Scharfsinn86

Scharfsinn86

Note:

I have covered Ballard Power Systems Inc. (NASDAQ:BLDP) previously, so investors should view this as an update to my earlier articles on the company.

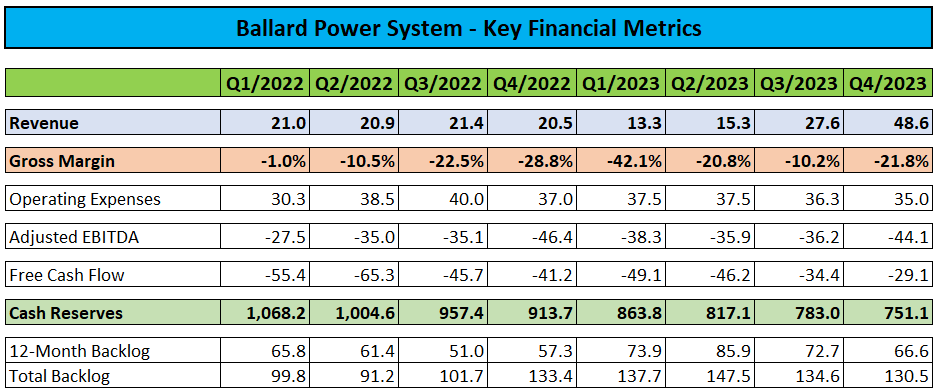

On Monday, leading Canadian fuel cell systems developer Ballard Power Systems Inc. ("Ballard" or "Ballard Power") reported mixed fourth quarter results. While revenues of $46.8 million came in well above consensus expectations, margins were impacted by substantial impairment charges related to "a specific customer experiencing liquidity issues and resulting program delays" as outlined in the company's regulatory filings.

Company Press Releases / Regulatory Filings

Adding insult to injury, the issue also resulted in the requirement to remove a whopping $21.7 million from backlog thus more than offsetting record order intake for the quarter as discussed in more detail by management on the conference call:

We achieved record new order intake of $64.7 million in Q4. Now when we look at our order backlog, it stood at $130.5 million at the end of the year, down 3.3% compared to the end of Q3.

There's some important context here. This new record order intake of $64.7 million in Q4 was more than offset by a reduction of $47.1 million, resulting from record engine shipments during the quarter, and the removal of $21.7 million from our order backlog of previously booked orders from a specific customer now experiencing financing and related program delays.

We believe this was a prudent approach at this time. We're working closely with this customer as they finalize their financing plans to enable a return of orders to the order book and a resumption of shipments in later 2024.

Applying the formula provided by management during the questions-and-answers session of the conference call, 2024 might be another year with no or even negative growth for Ballard Power (emphasis added by author):

Kashy Harrison

(...) Is there a simple way to reconcile the year-end order book, whether it's the 12-month one or the total one to the next 12 months of revenues? Like do you have a simple rule of thumb for how we should be thinking about translating the order book into revenues? (...)

Randy MacEwen

Yes, I think you could probably use 2023 as a bit of a guide, where in 2023 our order book was roughly 60-65% of the revenue that we actually recognized. So in other words, we had order book support coming into the year of in that 60-65% range for full year revenue.

To be fair, the company's 12-month backlog at the beginning of 2023 was just 55% of Ballard Power's full year revenue so there's still hope for at least some year-over-year growth but based on management's directional guidance, I would expect analysts to reduce 2024 expectations across the board.

Similar to previous years, order intake and backlog conversion is expected to be heavily-weighted towards the second half with negative gross margins expected to persist until Q4/2024.

Ballard Power finished the year with $751.1 million in cash and cash equivalents or approximately $2.50 per share, down by $32 million sequentially and $163 million year-over-year. The company continues to have no debt.

At the current rate of cash usage, Ballard Power has runway well into 2028.

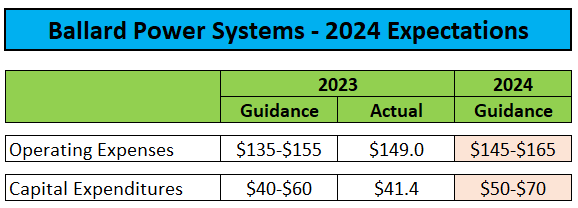

However, the company expects to invest in a new U.S. manufacturing facility this year (emphasis added by author):

In 2023, given an increasingly constructive hydrogen policy landscape and increased market activity in the U.S. and Europe, and given the continued hydrogen fuel cell policy uncertainties and market delays in China, as well as geopolitical risks, we decided to suspend our MEA localization plan in China while we completed a comparative analysis on manufacturing capacity expansion options and possible sequencing prioritization in the U.S. and or European markets.

We've concluded our comparative review and have prioritized the U.S. as the highest priority market for our next manufacturing facility. We have selected a site and are negotiating our land acquisition agreement. As an important part of this process, in 2023, we also submitted certain applications for government funding support in the U.S. when we expect to receive definitive feedback in the near-term.

Consequently, management projected operating expenses and capital expenditures to increase from 2023 levels:

Company Press Release

Unfortunately, the pace of worldwide fuel cell adoption continues to be slow with policy support and investment still nowhere near required levels.

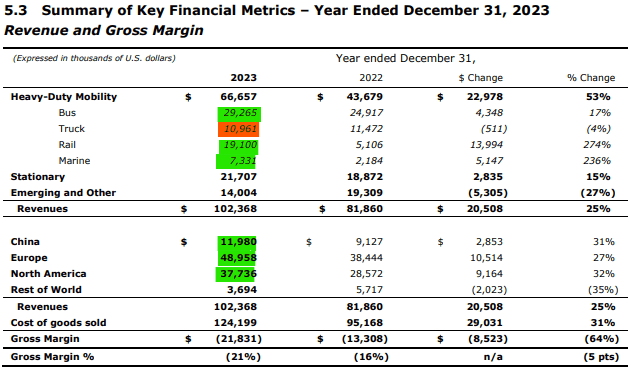

While there has been some progress in some of the company's major focus segments like buses and particularly rail applications, the fuel cell truck market continued to underperform management's expectations in 2023:

Regulatory Filings

Please note that 2022 was an exceptionally weak year for Ballard Power, while the company's 2023 sales performance was more in line with previous years.

Even promising new markets like data centers are not expected to generate material revenues for the company anytime soon, as stated by management on the conference call.

As a result, I would expect Ballard Power's business to remain challenged for the time being, with no clear path to sustained growth and profitability.

Ballard Power Systems reported mixed Q4 results, with strong top line outperformance and record order intake more than offset by substantial impairment charges and negative backlog adjustments after one of the company's larger customers experienced financial troubles.

While cash usage continues to be material, Ballard Power is still sitting on more than $750 million in cash, sufficient for another 4+ years at the current burn rate.

Based on management's directional guidance, 2024 might very well be another year with no or even negative growth for Ballard Power as worldwide fuel cell adoption continues to be slow.

While I don't see a compelling reason for initiating or adding to existing positions, the company's strong cash position is keeping me from outright downgrading shares to "Sell".