Imgorthand

Imgorthand

I have never been skiing in my life. And honestly, I probably will never go skiing. Or snowboarding. Or anything similar to it. I know that if I do, the last thing I will see is a tree rapidly approaching as I slam face-first into it. Having said that, there are many people in this world who love to ski and engage in other snow-related activities. My hat is off to them.

But what I do love is investing and understanding how companies work. That has led me to a company that many engaged in skiing and other related activities certainly can appreciate. And that is none other than Vail Resorts, Inc. (NYSE:MTN), an owner and operator of resorts that largely center around skiing.

The last time I wrote about Vail Resorts was in an article published in August of last year. I acknowledged that shares were attractively priced and that the company had an opportunity to achieve even stronger performance down the road. This was despite shares previously underperforming and mixed financial performance amidst wider economic uncertainty having a negative impact on its fundamentals.

Despite all of this, I ended up rating the company a "buy." Unfortunately, that bullish call has not paid off yet. Like many of its visitors, shares went down. Admittedly, the drop was only by 2.8%. But that's far worse than the 13.9% rise seen by the S&P 500 (SP500) over the same window of time.

Despite these disappointing figures, the fundamental picture for the company looks positive. The first quarter of the 2024 fiscal year did show a degree of weakness that the market has not been fond of. But guidance for 2024 in its entirety makes the company look attractively priced on a forward basis. Of course, this picture can change at a moment's notice. And the fact of the matter is that management is about to report results for the second quarter of the 2024 fiscal year. When this does come to pass, it will be interesting to see how the company has performed relative to analysts' expectations. It will also be intriguing whether or not the firm has made any changes to the guidance.

What news does come out will likely play a sizable role in the direction that shares move. Leading up to that point, I am remaining cautiously optimistic. But it would be helpful for Vail Resorts, Inc. shareholders and market watchers alike to understand what to expect for when that day comes.

