JJ Gouin/iStock via Getty Images

JJ Gouin/iStock via Getty Images

How many of you are fans of old school NBA basketball and remember when the Utah Jazz were always a contending team for the championship? That's back when they had two legendary players in John Stockton and Karl "The Mailman" Malone. He received this nickname for his consistent delivery on the court night in and night out.

That's what I think of when assessing REIT Postal Realty Trust (NYSE:PSTL), a REIT that has delivered consistent dividends over the years. And in this article we'll discuss the company's dividend safety, balance sheet, and forward outlook, understanding why they may be a REIT income investors want to own.

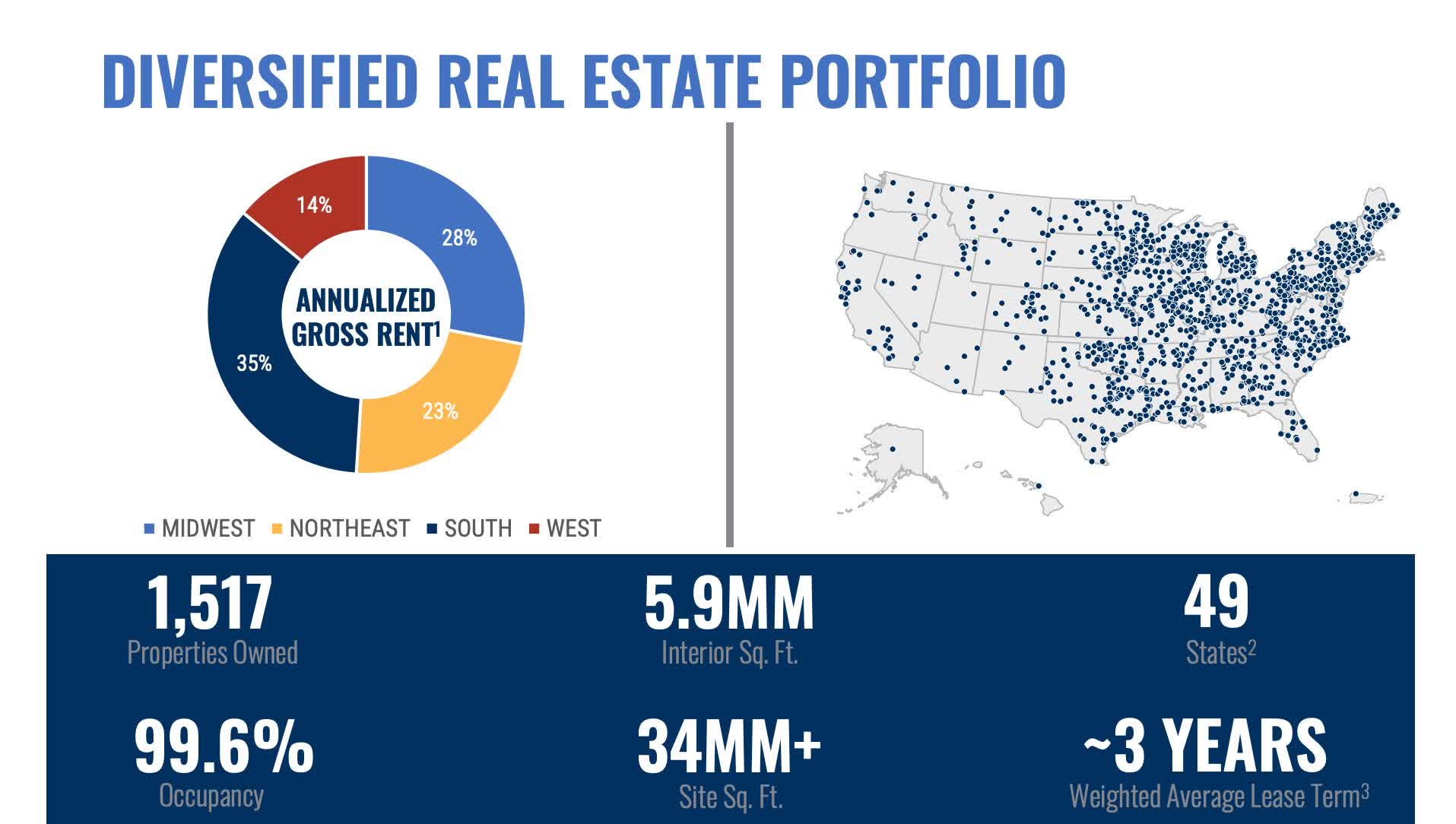

For those who may not know, Postal Realty Trust owns mission-critical properties such as post offices, primarily leased to the United States Postal Service, or USPS. The company owns more than 1,500+ properties across 49 states. I'm sure many of us constantly see them in our neighborhoods delivering our mail, which is a critical element of this country's logistics infrastructure.

