ozgurdonmaz

ozgurdonmaz

Since the last time I wrote about Tommy Hilfiger and Calvin Klein brands' owner PVH Corp. (NYSE:PVH) in August last year, its price is up by an impressive 67%. Even at that time, a 50-80% upside was visible based on the fact that its price was way too low compared to its financial performance prompting a Buy rating on it.

But after the sharp upturn, the question now is whether it's still a Buy. Here I assess this with an outlook on its fourth quarter (Q4 2023) and full-year 2023 results that are released at the beginning of April.

While the stock saw some increase between August and November last year, it was really the release of its Q3 2023 results on November 29, 2023, that sparked investor interest. It jumped by almost 7% the following day, the biggest single day rise seen in the past year, after a 20% jump on Mar 28, 2023, following its full-year 2022 earnings report (see chart below).

Price Chart, 1y (Seeking Alpha)

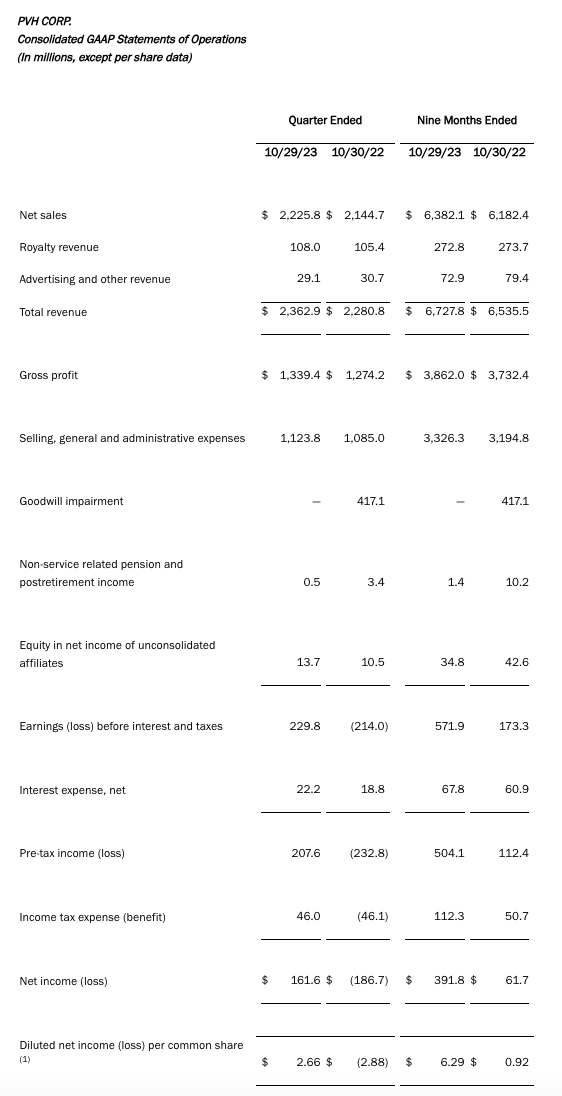

There was good reason for the price rise too. PVH's revenues rose by 3.6% in Q3 2023, the upper end of its previous guidance range of 3-4%. Growth was just a tad below the range at 2.9% for the first nine months of the year (9m 2023). But even this is an improvement from the 2.6% for the first half of 2023 (H1 2023), evidently on improved performance in Q3 2023.

PVH also exceeded its EPS estimates. The GAAP EPS came in at USD 2.66, which is 9.5% higher than the projection of USD 2.43. Similarly, the non-GAAP EPS came in at USD 2.9, 7.4% higher than the estimated USD 2.7. With the better-than-expected earnings, the net margin improved to 6.8% in Q3 2023 after softening to 4.3% in Q2 2023, when I last checked.

PVH Corp.

Underpinning the improved performance is the company's restructuring plan, PVH+, which aims at faster revenue growth and expanded margins, even though the company is clearly a long way off from achieving the desired objectives. It will have to grow revenues by 38.5% by the end of 2025 from 2022 to meet its target of USD 12.5 billion. Also, its operating margin of 10% for Q3 2023 is lower than the 15% target, though it can improve as the plan starts bearing more fruit.

Despite the improved recent performance though, as far as headline revenues are concerned, the upcoming results are expected to be disappointing. The company downgraded its full-year forecast to just 1% as it expects a 3-4% decline in Q4 2023. But this is not something to worry about. It's explained by the loss of revenues on account of the sale of its Heritage Brands intimate apparel business in November 2023 to focus on its key brands. The segment as a whole has a 5.35% share in the company's revenues as of Q3 2023. If the impact of this segment's sales is removed from the revenues, the number drops by 2.1%, which can explain the forecast.

But here's the catch. Removing the segment's sales from the base period too, which leaves just Tommy Hilfiger and Calvin Klein as revenue segments, actually bumps up revenue growth to 4.6% in Q3 2023, which is higher than the previous guidance range for the year. The basic point to note here is that ex-Heritage Brands, PVH Corp.'s revenue growth can still be expected to increase at a relatively healthy pace even in Q4 2023.