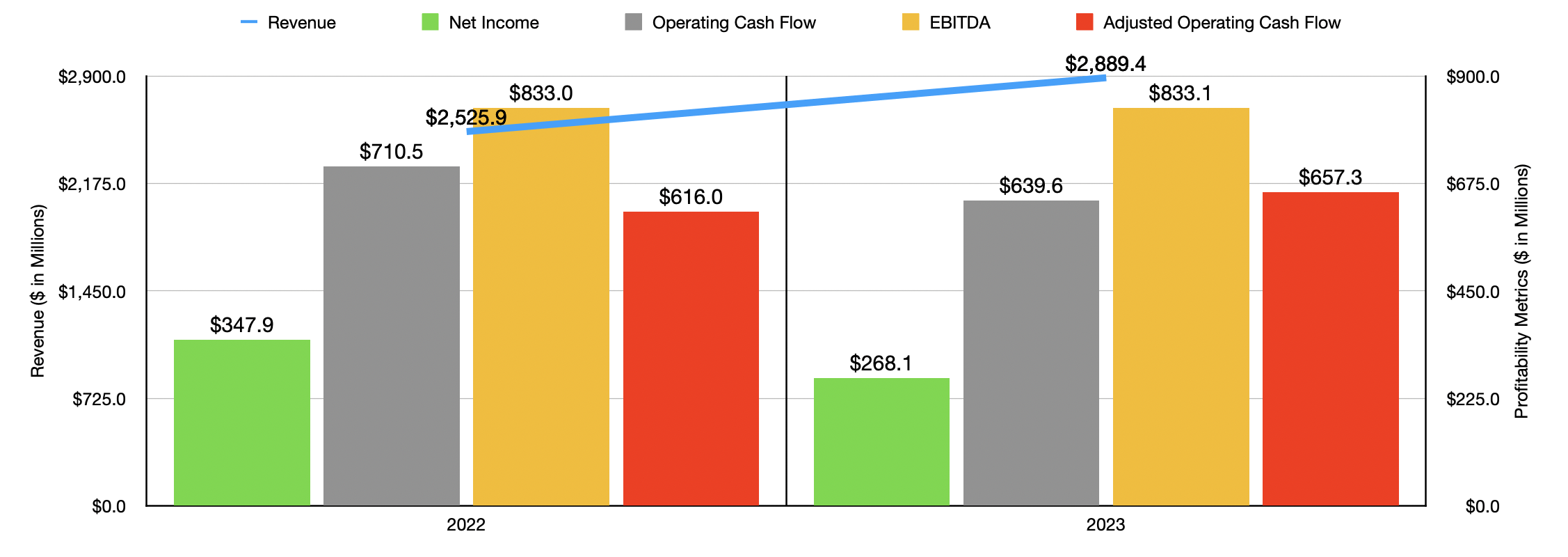

Before we get into expectations set by analysts, it might be helpful to quickly review the financial performance achieved by Vail Resorts. The fact of the matter is that management achieved some really attractive results in 2023. Revenue, for starters, came in at just under $2.89 billion. That's an increase of 14.4% over the $2.53 billion generated in 2022.

For the purpose of transparency, it's important to recognize that there are many different working parts when talking about what comprises the firm's revenue. You have large revenue, which is derived from room rates multiplied by the number of visitors at its resorts. The firm generates revenue from dining, retail and rental activities, ski schooling, and more. But most of its revenue comes from its Lift business, which is mostly made up of pass products and non-pass products related to these same operations.

