Justin Sullivan

Justin Sullivan

British American Tobacco p.l.c. (NYSE:BTI) (BATS) is the largest tobacco company in the world by revenue followed by Philip Morris International Inc. (PM) and Altria Group, Inc. (MO). The company has a rich history going back to the 19th century, and it has survived two world wars while still paying dividends to shareholders. The company started back in 1902 when the British Imperial Tobacco Company and the American Tobacco Company started a joint venture called British American Tobacco. The current company is a result of a big acquisition of Reynolds for $47B in 2017. The acquisition made them into largest tobacco company in the world today, with brands like Newport, Lucky Strike, and Pall Mall.

The company is selling tobacco brands across the entire world, but still makes about 50% of its profits from the USA. Traditional cigarette smoking is in a slow secular decline, but a lot of people still choose to smoke and will probably continue to do so over the next decade. The company is generating a lot of cash from these activities, reporting over $10b in free cash flow in FY2023.

Combustibles Brands (BTI, 2024)

The Reynolds acquisition also gave them a market-leading position in new categories of nicotine products, like vaping and nicotine pouches, which is part of their long-term strategy to transform the company into a smokeless future. They are growing their new Vuse, Glo, and Velo brands that deliver nicotine in alternative ways to address some of the health risks of smoking. These reduced risk products provide a good way for BTI to achieve future growth.

In addition to their very profitable cigarette operations, BTI owns a 29% stake in Indian Conglomerate ITC that should be worth $17.5B which is already over 20% of BTI's own market cap. BTI is considering selling off part of its stake in ITC to liquidate this substantial asset so an investment in BTI offers a lot of value for money. BTI communicated that it would use these funds to pay off debt and buy back shares; they planned to buy back $900m of shares in 2024.

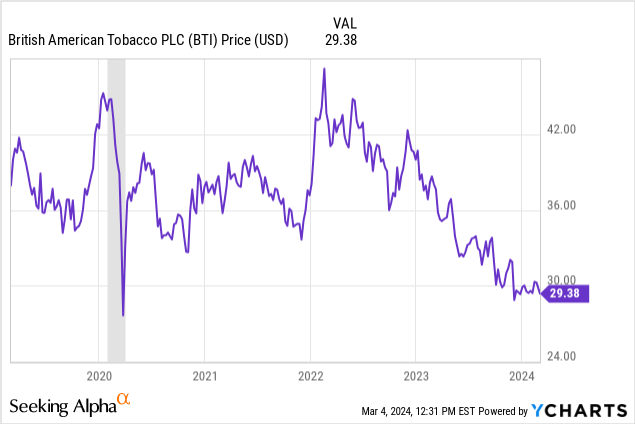

We rate BTI as a "buy" below $30 per share. The dividend yield of 10% is very good and the main attractive element for this investment because there is little prospect of earnings growth. Just based on dividends alone, the company could provide double-digit annual returns. In the near term, buybacks are a catalyst to drive significant shareholder returns. And in the long term, a successful transition towards "reduced risk" products could lead to a re-rating; doubling the valuation multiples from the bottom-of-the-barrel levels of today.

After a big decline over the last two years from $40 to $30 per share, the shares look attractively priced even below the 2020 pandemic crash levels. Reasons for this decline include the bad quarterly earnings report showing declining combustibles volumes, particularly in the US at over 10%.

In addition, the recent regulatory issue around menthol cigarettes that could lead to a ban on menthol cigarettes is expected to reach a decision in March. Menthol cigarettes make up about half of US sales, so that could have a large impact on BTI. However, the ban is far from certain and rumors suggest that Biden is putting it on hold because it's a risk for the upcoming elections.

Finally, the company took a big $30B impairment on its tobacco brands. Importantly, however, this $30B impairment is a non-cash expense. While the company reported negative net earnings for FY2023 because of this impairment, free cash flow was positive. In fact, the company is doing fine and reported a massive $10B in free cash flow in February at the end of FY2023.

This recent decline in share price could therefore provide an attractive entry point for value investors, with a 15% FCF yield and a 10% dividend yield. Moreover, several short-term catalysts could stimulate price actions such as postponing the menthol ban, banning illicit vapes, or commencing buybacks.

