Joe_Potato

Joe_Potato

With a market capitalization of $63.5 billion, Phillips 66 (NYSE:PSX) is one of the largest energy companies, not only in the US, but across the globe. Despite this, I feel like the firm does not receive all that much attention from investors. Even I have not kept track of its operations as closely as I should. The last time I wrote about the business, for instance, was in an article published in February of 2018. At that time, the discussion centered around an agreement struck between the firm and Warren Buffett’s Berkshire Hathaway (BRK.A) (BRK.B) whereby Phillips 66 would be acquiring $3.3 billion of its shares back from the conglomerate.

In that article, I argued that investors probably should not follow Warren Buffett out of that position. Although the very nature of the operations that comprise Phillips 66 mean that financial performance can be incredibly volatile, even by the standards of the energy market, I believed that the long-term outlook for the company was still positive. Since then, management has proven my stance on the matter right. While the S&P 500 has shot up 86.5% since then, shares of Phillips 66 have seen upside of 102.1%. Despite this, the stock still looks attractively priced, even though it might be a bit lofty compared to similar firms. And when you factor in the major investments that management is making into the business's future, I would argue that a soft ‘buy’ rating still makes sense at this time.

It would not be inaccurate to consider Phillips 66 a diverse player in the energy markets. Management describes the business primarily through the lens of the four operating segments that make up essentially all of the firm’s activities. The first of these is the Midstream segment, which centers around providing transportation services, terminaling and processing services, and more, for things like crude oil, refined petroleum products, natural gas, NGLs, and more. Other activities under this umbrella include storage, fractionation, marketing, and more.

Next in line, we have the Chemicals segment. This essentially includes the 50% equity ownership that the firm has in Chevron Phillips Chemical Company, which focuses on producing and selling petrochemicals and plastics across the globe. The Refining segment refines crude oil and other feedstocks into petroleum products. Examples that management provides include gasoline, distillates, aviation fuels, and even some renewable fuels. This is a hyper local line of business, with operations only between the US and Europe that consist of 12 refineries. And finally, there is the Marketing & Specialties segment. Through this unit, the company purchases and then resells refined petroleum products and renewable fuels. Some of its operations also include manufacturing and selling base oils and lubricants.

As a value investor, my preference is for companies that can demonstrate operational stability from one year to the next. I tend to stay away from prospects that can see wild fluctuations in cash flows or earnings. Unfortunately, Phillips 66 is the exact opposite of what I tend to prioritize. All of the companies operating segments have a history of extreme volatility. The two most extreme in recent years have been the Midstream segment and the Refining segment. But this isn't necessarily the fault of management.

When it comes to the Midstream, profits have been all over the map over the past three years. After seeing a rise from $1.50 billion in 2021 to $4.73 billion in 2022, profits plummeted to $2.77 billion last year. The midstream space is often considered pretty stable and a source of significant cash flow generation for businesses. However, Phillips 66 has been undergoing a number of transactions aimed at creating additional value for shareholders in the long run. In 2022, for instance, the Midstream segment benefited from a pretax gain of $3.01 billion associated with the DCP Midstream merger. That essentially caused results for 2022 to be overinflated.

