Khanchit Khirisutchalual

Khanchit Khirisutchalual

Progress Software Corporation (NASDAQ:PRGS) will report Q1 ’24 earnings on the 26th of March after the market closes. I wanted to go through what the company expects out of the quarter and what the analysts are estimating it will do. Furthermore, I will comment on the company’s outlook and how it may have changed since the last time I covered it back in December.

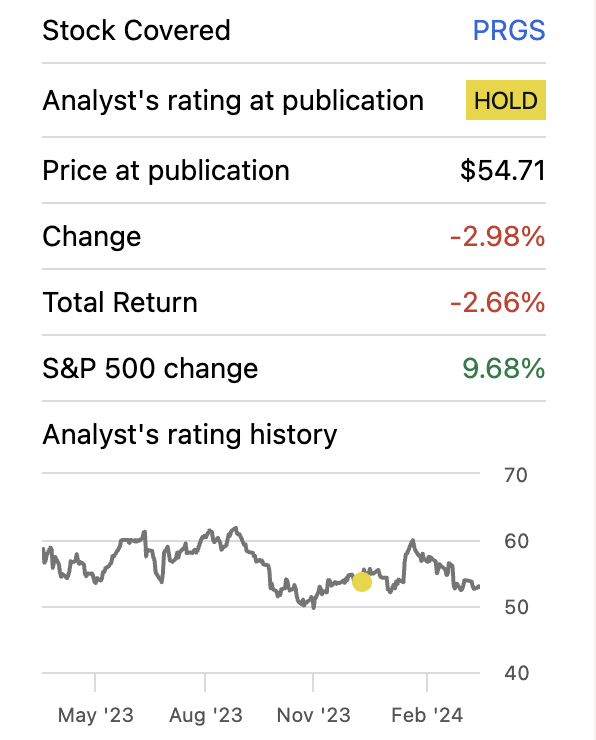

As I mentioned, the last time I covered the company was in mid-December ’23, when I assigned the company a hold rating due to its inability to improve its margins. It was not an attractive investment on GAAP and non-GAAP basis. Since that article, the company saw its share price pump to around $60 a share, only to come back down and currently down around 3%, compared to around a 10% gain on the S&P 500 index (SP500).

Company performance since last coverage (SA)

The company expects revenue to be between $180m to $184m, while EPS to be $1.12 to $1.16 a share. For the full year, the company expects to do between $722m to $732m in revenues, and between $4.58 to $4.68 in EPS. Furthermore, the management expects the operating margin to be between 39% to 40%, while free cash flow to be between $202m to $212m. Just to note, the EPS and operating margin numbers are non-GAAP, as that is what the company chose to focus on. GAAP EPS is much lower than its non-GAAP, which I don’t necessarily like but will go with the company’s preferences.