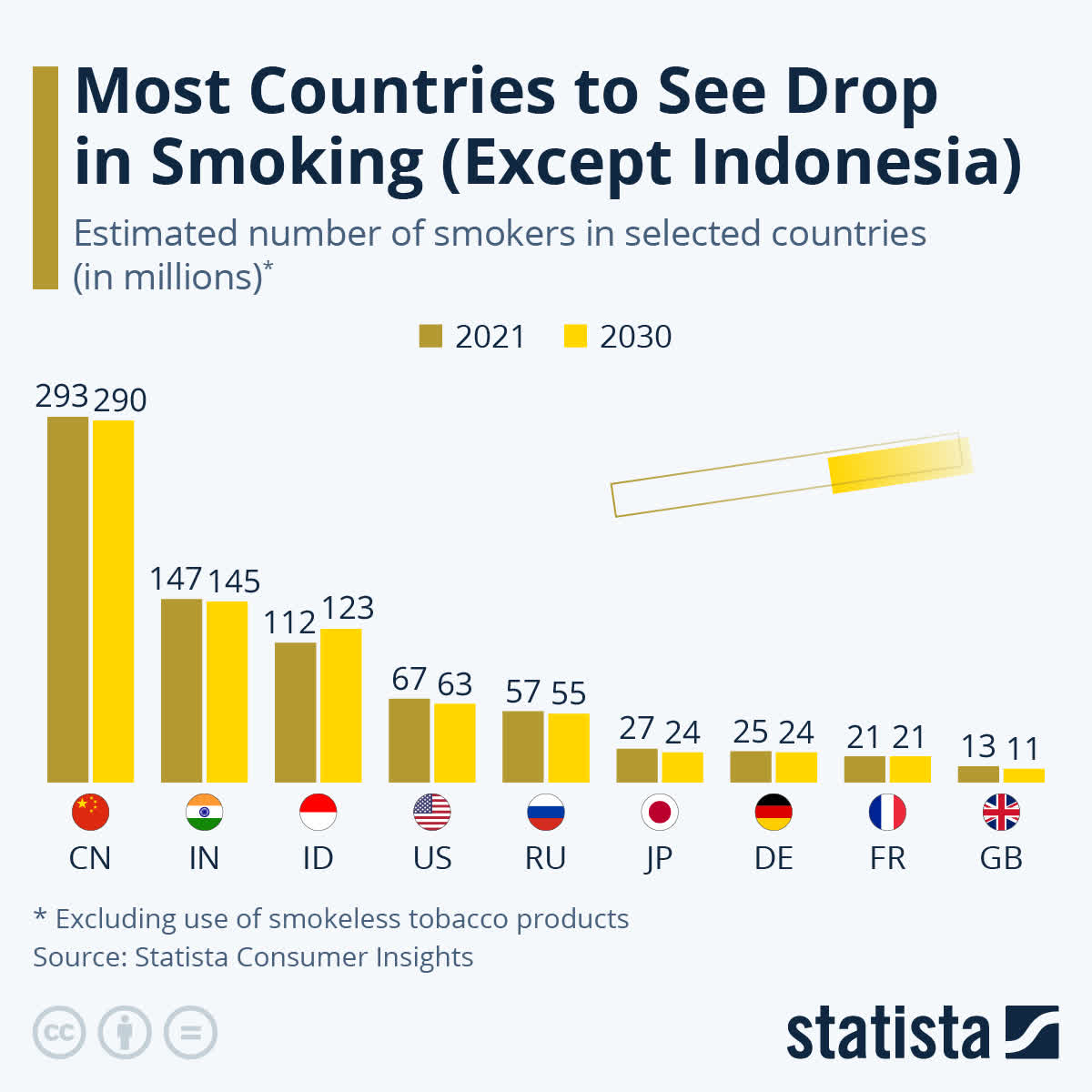

Smoking prevalence worldwide (Statista, 2024)

As you are probably all aware, BTI's legacy combustibles business is still very profitable but faces a slow secular decline. Less people around the world are smoking as a result of increasing public awareness of health risks and more government intervention. Young people now rarely start smoking anymore as a result of these initiatives. There are ethical concerns as well as legal/financial risks, which should be considered when investing in the tobacco industry.

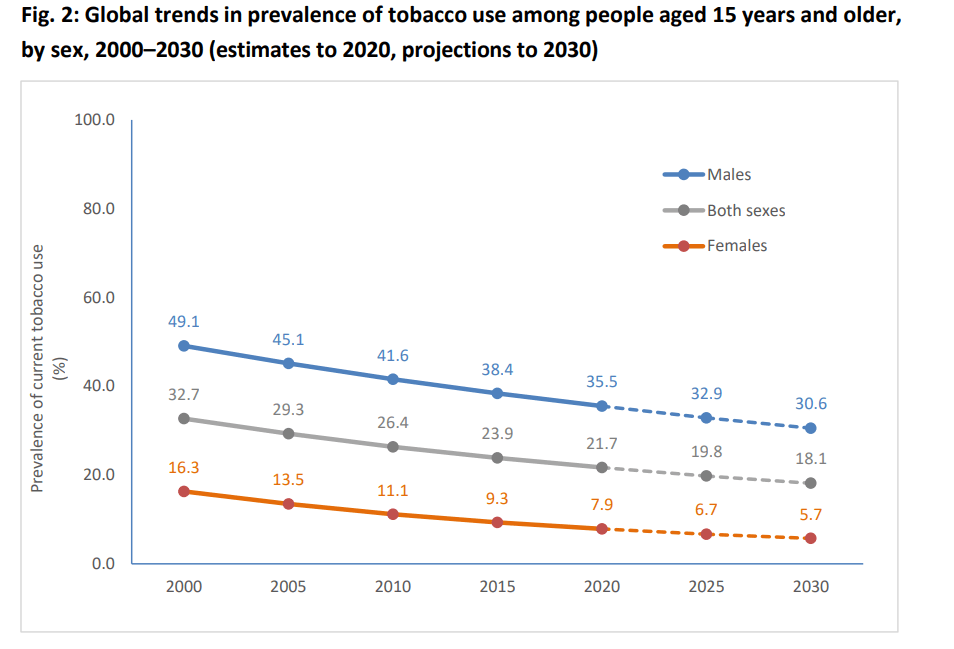

Smoking Prevalence Projections (WHO, 2024)

Importantly, however, WHO data and projections on smoking prevalence, indicate that the expected rate of decline is rather slow. This means that smoking is still expected to decline, but not that smoking is going to disappear anytime soon. For 2030, the WHO projects a decline of about 2% in global smoking prevalence compared to 2025 levels. Comparing this to the previous rate of decline from 2000 to 2005 (-4% prevalence) and 2010 to 2015 (-3% prevalence over 5 years), we can conclude that the decline is secular but happening at a relatively slow pace. Moreover, the rate of decline is slowing with estimations of a 2% decline in prevalence over the coming five-year periods.

BTI can maintain its revenue by increasing prices while volume decreases slowly over time, and cigarette demand is relatively inelastic so raising prices is a viable strategy. In conclusion, BTI can probably keep making money selling cigarettes at increasing prices while volumes are in a slow decline at least until 2030 and probably well beyond that. Moreover, the company has a large moat because it is pretty much impossible to start a new tobacco brand. This strict regulation has created significant barriers to entry for competitors.