And even though e-commerce has grown over the years with players like Amazon (AMZN), USPS continues to deliver to over 165 million unique points every day with the exception of Sundays. PSTL's portfolio represents 6% of the leased market with the next top 20 largest portfolio owners combined only owning 11%. Additionally, Amazon, UPS (UPS), FedEx (FDX), and DHL all tap in to USPS' logistics network daily. So, in short the REIT leases to a highly reliable tenant who is mission-critical to the nation's infrastructure.

PSTL investor presentation

PSTL closed out the year strong when they reported Q4 earnings at the end of February with a beat on FFO and revenue. FFO was $0.24 while revenue came in at $17 million. AFFO came in at $0.26. Revenue & FFO grew double-digits roughly 12% and 14% respectively while AFFO declined slightly from $0.27.

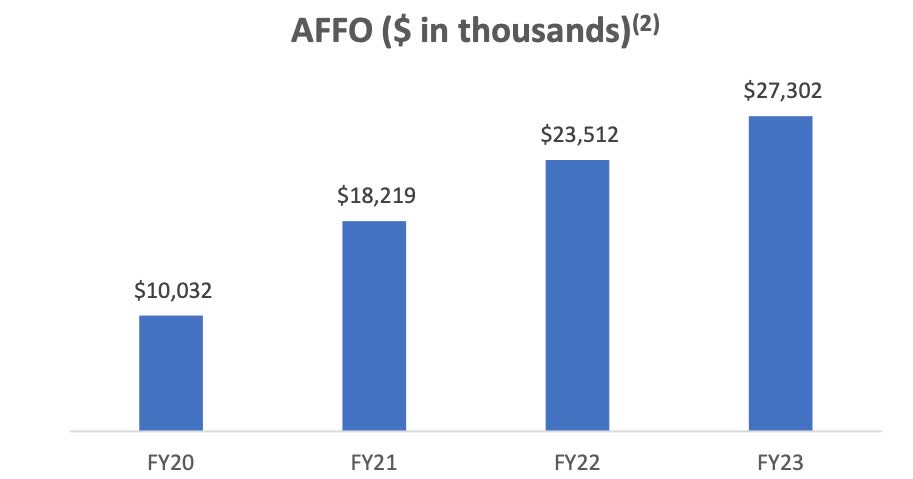

Despite the decline however, PSTL managed to grow their AFFO 6% year-over-year, totaling $1.01 for the full-year. FFO dropped slightly year-over-year from $0.96 to $0.94. Still a solid year overall considering the current macro environment. But looking at the chart below you can see PSTL has grown their AFFO, or adjusted funds from operations at a healthy rate over the past 3 years. And although FFO declined slightly, AFFO is the preferred method when measuring a REIT's financials and dividend safety.

PSTL investor presentation

The REIT had a wonderful year acquiring properties growing their portfolio and occupancy also remained strong at nearly 100%. During 2023 they acquired more than 223 properties totaling $78 million and 8 additional properties subsequent to quarter end. These had a healthy weighted-average cap rate of 7.7%.

And looking forward the REIT expects 2024 acquisitions in the same neighborhood, roughly $80 million. What impressed me the most about PSTL was that they managed to incorporate and negotiate strong rent escalators into their expiring leases at 3.5%.

Many may know most REIT rent escalators average roughly 1% - 2% annually, so this should support some strong rental revenue growth going forward. Their leases however aren't as long as some of their peers with a weighted-average lease term of 3 years while peers typically average 10+ years. Those like Essential Properties Trust (EPRT) leases tend to be much longer on average at roughly 14 years.

During my assessment this is probably the one metric that caused slight concern with the company. With a current payout ratio of 88.7%, this is higher than I like to see for REITs even though they are required to pay out most of their income in the form of dividends.

