pidjoe

pidjoe

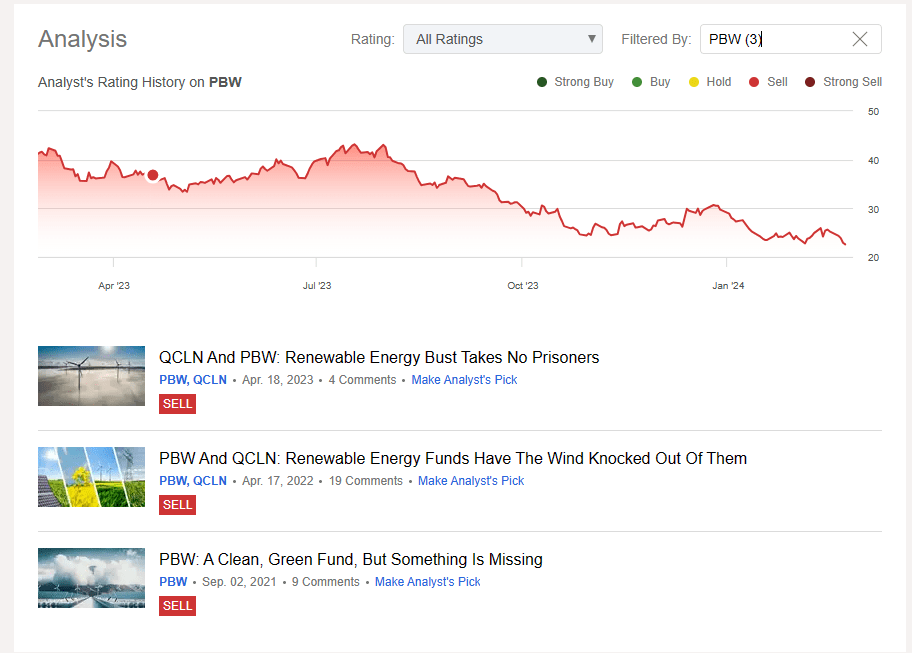

We have not written very frequently on Invesco WilderHill Clean Energy ETF (NYSEARCA:PBW), but we gave it the due attention and the correct rating. While the crowd has been enamored with "clean energy" theme, we have found little to like and even less to love. Our three ratings on PBW have all been "Sell" and on two occasions we also gave a similar treatment to First Trust NASDAQ Clean Edge Green Energy Index Fund ETF (QCLN).

Seeking Alpha

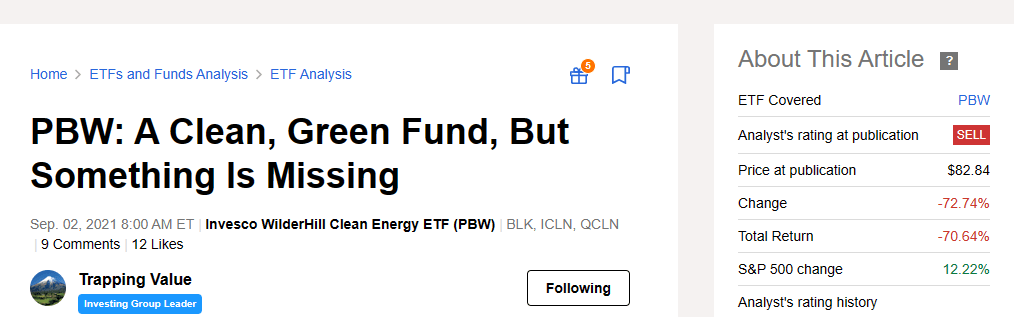

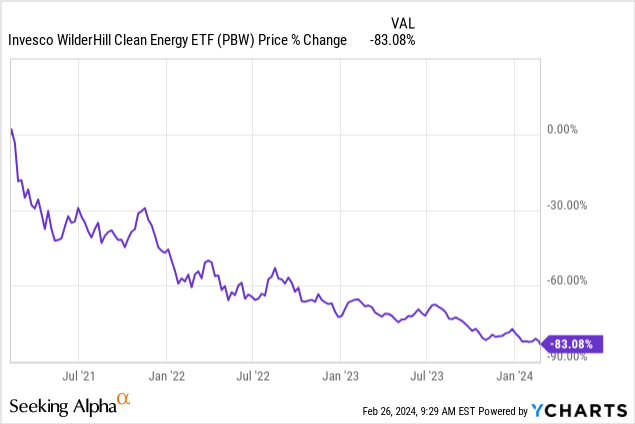

PBW has given investors quite the rollercoaster ride and is now down 72.74% since our first coverage.