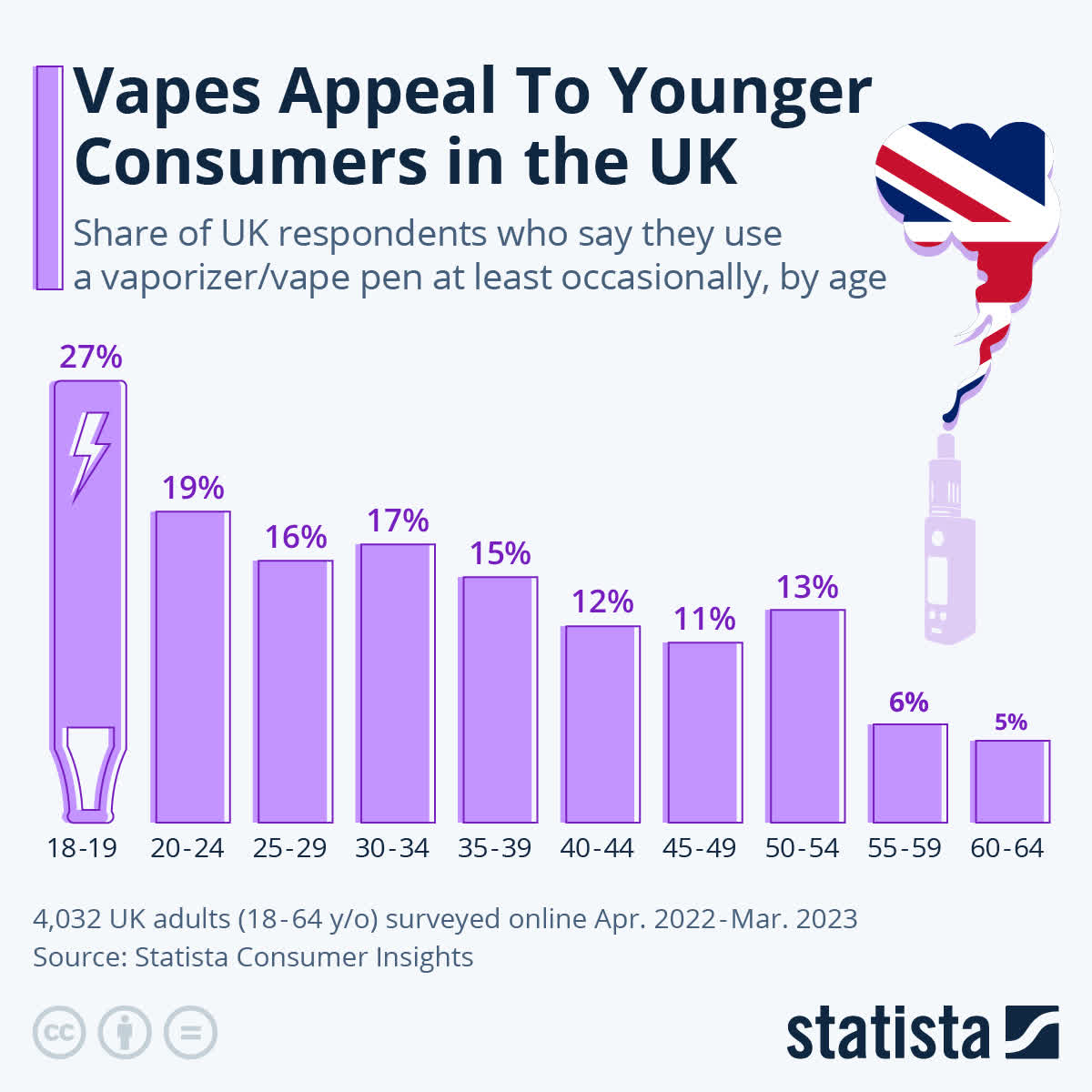

Vaping in the UK (Statista, 2024)