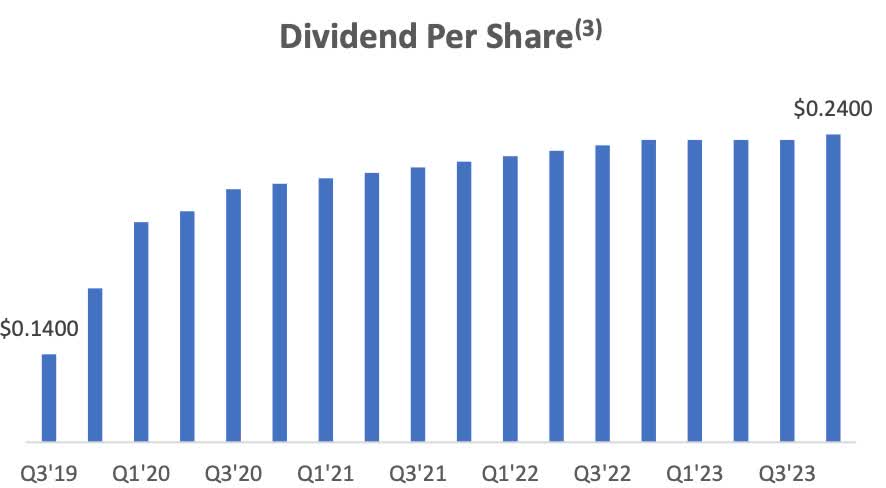

Some REIT peers like Realty Income (O) and Agree Realty (ADC) have payout ratios around 75% - 76%. NNN REIT (NNN), one of my favorites in my portfolio, has a AFFO payout ratio of 68.4%. Comparing them to office peers City Office (CIO) and Office Properties Income Trust (OPI), PSTL's payout ratio is much higher, but it should be considered that both of those peers cut their dividends recently. And PSTL has never cut their dividend since going public and raised it 71% since 2019.

And while this not overly concerning, it is something to keep an eye on going forward. But with the acquisitions the REIT has been making over the years, I suspect the gap will widen in the near to medium term. But to be fair they have delivered consistent growth and raised the dividend every year since IPO.

The recent 1% increase to $0.24 may have been disappointing and have slowed recently, but PSTL has delivered consistently every year just like the mailman. And I expect this to continue as they make accretive acquisitions. However, their payout ratio is something I'll be keeping close tabs on going forward.

