PeopleImages

PeopleImages

Powell Industries, Inc. (NASDAQ:POWL) investors have likely been surprised by the stunning reversal in POWL over the past month since Powell's earnings release in late January 2024. Accordingly, a post-earnings surge saw POWL take out new highs at the $198 level through early March. However, that proved a significant distribution zone, as earlier investors likely saw a "glorious" opportunity to cash in on substantial gains.

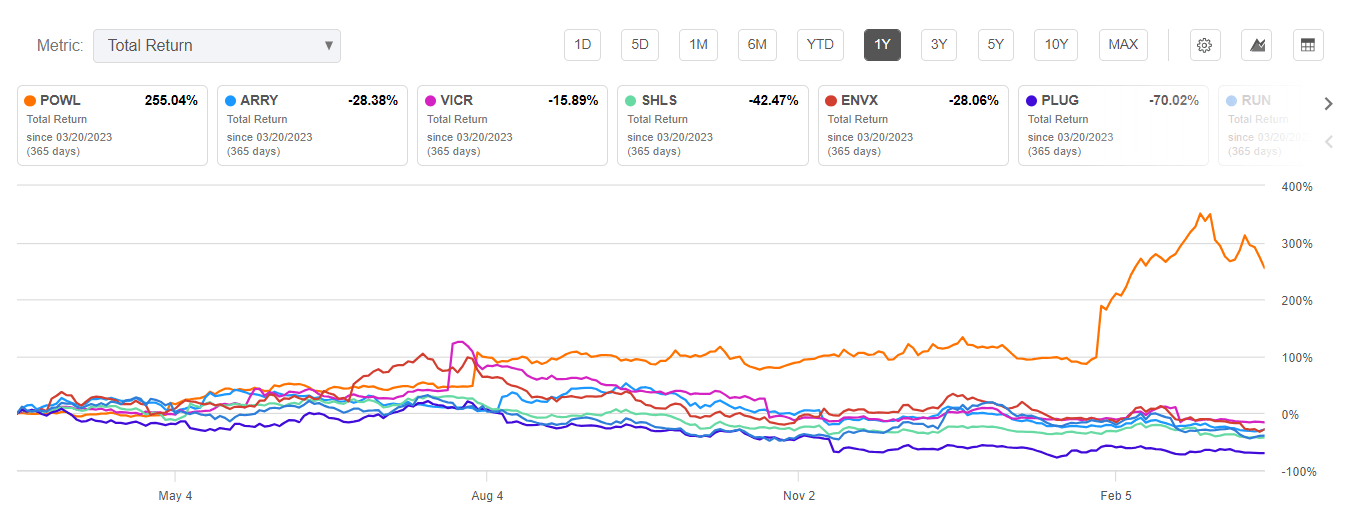

POWL Vs. Peers (1Y total return %) (Seeking Alpha)

Does it make sense? Absolutely. As seen above, POWL has significantly outperformed its electrical components and equipment peers in the industrials sector (XLI). Notwithstanding the recent downside volatility, POWL delivered a 1Y total return of more than 250% as investors rode the spike toward its March highs.

However, POWL has also fallen into bear market territory, declining more than 25% through this week's lows, threatening to engulf buyers trying to defend the $140 support level. Seeking Alpha Quant has downgraded POWL's rating from Strong Buy to Hold since late February, a timely call that has saved investors from chasing POWL's recent surge.

Powell Industries investors will likely point to the company's significant backlog and healthy balance sheet to justify remaining bullish. Powell's business model might not be easy for the retail investor to understand, as it's involved in the custom-engineered equipment and systems business. Moreover, Powell's concentration risks in the oil and gas industry shouldn't be understated, worsening business cycle risks. Nearly 60% of its revenue exposure is linked to oil and gas/petrochemical customers. As a result, Powell investors must pay close attention to the developments in these markets.

Notably, in Powell's fiscal first-quarter earnings conference, management articulated substantial risks linked to the recent decision by the Biden Administration to "pause LNG export approvals." Powell management didn't mince its words as CEO Brett Cope emphasized that Powell and its customers were "perplexed" by the Administration's decision. Despite that, Powell maintained its confidence that it envisions "encouraging levels of project activity within oil, gas, and petrochemical markets." Therefore, while the recent decision has led to near-term uncertainties and potential delays, the long-term outlook remains intact.

However, Powell also updated the LNG-related projects account for about 25% to 30% of the company's backlog. Moreover, Powell's sequential growth in its backlog has stalled in the fiscal first quarter, remaining relatively flat at about $1.3B. As a result, I believe the market likely anticipated significant near-term execution risks, leading to the recent bear market decline. Should investors consider capitalizing on the steep pullback to add more positions?

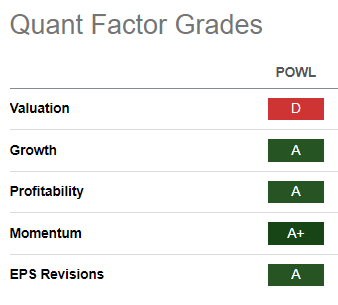

POWL Quant Grades (Seeking Alpha)

POWL's "D" valuation grade corroborates my observation that much of its growth momentum is likely reflected in its valuation. The company has diversified its exposure to other markets, including data centers and renewable energy players. However, the nearly 60% exposure to oil and gas/petrochemical customers must still be considered a significant risk. In addition, the LNG-related risks add to the worries about POWL's near-term uncertainties, suggesting it's apt for investors to allow more time for it to consolidate constructively.

