LIgorko

LIgorko

One of the most difficult challenges of being a value investor is that the market does not behave rationally. While this is great in the sense that it often results in companies being undervalued, the flip side of it is that expensive companies can continue to appreciate even if they don't deserve to. One good example of this involves RBC Bearings (NYSE:RBC), a firm that is focused on the production and sale of highly engineered precision bearings, components, and systems that are used in the industrial, defense, and aerospace industries.

Back in March of 2023, I wrote an article acknowledging that the fundamental performance of RBC Bearings was continuing to come in. However, attractive growth does not always equate to a worthwhile investment. In that article, I talked about how expensive shares were and ended up concluding that the stock was not yet cheap enough to warrant upside. This resulted in a ‘hold’ rating for the business, which is a rating that reflects my belief that shares are unlikely to outperform the broader market for the foreseeable future. Since then, that is precisely what occurred. While the S&P 500 is up 23.7% since the publication of that article, shares have seen upside of only 10.6%. Given how the stock is now priced and in spite of recent attractive top line and bottom line performance, I am starting to get worried that shares are going from pricey to materially overvalued. I'm not quite ready to downgrade the firm just yet. After all, it is difficult to justify a ‘sell’ rating on a company that continues to expand and that recently experienced an uptick in backlog. But if shares move up much further without a corresponding improvement on the bottom line, a downgrade might become inevitable.