PSTL investor presentation

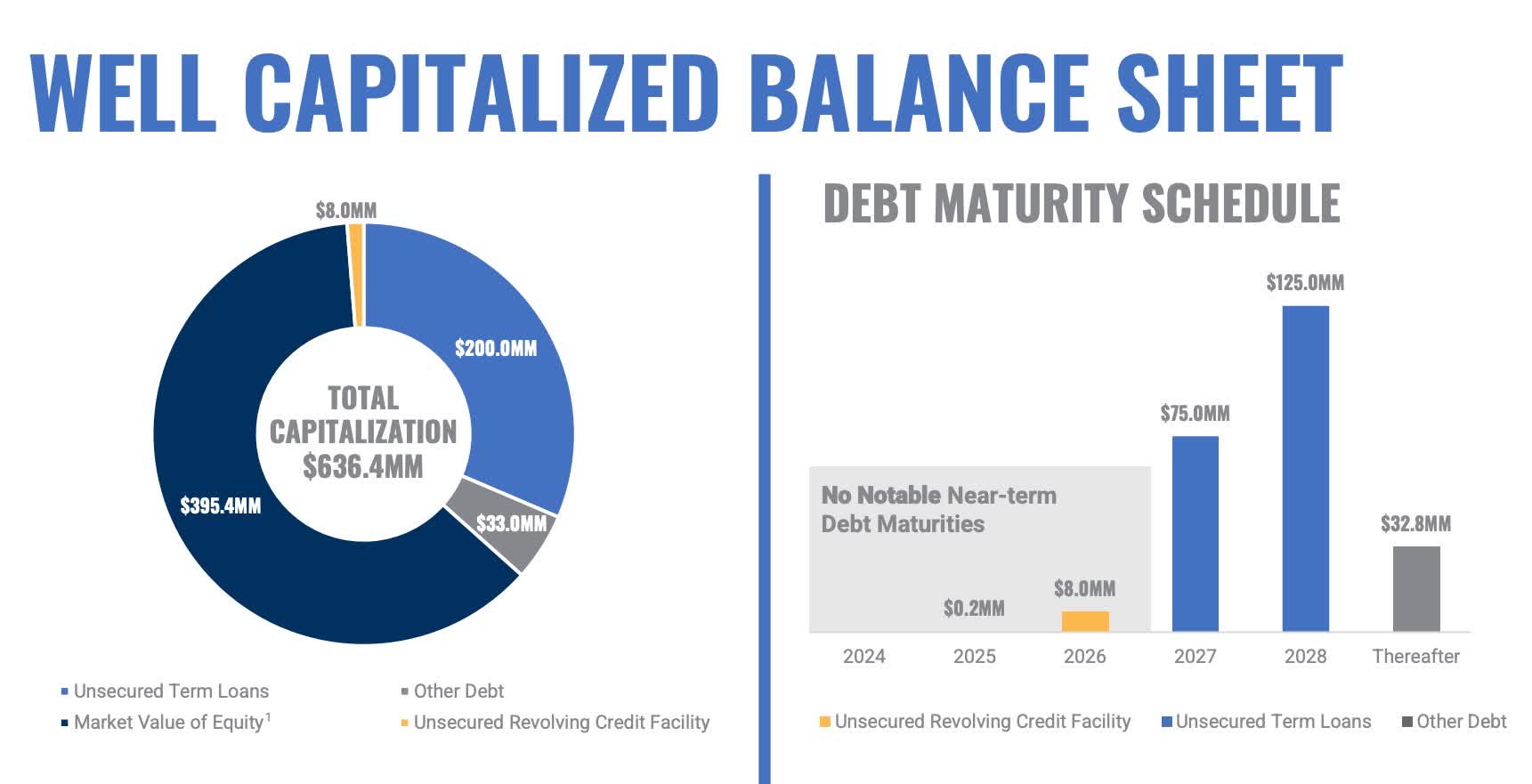

One way REITs can also support their dividend is by having a strong balance sheet. With ample liquidity and no debt maturities to worry about in the short term, REITs can pay their dividend from cash on hand if need be. PSTL's debt maturities are well-laddered with none maturing until 2027.

Furthermore, their net-debt-to EBIDTA was a healthy 5.6x with a fixed-charge coverage ratio of 4.3.x. This is similar to some retailer peers like Realty Income's 5.5x and W.P. Carey's (WPC) 5.6x. Comparing them to office peer City Office whose net-debt-to-adjusted EBITDA was 6.6x at the end of Q4, PSTL's balance sheet is more solid.

Additionally, most of this is fixed-rate with a weighted-average interest rate of 4.13%. And by the time PSTL has any notable debt due, interest rates will likely be much lower, so the REIT won't have to worry about refinancing any at much higher rates.

PSTL investor presentation

At the current price of $14 a share, I think PSTL is a good buy here. Considering their P/FFO of 14.8x and P/AFFO ratio of 13.08x trades below their 5-year average. The stock has had an P/AFFO as high as 19.6x, and if they can continue making accretive acquisitions growing their portfolio at a healthy rate, I think they can command a P/AFFO ratio of at least 14x -15x, giving them a fair value of $16.

Of course, this is all speculation and dependent on which way interest rates move in the coming months. This is also in-line with analysts' price target of roughly $16. Additionally, investors get a near 7% yield delivered while they wait for potential double-digit upside.

Seeking Alpha

The company has two main risks. First, interest rates which affects their cost of borrowing, in turn affecting cap rates making it more difficult to invest at attractive spreads. And second, their high payout ratio. With it near 90%, this means they have little margin for error and less cash to reinvest back into itself to grow internally.

If the economy experiences any sudden downturn which could impact company's operations, this could lead to a dividend cut. So far they've managed to grow it every year and though it is not overly alarming currently, this is something investors should keep a close eye on going forward.

Postal Realty presents a compelling opportunity at their current valuation. The REIT owns mission-critical properties and continues to make acquisitions to impressively grow its portfolio. Furthermore, they've managed to grow the dividend every year since IPO but growth has slowed in recent years.

And despite AFFO growing year-over-year, the current payout ratio is a bit high, giving them no margin for error. However, their balance sheet is solid and they don't have any debt maturities for the next 3 years, which puts them in a strong position financially. Although I'd like to see their payout ratio come down closer to 80%, for now I rate Postal Realty Trust a speculative buy.