Seeking Alpha

We take a fresh look at this one and tell you why we are now upgrading this fund.

As with most ETFs these days, PBW picks an index and sticks to it. In this case, the index is one that focuses on companies designed to reduce pollution and increase clean energy usage. As an added twist, there is language here for the advancement of conservation. This is generally missing in some other "clean energy" funds.

The Invesco WilderHill Clean Energy ETF is based on the WilderHill Clean Energy Index (Index). The Fund will normally invest at least 90% of its total assets in common stocks that comprise the Index. The Index is composed of stocks of companies that are publicly traded in the United States and engaged in the business of advancement of cleaner energy and conservation. The Fund and the Index are rebalanced and reconstituted quarterly.

Source: PBW

Regardless of how much time you might have taken to assimilate that, nothing would prepare you for what the constituents of this fund are. We were surprised the first time we looked at this, and we were surprised today as well.

PBW

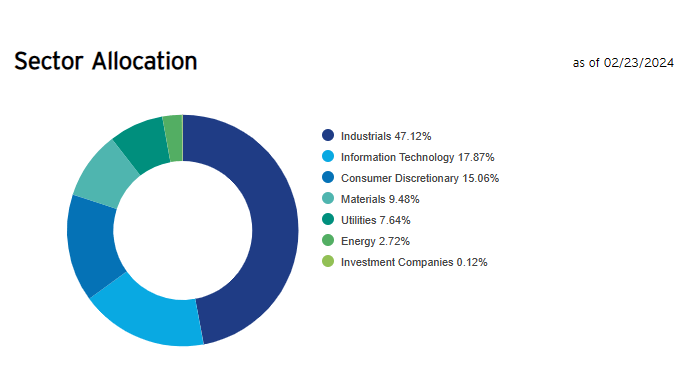

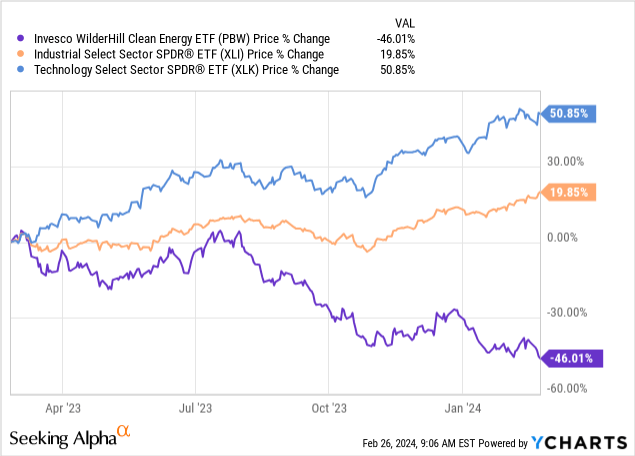

