Toni M/iStock via Getty Images

Toni M/iStock via Getty Images

I became a dividend growth investor at the end of the Great Recession. Having watched my portfolio devastated multiple times over the years as I struggled to find the correct strategy, dividend growth investing just made sense. You see, the part that challenged me most was understanding my end goal - should I try to accumulate $1 million, $10 million, as much as possible?

Investing without a clearly defined goal in mind wasn't working for me. I needed something I could measure and see progress to keep me motivated. Thinking of my goals from a wealth standpoint didn't cut it. Once I shifted to a cash flow mindset, everything began to fall into place.

At the time, I had a well-paying, high-stress job. I don't have expensive tastes and recognized that replacing my work income with passive income would allow me to live the lifestyle I want on my terms. Finally, I had a goal that made clear sense and was easy to measure. I began exploring ways to create passive income, and dividend growth investing became a key component.

Today, I have four dividend growth portfolios: My IRA, which also contains my non-dividend companies; an ETF dividend growth portfolio created as an experiment; a taxable account that I put new capital in and also sell covered calls and puts; and the one I write about here.

This portfolio has been closed to new capital since 2016. I found that constantly adding new funds made it difficult to measure the overall success of the strategy. Dividend growth investing has been a raging success for me by probably the most important metric - I sleep well at night! I don't worry about even the tiniest amount of possible market crashes. The lack of stress is the best sign that dividend growth investing is right for me.

March 9th will mark the 15th anniversary of the stock market lows of the Great Recession. This was a turning point in my investing journey, and I expect to be better prepared next time we experience a recession.

The portfolio goals are simple: Grow the income by 10% annually with dividends reinvested and 7% annually without reinvesting. This goal allows my income to double approximately every seven years while reinvesting and every ten years after I begin withdrawing the dividends. It's important to know that this portfolio has been closed to new capital since 2016. The graph below shows the steady progress of income growth.

Wyo Investments

I use guidelines rather than rules to achieve my goals. Rules imply something hard and fast, whereas guidelines are flexible but give a general direction to follow. I keep these simple, as I have found that complexity adds time without any real benefit. These have evolved over the years, the most recent being the addition of selling covered calls in certain circumstances.

Again, these are just guidelines and are flexible to accommodate what makes sense to achieve my overall goals. I follow a few other items but don't see them as integral to my investing. Instead, these tend to be more personal preferences. They include avoiding foreign companies because I don't enjoy accounting for the taxes and FX rates causing fluctuating dividends.

As of the end of the month, I am only projecting income growth for the year of 6.4%. This has ticked up slightly from last month and from my 2024 Look Ahead. The beginning of the year always starts low because I do not project forward dividend reinvestments. However, this year is looking exceptionally light compared to other years, primarily due to some sales last year that I still need to reinvest, but I am also expecting slower dividend growth this year in many companies.

As I mentioned in the 2024 look ahead, the portfolio is due for a down year in dividend growth as the income growth has gotten well ahead of the 10% growth projection that I have seen to be consistent. Even with the current estimate for 2024, the income is still above the long-term trend.

While I have no goals for the total return of the portfolio, many readers are interested, so I report it monthly. Year to date, the portfolio is up 3.6%, lagging the S&P 500 by a considerable margin.

February is the busiest month of the year for increases, with seven last month in this portfolio.

PepsiCo is unusual because it typically pays out twice in the first quarter of the year and none in the fourth quarter. They also announced a dividend increase in February that won't pay out until June. So investors must wait a while to see the 7.1% dividend increase.

This increase will mark the 52nd year of dividend increases for PepsiCo. The company has consistently held its increases around the 6-7% mark, never dipping below 5.5% in the past decade, with some as high as 13%.

In early February, CME announced a 4.5% increase in the quarterly dividend. This was below my expectation of 10%. Because CME pays an annual special dividend, it is difficult to say what the total increase for the year will be. However, if the special dividend matches last year, the company's forward yield sits at a healthy 4.5%.