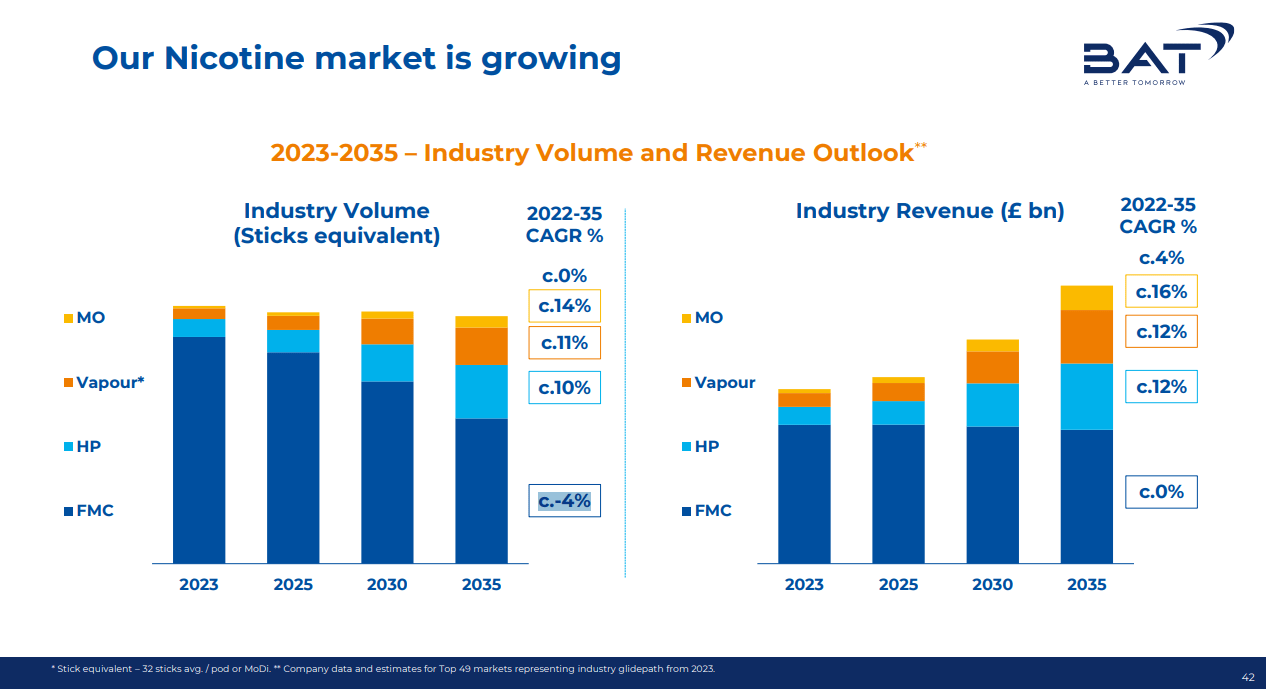

New product categories (e.g., vaping, pouches, and heated tobacco products) are growing surprisingly well at double-digit rates. The company is transitioning towards "reduced harm" products and aims to make about half of its total revenue from this new product category in 2035. According to several scientific studies, these reduced-harm products are indeed less harmful than traditional products that burn tobacco and produce smoke; labelled as "combustibles". It seems that the tar and smoke created during the combustion of traditional cigarettes are the main cause of cancer instead of the nicotine itself.

I will take health claims from big tobacco with a grain of salt and more research is needed, but it seems to me (as far as I can tell) that these new categories are indeed less harmful than traditional cigarettes which is a good thing. Alternative ways of delivering nicotine, like e-cigarettes or pouches, could therefore reduce cancer prevalence, but still allow people to enjoy the effects of nicotine. In conclusion, it seems to me that these new nicotine products have a lot of potential based on the limited research available so far.

Anticipating this, BTI has a market-leading position in the USA with vaping products with their Vuse brand at 40% market share in the US which is the most profitable market. If these new products solve some of the health issues associated with smoking, then this is a great innovation by tobacco companies in my opinion which can help to save both the consumers' health and the company's future profits. However, illicit vape products from China are eating into BTI's market share; BTI is talking with regulators to ban these products.

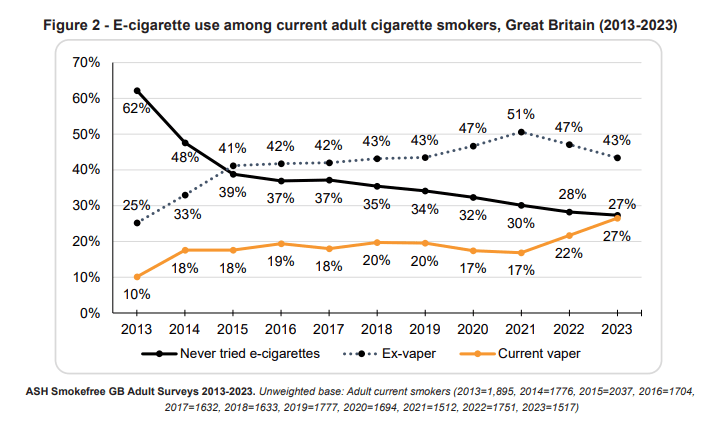

E-Cigarette use in the UK (ASH, 2023)

In contrast with regular smoking, the number of people vaping is actually growing and it is particularly popular among younger people, but the overwhelming majority of smoking worldwide is still done in traditional form with the combustion of cigarettes. Despite these products possibly being less harmful than traditional cigarettes which could help smokers, governments are still trying to reduce vaping and other new kinds of nicotine consumption.

As shown by the FDA crackdown on Juul, vaping is not welcomed by the FDA as the saving grace for the tobacco industry and will likely face similar headwinds from regulation as traditional tobacco products do. The FDA has banned certain colors and flavors in an effort to make vaping less appealing for young people. It remains to be seen whether these products are indeed less harmful and whether the FDA will change its stance on these products as more research on the relative safety of nicotine alternatives becomes available.

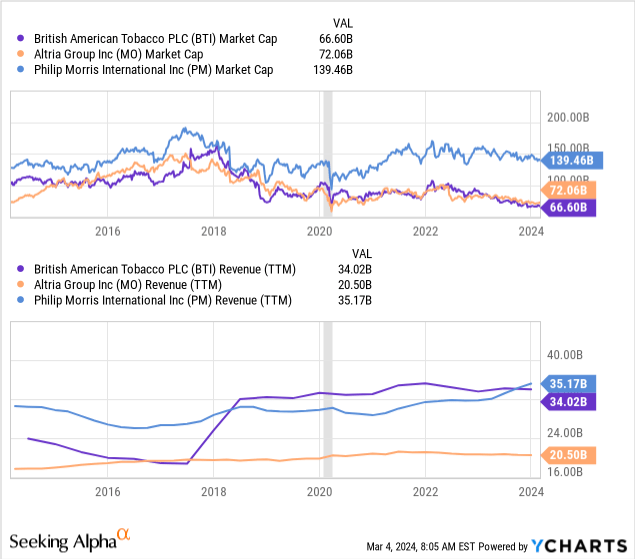

BTI's biggest competitors are Altria Group, Inc. (MO) and Philip Morris International Inc. (PM). On a relative basis, BTI is cheaper because it makes about the same in revenue as Phillip Morris but trades at about half the market cap. Altria is a much smaller company than both, but has a similar market cap as BTI. This higher valuation is due to the slight edge Altria has in the new product categories, and Altria has a 10% stake in Anheuser-Busch InBev SA/NV (BUD) that alone should be worth $12b.