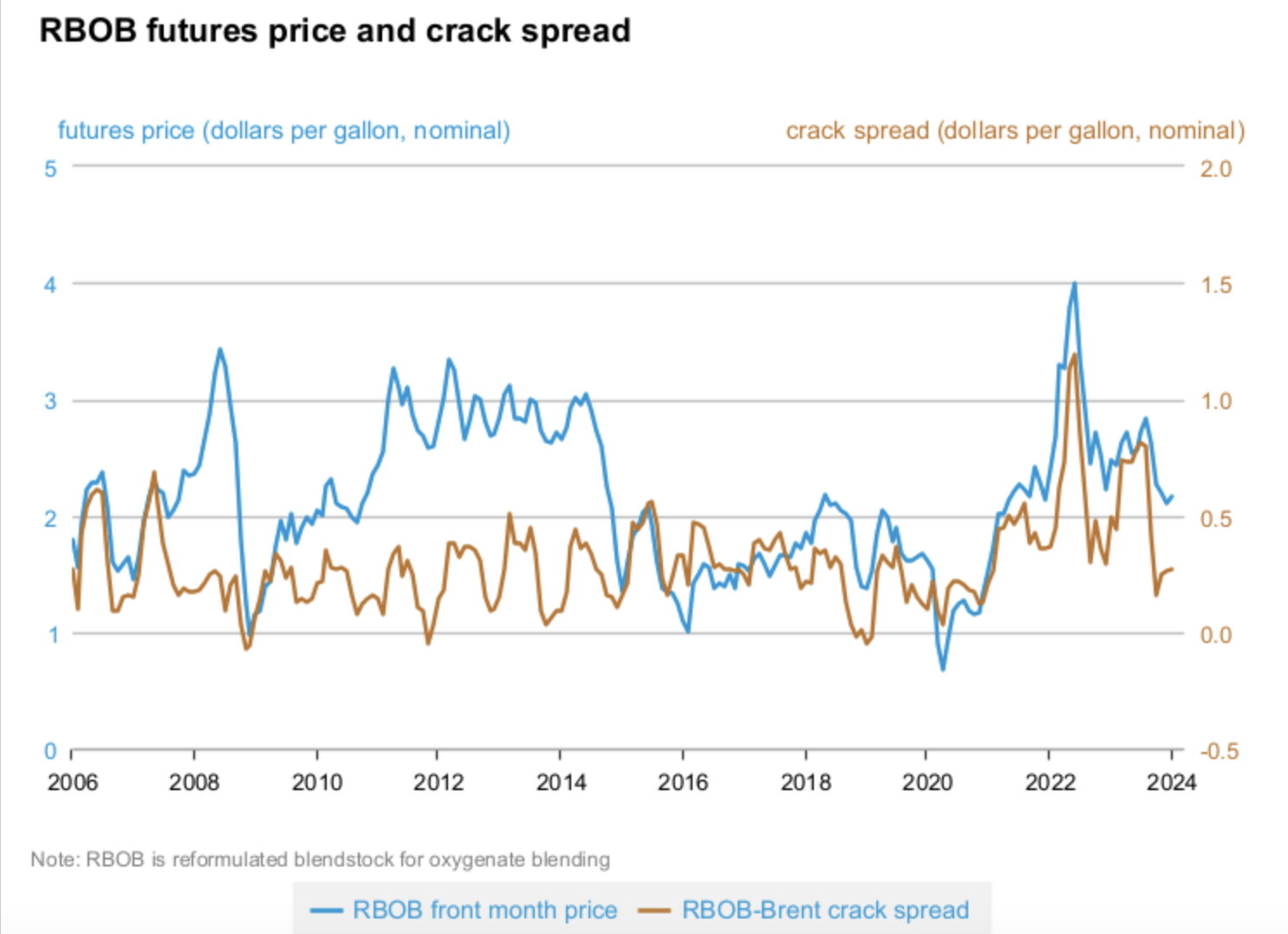

When it comes to the Refining segment, the picture is a bit more complicated. The refining industry is used to seeing tremendous volatility because the primary determinant of profitability is the spread between which the products produced by a player in that market are sold and the price of the crude oil and other inputs that go into making said products. This topic alone would be worthy of a significant amount of discussion. But for the sake of brevity, what you would be best knowing about is referred to as the crack spread. In particular, the 3:2:1 crack spread measures the difference between the purchase price of a barrel of crude oil and the selling price of the two barrels of gasoline and the one barrel of diesel fuel that should result from said crude going through the refining process.

