Laurence Dutton

Laurence Dutton

Based on my current outlook and analysis of PTC Inc. (NASDAQ:PTC), I recommend a buy rating. I believe the long-term growth outlook for PTC is very positive given its exposure to key growth verticals. I expect the underlying industrial companies to eventually adopt these advanced technological solutions as they compete with their peers to become more productive and cost-efficient, and PTC is well-positioned to capture these demands.

PTC is a software solution provider for clients in industries that are heavy in design, manufacturing, and project management. The three main solutions that PTC provides are computer-aided design (CAD), product lifecycle management (PLM), and augmented reality (AR). PTC has also recently entered the Internet of Things (IoT) vertical. The business reporting is segmented into three parts: recurring revenue, perpetual licenses, and professional services. The recurring revenue segment is the largest of the three, representing 91% of FY23 revenue. f

PTC

PTC has a long runway of growth ahead given its exposure to growing verticals: CAD, PLM, AR/IoT.

First, let's talk about the CAD market. As a little background, CAD is software that was developed to enhance the design process by making it more efficient, better organized, and more documented. It also introduced the ability to iterate. By essentially automating the once-manual process of drawing and design calculations, CAD greatly enhances efficiency. For sectors like construction and civil engineering, where large-scale projects necessitate numerous revisions and zero tolerance for error, the value proposition is thus exceptionally compelling. According to third-party research, the global CAD market is expected to continue growing at mid-single-digits for the coming decade. In my view, growth is going to be higher than mid-single-digits because of AI, as the infusion of AI into CAD significantly enhances productivity, which can reduce the overall cost of projects.

PLM is the next attractive market that PTC has exposure too. To provide some background, PLM software makes it easier for clients to streamline their design and manufacturing processes by centralizing and organizing all of the important product data generated during the development process. Essentially, PLM aids clients in reducing expenses, simplifying processes, and shortening lifecycles. As technologies like AR and the Internet of Things gain traction, PLM plays an increasingly important role in making information more accessible across organizations, which in turn improves the efficiency of engineering and manufacturing processes. With the help of IoT (more below) sensors, PLM can cover more ground than just product development and now encompasses the whole product lifecycle. As the amount of data, documentation, specifications, and computations associated with projects continues to rise along with the sophistication of the underlying models, I foresee a rising demand for PLM in the years to come.

Touching more on IoT, it is the use of software solutions to link more industrial and manufacturing machines and plants for the purpose of increasing data aggregation, decreasing production risk, and improving efficiency and productivity. Unlike consumer-based IoT products, I believe commercial IoT products have a lot more value as they are a more cost-effective solution that can be incorporated across plants and factories rather than having employees do checks on a periodic basis (which is not as good as the 24/7 surveillance that IoT can provide). This As a result, data aggregation has become a lot more important, as businesses need these data to enhance their digital twins and get more value from them through advanced data analysis. The way I see it, IoT has become a table stake for industrial companies. They have to eventually implement IoT solutions (only 60% are using IoT now) in order to stay competitive on cost and productivity, and PTC is here to pick up share.

Lastly, I have a strong belief in the demand within the augmented reality vertical. When it comes to industrial companies, augmented reality allows for more robust training programs that optimize workforces by reducing onboarding requirements and improving early success rates. Businesses can also gain a competitive edge with industrial AR software by creating and projecting augmented reality training instructions into industrial settings like plants and factories.

A good product requires a strong distribution strategy to drive growth; if not, it is just a good product. Fortunately, management has gotten this part of the growth equation right as well. As part of the effort to transition into a subscription business model, PTC invested heavily in its go-to-market team, with a focus on being a customer success organization that is built around a customer success manager. While PTC does not disclose the actual renewal rates, from the transcripts, we can tell that renewal rates have been strong, which is an indication that the GTM strategy is working. I also highlight that this GTM model works very well for the nature of PTC products, which have a long duration due to the underlying industrial project durations; hence, it gives PTC multiple opportunities to upsell new products and solutions that can make life easier for its clients. Aside from that, PTC also has three significant partnerships, one each with industry leaders Microsoft, Rockwell Automation, and Ansys. Of the three, I think the partnership with Microsoft is going to be a key one, as PTC can leverage the MSFT global enterprise sales force to sell PTC cloud-based products linked to MSFT's Azure IoT Hub for ingesting data.

