skynesher/E+ via Getty Images

skynesher/E+ via Getty Images

In an ideal world, every investment that every person makes would pan out the way that they expect it to. Unfortunately, we do not live in such a wonderful place. Every investor makes mistakes from time-to-time. Even the most experienced of us cannot deny this.

One company that I now recognize I was wrong about some time ago is Pool Corporation (NASDAQ:POOL). As its name suggests, the company is engaged in the business of providing swimming pools and related products and services to its clients. The vast majority of these operations are in North America. The business does also have an irrigation and landscape business. But that's a fairly small part of the overall pie.

Back in September of 2021, I ended up writing a bullish article about the business. I found myself impressed with its leadership position in the industry and I felt as though the rapid growth the enterprise was achieving was worth the premium price that investors had to pay in order to participate in its potential moving forward. Some of this optimism was based on expectations for future growth. Regardless, the decision to rate the business a "buy" to reflect my view at the time that the stock should outperform the broader market for the foreseeable future was faulty. Since the publication of that piece, shares have plummeted, generating downside for investors of 16.2%. That is awful compared to the 14.5% rise seen by the S&P 500 over the same window of time.

Today, the Pool Corporation business is seeing some weakness compared to what it experienced back in 2022. That weakness and what it means for how shares are priced leads me to believe that a downgrade to a "hold" is appropriate at this time.