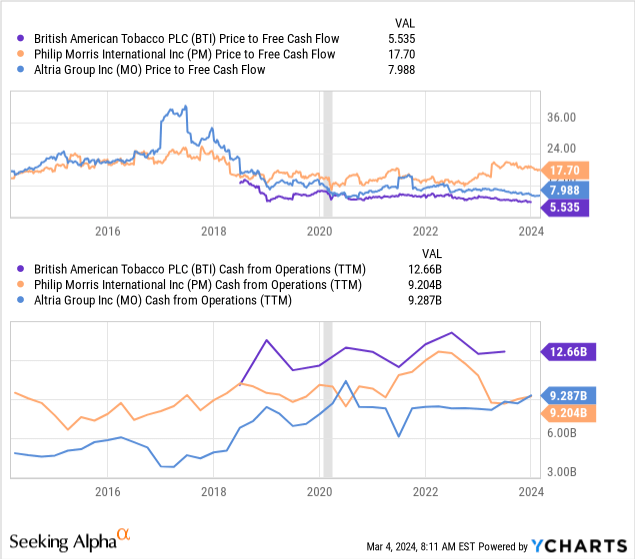

In terms of profitability, BTI actually has the highest operating cash flow out of these three companies, but the lowest market cap. So on a relative basis, it seems that BTI is the cheapest option out of these three tobacco companies. Similarly, BTI trades at 5.5 times free cash flow, which is very cheap even when compared to other tobacco companies like Altria Group, Inc. (MO) trading at 8 times FCF and Philip Morris International Inc. (PM) trading at 18 (!) times FCF.

The difference in valuation between PM and BTI is remarkably large even though they are exposed to many of the same risks and challenges. Importantly, however, PM is further ahead in its transition towards new category products, with about 40% of PM's revenue coming from new categories while BTI makes about 12% of its revenue from new categories. If BTI also manages to pull off its transition like PM did, then the market could take note and re-rate BTI at a higher multiple such as 10 times FCF like PM.

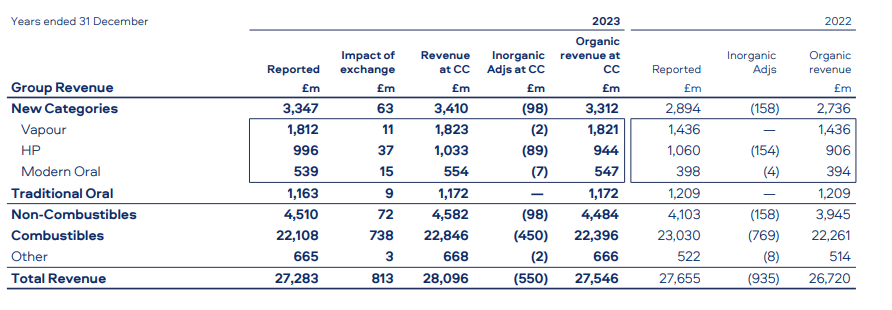

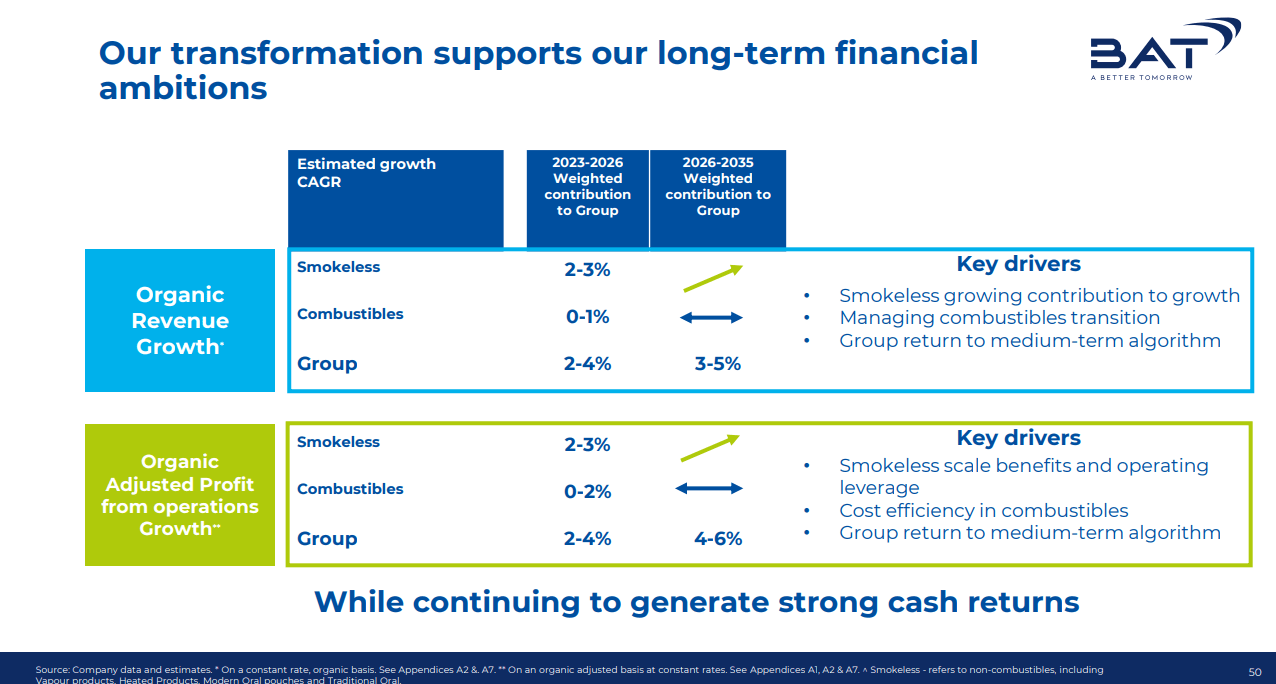

While people expect cigarette sales volume to go down, the company actually manages to report some revenue growth due to price increases every year. The company expects the traditional category of combustibles ("FMC") to gradually decrease in volume over time at about a negative 4% CAGR. However, they expect their revenue from this category to remain flat because of price increases. This seems like a reasonable outlook, but it is quite optimistic. To remain conservative, we project FMC revenues to decline.

