What Does Powell Industries, Inc.'s (NASDAQ:POWL) Share Price Indicate?

Powell Industries, Inc. (NASDAQ:POWL), might not be a large cap stock, but it saw a significant share price rise of 109% in the past couple of months on the NASDAQGS. While good news for shareholders, the company has traded much higher in the past year. Less-covered, small caps tend to present more of an opportunity for mispricing due to the lack of information available to the public, which can be a good thing. So, could the stock still be trading at a low price relative to its actual value? Let’s take a look at Powell Industries’s outlook and value based on the most recent financial data to see if the opportunity still exists.

See our latest analysis for Powell Industries

Is Powell Industries Still Cheap?

According to our price multiple model, which makes a comparison between the company's price-to-earnings ratio and the industry average, the stock price seems to be justfied. In this instance, we’ve used the price-to-earnings (PE) ratio given that there is not enough information to reliably forecast the stock’s cash flows. We find that Powell Industries’s ratio of 24.86x is trading slightly above its industry peers’ ratio of 20.85x, which means if you buy Powell Industries today, you’d be paying a relatively reasonable price for it. And if you believe that Powell Industries should be trading at this level in the long run, then there should only be a fairly immaterial downside vs other industry peers. Furthermore, Powell Industries’s share price also seems relatively stable compared to the rest of the market, as indicated by its low beta. This may mean it is less likely for the stock to fall lower from natural market volatility, which suggests less opportunities to buy moving forward.

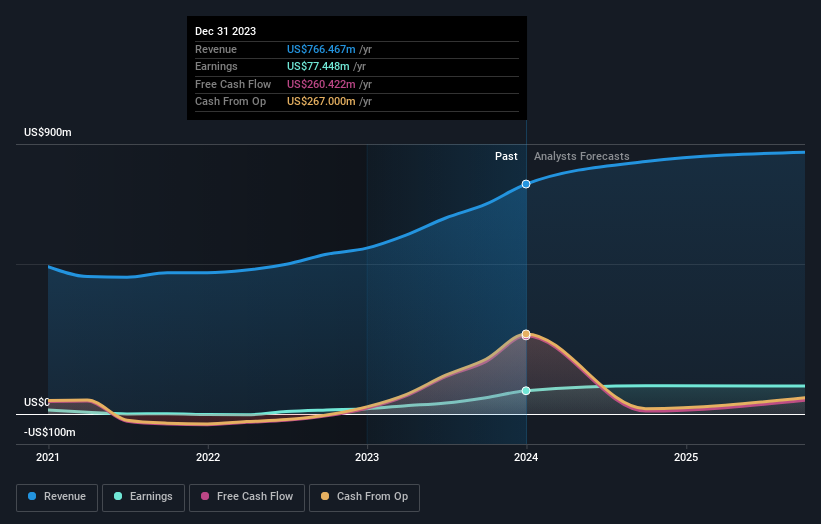

What does the future of Powell Industries look like?

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company's future expectations. With profit expected to grow by 21% over the next year, the near-term future seems bright for Powell Industries. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What This Means For You

Are you a shareholder? POWL’s optimistic future growth appears to have been factored into the current share price, with shares trading around industry price multiples. However, there are also other important factors which we haven’t considered today, such as the track record of its management team. Have these factors changed since the last time you looked at POWL? Will you have enough confidence to invest in the company should the price drop below the industry PE ratio?