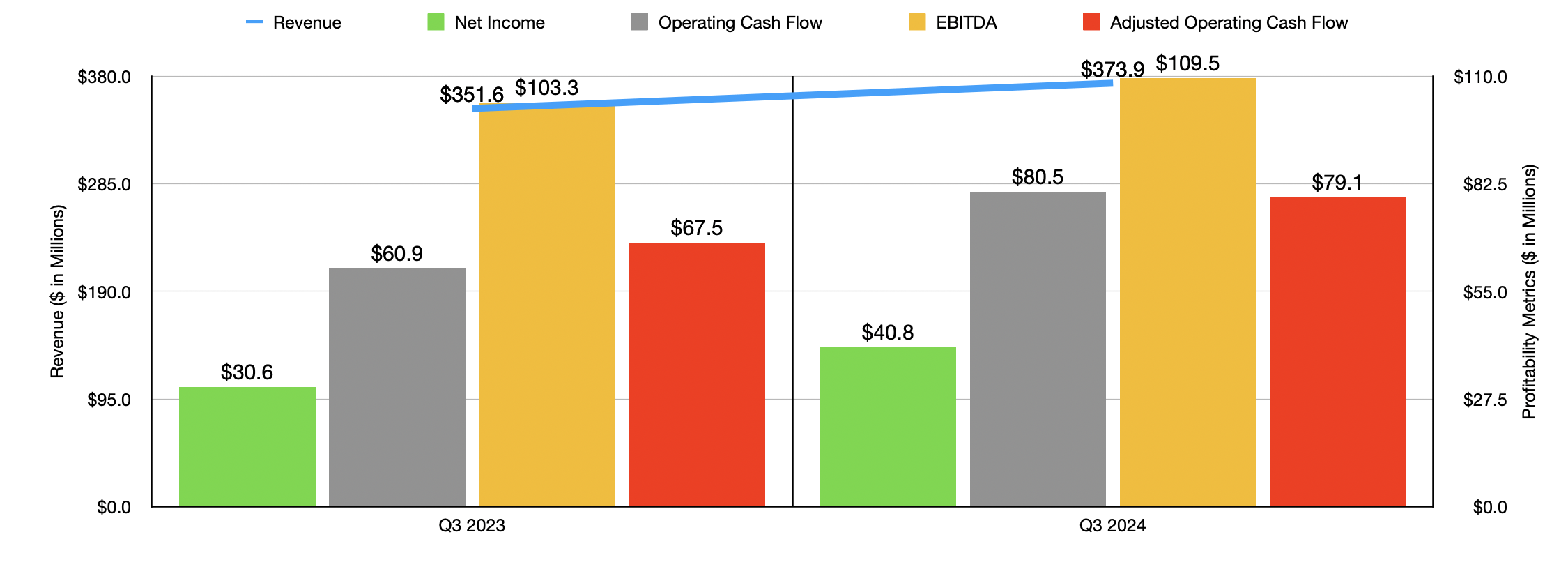

From a fundamental perspective, things are going quite well for RBC Bearings right now. Take, for instance, the third quarter of the company's 2024 fiscal year that management just reported data for on February 8th. Revenue for the quarter came in at $373.9 million. That represents an increase of 6.3% over the $351.6 million generated one year earlier. According to management, the growth in sales was driven by a 22.5% surge in its Aerospace/Defense segment. Revenue for that unit skyrocketed from $105.5 million to $129.2 million. Commercial aerospace revenue managed to rise by 19.9% year over year as the world sees a continued recovery from years of lower traffic in air space travel and as build rates and orders grow in the original equipment manufacturer market.

Author - SEC EDGAR Data

I actually wrote about this to some extent in another article recently. I would recommend that you read it, as opposed to me rehashing all of the details here. But in short, toward the middle to end of last year, the world finally returned to pre pandemic levels of air travel. Total enplanements are actually forecasted to surpass the all-time highs experienced in 2019 this very year. So it's not surprising to see an uptick in demand associated with these operations. Even more impressive was the defense side of things, with revenue jumping 28.2%. Management stated that orders associated with marine vessels were particularly strong, especially when it came to submarines. In a world with such geopolitical uncertainty, it's not surprising to see a rise in demand for such vessels.

This is not to say that there was not any weakness for the company. The Industrial segment reported a decline in revenue of 0.6%, resulting in sales falling from $246.1 million to $244.7 million. Food and beverage, as well as mining and metals, ended up being weak spots for the company. But these were partially offset by demand growth when it involves the semiconductor space.

The overall growth in revenue for the business resulted in net profits rising from $30.6 million to $40.8 million. A slight improvement in gross margin was visible in the Industrial segment, with gross margin inching up from 42.4% to 42.8%. But this was more than offset by a rise in selling, general, and administrative costs from 11.8% of sales to 13.3%. The Aerospace/Defense segment, meanwhile, saw gross margin climbed from 39.5% to 41.2% as higher sales volumes, a favorable change in product mix, and operational efficiencies achieved by management, all helped the company out. Naturally, other profitability metrics followed suit. Operating cash flow went from $60.9 million to $80.5 million. If we adjust for changes in working capital, we would get an increase from $67.5 million to $79.1 million. And lastly, EBITDA for the enterprise rose from $103.3 million to $109.5 million.

