imaginima

imaginima

Pure Storage, Inc. (NYSE:PSTG) delivered an enticing outlook for fiscal 2025 (the current calendar year) with its Q4 fiscal 2024 results. Note that PSTG's fiscal year and calendar year are misaligned.

What ignited the bull case for investors is that PSTG has found a path to increase its underlying profitability, while at the same increasing its growth rates.

Investors are asked to pay approximately 29x forward non-GAAP operating income for a business with about 8% of its market cap made up of cash, that's well positioned for reasonable growth in the next year and beyond.

There's a lot to like in this stock, and investors should be able to look back to $55 per share as a low price in the next several months.

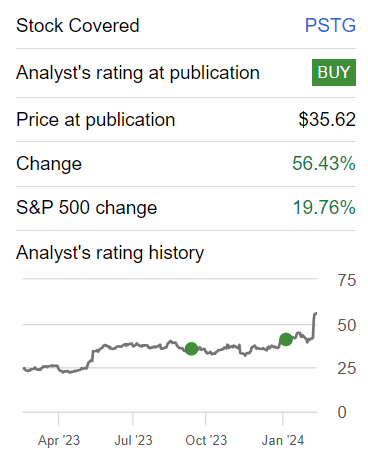

Back in January, I said in a bullish analysis:

The bull case for Pure Storage is found in its strong free cash flows, together with the fact that it holds close to $1.4 billion of net cash on its balance sheet.

Even though this investment thesis is not blemish-free, I contend that there's a lot to like in this name

Author's work on PTSG

As you can see above, PSTG has nicely outperformed the S&P 500 (SP500) since I first recommended it. However, I believe this trade is only now getting started. Here's why I'm bullish on this stock.

Pure Storage provides advanced data storage solutions. They focus on modernizing and simplifying how businesses store and manage their data. Pure Storage aims to offer high-performance and cost-efficient storage solutions. Their platform strategy emphasizes a unified operating environment, enabling customers to seamlessly handle data across various storage needs, from traditional systems to emerging technologies like AI.

Moving on, Pure Storage appears to be well positioned for solid growth in the near term, primarily driven by the successful expansion of its Evergreen portfolio.

The company's Q4 and fiscal 2024 performance reflects a solid trajectory, with sales momentum and balanced performance across theaters and product portfolios. The Evergreen portfolio, accounting for over 40% of total revenue, has seen substantial growth, particularly in the Evergreen/One and Evergreen/Flex categories, which more than doubled to over $400 million in total contract value sales.

Pure Storage highlights the hindrances that existing data storage environments pose to AI deployment and emphasizes the need for efficient access for unlocking AI's full potential.

Despite the promising outlook, Pure Storage faces certain headwinds too. A crucial challenge lies in the competitive landscape within the storage solutions market. As Pure Storage continues to expand its Evergreen portfolio and subscription services, it faces competition from other established players too, for example, NetApp, Inc. (NTAP).

Given this background, let's now discuss its financials.