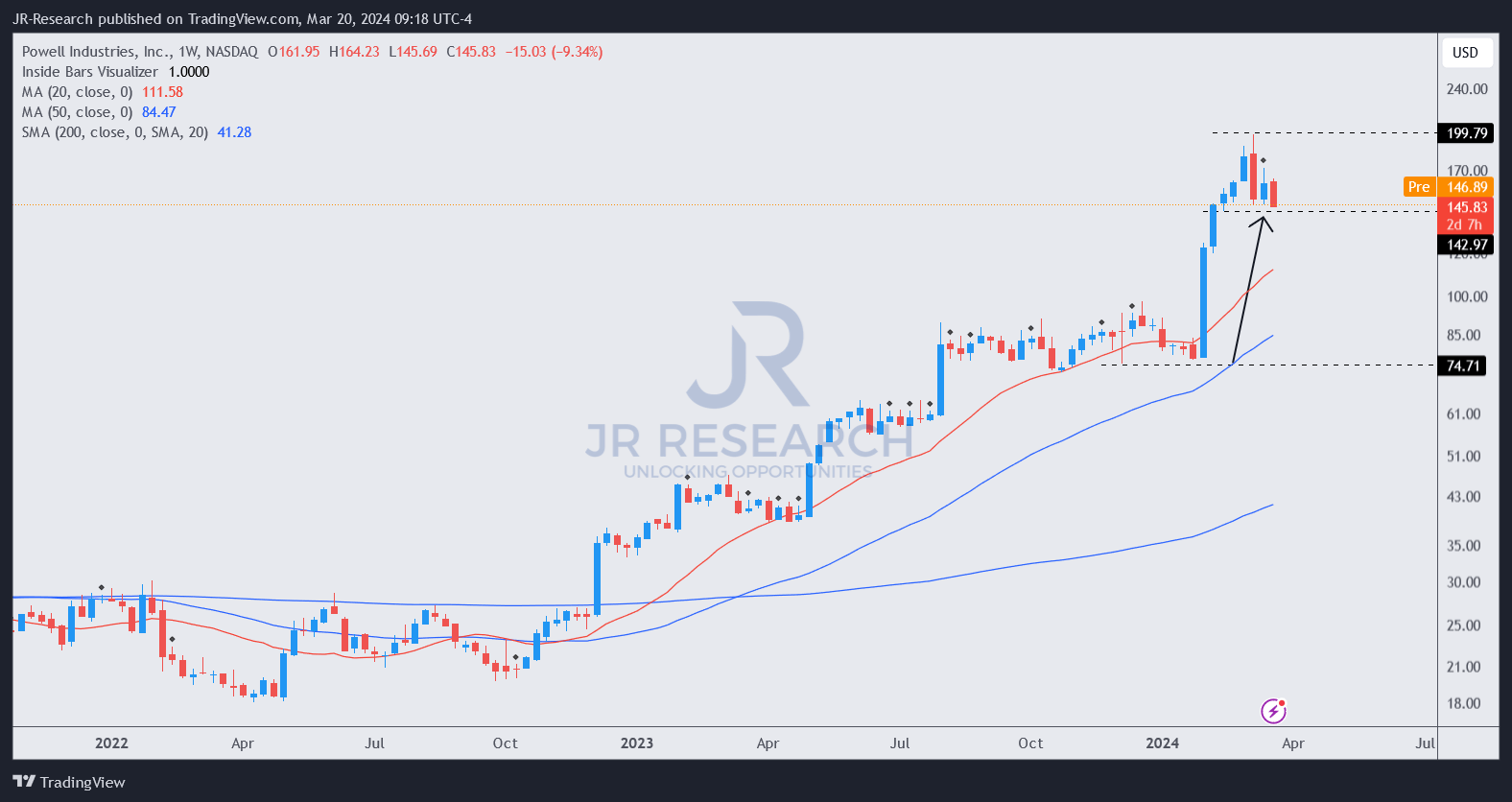

POWL price chart (weekly, medium-term, adjusted for dividends) (TradingView)

POWL surged toward its March highs ($198 level) from its December lows of $75. I didn't assess red flags, suggesting a significant distribution zone, behooving the need to cut substantial exposure.

However, caution is advocated, as a decisive breakdown below the $145 level could cause mayhem in investors who bought POWL's initial post-earning surge in late January 2024. In other words, the sharp upward spike suggests investors added POWL quickly as they reacted positively to Powell's FQ1 earnings scorecard. However, a decisive breach of the $145 level could cause these investors to bail out in a hurry as they aim to protect their gains.

Hence, given the recent uncertainties, I assessed it's appropriate for investors to consider a more cautious posture when assessing POWL's recovery thesis. If POWL can constructively hold its $145 level over the next four to six weeks, it should afford more confidence to dip buyers looking to add exposure.

Rating: Initiate Hold.

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn't? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!