Author - SEC EDGAR Data

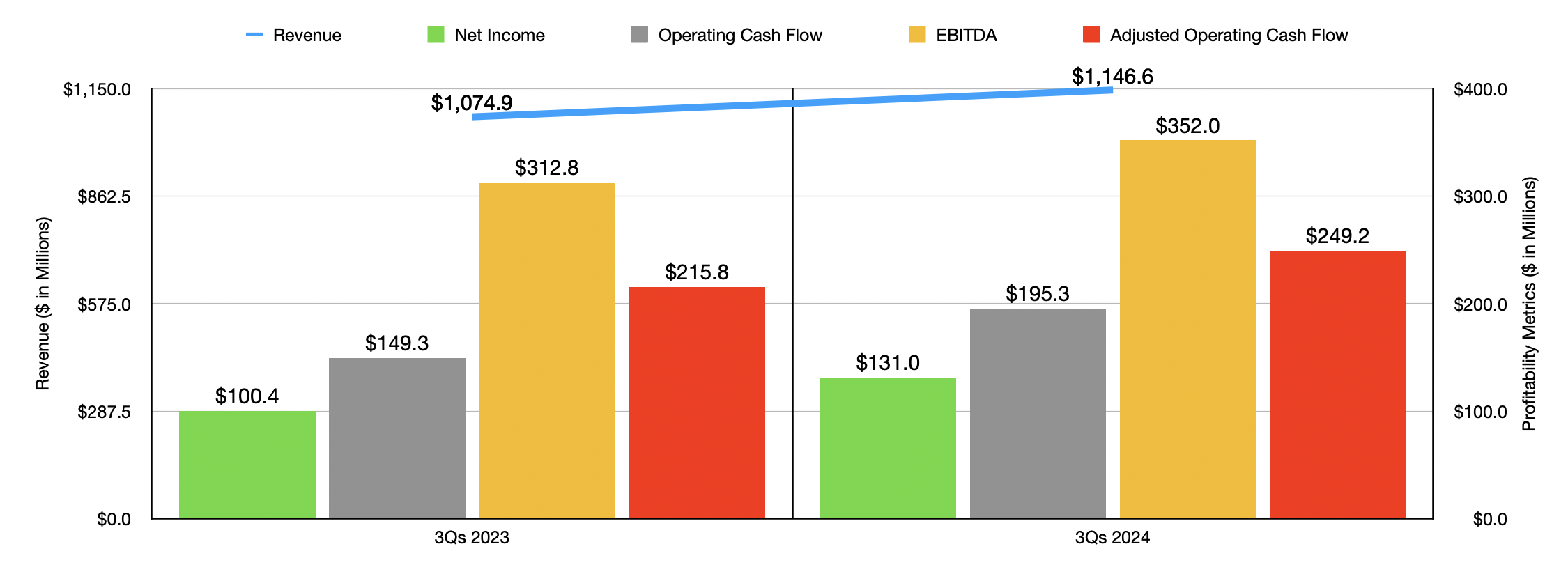

The overall improvement for the company on both its top and bottom lines was not a one-quarter event. If you look at the chart above, you can see financial results for the first nine months of the 2024 fiscal year compared to the first nine months of the 2023 fiscal year. Revenue, profits, and cash flows, all increased year over year. Clearly, this is part of a continued trend, a trend that I talked about in my last article on the company almost a year ago.