In addition to the "traditional" cigarette segment, the company is investing in new categories ("NC") such as vapes, heated tobacco products, and modern oral products which are nicotine pouches such as Zyn (owned by PM). BTI expects all these new categories to grow at double-digit rates. This sounds very positive, but I am quite skeptical about their ability to pull this off. We will make some more conservative forecasts in the following section. We expect these new categories to grow but not at the rates projected by the company.

Revenue Outlook (BTI, FY2023)

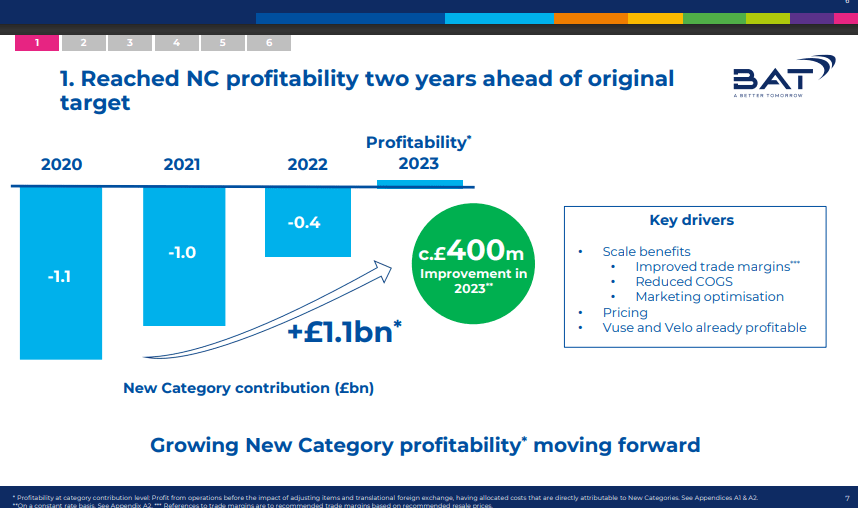

In line with company guidance, we expect declining volumes for the main combustibles segment but some volume growth for the new categories. This volume decline can be partially offset by pricing increases, but we project that FMC revenues will still decrease over time at about 4% annually whereas the company's guidance projects flat revenue for the FMC category. In contrast, their new "reduced risk" category is projected to grow at double digits and make up almost half of the company's revenue in 2035 and most of it beyond that. For FY2025, BTI aims to accelerate the growth of this New Category revenue at a much faster rate than total revenue, reaching £5bn in 2025. This target implies a revenue CAGR of 23% for new categories going to 2025.

This target seems very ambitious, so I am more conservative and expect this new category's growth to moderate instead of accelerate. Growth could slow down after a strong start in recent years due to increased regulation (e.g., banning flavors) and growing awareness of the health risks of these "reduced risk" products. Maintaining double-digit growth rates seems difficult to me, and I expect new categories to grow at about 5-10% maximum.

The company's own forecast is very optimistic, but the market simply isn't buying it. That is why the stock is so cheap compared to other companies, despite their positive outlook showing a 50% revenue increase from now to 2035. The market seems to be pricing in declining revenues and profits instead of reasonable growth for this company. Growth might seem unlikely, but if we look at PM it does seem possible for a tobacco company to re-invent itself.

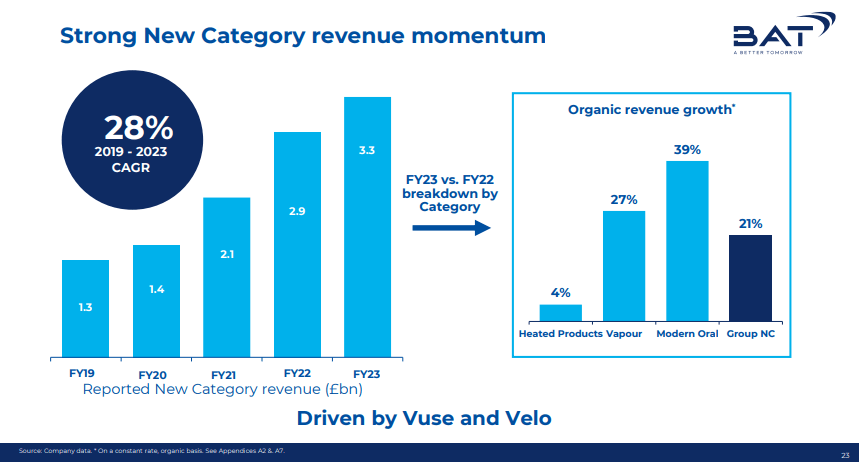

BTI revenue (BTI, FY2023) BTI NC growth (BTI, FY2023)

Looking back at previous growth rates of these new categories, we do see significant growth, but this has slowed down in recent years. This year, NC revenue grew from $2.9B to $3.3B, which is "only" 13.7% revenue growth. Still, especially for a tobacco company, this growth is impressive and I will give them some credit for that. To remain conservative, we expect new categories to grow at a lower growth rate, namely a 5% CAGR for the next five years.

