Ingus Kruklitis

Ingus Kruklitis

Piedmont Lithium (NASDAQ:PLL) is a US-based mining company focusing on lithium hydroxide production with operations in the US, Canada, and Ghana.

Share performance has been relatively weak since going public in 2018 in NASDAQ. PLL went public at around $17.2 per share, but upon reaching an all-time high of $79 in 2021 and trading sideways at a relatively elevated price level of $50 - $70 in 2022, PLL has been trending downwards considerably since the start of 2023. Today, the stock is trading at merely $11, down by staggering 77% over the past year alone.

I initiate my coverage with a buy rating. My 1-year price target of $15 presents a 38% upside from $11 today.

10K

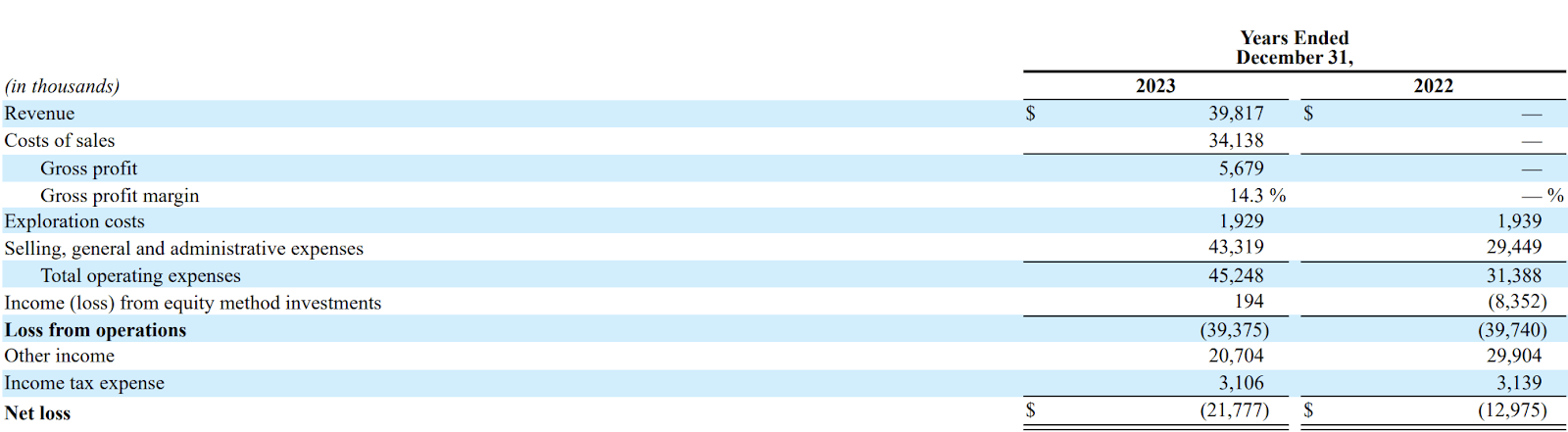

PLL started generating revenue from the offtake contract with Sayona Quebec in FY 2023. However, despite realizing a $39.8 million of revenue, PLL has not yet achieved an operating profitability. While I would expect exploration costs to remain steady every year due to the nature of PLL’s mining business, the biggest drag to operating profit has been SG&A expenses. SG&A expenses already increased by 1.5x YoY to $43 million in FY 2023, surpassing revenue. As such, despite realizing revenue, net loss actually widened to -$21.8 million in FY 2023.

