JHVEPhoto

JHVEPhoto

Earnings of Pacific Premier Bancorp, Inc. (NASDAQ:PPBI) will most probably decline this year because the average loan balance will be lower in 2024 compared to 2023. I'm expecting the company to report earnings of $1.81 per share for 2024, down 20% from last year's adjusted earnings. PPBI is offering quite an attractive dividend yield of over 5%. However, the December 2024 target price is close to the current market price, implying a small upside. Following the strong stock price rally over the last few months, I'm downgrading Pacific Premier Bancorp to a Hold rating.

Pacific Premier Bancorp reported a large loss of $1.44 per share for the last quarter of 2023 because of balance sheet repositioning. Under this repositioning strategy, Pacific Premier sold a large part of its securities portfolio that had racked up significant unrealized mark-to-market losses as interest rates had risen over the last two years. Pacific Premier booked a loss of $254 million on this sale, according to details given in the earnings release. On the plus side, this sale had an immediate positive impact on the net interest margin as the proceeds from the sale brought down expensive borrowing. The margin grew by 16 basis points in the last quarter, after falling by 49 basis points in the first nine months of 2023.

The management has planned further balance sheet changes for the first quarter of 2024, as mentioned in the conference call and quoted below.

For the first quarter, we expect further balance sheet optimization through a combination of lower cash levels and a reduction in higher cost wholesale funding, namely, we expect both broker deposits and FHLB advances to trend lower from year-end levels. We believe the combination of these items will help partially mitigate net interest margin pressures in the first quarter."

Therefore, balance sheet changes will likely continue to support the net interest margin this year.

On the other hand, the margin will face pressure from interest rate cuts. Based on the Fed's projections, I'm anticipating 50-75 basis points Fed funds rate cuts in 2024. As can be gleaned from the details on fixed, variable, and adjustable-rate loans given in the latest presentation, only around 27.8% of PPBI's existing loans will re-price after one year; all other loans will re-price within a year. Therefore, the company's asset yield can be expected to be quite sensitive to interest rate cuts this year.

On the liability front, around 48% of deposits are either non-interest-bearing or certificates of deposits; therefore, their cost will be sticky this year. Considering the loan and deposit mixes, I believe the net interest margin will be marginally sensitive to interest rate cuts in 2024.

Overall, I'm expecting the margin to increase by twelve basis points in the first half of the year and then remain mostly flat in the second half of the year.

The loan portfolio size remained somewhat flat in the last quarter of 2023 after five straight quarters of decline. The management mentioned in the conference call, "For the foreseeable future, we see pretty muted demand."

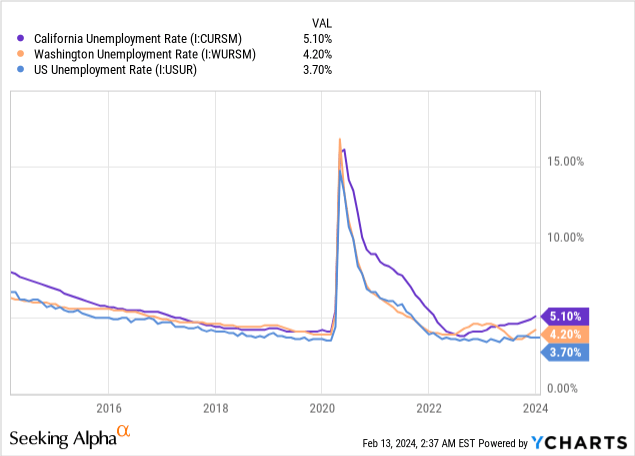

The management's guidance is not surprising considering economic factors. Pacific Premier mostly operates in the states of California and Washington, with some presence in Oregon, Nevada, and Arizona as well. The labor markets of both California and Washington have worsened over the last few months (see below), which shows that regional business activity is headed in the wrong direction. The economic slowdown bodes ill for credit offtake in the region and, consequently, Pacific Premier's loan growth.

As a result, I'm expecting minimal loan growth for 2024. In the past, Pacific Premier has relied on acquisitions for growth; however, as the company has not made any related announcements so far, I have decided to exclude M&A options from my investment thesis. I'm expecting the company to report loan growth of just 0.40% in 2024. As loans will be flattish this year while they sharply declined last year, the average loan balance will be lower this year compared to last year. I'm expecting loans to average $13.1 billion in 2024, down 3.6% from the average for 2023.

Further, I'm expecting deposits to change in line with loans. The following table shows my balance sheet estimates.

| Financial Position | FY19 | FY20 | FY21 | FY22 | FY23 | FY24E |

| Net Loans | 8,687 | 12,968 | 14,098 | 14,481 | 13,097 | 13,149 |

| Growth of Net Loans | (1.3)% | 49.3% | 8.7% | 2.7% | (9.6)% | 0.4% |

| Other Earning Assets | 1,695 | 4,821 | 5,008 | 5,079 | 2,970 | 2,982 |

| Deposits | 8,899 | 16,214 | 17,116 | 17,352 | 14,996 | 15,056 |

| Borrowings and Sub-Debt | 732 | 533 | 889 | 1,331 | 932 | 936 |

| Common equity | 2,013 | 2,747 | 2,886 | 2,798 | 2,883 | 2,879 |

| Book Value Per Share ($) | 32.8 | 34.5 | 30.7 | 29.7 | 30.6 | 30.6 |

| Tangible BVPS ($) | 19.6 | 22.2 | 20.4 | 19.6 | 20.6 | 20.5 |

| Source: SEC Filings, Earnings Releases, Author's Estimates (In USD million unless otherwise specified) | ||||||