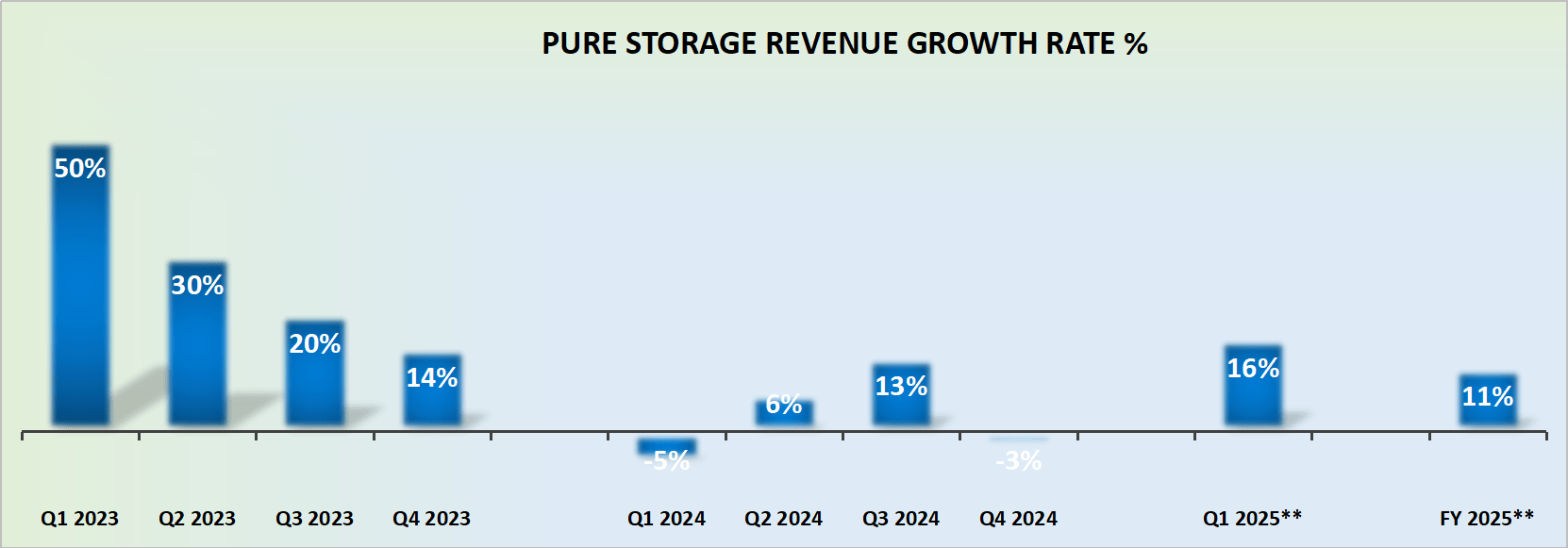

PSTG revenue growth rates

In my previous analysis, I said,

[Pure Storage is a] business that was previously expected to grow in a sustainable fashion by close to 15% CAGR per year. However, its fiscal Q4 2024 guidance appears to reflect sustainable revenue growth rates somewhere in the ballpark of 8% to 10% CAGR in the near term, rather than the mid-teens revenue growth rates I previously assumed.

That was the assumption that I was going with for fiscal 2025, revenue growth rates of approximately 9%. Therefore, when PSTG has now guided for approximately 11% CAGR, this means that this business still has some growth left in its tank.

It's difficult to say that this is a lot of growth. But it's all about the expectations. The expectation is that there's now more growth in this business than previous assumptions.

That being said, it isn't in its growth rates where this bull case is found. The bull case is found in the change in its underlying profitability. A topic we address next.

PSTG guides for Q1 2025 to see around 10% non-GAAP operating margins. For a business that just delivered 20% non-GAAP operating margins in Q4 2024, you'd be right to ponder, is that all that exciting?

And that's where things get interesting. Back in Q1 of the prior year, PSTG delivered 3.3% non-GAAP operating margins. This means that this time around, its non-GAAP operating margins will be approximately 700 basis points higher than 12 months ago.

On top of that, PSTG guides for about 17% of non-GAAP operating for fiscal 2025. Right away, one would like to believe that this is a conservative margin, meaning that perhaps 18% non-GAAP operating margins could end up being on the cards for fiscal 2025.

Therefore, investors are looking ahead and thinking that approximately $600 million could be on the cards at some point in the next twelve months, as a forward run rate.

This leaves the stock priced at 29x forward non-GAAP operating income. That's not so cheap, for a business that's growing at Pure Storage's rate. But it's far from expensive, either. Particularly, for a business that carries close to 8% of its market cap as net cash.

In conclusion, Pure Storage's fiscal 2025 outlook appears promising, driven by a combination of increased profitability and sustained growth rates. Investors are drawn to PSTG's attractive valuation, with the stock trading at approximately 29x forward non-GAAP operating income.

What enhances the bullish case is the substantial net cash position, constituting about 8% of the market cap.

The recent shift in underlying profitability, reflected in its expanding non-GAAP operating margins, signals positive momentum, making the stock an intriguing prospect.

Despite facing challenges, including competitive pressures and economic uncertainties, Pure Storage's strategic positioning and robust financials position it for continued success.

This is a good entry point for investors to consider.