TommL

TommL

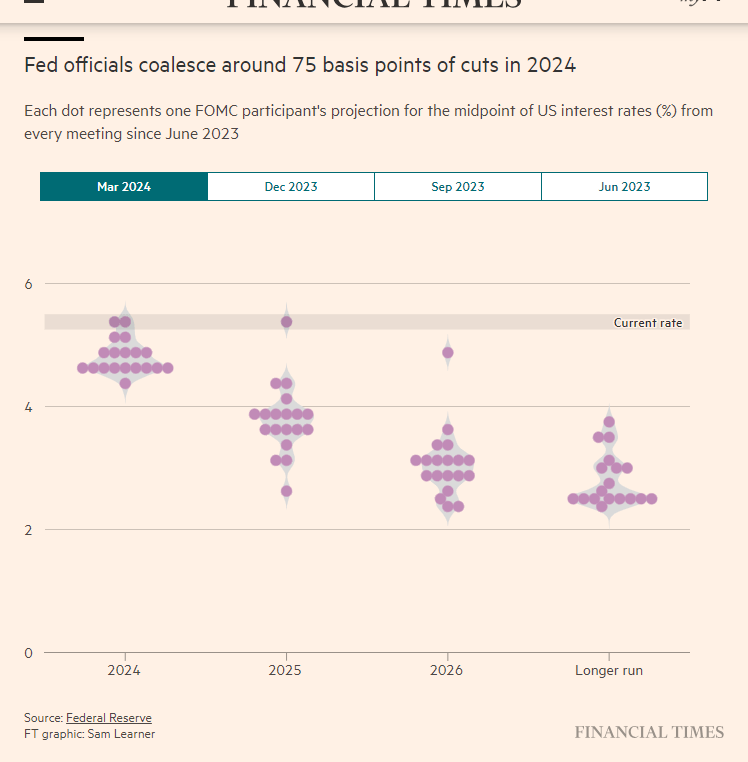

Following my coverage of Pactiv Evergreen (NASDAQ:PTVE), for which I recommended a neutral rating as I thought FY23 was a messy year with many one-off events that were obstructing investors’ ability to better value the business, this post is to provide an update on my thoughts on the business and stock. I am upgrading my rating from a neutral to a buy rating as the business has shown very early signs of demand recovery. What is more important is that management executed really well in reducing the business cost structure. As PTVE completes all its intended cost savings initiatives by FY26, I expect to see a surge in FCF, which, based on my estimates, translates to ~11% FCF yield on today’s share price. Assuming the Fed cut rates back to 2+%, as the dot plot indicates, the historical spread suggests that PTVE’s stock could see 50% capital appreciation.

Just to quickly touch on the recent performance, total 4Q23 revenue fell to $1.274 billion, where Foodservices [FS] saw $626 million in sales (-1.1% y/y); and Food & Beverage Merchandising [FBM] saw sales fall by 25.1% to $653 million. That said, EBITDA improved by $40 million to $207 million, indicating an EBITDA margin improvement of 490 basis points from 11.3% to 16.2% on a consolidated basis. Margin improvement was seen in both segments, where FS saw improvement from 13.4% to 17.9% and FBM saw expansion from 12.5% to 17.3%.

Frankly, I thought the results were actually not bad, considering that EBTIDA came in way stronger than expected, which really speaks well of PTVE's ability to drive cost rationalization that sets the stage for further margin expansion when volume starts coming back online. However, the stock price saw a big dive post-earnings, which I believe was due to the rather poor FY24 EBITDA guide. Management guided FY24 adjusted EBITDA of $850 to $870 million, which came below consensus expectation for $868 million, and 1Q24 adjusted EBITDA is expected to be in the range of $160 to $170 million (run rate of $668 million), which implies a ramp up in 2H24. This basically got investors to take a conservative stance in forecasting FY24 results, and especially since the share price has already seen a strong rally, I believe a lot of investors went into profit-taking mode as well.

My view is that FY24 is the last period before we start to see a strong margin ramp up with the top line recovering. If we look deeper into recent performance, there is one very early sign of PTVE pivoting to a recovery. In the FS segment, PTVE grew organic volumes despite weakness in the overall industry, with management highlighting market share gains. Beyond the headline numbers and management comments, I think this also shows that the PTVE strategy to optimize the portfolio has clearly worked out, putting it in a better position to grow ahead of the broader market when the macro conditions recover. Of course, this is overwhelmed by the overall company performance, but this is nonetheless a very positive indicator of potential recovery in the coming quarters, in my opinion.