The growth momentum continues to be strong as management reiterated a constant currency ARR of $2.19 billion to $2.25 billion, implying a growth rate of 11 to 14%. This guidance also implies that PTC growth is back to a more normalized level, in line with its pre-covid growth range of low-teen percentages. Revenue guidance is also reiterated at $2.27 billion to $2.36 billion, implying a growth rate of ~10%. The revenue guide reiteration is significant because it implies that normalized growth (I use the term normalize here because ARR is trending back towards a normalized range) is now above the 10% threshold, a level that PTC has failed to attain outside of the COVID period (FY20/21).

There are a number of qualitative signs that growth is going to be robust in the future as well. For example, PTC's on-premise Windchill systems are still in the early stages of being the customer base's central repository for product data. ServiceMax and ALM (application lifecycle management) led by Codebeamer and augmented by PureVariants are two additional cross-selling opportunities for PTC. The former greatly improves PTC's SLM (service lifecycle management) portfolio and allows PTC to provide a complete solution for optimizing service processes. Additional opportunities include expanding CAD and shifting to SaaS for all products. These two paths will cross paths to a certain degree as PTC sees Creo customers transitioning to Creo Plus, a SaaS offering similar to Windchill Plus.

So as we mentioned, I think last earnings call, we've been seeing Codebeamer as a tip of the spear, where we're particularly in automotive suppliers, where now we're getting in the conversation as we're showing them the Codebeamer value prop.

A second cross-sell opportunity is ServiceMax. We acquired ServiceMax in January 2023, and the strategic fit with PTC is solid. For many of our customers, growing the services business is their top priority.

Clearly, continuing to grow CAD and converting our installed base over to SaaS across all products are two additional opportunities, which overlap to some extent because we will see conversion of Creo customers to our Creo+ SaaS offering over time, much like Windchill+. 1Q24 call

Author's work

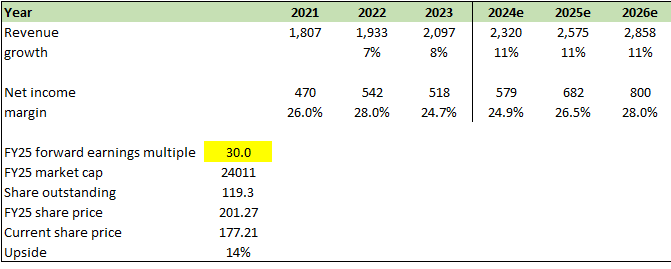

I believe PTC can grow at 11% for the coming 3 fiscal years as the impact of COVID finally goes away, allowing it to show its normalized growth, which I believe management has guided. Supporting this growth are multiple growth drivers within the CAD, PLM, AR, and IoT markets that I expect to see continuous demand in the coming years as industrial companies need to leverage these technologies to become more productive on both cost and efficiency fronts. As PTC scales its revenue, it should also drive margin expansion as it has a high incremental margin, which can be seen from the increasing EBIT margin (from 20% in FY19 to 36% in FY23). I would also note that peers like Dassault Systemes and Autodesk have net margins of 18% and 17%, respectively, so there are precedents for PTC to continue expanding margins. In determining the right multiple for PTC, I benchmark its fundamentals against the same peers (Dassault Systemes and Autodesk). Both peers have a similar growth outlook but higher margins and a better balance sheet profile. As such, I think PTC should trade at a discount to them. I assumed PTC to trade at 30x, which is a 1x discount vs. Autodesk and also its own historical average.

Demand for PTC solutions is indirectly impacted by the macroeconomic situation. In a recession, there is likely to be fewer new construction activities and projects as clients take a risk-off approach (avoid huge capital outlay with soft economic outlook, and weak pricing environment), which means there is a lesser need for PTC solutions (lesser need for CAD, for instance). While the product is sticky because of all the data combined, businesses could look to downsize their needs (i.e., reduce tier), thereby impacting ARPU for PTC.

All in all, I recommend a buy rating for PTC given its strong exposure to key growth verticals. PTC's strategic partnerships and a robust distribution strategy are key factors that helps PTC to capture demand. Based on management guidance, near-term performance for FY24 reflects a return to normalized growth levels, and a favorable outlook. I expect PTC to see growth of low-teens over the next three fiscal years, driven by ongoing demand in key markets and potential margin expansion.