Author - SEC EDGAR Data

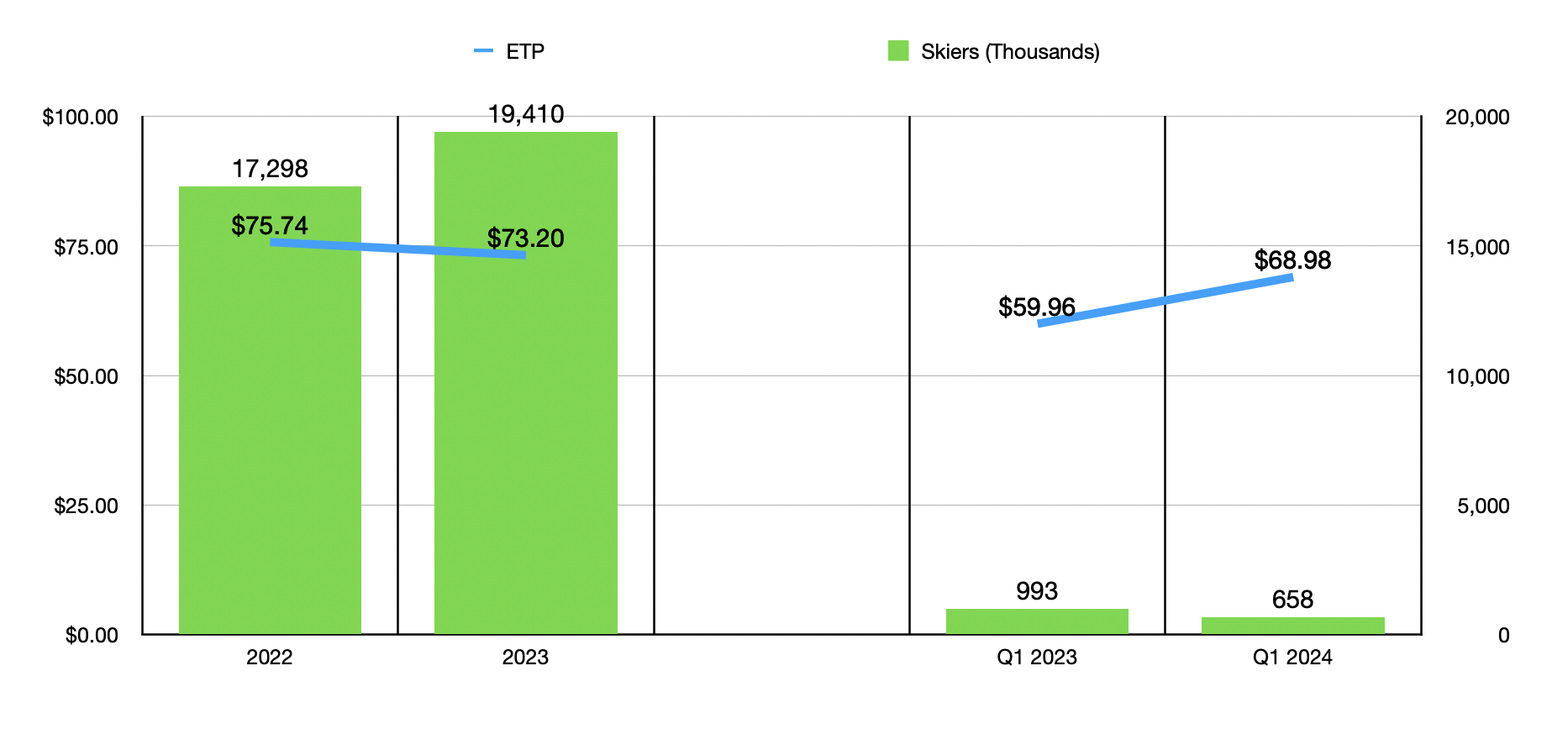

At the end of the day, when you look at the numbers enough, you come to realize that the most significant driver of revenue for the company is ultimately the number of skiers that it receives, combined with what it calls the ETP (effective ticket price) that it charges said skiers. In 2023, Vail Resorts saw 19.41 million skiers. That was up rather significantly from the 17.30 million reported for 2022. This was only marginally offset by a decline in ETP from $75.74 to $73.20.

Author - SEC EDGAR Data

With the increase in sales, you would think that profits would rise as well. But this is where things get a bit complicated. Because of higher labor costs, as well as other expenses aimed at scaling the business, net profits fell from $347.9 million to $268.1 million. Other profitability metrics followed a similar trajectory. Operating cash flow, for instance, went from $710.5 million to $639.6 million. The good news is that if we adjust for changes in working capital, we get a rise from $616 million to $657.3 million. Meanwhile, EBITDA for the firm expanded from $833 million to $833.1 million.