Putting all of this together, I make a more conservative forecast projecting FMC revenues to decline 4% annually and NC revenues to grow at about 5% annually. I also project profitability to decline because the NC is currently less profitable than the FMC products. The new categories have only just turned profitable according to the company (with some creative accounting), but probably still barely breaking even on a GAAP basis. As new categories mature, this might improve but for now, we project declining margins as NC takes revenue share. At the same time, however, increasing prices will improve the profitability of the main legacy FMC segment. On the whole, this cancels out.

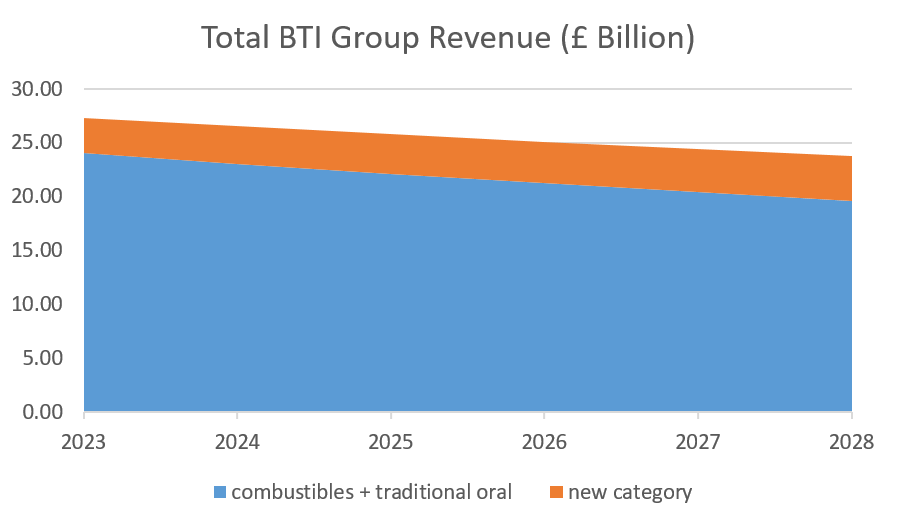

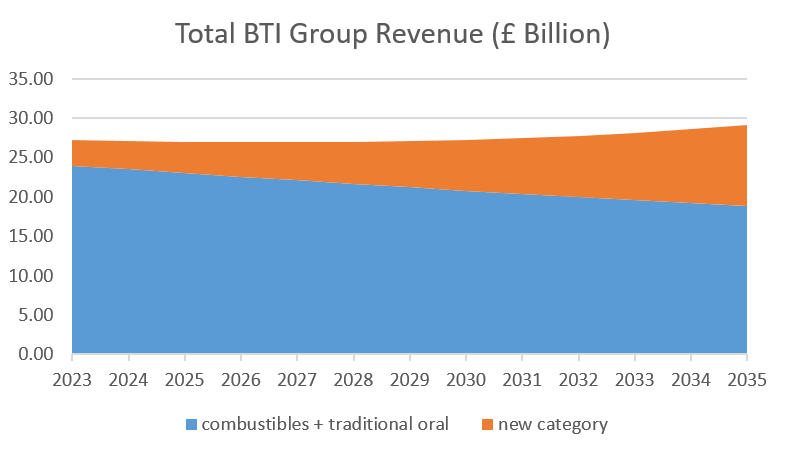

Given our assumptions, we project the main legacy segment of combustibles (-4% CAGR) to do about £18B in revenue in five years' time, which is down £4.1B from £22.1B where it is at today. On the flip side, we expect that new categories will grow at 5% from £4.5bn in 2023 to £5.75bn in 2028. So overall revenue will decrease in this scenario down to about £24-25B from today's levels at £27B. As a percentage of total revenue, we expect new categories to make up 25% of total revenue in 2028 up from 17% today. This is a relatively bearish estimate where total revenue is expected to decline 2-3% annually.

Bearish Revenue Projections (Own Research, 2024)

Importantly, the profitability of the new categories is currently lower than the traditional combustibles segment. So as the NC starts making up more of the total revenue, we expect margins to decrease. However, the company does expect the profitability of this segment to improve as R&D and marketing expenses cool off after establishing this new product category. To remain conservative, we estimate a 25% free cash flow margin that is down 10% from today's levels.

NC profitability (BTI, FY2023)

In terms of margins, we expect a decrease as now 18% of revenue comes from NC in 2028. At the same time, however, price increases will improve margins in the traditional FMC segment. In our bearish scenario, we therefore expect the margins to remain relatively flat or decline slightly from where it is now. The company again has a positive outlook, projecting margins to improve.

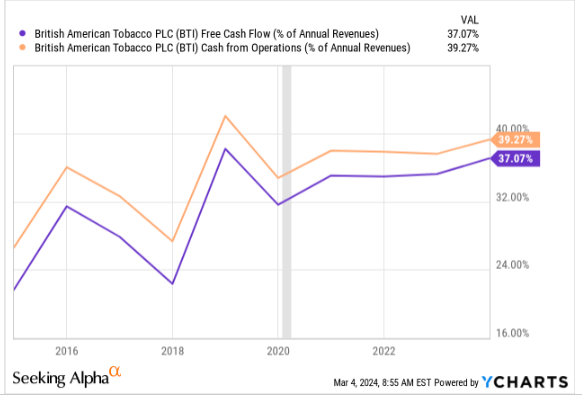

To remain conservative, we project FCF margins to decrease to 30% from where they are now at 40%. These assumptions are very conservative given that profitability has actually improved over time. As shown below, the profitability of the BTI group has actually been increasing as a result of continued price increases in the traditional FMC segment. The company guides NC profitability to improve over time, and profitability from combustibles to improve as well.

