ProPhase Labs, Inc. (NASDAQ:PRPH) Shares Could Be 29% Above Their Intrinsic Value Estimate

Key Insights

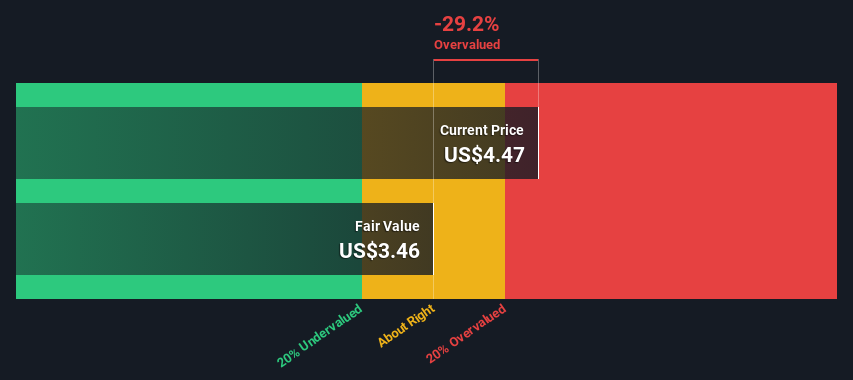

-

The projected fair value for ProPhase Labs is US$3.46 based on Dividend Discount Model

-

ProPhase Labs is estimated to be 29% overvalued based on current share price of US$4.47

-

The average discount for ProPhase Labs' competitorsis currently 35%

Today we will run through one way of estimating the intrinsic value of ProPhase Labs, Inc. (NASDAQ:PRPH) by projecting its future cash flows and then discounting them to today's value. Our analysis will employ the Discounted Cash Flow (DCF) model. Before you think you won't be able to understand it, just read on! It's actually much less complex than you'd imagine.

We would caution that there are many ways of valuing a company and, like the DCF, each technique has advantages and disadvantages in certain scenarios. For those who are keen learners of equity analysis, the Simply Wall St analysis model here may be something of interest to you.

Check out our latest analysis for ProPhase Labs

Crunching The Numbers

As ProPhase Labs operates in the pharmaceuticals sector, we need to calculate the intrinsic value slightly differently. In this approach dividends per share (DPS) are used, as free cash flow is difficult to estimate and often not reported by analysts. This often underestimates the value of a stock, but it can still be good as a comparison to competitors. We use the Gordon Growth Model, which assumes dividend will grow into perpetuity at a rate that can be sustained. For a number of reasons a very conservative growth rate is used that cannot exceed that of a company's Gross Domestic Product (GDP). In this case we used the 5-year average of the 10-year government bond yield (2.3%). The expected dividend per share is then discounted to today's value at a cost of equity of 6.0%. Relative to the current share price of US$4.5, the company appears slightly overvalued at the time of writing. Valuations are imprecise instruments though, rather like a telescope - move a few degrees and end up in a different galaxy. Do keep this in mind.

Value Per Share = Expected Dividend Per Share / (Discount Rate - Perpetual Growth Rate)

= US$0.3 / (6.0% – 2.3%)

= US$3.5

Important Assumptions

The calculation above is very dependent on two assumptions. The first is the discount rate and the other is the cash flows. You don't have to agree with these inputs, I recommend redoing the calculations yourself and playing with them. The DCF also does not consider the possible cyclicality of an industry, or a company's future capital requirements, so it does not give a full picture of a company's potential performance. Given that we are looking at ProPhase Labs as potential shareholders, the cost of equity is used as the discount rate, rather than the cost of capital (or weighted average cost of capital, WACC) which accounts for debt. In this calculation we've used 6.0%, which is based on a levered beta of 0.800. Beta is a measure of a stock's volatility, compared to the market as a whole. We get our beta from the industry average beta of globally comparable companies, with an imposed limit between 0.8 and 2.0, which is a reasonable range for a stable business.