Author - SEC EDGAR Data

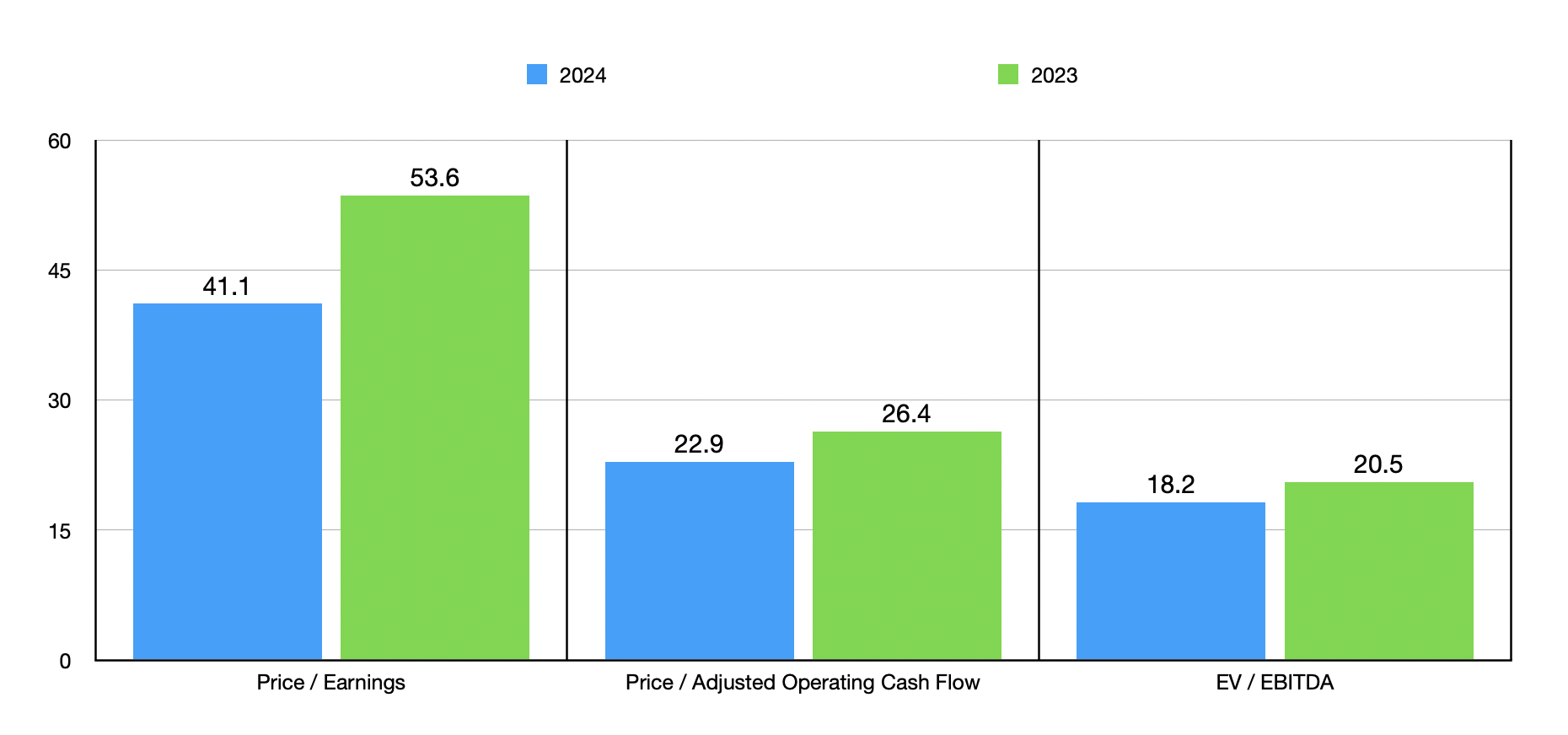

Management has, unfortunately, been rather quiet when it comes to guidance on the bottom line. If we annualize result seen so far for the first nine months of the current fiscal year, we would anticipate net profits for the year of $187.6 million. Adjusted operating cash flow would be $336.8 million, while EBITDA would come in at $613.6 million. Although the stock does look cheaper when using the 2024 estimates instead of the 2023 results that were officially achieved, the company still does look very expensive. This is especially true when it comes to the price to earnings multiple. This is the kind of multiple that you expect for a business that's growing at a rather rapid pace. But that is not the case here. Even relative to similar firms, shares look rather pricey. As you can see in the table below, I compared RBC Bearings to five similar enterprises. When it comes to the price to earnings approach and the EV to EBITDA approach to valuing the companies, four of the five businesses ended up being cheaper than our prospect. And when it involves the price to operating cash flow approach, three of the five ended up being cheaper.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| RBC Bearings | 41.1 | 22.9 | 18.2 |