Despite the revenue decline, however, the EPS guidance was upgraded for the second time in the past quarter with better-than-expected performance so far this year. The company now expects full-year 2023 EPS to come in at USD 9.75 on a GAAP basis and at USD 10.45 on a non-GAAP basis. This isn't a significant improvement over the previous guidance, with an increase of 1.6% and 1.1% in the GAAP and non-GAAP projections respectively.

However, the GAAP estimate is a massive 222% year-on-year (YoY) increase likely on the gains from the sale of the Heritage Brands business. The non-GAAP estimate is expected to see a much smaller but still healthy 16.6% growth. The EPS increase is expected to spill over into Q4 2023 as well, with a 59.6% increase in GAAP EPS to USD 3.48 and a 45% rise in non-GAAP EPS to USD 3.45.

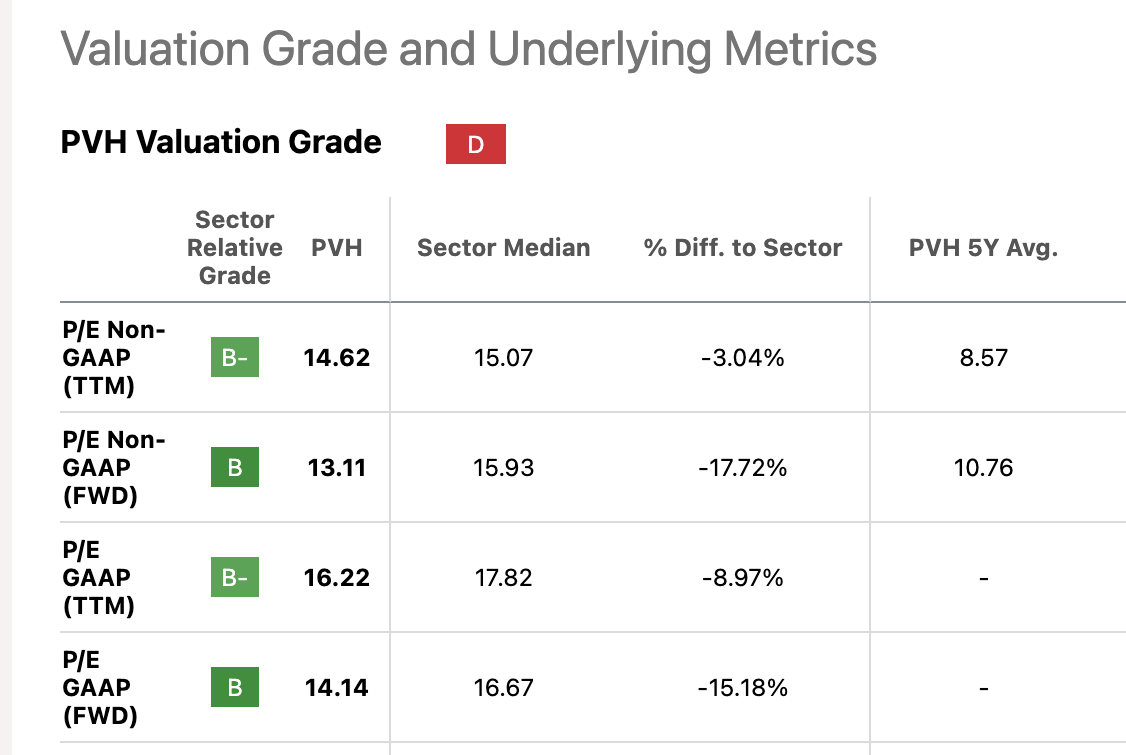

With these EPS upgrades, the PVH stock's market multiples still look attractive. Here I've considered the upcoming numbers instead of the existing trailing twelve month [TTM] figures. These yield a TTM GAAP P/E of 14.15x and a non-GAAP P/E of 13.2x. These compare favourably with the corresponding median P/Es for the consumer discretionary sector at 17.8x and 15.1x respectively.

Further, the forward P/E for PVH's current financial year based on analysts' estimates on Seeking Alpha also looks good at 11.5x, as compared to that for its peers like Ralph Lauren (RL) and Levi Strauss (LEVI) at 17.1x and 15.6x.

Seeking Alpha

The current multiples for PVH are still higher than its 5-year averages (see table above) but going by its ongoing restructuring, I believe the sectoral and peer comparisons are more relevant at present. These figures essentially indicate that there's a 15-25% upside to the PVH stock going forward. This upside can be even higher if the company exceeds its EPS expectations again.

The key takeaway here is that the PVH stock still looks good. And chances are, its outlook for the current financial year will be positive too, going by the improvements shown with its restructuring plan underway. The company's revenue growth has improved and while the sale of the Heritage Brands business can impact the upcoming figures, ideally the number should be considered after removing its impact from the base year.

A highlight feature for PVH recently has been its EPS, which has exceeded guidance. This in turn has resulted in attractive P/E ratios for the stock despite the sharp price over the recent months. With the company's focus now more on its key brands, there's a possibility that its numbers may continue to surprise on the upside. I'm retaining a Buy rating on PVH.