As a twin holding to CME, Intercontinental Exchange manages its considerable cash flow differently than CME. Whereas CME tends to pay out all the cash to investors, ICE prefers regular acquisitions with debt and deleverage afterward. This has been a successful strategy for the company over many years and acquisitions.

On February 7th, the company announced an increase of 7.1%, considerably below its 5- and 10-year averages of just under 12%. This isn't entirely surprising as earnings growth has slowed in the last couple of years but is expected to tick up again.

Home Depot will extend its dividend growth streak to fifteen years, with its most recent increase of 7.7%. The increase is well below its five-year dividend growth rate of over 15%, but it is better than expected.

While Home Depot has been increasing its dividends since the Great Recession, it never cut during that time. According to the company website, it has paid dividends since 1987 without a dividend cut.

Prudential is a slow and consistent dividend growth company. In February, the company announced a 4% dividend increase. This increase was in line with its last few, although below its five-year average of just under 7%.

Best Buy announced a 2.2% dividend increase on the last day of the month. This was below my expectation in the 5% range. The company is still experiencing a hangover from the pandemic boom they experienced. While next year could be another rough year for the company, things will begin to normalize as electronics age out after that.

Last month, SPG raised the dividend by 2.6%, marking the ninth increase since cutting the dividend during COVID-19 in 2020. While the current quarterly dividend is still below the dividend at the time of the cut, it is rapidly gaining and could match it in 2025.

While the first two months of the year bring a flurry of dividend increases, March is an unusual month with no expected increases for the portfolio. In fact, of the 110 companies I track, Williams-Sonoma (WSM) is the only company with an expected March increase, so March is a slow increase month across the board.

In January, I made an unusual move and sold half my position in Omega Healthcare Investors (OHI). I have held OHI since building the position in 2015 and 2016 at an average purchase price of $27.01. This is the second time I have halved the position, with the first being in 2019.

The sale wasn't because I was particularly pessimistic about OHI's future. We have seen regular negative articles on OHI since 2017, and the dividend has been chugging along just fine. However, there is much more risk with the company than a company like Enterprise Products Partners (EPD). I am also working to reduce the size of riskier positions that lack any dividend growth.

At the time of the sale, OHI accounted for about 3% of the total income in the portfolio and was the number ten income producer. The sale will put it right around the middle of the pack for income production, a level I am much more comfortable with for the risk.

The downside with selling a company yielding 8.5% is that the replacements are limited, at least without taking on similar or more risk. However, I would rather have the risk spread out rather than concentrated in one company like it was before. I plan to use the proceeds to start a position in Blackstone Secured Lending (BXSL), which, with a higher yield, should allow me to use part of the proceeds to add to stronger dividend growth companies.

While I keep saying I am committed to reinvesting at least half the dividends and holding the other half as cash, I am having trouble putting this into practice. Everything is just too expensive! I'm even struggling with making replacement purchases, for which I am less concerned about price. Instead of making purchases, I continue to see my cash pile grow to record highs, yielding a solid 5% in money market funds as I wait for a decent correction.

During February, I continued to work on replacing the Walgreens (WBA) I sold in December. For the month, I added 13 shares of EPD at an average cost of $26.35. So far, about 33% of the proceeds from the sale have been reinvested.

The remaining cash from the WBA sale, coupled with the OHI trim, leaves me with many replacement purchases to make. However, as high yield looks overvalued, I am being measured with my replacement purchases.

While I focus on getting bargain prices with my reinvestment purchases, I have loosened my requirements currently. This is primarily because of my commitment to reinvest half the dividends, although cash yielding 5% isn't a bad place to wait for better prices. Below is a table of the regular purchases made during February.