Crack Spread

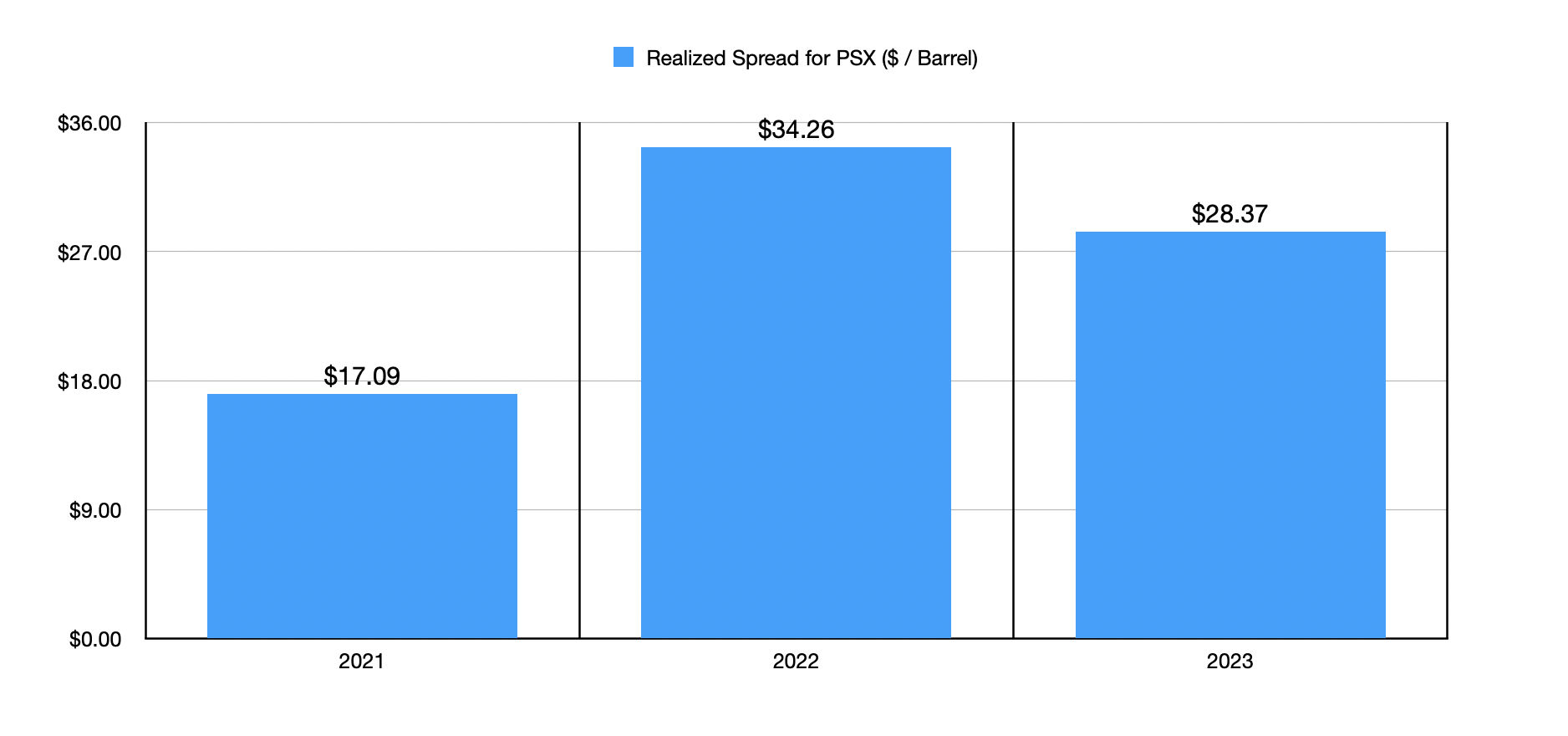

This kind of fluctuation based on changes in oil and gas prices allowed the company to go from generating a pre-tax loss of $2.35 billion under the Refining segment for 2021 to generating a profit of $7.82 billion the next year. Then, in 2023, profits fell to $5.27 billion. Normally, you would think that such wild fluctuations would be caused by significant variations in how much output the company can generate. But what we saw during this window of time was only a modest and consistent decline from 1.97 million barrels per day to 1.90 million barrels per day. This decline came even as capacity utilization globally went from 84% to 92% and was attributable largely to the company's decision, in the final quarter of 2021, to shut down its Alliance Refinery and to convert it into a terminal.