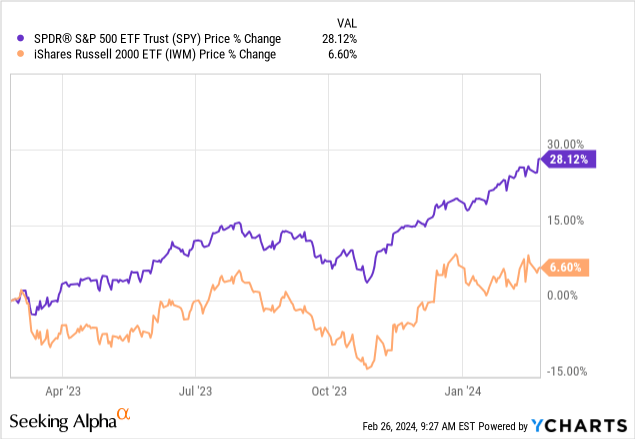

Industrials make up nearly half of the fund, and information technology stocks make up almost 18%. Utilities and energy come to only 10% combined. If you have been following anything at all in the news cycle, you would know for sure that industrials have been doing very well lately. Industrial Select Sector SPDR (XLI) has been a delight to own. Information technology is breaking all bounds of rational valuations and mooning on a daily basis and Technology Select Sector SPDR (XLK) has done 50% over the last 12 months. So with those two sectors as the top two in this fund, PBW's performance is truly shocking in comparison.

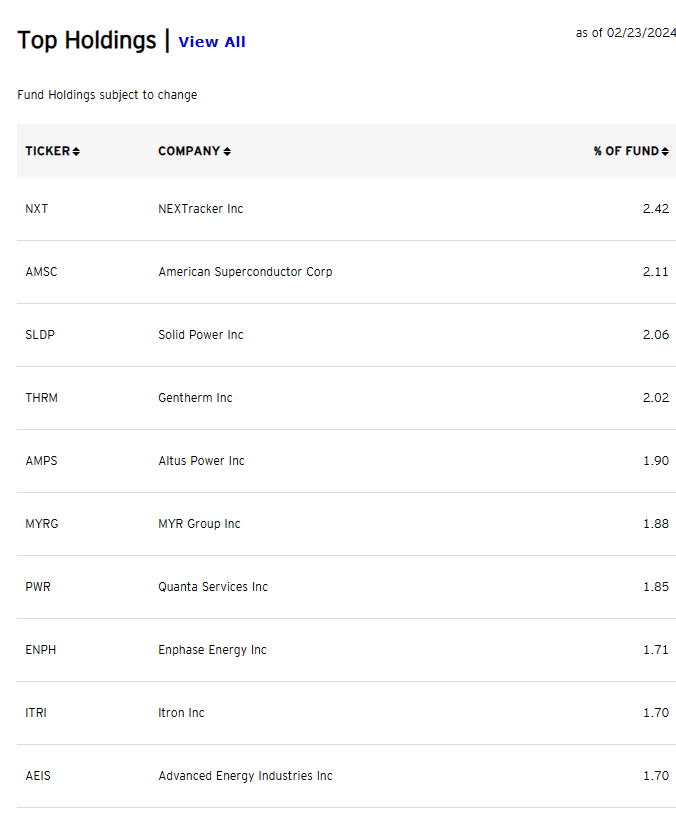

Flabbergasting, right? Well, yes and no. Based on sector weights you could be fooled, but when you examine the individual holdings you can understand. Below are the fund's top 10 holdings as of February 23, 2024, and in all honestly, we recognized 1 of those 10 names and one other one sounded vaguely familiar.

PBW

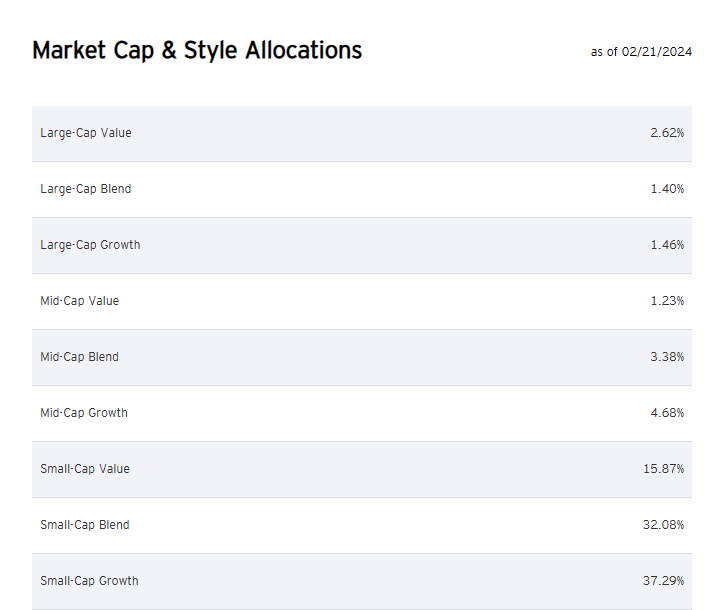

You can see why when you look at the capitalization and growth/value split of all the stocks in this fund. Large cap makes up about 5.5% of the total.