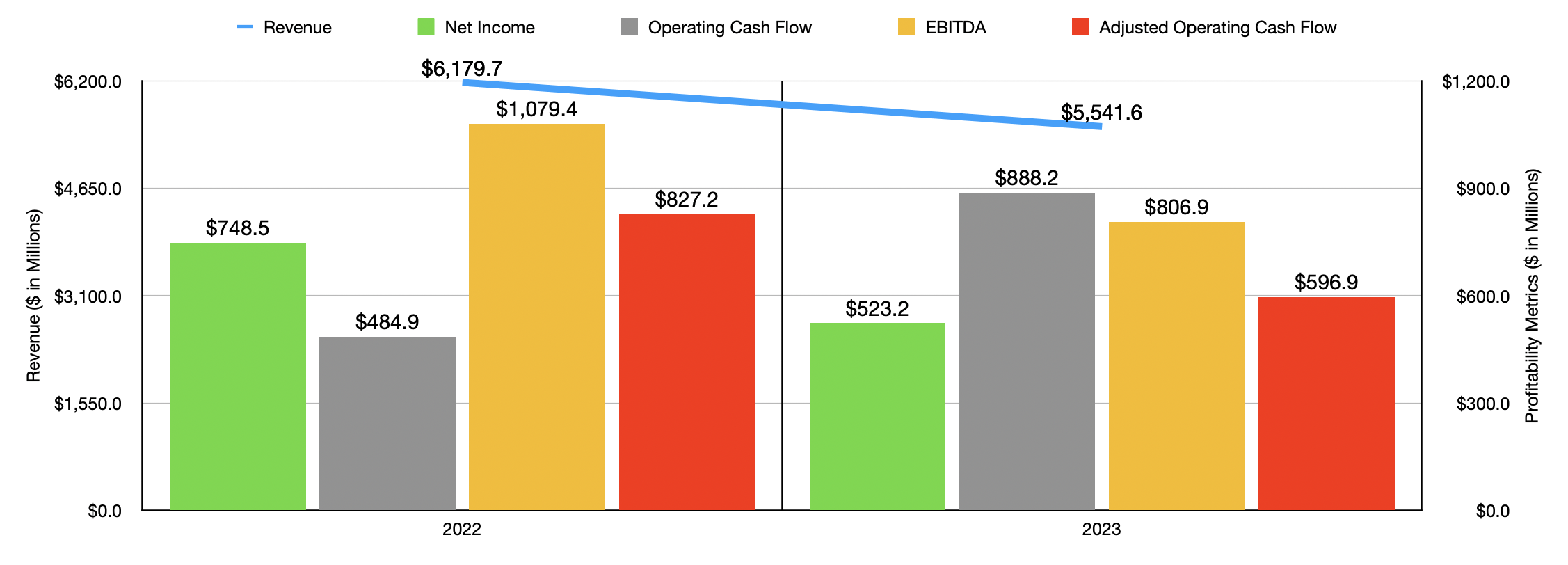

A great deal has happened since I last wrote about Pool Corp. Let's consider financial results for 2023 relative to 2022 as an example. Sales in 2023 totaled a hefty $5.54 billion. Even though this is a large chunk of cash, it represents a meaningful decline of 10.3% compared to the $6.18 billion generated in 2022.

The picture would have been worse had it not been for the fact that management was able to get some benefit from raising prices by between 3% and 4%. Unfortunately, this was more than offset by unfavorable weather conditions in some markets that occurred during the first half of the year. That caused what management describes as a "slow start" to the swimming pool season that ultimately created lower levels of maintenance activity than the company was hoping for. Lower volumes of discretionary pool products were also experienced because of a reduction in pool construction activity and as people allocated their discretionary income to other activities.

Author - SEC EDGAR Data

As a result of the decline in sales, profits and most cash flow figures for the company came in lower year over year. Net income of $523.2 million was substantially lower than the $748.5 million generated in 2022. It is true that operating cash flow almost doubled, climbing from $484.9 million to $888.2 million. But if we adjust for changes in working capital, we get a drop from $827.2 million to $596.9 million. Lastly, EBITDA for the company fell from $1.08 billion to $806.9 million.