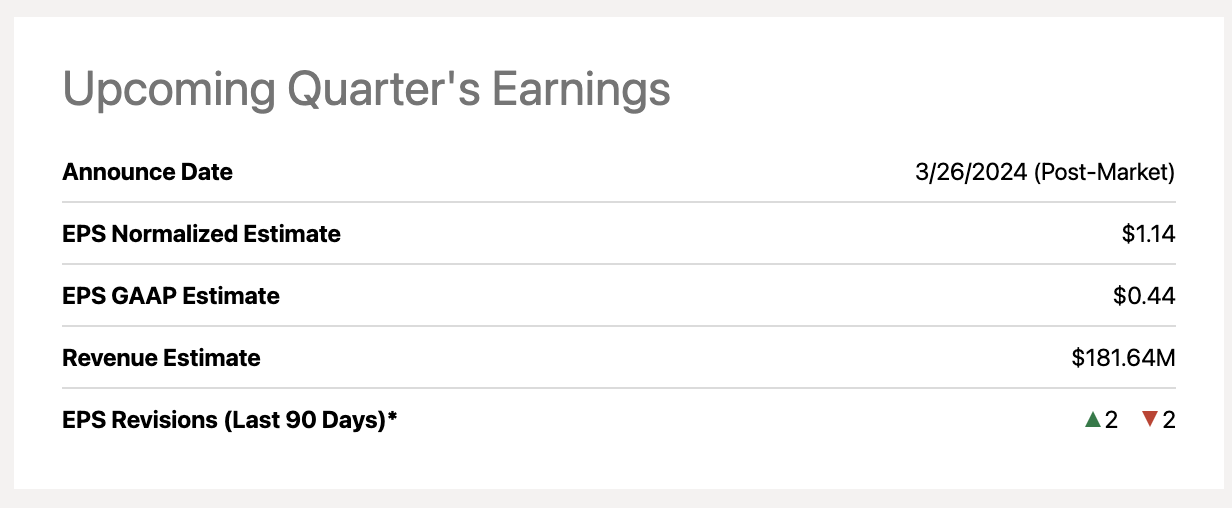

So, how do these numbers stack up against analyst estimates? Analysts are expecting around $181.64m in revenue, $1.14 of non-GAAP EPS, and $0.44 on a GAAP basis. So, analysts are expecting the mid-point of the company’s guidance for the upcoming quarter, which is a safe bet. For the year, analysts are expecting around $728.5m in revenues and $4.64 in non-GAAP EPS, which are also at the mid-point of the company’s estimates.

Upcoming Earnings Estimates (SA)

These results are not the most outstanding, with around 3% to 5% growth on the top line and the usual large deviation from GAAP metrics due to stock-based compensation, amortization of intangibles, and some other small adjustments related to acquisitions and restructuring. Comparing the top-line growth to the previous quarter, we can see it has slowed down quite a bit. In Q4 ’23, the company saw 11.5% y/y growth, which is quite a slowdown, however, it is around 10% y/y growth.

The company’s acquisition of MarkLogic last year is yet to bear fruit in the broad term. Sure, it has added some inorganic top line growth, however, to fully integrate it with its current offerings is going to take much longer than the management anticipated (according to the transcript), so I can understand the subpar sequential growth for now. This longer-than-expected time to gain value may weigh on the company’s margins also, so I wouldn’t be surprised if we see further margin deterioration, especially in GAAP terms. The company is looking to generative AI tools that will help their customers’ businesses, however, it all is quite experimental still, so I doubt we will see any substantial growth in that area right now.

In the previous article, I mentioned the potential of further M&A activity, and in the last earnings call, the management said they have been very active in this space, and said no to a lot of companies that didn’t meet their criteria or didn’t have enough synergies with their current offerings. However, the management is very confident that the company will do at least one acquisition in FY24.

A MOVEit data breach is still ongoing. The data breach was noticed sometime in May of 2023, and the company is still dealing with the backlash of the issue. Any further legal issues concerning MOVEit will affect the company’s operations negatively, in terms of litigation fees, loss of customers, and even reputation. In the last earnings call, the company said that it managed to retain most of its customers, which is a good sign, however, the company is still being hit with legal consequences of the breach, and there may be more over the year, which may weigh on the company’s share price in the short run.

I believe that there will be quite a few uncertainties for the next year in terms of the company’s efficiency and profitability, which are not set in stone yet, due to further implementation of MarkLogic and the aforementioned data breach incident. There will be further costs associated with the two mentioned items, which will weigh on the company’s GAAP metrics further, and will deviate further from its non-GAAP measures.

I would like to see GAAP metrics starting to improve and to see how the legal issues develop over the next year before I would consider starting a position. Furthermore, I would like to see the real potential of MarkLogic coming through, which will hopefully rejuvenate the company’s top-line growth. I am also excited to hear what the company is going to acquire next and how that will help its top line growth. Maybe we will hear some more news on the M&A front in the upcoming earnings call.

I am keeping my hold rating on Progress Software Corporation stock for now. I don’t think my stance will change over the next couple of quarters unless the company can show substantial improvement in its operations and legal issues are fully behind them, as this is very hard to model. The legal fees could be massive, so it is not an ideal time to start a position right now, especially when the company has such a negative sentiment toward it.