Traimak_Ivan

Traimak_Ivan

Co-authored by Treading Softly.

Fear is considered to be one of the greatest emotions that a human can experience, and by greatest, I don't mean the best or the most exciting. I mean the most powerful. For those who believe in the evolutionary theory, fear is a primal emotion that causes one to flee a dangerous situation to keep them alive. For many, we run into a situation where we can have a fight or flight response where either we are going to be jacked up on adrenaline to get the heck out of there or to try and beat whatever threat is in front of us. Overwhelmingly, though, most people choose the flight option versus the fight option.

When it comes to the market, investors can be exceptionally trigger-happy. What this means, is that even at the slightest chance of negative news, an investor will sell everything - ironically locking in massive losses under the intent of preserving their capital. It's a frequent mistake that investors will make. It is understandable because many investors are novices in this space or they are hard-working individuals or retirees who are using their life savings to try and generate wealth in the market. They have the greatest fear of losing it all and seeing all of that hard work go up in a puff of smoke. Unfortunately, many will cause that puff of smoke to occur by their reactionary decision making than if they would have done nothing at all.

Today I want to look at two opportunities to invest in outstanding picks. These opportunities have seen good times and bad times, but regardless, they have been able to provide strong and steady income and at times even strong market-beating returns. They're headed up by some very skilled management teams that make them worth taking a deeper look into - so that's what we're going to do.

Let's dive in!

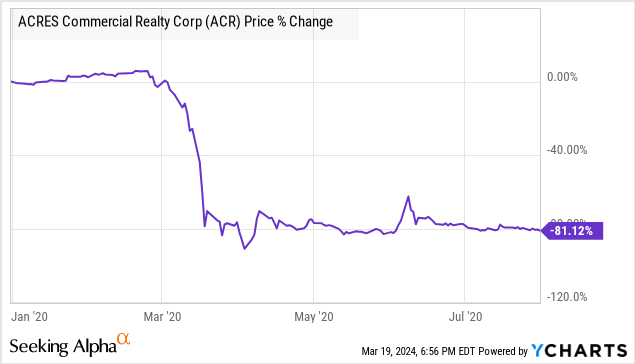

ACRES Commercial Realty Corp. (ACR) has lived a very interesting life. Previously this company was Exantas and the prior management failed to manage the company effectively through the COVID crash.

2020 was a time when many firms, especially mortgage REITs, were hit hard. ACRES took control in August of 2020 and has since carefully unwound the prior management's portfolio and focused on reducing risk while getting expenses under control. Currently, ACR doesn't pay a common dividend and they don't have to, even though they're generating plenty of would-be taxable income.

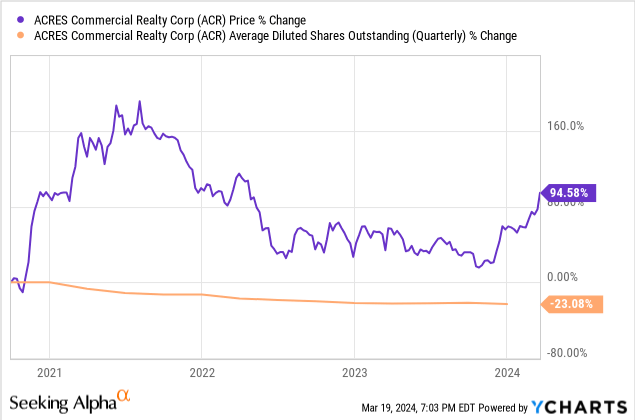

When the new management took over and they liquidated large parts of the prior management portfolio, they were able to lock in taxable loss carry-forwards. This allows them to offset any tax earnings they earn in the future with these losses. What has since occurred is that while the new portfolio is generating plenty of taxable income, the management is applying these carry-forward losses against them, causing them to have no taxable income whatsoever. This means that the common shareholders are not receiving a dividend because there is no taxable income that they are required to distribute to them. We expect by the end of 2024 or mid-2025 that ACR will be forced to resume its common dividend. Their stated goal is to have a common dividend that is about 10% yield on book value. ACR trades at a massive discount to book value largely, so in the near term, management has focused on buying back common shares.

Since taking over on August 3, 2020 this new management team has been able to reduce the overall share count by 23% and they continue to actively buy back shares. Furthermore, this has led to a 94% rise in share price.

When evaluating ACR, we choose to look higher into the capital stack and instead invest in ACRES Commercial Realty Corp 8.625% Fixed-to-Float Series C Cumulative Redeem Preferred Stock (ACR.PR.C). This is a highly unique fixed-to-float preferred security in that it maintains an interest rate floor equivalent to its prior fixed rate. So the floating feature only serves as a route to see higher income than during its prior fixed rate, never less. If it is not redeemed on July 30, 2024, then at the current SOFR rate the floating coupon rate would be 11.5%.

ACR is covering their preferred obligation by a thin 1.12x for 2023, but we expect this to continue to improve as ACR is seeing rising earnings with their portfolio's performance continuing to improve.

We're happy to hold a preferred that has coverage and a management team focused on being conservative and careful.

It is no secret that PIMCO is one of my favorite CEF managers in the fixed-income space. PIMCO has a proven track record of navigating the bond markets and coming out looking smarter than everyone else.

PIMCO Corporate & Income Opportunity Fund (PTY) could be described as PIMCO's "flagship fund." It is also one of my favorites. Judging by the high premium that it typically trades at, it is a favorite for a lot of other folks too.