The Aflac (AFL), Snap-on (SNA), and Automatic Data Processing (ADP) purchases were all made around 10% above the price I consider a good buy. PepsiCo was purchased at a 3.2% forward yield on the June dividend, which is a good but not great yield for the company. These companies are strong dividend growers going forward, and I am willing to reach a bit for them.

While the market as a whole seems expensive to me, there are a surprisingly large number of companies that I track showing up as potential buys. Of course, some of these are due to the recent dividend increases, as I use dividend yield as my primary indicator.

After NextEra Energy (NEE) announced its most recent increase and guidance, I initiated a position in one of my other portfolios. I still don't think it's a screaming buy, but it is one of the better dividend growth companies. It becomes only the second utility I hold across all my portfolios, along with Duke Energy (DUK) in this portfolio.

One of my speculative picks, Nexstar Media Group (NXST), announced a 25% dividend increase last month and is again yielding above 4%. Even with the raise, the company maintains a low payout ratio, paying out around 15% of its operating cash flow. I am considering adding to my position, which I established last time it was yielding above 4%. NXST should be considered a speculative company as it only has a BB+ credit rating.

In the same area as Nexstar, Comcast (CMCSA) has quickly climbed up my list of bargains and is now yielding close to 3%. Comcast might be a hated company, but it has solid and consistent earnings growth and is an excellent buy at its current price. The FAST Graphs below shows its relative undervaluation to its historical PE ratio.

FAST Graphs

A company that has climbed my list over the last few months is MarketAxess Holdings (MKTX). The company is offering the best yield in over a decade. However, getting excited about it at a PE of over 30 and low dividend growth in the last couple of years is hard. Investors buying today are betting on a return to faster growth, which analysts believe is coming. I'm just not sure there's enough growth to justify paying 30 times earnings.

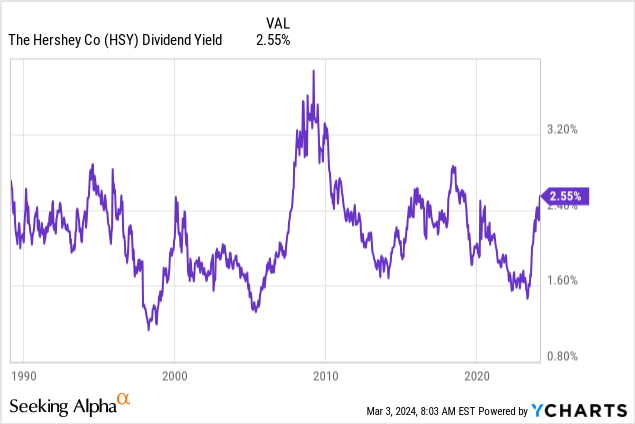

Another company that climbed up my list rather quickly, primarily due to its February increase, is Hershey (HSY). I rank Hershey highly overall due to its 5- and 10-year dividend growth rates of 9% and its flat payout ratios. The chart below shows that the company has rarely reached the 3% yield mark. While the next few years could see slower earnings growth, today's forward yield of 2.9% looks like a good entry point.

It really feels like we are reaching the irrational exuberance stage of the market. But let's not forget the markets felt this way in 1999 before adding much more before the bust in 2000. Still, it feels like we are in something unsustainable. Maybe with all the automated 401K investing, the markets can never drop again? What happens when the algorithms get caught in a down cycle? Will it lead to ever-crashing prices?

I have been buying some high-yield positions and talking about buying others for the last few months. Normally, I would consider today a bad time to be buying these. They are yielding less today than they did when interest rates were at zero. With cash at 5% today, getting a 10% yield on a high-risk investment is just poor risk management, in my opinion. Of course, each individual investor has their own needs and overall risk to manage.

The high-yield purchases I have discussed are only to replace income from sales, and I am only investing as much as necessary to replace the income. As I do so, I will hopefully keep my risks down and place a portion of every sale into high-quality dividend growth companies. The time to chase high yield is when the markets are crashing as they all get treated as if they are going out of business.