Author - SEC EDGAR Data

The reason for the fluctuations in profit, then, had to do with fluctuations in the crack spread. In 2021, this averaged $17.09 per barrel. It then shot up to $34.26 per barrel in 2022 before pulling back slightly to $28.37 per barrel in 2023. As the COVID-19 pandemic wound down and the global economy reopened, demand for end products started rising rather rapidly. Supply constraints caused by the conflict between Russia and Ukraine also played a role in this. Recently, there has been evidence that the crack spread is falling to some extent. But in all likelihood, this will prove to be temporary. OPEC+, for instance, is considering extending its voluntary oil production cuts, perhaps through the end of this year. And while there has been some refinery capacity growth globally as of late, current expectations call for global refining capacity to drop by about 24% by 2050 in order to meet emissions targets aimed at combating climate change. Naturally, this should prove bullish for companies that already have significant amounts of capacity. Attractive demand, restricted supply, and the prospect of additional capacity coming offline, all bodes well when it comes to talking about margins.

Author - SEC EDGAR Data

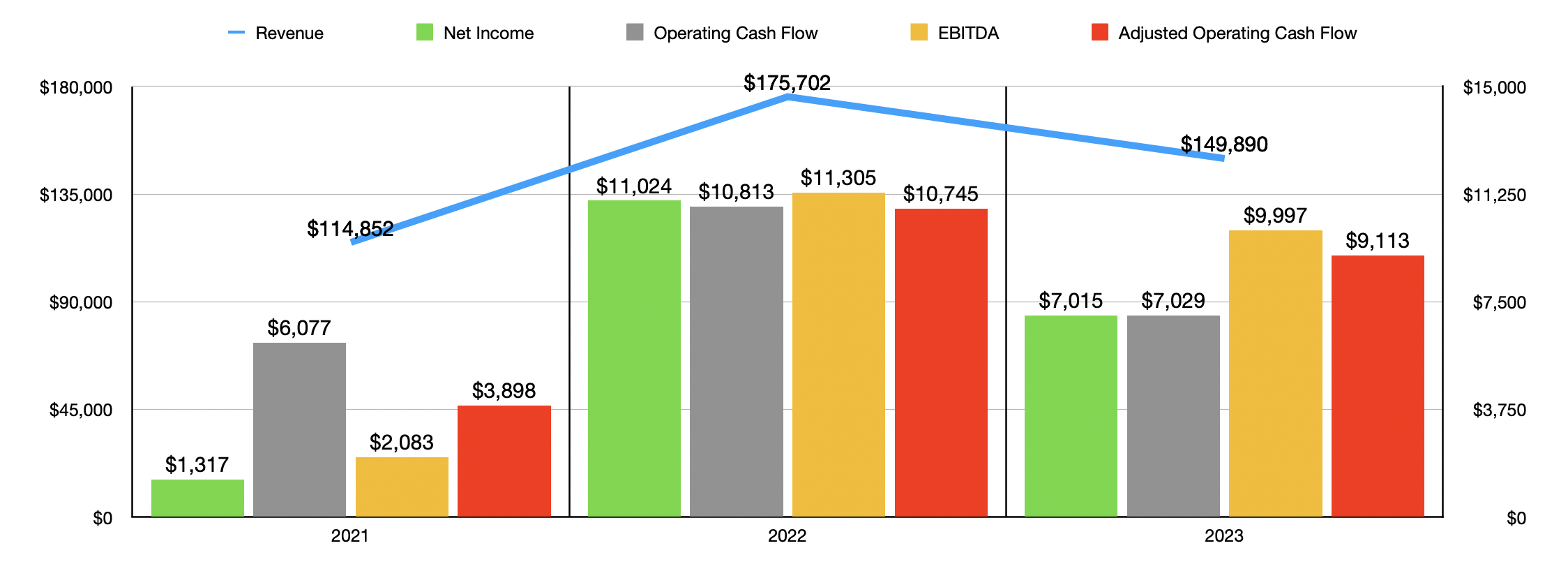

Even though it's probable that the fundamental picture for Phillips 66 and companies like it will remain favorable, at least for the foreseeable future, that does not change the fact that volatility will still be a very real threat for investors. Hopefully, that volatility will skew in the direction of creating additional value for shareholders as opposed to stripping away value. But there are no guarantees. If we do assume that the future will look fairly similar to what the past has been like, then shares of Phillips 66 look attractively priced. Using 2023 results, the firm is trading at a price to adjusted operating cash flow multiple of 7x while its EV to EBITDA multiple comes in just a bit higher at 8x. In the table below, I then compared the firm to five similar firms using these metrics. On a price to operating cash flow basis, I found that four of the five were cheaper than it. And when it comes to the EV to EBITDA approach, that same ranking held true. On a price to book basis, however, three of the five comparable firms ended up being cheaper than our target.