company presentation

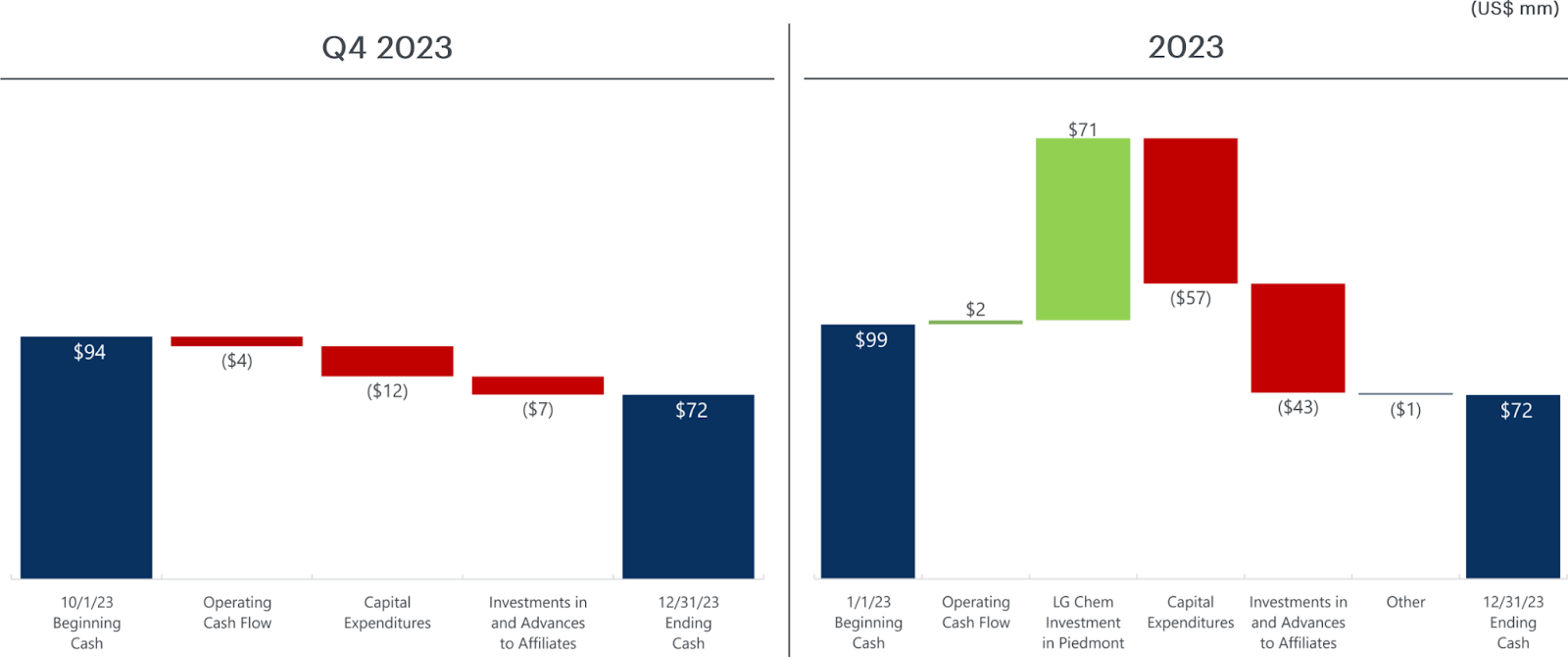

PLL seems to still have a decent liquidity position today despite the intensive business activities in FY 2023, partially thanks to the $71 million investments from LG Chem. In FY 2023, there were two major uses of cash. Firstly, PLL spent over $57 million for CAPEX needs, primarily in its Lithium sites in Tennessee and Carolina. Secondly, PLL also spent $43 million for investments and advances to affiliates. The spending here was related to PLL’s business activities in Ghana and also its relationship with Sayona Quebec. PLL finished the year with $72 million of cash, which should be sufficient to sustain PLL’s operations into FY 2024, given the lower CAPEX outlook.

As we look beyond the temporary headwinds caused by the lower global lithium price today, there are some identifiable catalysts that should help boost liquidity and drive demand growth upon recovery.

10K

As a start, PLL will enter Q1 2024 with more liquidity after successfully selling its shares in Sayona Mining for over $41.4 million. With over $113 million of cash today, it means PLL also begins the year with an even stronger balance sheet than it did in 2023. Overall, I believe the move towards conserving capital is a sound decision to anticipate a potentially prolonged downturn. Given the broader challenges faced by many companies across the EV / Electric Vehicle value chain today, I believe PLL’s management is acting prudently.

company presentation

Furthermore, optimisations are also taking place across different areas of the business. For instance, PLL will reduce CAPEX to merely $10 million to $14 million in FY 2024, already 75% lower than in FY 2023.