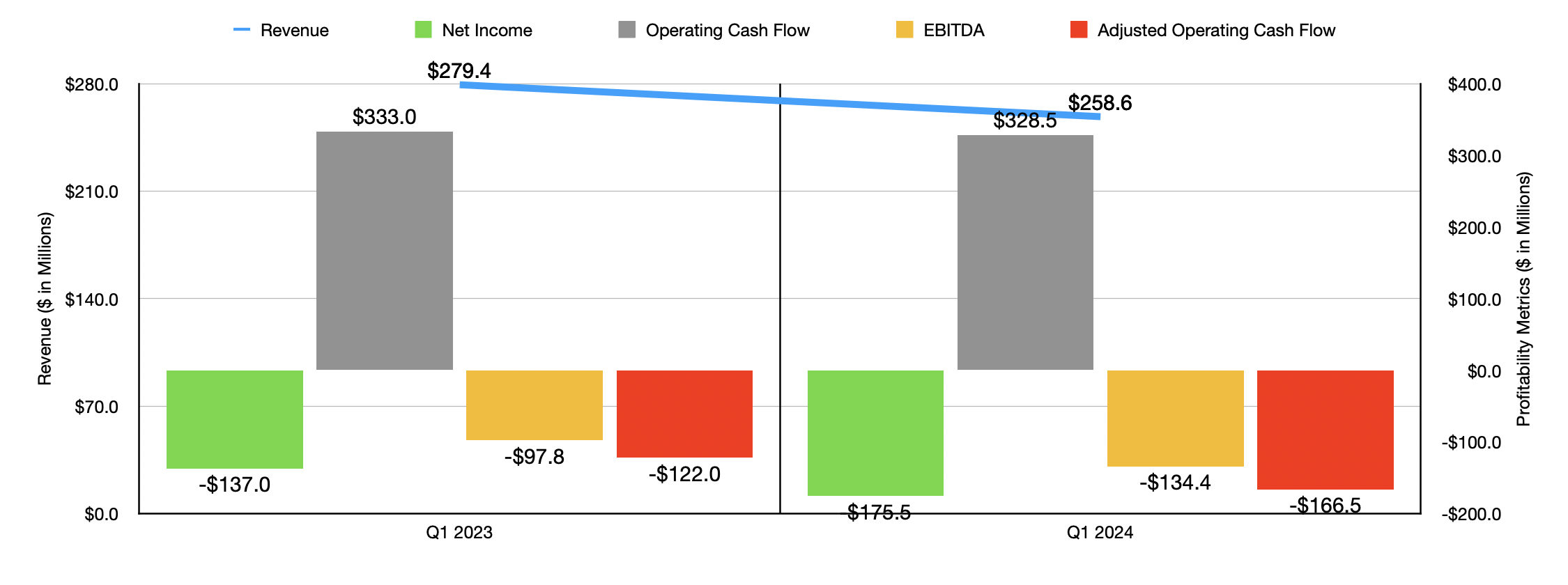

If you were to guess what financial performance would be for 2024 based on results for the fiscal first quarter of the year, you would likely be pessimistic. I say this because revenue of $258.6 million in the first quarter fell short of the $279.4 million generated one year earlier. Even though the company benefited from an increase in ETP from $59.96 to $68.98, it saw the number of skier visits drop from 993,000 to 658,000. This was driven, according to management, mostly by inclement weather. As a result of the decline in revenue, the firm's net loss expanded from $137 million to $175.5 million. Operating cash flow dipped from $333 million to $328.5 million, while the adjusted figure for this went from negative $122 million to negative $166.5 million. And lastly, EBITDA for the company fell from negative $97.8 million to negative $134.4 million.

Author - SEC EDGAR Data

The good news is that the fiscal first quarter is a pretty slow time for the company. In 2023, for instance, it accounted for only 9.7% of the firm's overall revenue despite accounting for basically a quarter of its calendar year. When it comes to the 2022 fiscal year in its entirety, management has not provided guidance from a revenue perspective. But they did say that net profits should come in at between $316 million and $394 million. The midpoint of $355 million would be quite a bit higher than the $268.1 million reported for 2023.

Meanwhile, management said that EBITDA will likely be in the range of between $912 million and $968 million. That same midpoint of $940 million. If we assume that operating cash flow will rise at the same rate that EBITDA did from the $833.1 million the company saw last year, then we would anticipate adjusted operating cash flow rising from $657.3 million to $742 million.