Profit Outlook (BTI, FY2024) BTI FCF margins (SA, 2024)

In our bearish projection, we estimate that the company will lose about $4-5B of combustibles revenue over the next five years and drop 10% of its free cash flow margins. Even with these very bearish estimates, this company would still easily return over $7B annually in free cash flow compared to a current market cap of $69b that is a 10% free cash flow yield. This scenario would also allow them to maintain the $5B dividend that they are paying out at the moment. Under this bear case, you can get 50% of your entire initial investment back through dividends by 2028, assuming a constant dividend with 10% yield.

Bullish Revenue Projections (Own Research, 2024)

In the bull case where the company does actually approach its objectives as defined in the outlook, this investment return could be substantially higher. At the moment, the company returned over $10B of free cash flow in FY2023, which is very healthy. Estimating combustibles revenue to still decline but at a lower 2% rate, while NC grows faster at 10% results in a very positive outlook for the company where total group revenue is flat or actually growing in low single digits until 2030 and accelerating significantly beyond that. Here, NC revenue is projected to make up 35% of total group revenue by 2035.

In this bull case, the profitability of NC is improving over time as well. Keeping FCF margins constant at 40% for 2028 would mean that the company will return over $10B in revenue in 2028 which is an FCF yield of more than 15%. In this case, buybacks could be done and the dividend could be raised. A reason for the bull case is the outlook from BTI itself, projecting stable FMC revenue and faster growing NC revenue with improving margins; but this seems a bit too good to be true.

Finally, a successful transition towards NC products could surprise analysts and lead to a re-rating by the market like what happened in the case of PM. In the case where the market re-rates the company to 10 times FCF, we could easily be trading north of the $100b market cap, representing over 100% upside in 5 years time when including 50% of yield from dividends. However, a crucial factor for a long-term investment in this company is the success of NC products.

Capital Allocation (BTI, FY2023)

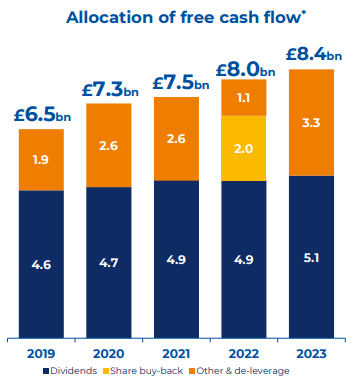

The company makes a lot of free cash flow (>$10b FY2023); they can keep it going with little investments to generate a lot of cash from the legacy FMC segment for the foreseeable future. This free cash flow is currently being returned to shareholders in the form of a dividend, last year over $5B in dividends which is over 50% of the free cash flow. At the current market cap, this dividend is a spectacular 10% yield even at a 50% payout ratio.

Next to this great dividend, buying back stock would be a strong catalyst for stock price returns as well. The company could have easily used $6B of its ample free cash flow in FY2023 to buy back around 10% of shares outstanding and significantly increase shareholder returns. Moreover, buying back stock would reduce recurring expenses for the company because they have to pay dividends to every share outstanding; they're currently paying out >$5B just in dividends annually. Buybacks might be a better allocation of capital than paying dividends in terms of generating shareholder returns.

However, the company still holds a significant amount of debt. BTI paid way too much for the Reynolds acquisition at almost $50B in 2017, and they're still paying down this big debt today. They are currently using their leftover free cash flow to pay down long-term debt. This is a wise decision with interest rates currently at 5%. Importantly, however, I expect that they will continue to pay down debt until they are around a 2-3 LT debt to EBITDA ratio. After that, they can start to buy back stock at around $2b annually. At the current market cap, of about $65b that would be about 3% of shares outstanding annually. Buying back 3% of shares would also save them about $150m annually in dividend payments, which I think is a good investment because this frees up capital for other uses and the shares are undervalued right now.

In conclusion, a significant buyback program (after paying off a significant chunk of the debt) could be the spark to generate shareholder return via both dividend yield and share price appreciation going forward in the coming years.

Our rating for British American Tobacco p.l.c. (BTI) is a "Buy". Even in a worst-case scenario, the shares of the company look significantly undervalued compared to its competitors. Despite little to no growth on a group level or even declining revenues for combustibles, the existing operations of the company are still stable and very profitable which enables them to generate significant value for shareholders. Generating over $10B in free cash flow last year, the company is very efficient and perfectly able to generate shareholder returns.

The company is priced by the market like it's going out of business in the next few years, but this is probably not going to happen as a lot of people still smoke. Moreover, a successful transition towards reduced risk products could actually result in impressive growth numbers that could surprise analysts. The very profitable combustibles category can be used to fund the transition towards new categories such as vaping and pouches, which are growing and seem very promising as less harmful alternatives compared to traditional smoking. A successful transition could also lead to a re-rating by the market as happened with Philip Morris International Inc. (PM) who trade around 3x the valuation of BTI.

Buying BTI now is a cheap investment in a very profitable business. You can collect a 10% dividend yield while the company is still around and churning out free cash flow. Buybacks could be a strong catalyst for shareholder returns next year, and the continued success of new categories might positively surprise a lot of people. The 30% drop from an already bottom-of-the-barrel valuation seems overdone and we expect some share price appreciation next year.

It is an open question whether the company will still be around 30 years from now but betting on the coming five years seems like a reasonably safe bet. In the long term, their transition towards reduced-harm products could be a good way for the company to continue its operations if successful. If this alternative nicotine transition is successful, then BTI could actually surprise a lot of people by actually growing profitably into the future. If not, we can simply sit and collect the dividends of a dwindling but still profitable operation. We shall see!

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.