Earnings of Pacific Premier Bancorp will most probably decline this year because the average loan balance will be lower in 2024 compared to 2023. Normal growth of operating expenses will also pressure earnings. On the other hand, the anticipated slight margin expansion will offer some support to the bottom line. Overall, I'm expecting the company to report earnings of $1.81 per share for 2024, down 19.8% from the earnings of 2023 adjusted for loss on securities sale. The following table shows my income statement estimates.

| Income Statement | FY19 | FY20 | FY21 | FY22 | FY23 | FY24E |

| Net interest income | 447 | 574 | 662 | 697 | 625 | 566 |

| Provision for loan losses | 6 | 192 | (71) | 5 | 10 | 8 |

| Non-interest income | 35 | 71 | 108 | 89 | (174) | 82 |

| Non-interest expense | 259 | 381 | 380 | 397 | 407 | 409 |

| Net income - Common Sh. | 160 | 60 | 336 | 280 | 31 | 171 |

| EPS - Diluted ($) | 2.60 | 0.75 | 3.58 | 2.98 | 0.31 | 1.81 |

| Adjusted EPS - Diluted ($) | 2.60 | 0.75 | 3.58 | 2.98 | 2.26 | 1.81 |

| Source: SEC Filings, Earnings Releases, Author's Estimates(In USD million unless otherwise specified) | ||||||

Pacific Premier Bancorp's risk is limited, in my opinion. Although the uninsured and uncollateralized deposits made up 34% of total deposits as of December 31, 2023, liquidity available to the company was around 1.9 times the balance of uninsured and uncollateralized deposits, as mentioned in the presentation.

Following the sale of securities in the last quarter, the risk related to the securities portfolio has also considerably declined. With interest rates set to dip this year, I'm sure the remaining unrealized losses on the securities portfolio will reverse soon.

The only substantial risk to my thesis comes from Pacific Premier's exposure to office commercial real estate loans. According to details given in the presentation, office loans made up 4.7% of total loans at the end of 2023. Defaults in this segment could materially impact Pacific Premier's earnings.

Pacific Premier Bancorp is offering an attractive dividend yield of 5.3% at the current quarterly dividend rate of $0.33 per share. The earnings and dividend estimates suggest a payout ratio of 73% for 2024, which is above the five-year average of 62%. Nevertheless, I don't think the dividend payout is threatened because a payout ratio of 73% is manageable. Additionally, Pacific Premier is very well capitalized, so there is no danger of dividend cuts to meet regulatory requirements. The company reported a total capital ratio of 17.29% as opposed to the minimum regulatory requirement of 10.50%, as mentioned in the earnings release.

I'm using the historical price-to-tangible book ("P/TB") and price-to-earnings ("P/E") multiples to value Pacific Premier Bancorp. The stock has traded at an average P/TB ratio of 1.52x in the past, as shown below.

| FY19 | FY20 | FY21 | FY22 | FY23 | Average | |

| T. Book Value per Share ($) | 19.6 | 22.2 | 20.4 | 19.6 | 20.6 | |

| Average Market Price ($) | 30.2 | 23.9 | 41.0 | 34.4 | 24.3 | |

| Historical P/TB | 1.54x | 1.08x | 2.01x | 1.76x | 1.18x | 1.52x |

| Source: Company Financials, Yahoo Finance, Author's Estimates | ||||||

Multiplying the average P/TB multiple with the forecast tangible book value per share of $20.5 gives a target price of $31.1 for the end of 2024. This price target implies a 24.8% upside from the February 12 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

| P/TB Multiple | 1.32x | 1.42x | 1.52x | 1.62x | 1.72x |

| TBVPS - Dec 2024 ($) | 20.5 | 20.5 | 20.5 | 20.5 | 20.5 |

| Target Price ($) | 27.0 | 29.0 | 31.1 | 33.2 | 35.2 |

| Market Price ($) | 24.9 | 24.9 | 24.9 | 24.9 | 24.9 |

| Upside/(Downside) | 8.3% | 16.5% | 24.8% | 33.0% | 41.2% |

| Source: Author's Estimates |

The stock has traded at an average P/E ratio of around 11.4x in the past, excluding the anomaly in 2020, as shown below.

| FY19 | FY20 | FY21 | FY22 | FY23 | Trimmed Average | |

| Adjusted Earnings per Share ($) | 2.60 | 0.75 | 3.58 | 2.98 | 2.26 | |

| Average Market Price ($) | 30.2 | 23.9 | 41.0 | 34.4 | 24.3 | |

| Historical P/E | 11.6x | 31.8x | 11.5x | 11.6x | 10.8x | 11.4x |

| Source: Company Financials, Yahoo Finance, Author's Estimates | ||||||

Multiplying the average P/E multiple with the forecast earnings per share of $1.81 gives a target price of $20.6 for the end of 2024. This price target implies a 17.4% downside from the February 12 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple | 9.4x | 10.4x | 11.4x | 12.4x | 13.4x |

| EPS 2024 ($) | 1.81 | 1.81 | 1.81 | 1.81 | 1.81 |

| Target Price ($) | 17.0 | 18.8 | 20.6 | 22.4 | 24.2 |

| Market Price ($) | 24.9 | 24.9 | 24.9 | 24.9 | 24.9 |

| Upside/(Downside) | (31.9)% | (24.7)% | (17.4)% | (10.1)% | (2.8)% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $25.8, which implies a 3.7% upside from the current market price. Adding the forward dividend yield gives a total expected return of 9.0%.

In my last report on the company, I determined a target price of $22.80 for the end of 2023, which implied a 27.5% price upside at that time. As a result, I adopted a Buy rating on PPBI in my last report. Since then, the stock price has rallied by around 33%. Based on the updated total expected return, I'm downgrading Pacific Premier Bancorp to a Hold rating.