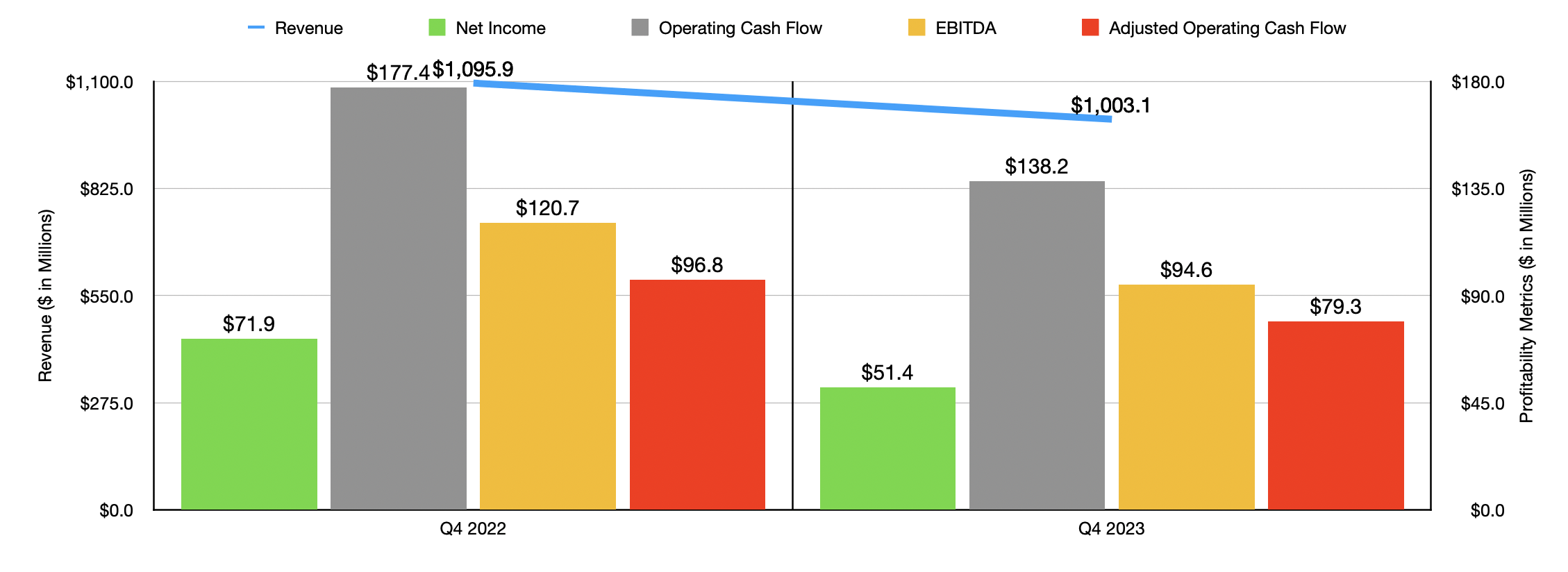

Unfortunately, while the first half of 2023 was when the company experienced the most pain, the final quarter of the year that management just reported before the market opened on February 22nd didn't do shareholders any favors. I say this because revenue of $1 billion came in $20 million lower than what analysts anticipated. It was also a bit lower, about 8.5% in all, then the roughly $1.10 billion management reported for the final quarter of 2022. Management said that maintenance activities and demand for non-discretionary products that it sold ended up being stable year over year. However, softer spending on discretionary products and on pool construction activities more than offset this.

Author - SEC EDGAR Data

It should come as no surprise, given these figures, that profits would also take a hit. The company generated a profit per share of $1.32. In addition to being lower than the $1.82 generated the same time one year earlier, earnings fell far short of the $2.54 per share than analysts were anticipating. On an adjusted basis, however, the $1.30 per share reported by management was actually $0.03 per share higher than the adjusted earnings analysts forecasted. Put another way, actual net profits for the business fell from $71.9 million to $51.4 million.

Other profitability metrics followed a similar trajectory. Operating cash flow declined from $177.4 million to $138.2 million. On an adjusted basis, it went from $96.8 million to $79.3 million. And finally, EBITDA for the company came in at $94.6 million. That’s a meaningful decline from the $120.7 million reported in 2022.

When it comes to guidance for 2024, management has not provided very much. The only thing that they said is that earnings per share should be between $13 and $14. At the midpoint, that would translate to net income of $521.7 million. That's down just a hair from the 2023 figures provided by management. If we assume that other profitability metrics change at the same rate that net profits are expected to, we should anticipate adjusted operating cash flow of $595.2 million and EBITDA of around $804.6 million.