Since PTY is one of my favorite funds, I've written about it quite a bit. Somewhere around 100% of the time, when I write about PTY, folks will have a panic attack over the size of the premium. Hey, I love a discount as much as the next guy, and more than most. Yet, I also recognize that some things are worth a premium.

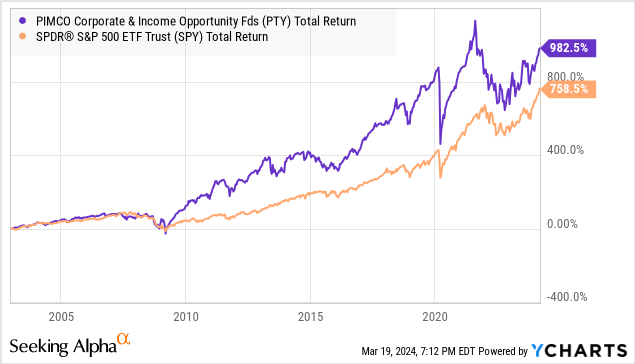

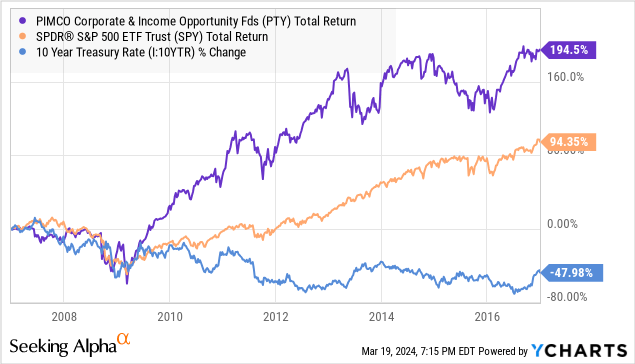

PTY is PIMCOs best-performing bond fund on a 3-year, 5-year, 10-year, and since inception NAV basis.

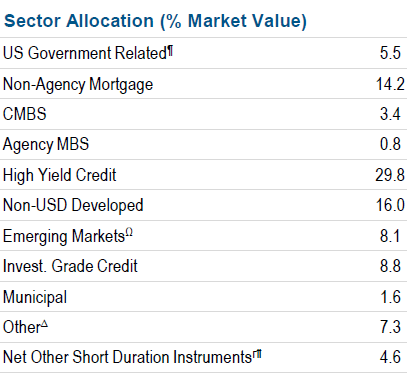

Every PIMCO fund has a bit of a different asset mix. PTY focuses on high-yield credit and non-USD investments. Source.

PTY Fund Card

These are sectors where PIMCO has historically shined, using its size and expertise to evaluate and profit from situations that others run away from. PTY's goal is broad, providing the management team with a lot of leeway:

"PIMCO Corporate & Income Opportunity Fund's investment objective is to seek maximum total return through a combination of current income and capital appreciation."

Maximum total return is what PTY has provided over the decades. For over 20 years, PTY has been providing investors with a bond fund that has outperformed peers. It has actually outperformed the S&P 500 during a time when equities radically outperformed fixed income.

So, we are measuring to a time when equities are at all-time high prices, and bonds are at long-term low prices, and measuring to that date, PTY still outperformed the S&P 500 (SP500) since 2003.

Imagine how great PTY would look if the asset class they invest in actually outperformed!

We don't have to imagine; we can actually see what happened the last time the 10-year Treasury (US10Y) took a trip from the 4%s down to the 2%s:

It is a historic opportunity to be buying fixed-income. The Fed hiked interest rates very quickly, and it has been brutal to bond prices, and that has been reflected in PTY's NAV and share price.

Yet, we need to keep in mind what lower bond prices mean. Lower bond prices mean higher yields. When interest rates are higher, who is getting paid more? Those who own debt! When interest rates are high relative to where they have been in the past and probably will be in the future, would you rather be a lender or a borrower?

Personally, I favor being a lender over being a borrower at all times. There are two types of people in this world: Those who pay interest and those who collect it. The day I figured out that simple fact and dedicated my life to collecting interest rather than paying it, my financial world improved for the better. When interest rates are higher, it is that much better to be an interest collector.

I've been buying debt over the past few years. As interest rates rose and prices of existing debt declined, I continued to reinvest the majority of my investment dollars into various types of debt. PTY is a fund that holds a wide variety of debt, and with management's track record, it is a position that I reinvest in routinely.

When it comes to being able to lock in high yields, while others are driven by panic and misinformation, a key component of that is being the one who is paid interest, instead of the one who is paying interest. With PTY and ACR, I can be in a position where I am paid the interest on the debt. In ACR's case, I am a preferred shareholder thus I am owed interest that builds on a cumulative basis even if they are unable to pay me in the immediate term. With PTY, I am paid interest from countless other parties with whom I own the debt through the fund. At the end of the day, I can lock in high yields while others are worried about what's going on with the AI boom, worried about what's going on with the elections, or wondering why Facebook stopped working last week. Instead, I can sit back, relax, collect high levels of income today, and enjoy the present.

When it comes to retirement, I don't want you to be stressed about where your money's coming from or how you're going to be able to pay your debts. Instead, I want you to be collecting on the debts of others and getting interested in the meantime. That way when the weather is warm and the sun is shining, you're able to strike up the barbecue, enjoy a cookout with your family, drink some of your favorite beverages, and salute another day being done, knowing that you have financial independence.

That's the beauty of my Income Method. That's the beauty of income investing

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.