| Company | Price / Operating Cash Flow | EV / EBITDA | Price / Book |

| Phillips 66 | 7.0 | 8.0 | 2.03 |

| Marathon Petroleum (MPC) | 3.7 | 5.0 | 2.44 |

| Valero Energy (VLO) | 5.5 | 3.6 | 1.80 |

| Neste Oyj (OTCPK:NTOIY) | 8.7 | 11.7 | 2.57 |

| HF Sinclair (DINO) | 4.9 | 4.2 | 1.15 |

| Cosan S.A. (CSAN) | 3.1 | 7.3 | 1.88 |

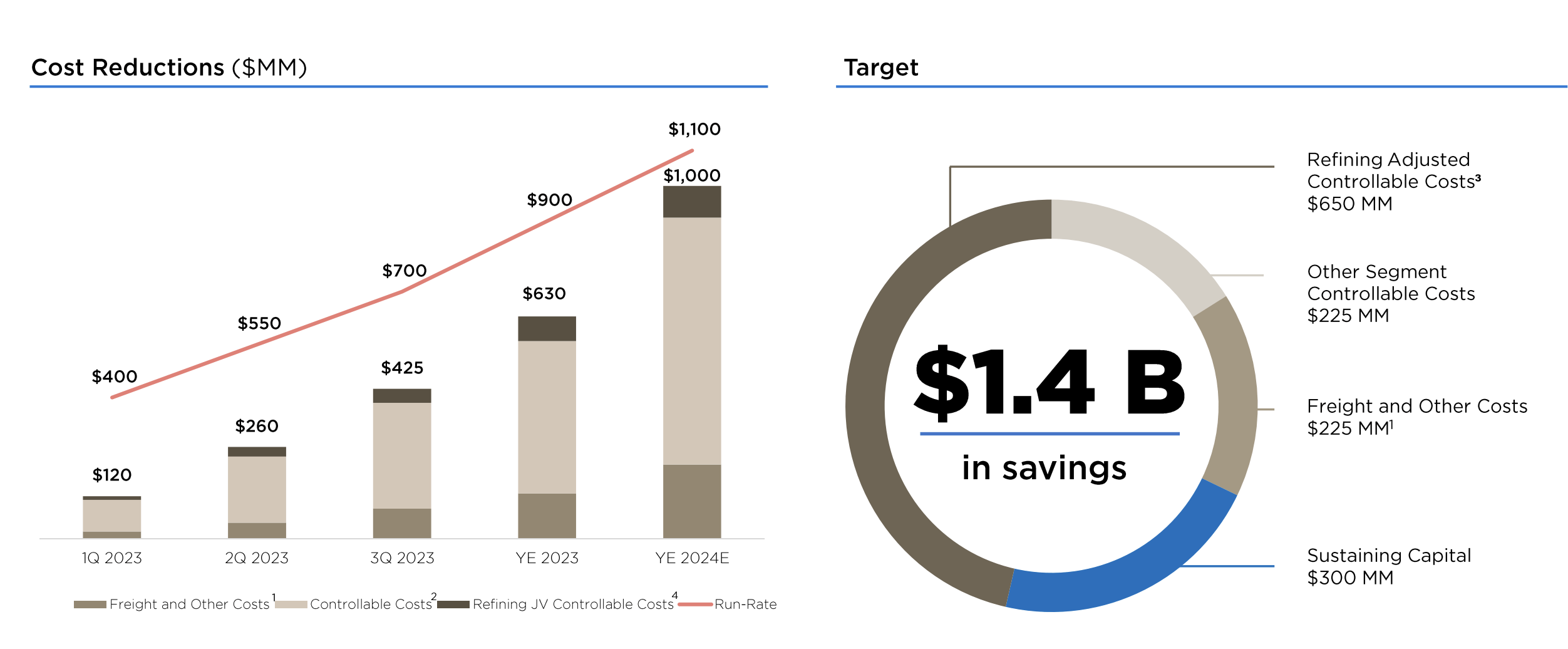

If your objective is to buy the cheapest opportunities in this space, it's clear that Phillips 66 is not an ideal prospect. However, there are reasons for investors to still remain bullish in the long run. First and foremost, management has a long track record of rewarding shareholders. Since July of 2022, the company has allocated $8.3 billion toward shareholder distributions. Their objective is to make aggregate distributions from that time through the end of 2024 total between $13 billion and $15 billion. With all that cash flowing out, the firm is also paying attention to how it can improve its bottom line materially. For instance, over the past year or so, the company has been working to achieve over $500 million in run rate cost savings associated with its refining operations. Other parts of the business are also being focused on as well from a cost perspective. The current target is for savings of at least $1.4 billion. Between $1 billion and $1.1 billion of this is expected to be achieved by the end of this year.