Author - SEC EDGAR Data

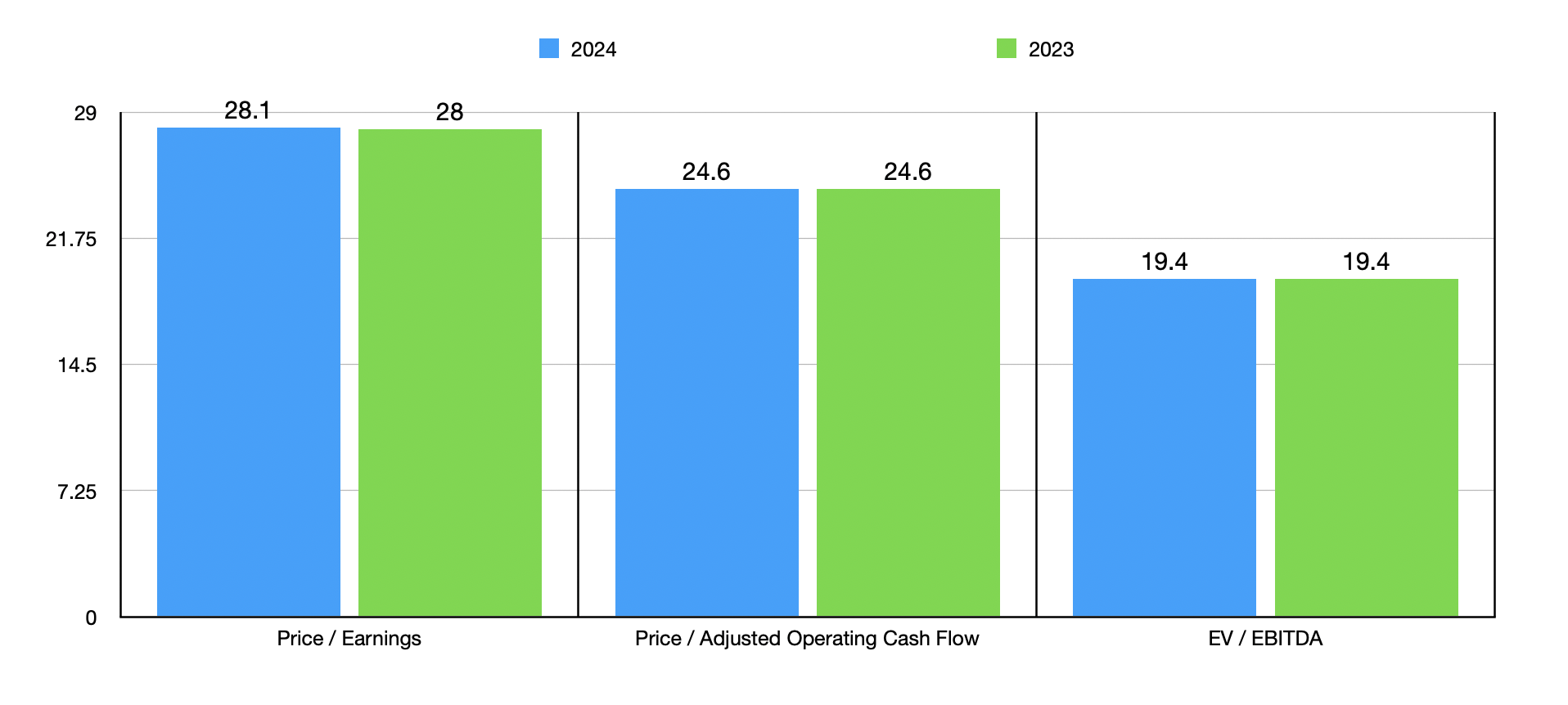

Using these results, I was then able to value the company as shown in the chart above. I did this using the historical results from 2023 and the estimated figures for 2024. On an absolute basis, shares look rather pricey. I then decided to compare the firm to four similar enterprises (three of which are intimately involved in the swimming pool space) in the table below. What I found is that, while only one of the five firms was cheaper than it on a price to earnings basis, it ended up being the most expensive of the group when it comes down to the other two profitability metrics.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Pool Corp | 28.0 | 24.6 | 19.4 |

| Latham Corp (SWIM) | 46.0 | 2.6 | 10.8 |

| Leslie's (LESL) | 68.9 | 10.7 | 16.4 |

| Hayward Holdings (HAYW) | 43.8 | 14.8 | 17.0 |

| Core & Main (CNM) | 21.8 | 10.1 | 10.9 |

Clearly, shares of Pool Corp are expensive at this point in time. But this doesn't necessarily mean that the company itself is bad. Frankly, the stock is too expensive for my liking. But management has been doing a fine job pretty much across the board. Using some of the firm's capital expenditures, it has managed to continue growing. It bought 5 new locations during 2023 and added 14 new ones, bringing its store count up to 439 from the 420 that it stood at in December of 2022.

Management also succeeded in allocating $167.5 million toward cash dividends and they bought back $306.4 million worth of shares. On top of this, the company has succeeded, actually even surpassed, its goal when it comes to leverage. Back when I wrote about the business in 2021, management's goal had been to get the net leverage ratio of the enterprise down to between 1.5 and 2. As of the end of 2023, that number is down to only 1.2.

Fundamentally speaking, Pool Corp is a quality company that should, over the long run, perform well. But this doesn't necessarily mean that it makes sense to buy into. Recent Pool Corporation financial performance has shown a deterioration in demand. Bottom line results have worsened, and it's unclear when that trend will reverse. If anything, it's looking like 2024 will be very similar to 2023 from a profit and cash flow perspective.

Given how pricey the stock is, it's almost to the point of warranting something fairly bearish like a "sell" rating. But considering the high quality operation we are looking at, a more modest "hold" rating for Pool Corporation is what I have decided to settle on at this time.