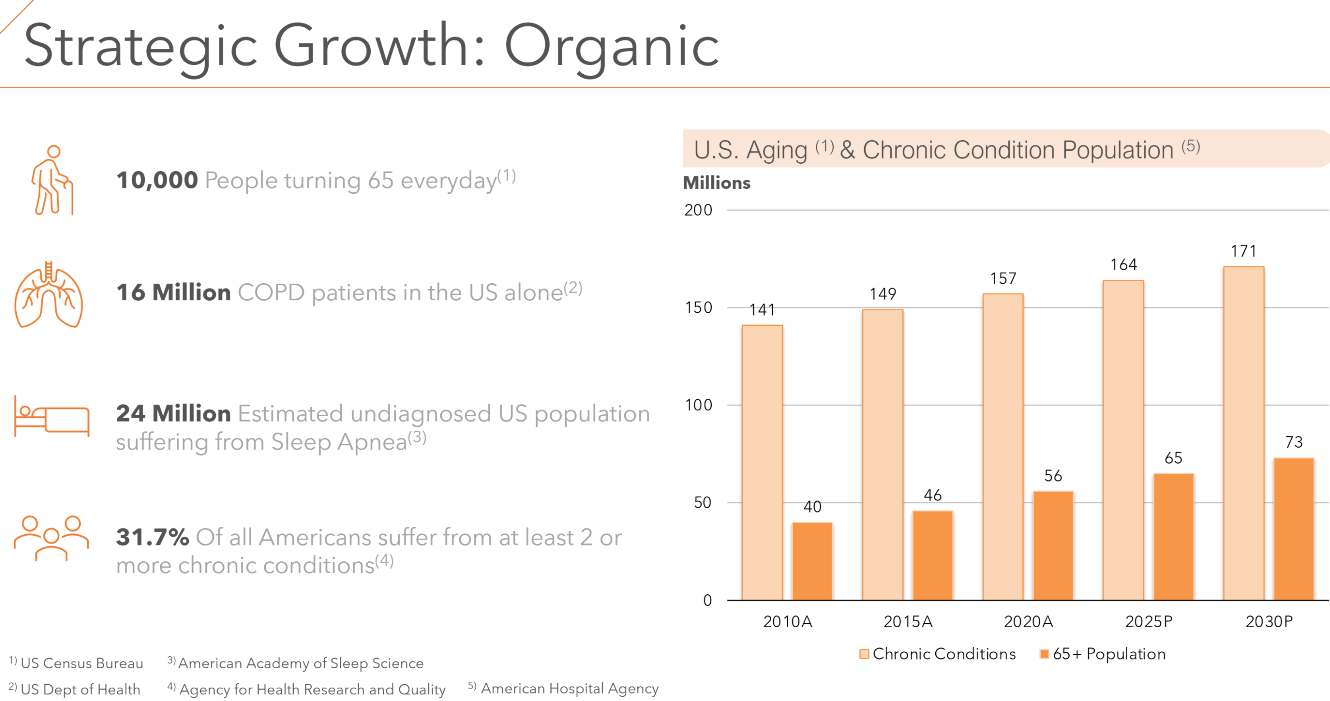

From a high-level perspective, the tailwind for health care and medical supplies starts with what is understood to be an aging U.S. population where chronic conditions become more prevalent.

The addressable market considers an estimated 16 million COPD patients in the U.S. and 24 million people suffering from sleep apnea. The opportunity for Quipt Medical is to continue gaining market share by rolling up smaller players as it enters new states and regions.

source: company IR

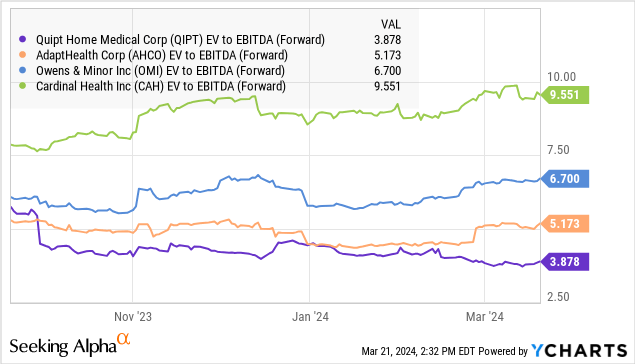

The setup is compelling for the stock against a current $256 million enterprise value implying just a 4x multiple on the Q4 adjusted EBITDA annualized run-rate. In other words, QIPT appears too cheap to ignore considering the growth and earnings momentum.

We'd carry that point further by noting QIPT trades at a discount on the same EV to EBITDA metric compared to related medical supply names including AdaptHealth Corp. (AHCO), Owens & Minor, Inc. (OMI), and Cardinal Health, Inc. (CAH) recognizing these companies focus on various categories. QIPT is a smaller player in this group which could justify some discounts but is also generating higher growth.

We rate QIPT as a buy with a year-ahead price target of $6.00, representing an EV to forward EBITDA multiple of 5x as closer to fair value. Looking ahead, the ability of management to continue driving growth and margins higher a path for earnings to accelerate through fiscal 2025 should unlock value in the stock as part of the bullish case.

In terms of risks, the company remains exposed to broader financial market volatility with a scenario where the macro outlook deteriorates and forces a reset of expectations. There is also a component here related to legal proceedings and even regulatory inquiries given the nature of the business.