Phillips 66

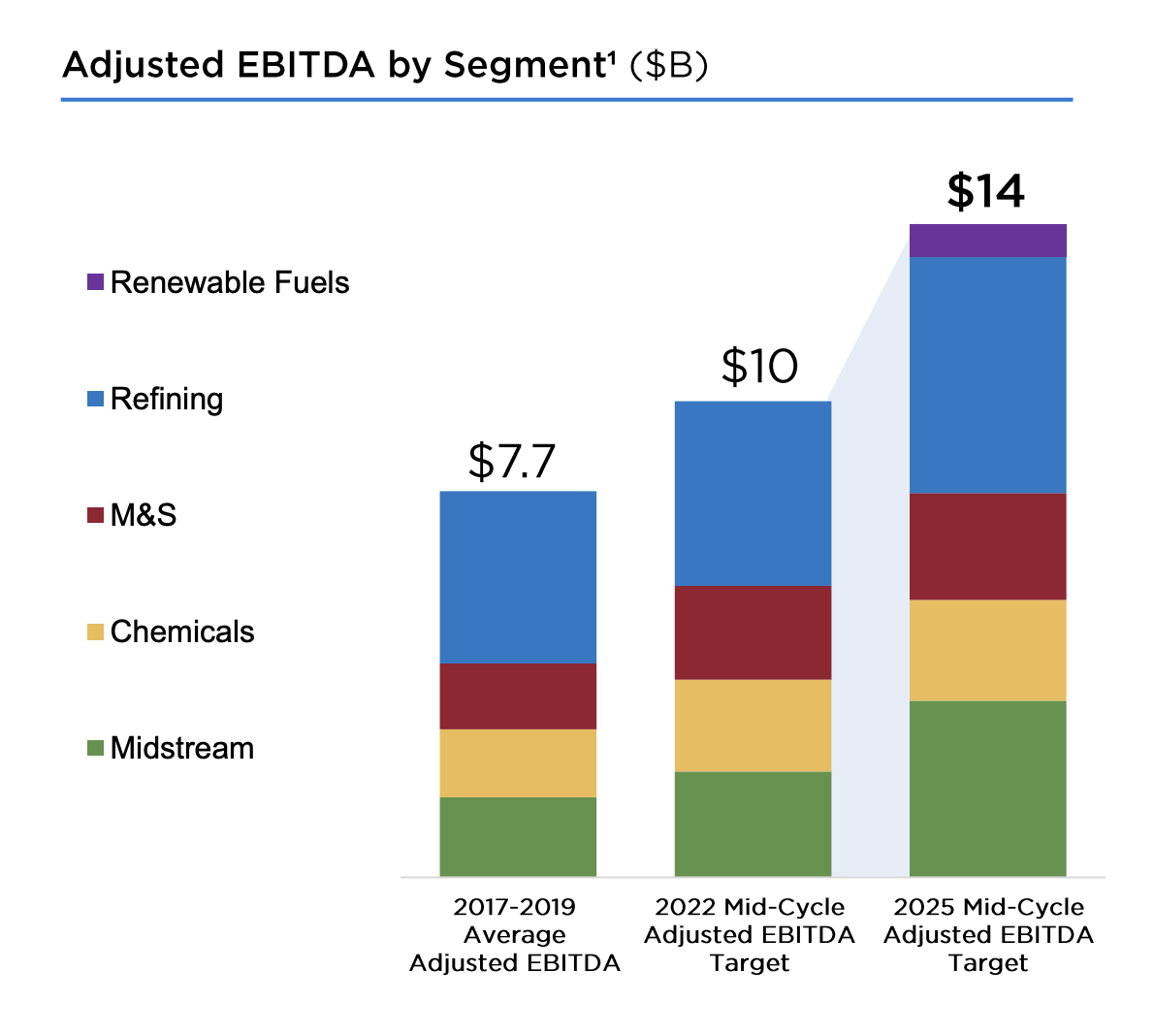

By focusing on costs across various parts of the business, management is hoping to push EBITDA for the company up to $14 billion by 2025. If this kind of improvement comes to fruition, then management intends to use over 60% of the cash flow that it has, after paying for planned dividends and sustaining capital, on things like share repurchases and other discretionary uses. Examples of discretionary uses include growth-oriented capital expenditures and debt reduction. With net debt as of this writing of $16.04 billion, cutting off a chunk of that would help to boost the bottom line considerably because of the reduction in interest expense. But of course, that would be balanced against the prospect of share repurchases. Since the company was spun off in 2012, it has allocated billions of dollars toward buying back 31% of all shares outstanding. That's impressive no matter how you cut it.