Author - SEC EDGAR Data

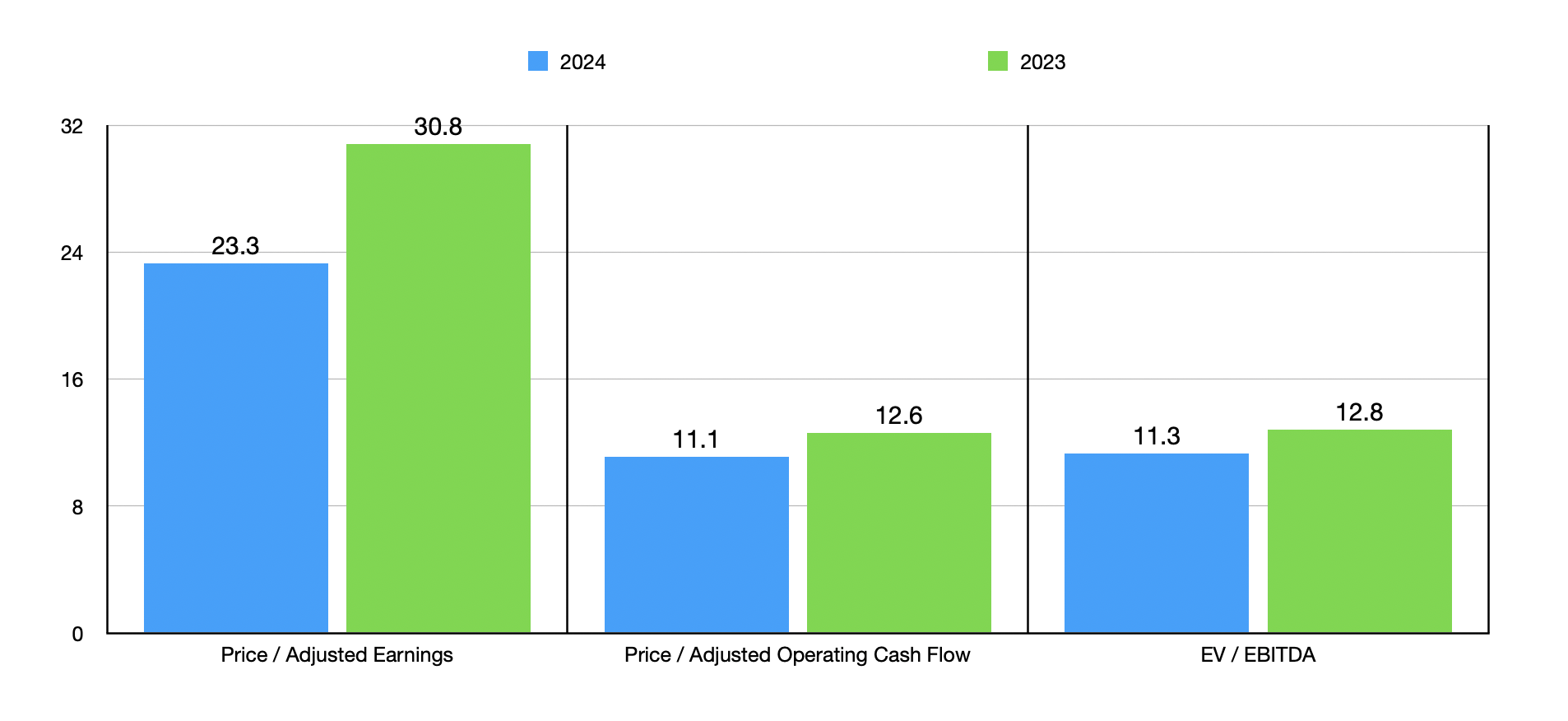

Using these results, valuing Vail Resorts, Inc. becomes quite simple. In the chart above, you can see how stocks are priced using data from 2023 and estimates for 2024. Relative to earnings, shares are very expensive. But when it comes to other profitability metrics, shares don't look bad at all. Relative to similar firms, as the table below illustrates, the stock is slightly on the cheap end of the spectrum. On a price-to-earnings and price-to-operating cash flow basis, only two of the five companies I compared it to ended up being cheaper than it. And only one of the five ended up being cheaper when it comes to the EV-to-EBITDA approach. Now to be fair, none of these companies are all that comparable to Vail Resorts. But they are probably as close as we are going to get.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Vail Resorts | 30.8 | 12.6 | 12.8 |

| Planet Fitness, Inc. (PLNT) | 39.4 | 16.7 | 15.8 |

| Six Flags Entertainment Corporation (SIX) | 55.7 | 8.3 | 13.1 |

| Cedar Fair, L.P. (FUN) | 17.1 | 6.6 | 9.3 |

| Hilton Worldwide Holdings Inc. (HLT) | 47.1 | 27.6 | 25.8 |

| Marriott International, Inc. (MAR) | 24.3 | 23.7 | 19.7 |

All things considered, the stock looks to be decently priced, and it is a high quality business that has achieved attractive growth in prior years. But as I mentioned earlier in this article, we need to be paying attention to what other data comes out. On March 11th, after the market closes, the management team at Vail Resorts is expected to announce financial results covering the fiscal second quarter of its 2024 fiscal year.

