Klaus Vedfelt

Klaus Vedfelt

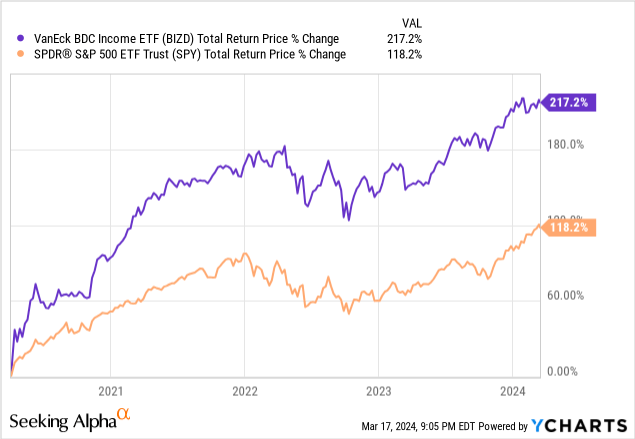

The VanEck BDC Income ETF (NYSEARCA:BIZD) has been on a strong run over the past four years, nearly doubling the total return performance of the S&P 500 (SPY) over that span:

The three big factors driving this massive outperformance are:

However, all three of these major tailwinds for BDCs over the past four years have either already disappeared or are very likely about to. As a result, we believe that BIZD's run of significant market outperformance is likely about to end. In this article, we detail why.

While BDC valuations have stood at discounted levels for much of the time over the past four years - thereby fueling strong total return performance through expanding valuation multiples - today they stand at fairly rich levels.

BIZD's top 10 holdings make up 75% of its total portfolio with the following breakdown:

However, all but FSK and PSEC among these holdings are trading at significant premiums to NAV and/or are trading at large premiums to their historical averages. FSK and PSEC, meanwhile, are both dealing with significant issues that at least somewhat justify their discounts. As a result, further multiple expansion on a sector-wide basis is highly unlikely at this point.

Another reason why BIZD is unlikely to outperform the broader market moving forward is that there is a greater than 50% chance that the Federal Reserve will cut its interest rate in June and the market expects several rate hikes by the end of 2024. Given that BIZD's underlying holdings invest primarily in loans with interest rates that float based on short-term interest rates, this will likely lead to a meaningful decline in net investment income, taking a bite out of the lucrative special dividends from BDCs in recent years that have helped to fuel their strong outperformance.

Last, but not least, in the case of funds like FSK and Oaktree Specialty Lending (OCSL), non-accruals have already begun to spike (FSK's surged from 2.4% to 5.5% on a fair value basis over the last quarter and OCSL's soared from 1.8% to 4.2% on a fair value basis over the last quarter), and the management of large and prestigious BDCs such as ARCC has warned that defaults are likely to spike across the industry this year:

we're likely to see defaults in the industry increase this year... you have some companies that are making interest payments but continue to live off revolver availability, cash, et cetera, but the liquidity is getting tighter and tighter. And so my expectation is that defaults will go up this year.

With the labor market showing signs of weakening as unemployment has now reached a two-year high and consumer spending also appearing to weaken with retail sails decelerating and overall growth halting in recent months and the yield curve remaining very inverted, the warning signals of an economic slowdown if not a recession are flashing. All of this implies that BDCs will likely be facing NAV and potentially even net investment income headwinds in the coming months and quarters.

BIZD's epic run of massive outperformance relative to the S&P 500 was fueled by its sky-high dividend yield, rapid net investment income growth (with accompanying lucrative special dividends from its underlying holdings) due to rising interest rates, significant valuation multiple expansion as COVID and economic fears cooled, and steady to even growing NAV due to resilient economic conditions over the past four years.

However, with short-term interest rates likely at their peak and expected to decline in the near future, valuations looking quite stretched in the sector, and deteriorating economic conditions and a likely rise in non-accruals and defaults for the BDC sector this year, it appears likely that BIZD's run of outperformance has come to an end. As a result, we have recently significantly reduced our exposure to the sector and are allocating our capital elsewhere into undervalued and more defensive sectors that are likely to benefit from falling interest rates such as utility (XLU), REIT (VNQ), and midstream (AMLP) stocks.