Phillips 66

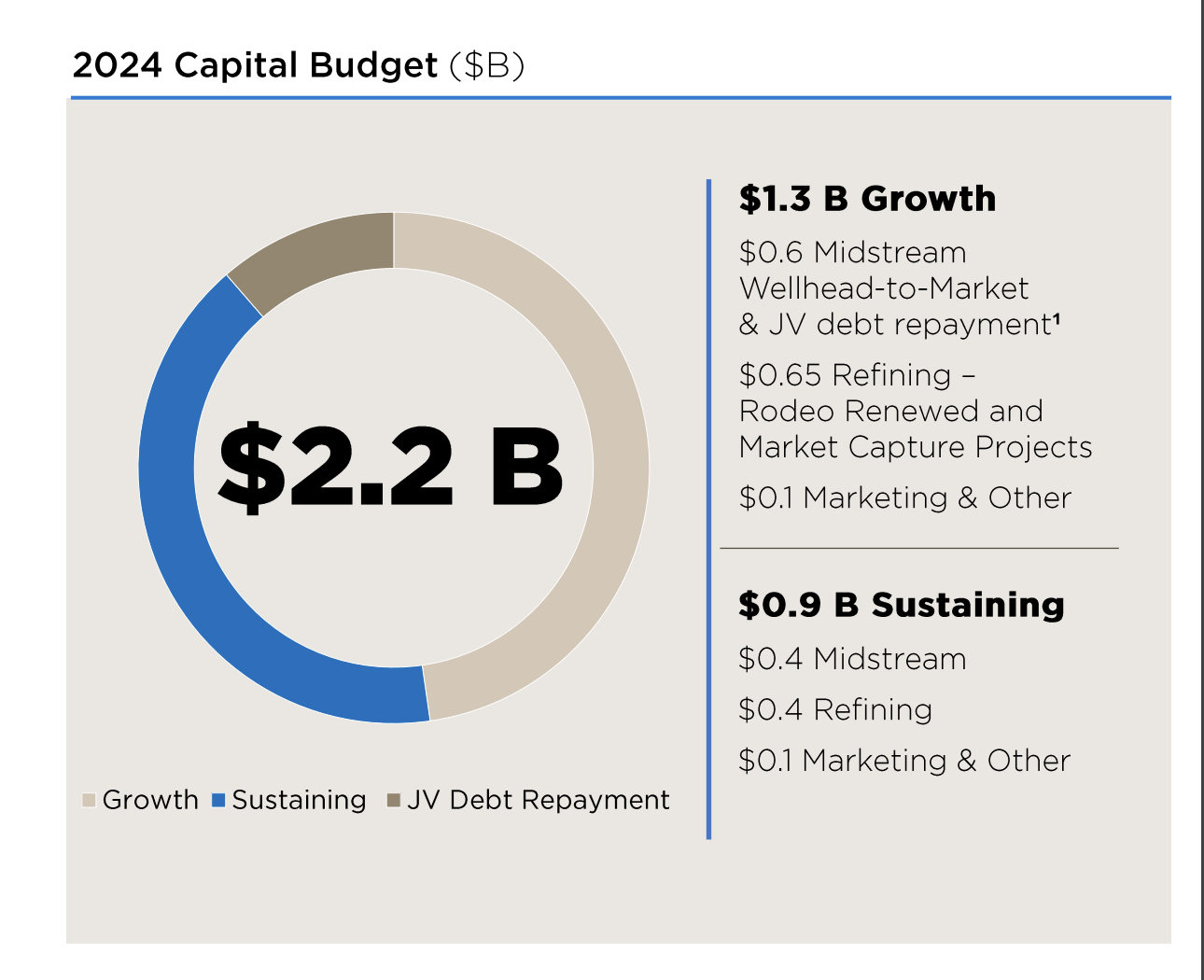

Personally, however, I have always favored growth, so long as that growth makes sense. And in recent years, the company has spent billions of dollars on growth prospects. Take the projections for 2024 as an example. Management intends to allocate around $923 million toward sustaining capital expenditures. The rest of the $2.2 billion that the company intends to allocate will be focused mostly on growth prospects, with around $600 million focused on Midstream Well-to-Market and joint venture debt repayments. Another $650 million would be focused on Refining activities, including plans to capture some additional market share. And the rest of the growth will be centered around marketing and other related activities.

Phillips 66

Is Phillips 66 a firm that's likely to generate such strong returns in the future that it can make you rich? Probably not. The company is priced a bit toward the high end of the spectrum relative to similar players. However, management has demonstrated time and again that this is a high quality operation we are dealing with. Significant cost-cutting plans should help to improve the picture even more. Add on top of this current market conditions, and I would argue that a soft ‘buy’ rating for the enterprise is still logical at this time.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.