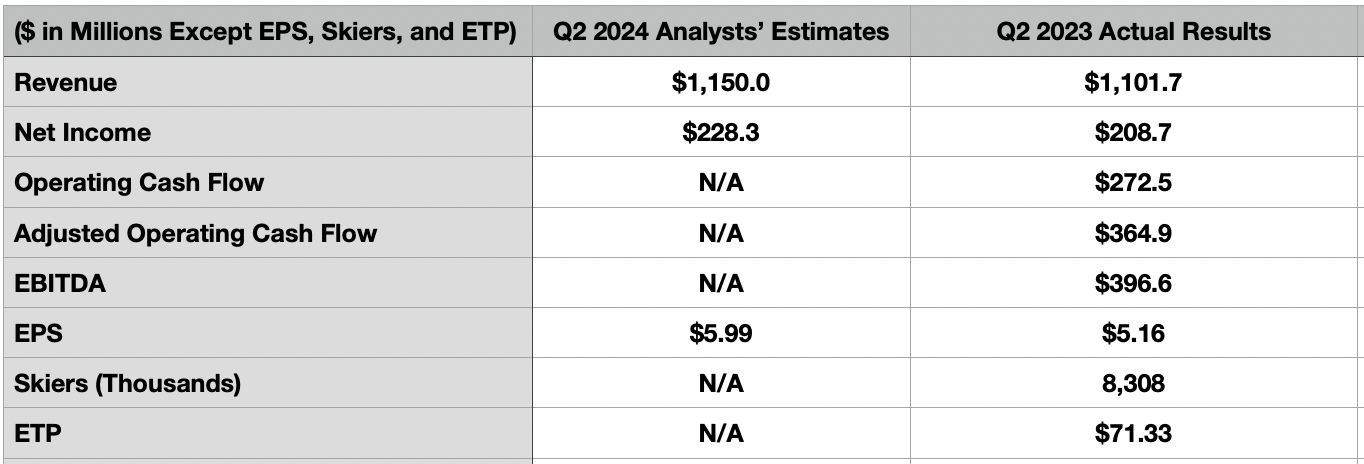

In the table below, you can see current expectations stacked against what the company achieved in the same quarter of 2023. Revenue, for instance, is expected to come in at $1.15 billion. If this comes to fruition, it would be about 4.4% above the $1.10 billion generated at the same time of the 2023 fiscal year.

Author - SEC EDGAR Data

Earnings per share for the second quarter are expected to be about $5.99. This would represent a nice improvement over the $5.16 per share generated in the second quarter of 2023. That would translate to net profits rising from $208.7 million last year to $242.9 million this year. Other metrics do not have corresponding guidance. But in the aforementioned table, you can see operating cash flow, adjusted operating cash flow, and EBITDA for Vail Resorts. You can also see that, during the second quarter of 2023, the firm boasted 8.31 million skiers with an ETP of $71.33. I wouldn't be surprised to see the number of skiers decline somewhat year over year, even as a rise in the ETP increases sales.

Longer term, the company aims to continue growing by means of acquisition. Its operations have historically largely been centered in North America. However, the company has begun expanding overseas. It has made some investments, for instance, throughout Asia. But a lot of the potential for it seems to be in Europe. This is because the European market for skiing is estimated to be three times the size of what it is in North America. The latest investment that Vail Resorts made in Europe came at the end of November of last year when it acquired the Crans-Montana Mountain Resort in Switzerland at an undisclosed price. This makes it the company's second ski resort in Europe, the other one being its majority ownership of Andermatt-Sedrun.

I understand why Vail Resorts investors might be a bit cautious at this point in time. Shares underperformed the market for quite a while now. Having said that, relative to cash flows, the stock does not look terribly pricey at all. If anything, it might be around fair value or only slightly below that. But when you factor in continued growth, both by means of acquisition and by means of additional revenue from higher ETP, the long-term outlook looks positive.

Of course, this picture can always change, and the most likely time for such a change would be when earnings are reported. That's why investors and market watchers alike should be paying careful attention to earnings results that come out in the coming days. But for now, I think maintaining a bullish stance on Vail Resorts, Inc. makes sense.