PBW

Small caps make up 85% of the total when you add the value, blend and growth categories. That sector has been exceptionally poor in performance relative to large caps, and that is part of the issue here with PBW.

With all that said, we now give you three reasons as to why we are moving out from the sell rating and upgrading this to a "hold".

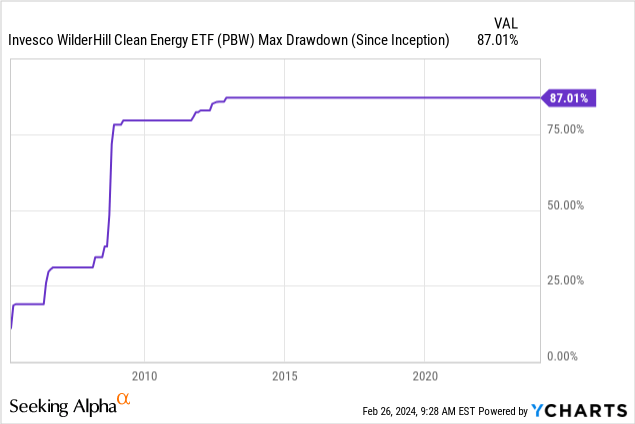

If you bought at the absolute peak of this cycle, PBW has delivered a drawdown of 83.08%.

This is not the maximum for sure, and we have seen worse, even in this ETF.

But 80% of drawdowns are associated with a large amount of disdain and negativity. They dramatically improve your odds of making good returns. This is especially true for asset classes. Individual stocks can and do go to zero. Asset classes do not. So we are in good territory here to look at this optimistically.

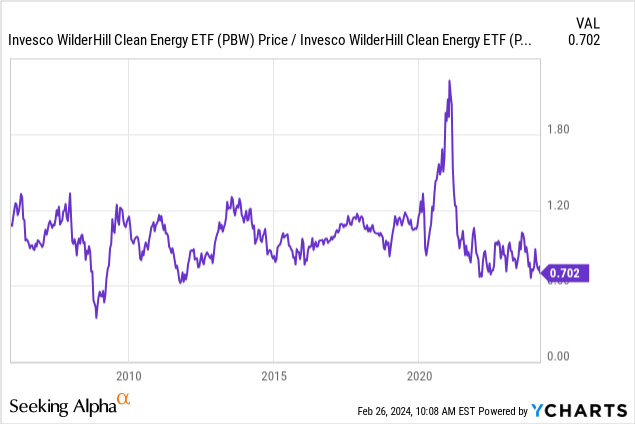

We always like to see where a stock is trading relative to its own 200-day moving average. That parabolic move off the 2020 bottom produced a ridiculous 2.2X 200-day moving average price. At 0.7X, this looks ripe for a rebound.

Historically, you had only one really bad entry if you used these criteria, and that was in the global financial crisis. While we are not using this for a long side entry, it at least makes the prospect of upgrading this to a hold, far more appealing.

While we have not (and will not) done due diligence on all the holdings of this fund, we think the poor performance has a lot to do with the unwinding of the bubble from 2021. These bubbles almost always go to the other extreme and create a value situation at the end. Our personal research has also shown that many renewable energy stocks are now a bit on the cheap side. We wrote on one just recently. So considering that baby is going out with the bathwater, we see things as less bearish. We are certain, that on the whole, the fund's holdings are also trending the same way.

An upgrade to Hold does not mean everyone should go and buy. It just means a "Sell" rating or a short selling activity is no longer a good choice. As investors and traders well know, the most oversold stocks and ETFs can bounce the hardest. We see the potential for that here, and hence we are ready to declare victory and move on. Those interested in this should consider scouting for long entries, as the short case is a bit overbaked. Good luck.