| Pentair (PNR) | 19.7 | 19.8 | 16.7 |

| Donaldson Company (DCI) | 22.3 | 14.4 | 14.6 |

| Chart Industries (GTLS) | 290.1 | 80.9 | 22.5 |

| ITT Inc. (ITT) | 24.1 | 18.4 | 15.4 |

| Crane Company (CR) | 27.5 | 30.8 | 17.0 |

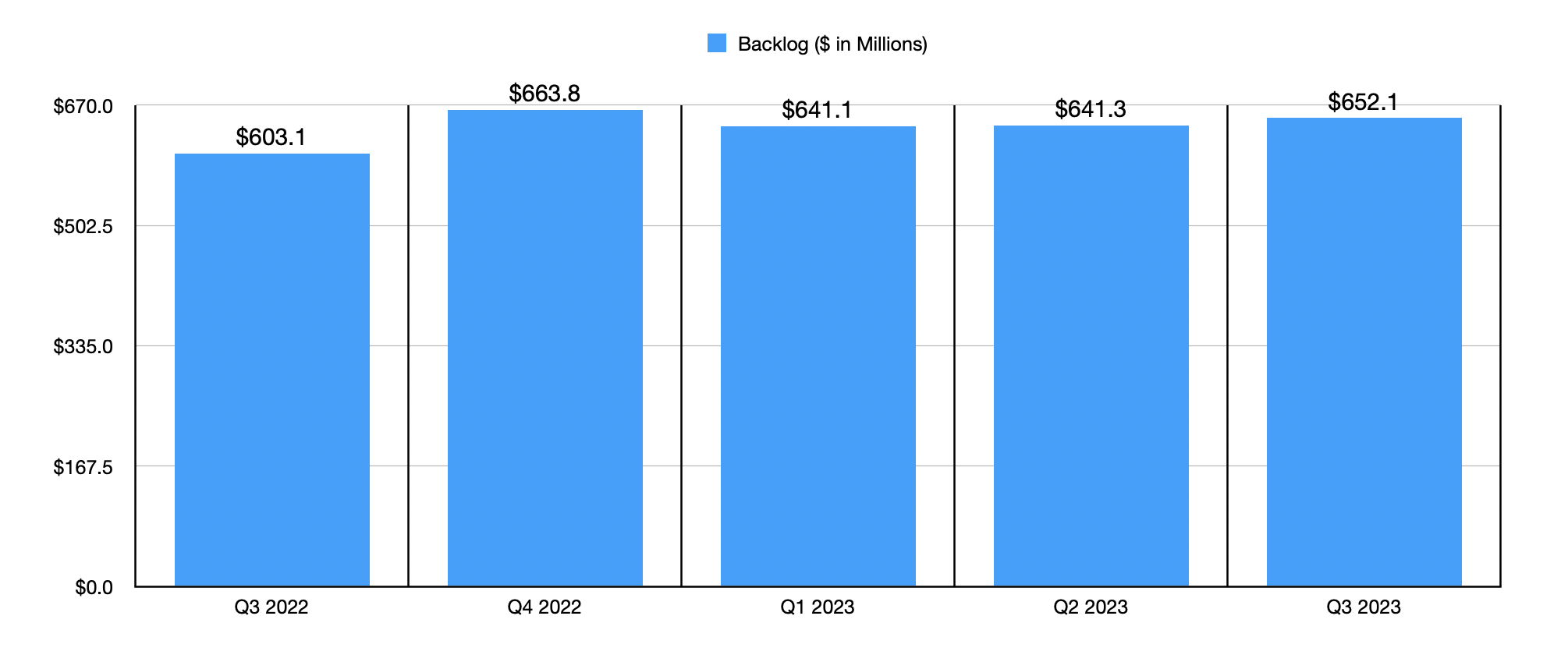

The stock is very expensive at this time and, frankly, it is very difficult for me not to downgrade the firm. However, continued growth does work in the business's favor. In addition to this, there's also the fact that, after seeing a couple of quarters of declines in backlog, we did recently see an improvement. As you can see in the chart below, after dropping from $663.8 million in the final quarter of the 2023 fiscal year to $641.1 million in the first quarter of 2024, there was a modest increase in the second quarter before experiencing a more material improvement in the third quarter. In that quarter, backlog totaled $652.1 million. Although it's not the kind of growth I would love to see, it does show that demand for the company's products and services continues to expand as well.

Author - SEC EDGAR Data

As things stand, RBC Bearings seems to be a very solid business. Long term, I have no doubt that the company will survive and continue growing. But this doesn't mean that the firm is an ideal prospect for investors to buy into. Shares are very expensive at this point in time, almost to the point of justifying a downgrade. But the quality of the business, combined with the recent uptick in backlog, has me unwilling to make such a move at this moment. In the event that shares rise further from this point on without a change in bottom line expectations, I probably will downgrade the company. But for the moment, I am keeping it rated a ‘hold’.