PTVE also announced a manufacturing and warehouse restructuring plan aimed at improving operational efficiency, with estimated run-rate cost savings of $35 million by FY26. Capex related to the plan is expected to be in the range of $40 to $50 million, primarily in FY24/25, and to incur total cash charges of $50 to $65 million and total non-cash charges of $20 to $40 million relating to the effort. $35 million might not seem like a lot by itself, but this represents 13% of FY23 pre-tax income. If we look at the track record of realizing these cost savings in recent history, I am optimistic about management’s ability to realize this $35 million by FY26. The most recent example would be that consolidated EBITDA margins came in at 16.2% in 4Q23 as cost benefits from the closure of the Canton, NC, mill and ongoing restructuring efforts continued to come through. The way I see it, there are still plenty of opportunities for PTVE to continue to reap cost-saving benefits. Specifically, management noted there will be an even larger step up from the benefits from its Footprint Optimization program, where they expect to reach a $10 to $15 million cost on a run rate basis by FY24 (most of this will come in 4Q24). They also hinted at the possibility of divesting the Pine Bluff mill, which could deliver further cost savings if divested.

Therefore, my outlook ahead for PTVE is that FY24 will continue to see further cost optimization. As PTVE completes its cost rationalization initiatives over the coming years, which would bring down the structural cost profile of the business and also release more FCF as CAPEX steps down, along with a recovery in volume due to improved consumer demand (as the economy recovers with inflation gradually tapering down), FY26 could see a really strong boost in EBITDA and FCF.

Own calculation

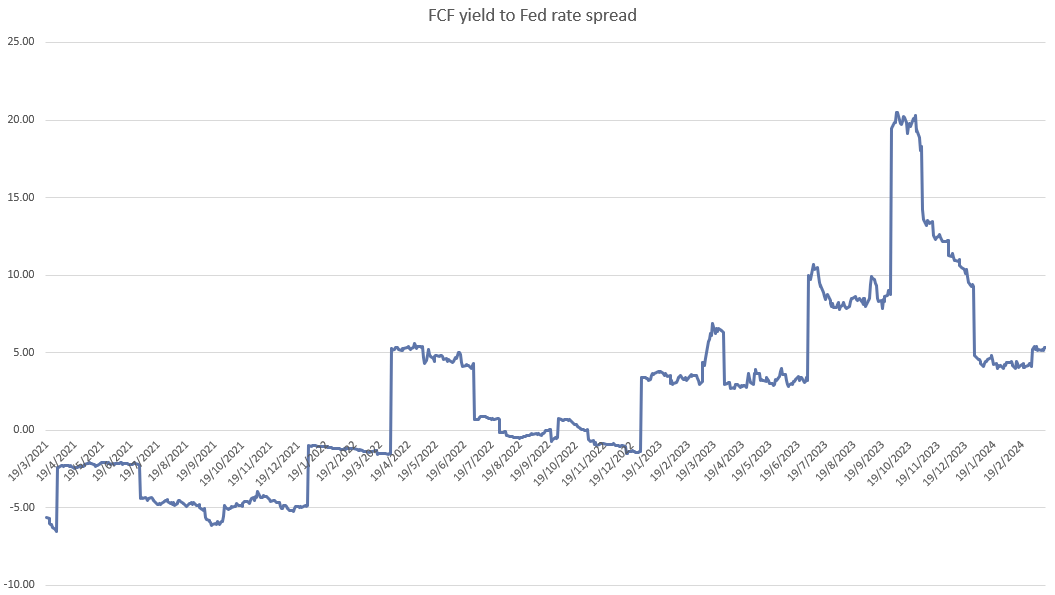

As of FY23, PTVE FCF yield is around 10% (FY23 FCF of $249 million / $2.49 billion in market cap). When compared to the current near-term Fed rate of ~5.25%, this implies a spread of ~500 bps. Because of some of the incremental capex (as I stated above) that is going to come online in FY24/25, FY26 will be the year where PTVE sees its true FCF. If we look back to PTVE pre-covid, where there were no major cost restructuring programs, PTVE has an FCF margin of around mid-single-digits. Using the FY26 consensus revenue estimate of $5.7 billion, this implies an FCF of $285 million, which translates to a FCF yield of ~11.4%. Assuming the Fed cut rates back to ~2+% (using the recent dot plot as a gauge) and the spread remains the same at 500bps, this implies PTVE should trade at ~7+% FCF yield. A compression of FCF yield from 11.4% to 7.5% implies that PTVE will see a capital appreciation of ~50% (11.4%/7.5%).

FT

Management could mess up the restructuring program, which could delay the expected timeline for margin improvement. The worst is if they cut too much, so much that they are not able to meet the demand recovery ahead. If this happens, it could trigger the need to step up CAPEX spending to improve capacity, which will reduce FCF.

In conclusion, my rating for PTVE is an upgrade to a buy rating as I expect strong FCF generation ahead, with yield possibly touching 11% by FY26 based on current share price. FY24 will likely see continued cost optimization, and as the macro economy gets better, PTVE should see a recovery in demand. Suppose my expectation for FCF materialize, using historical FCF yield to Fed rate spread, I see a potential for 50% capital appreciation (stock price go up). Risks include potential missteps in the restructuring program that could delay margin improvement or necessitate increased CAPEX spending.