company presentation

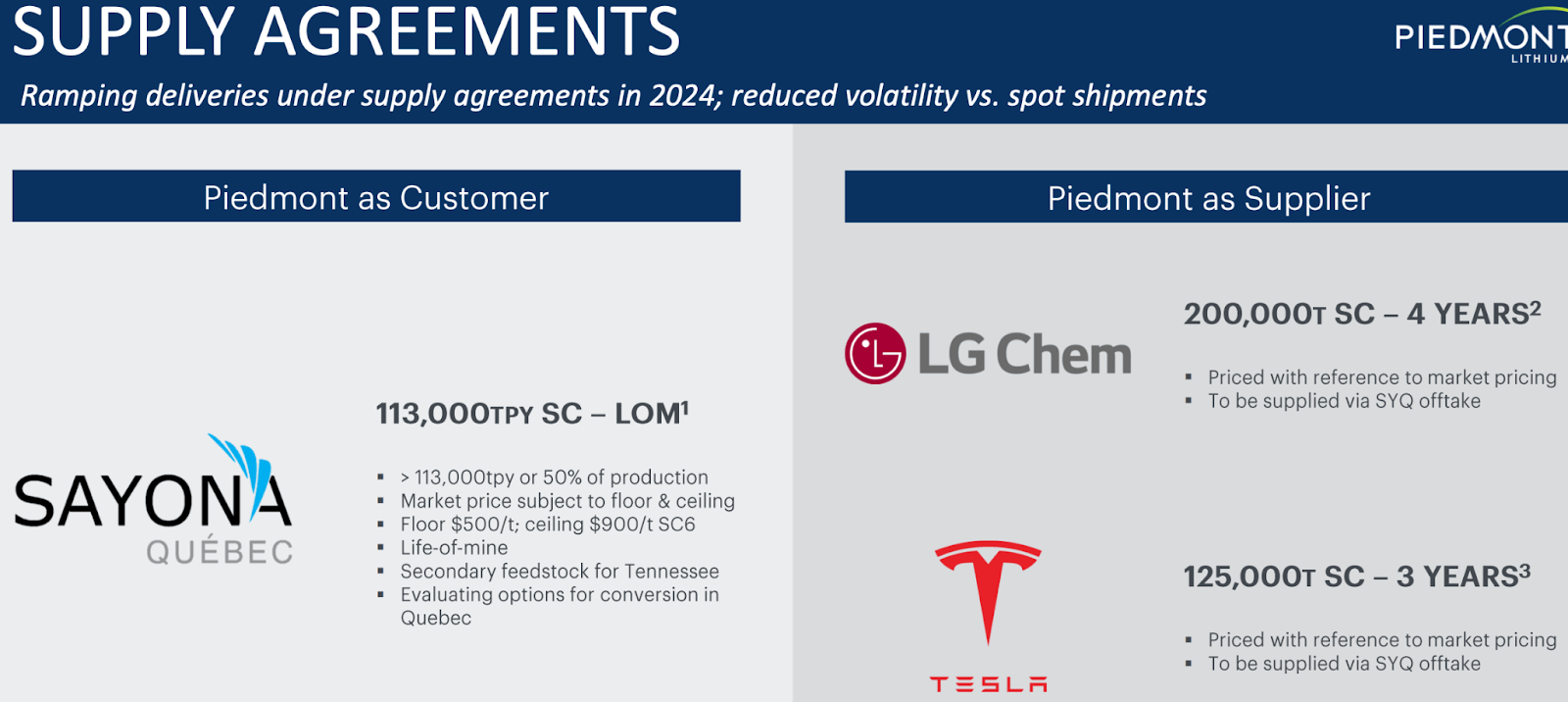

PLL has also optimized the structures of its offtake contracts across buying and selling in 2024. In both cases, I believe the terms should be relatively favorable to PLL. On the buying side, for instance, PLL will lock in a ceiling price of $900 / tonne for the SC6 / Spodumene Concentrate produced by Sayona Quebec, suggesting that PLL should not pay more than the market average today, reducing downside risk. On the selling side, PLL has also shifted away from spot and towards market pricing strategy, which should reduce pricing volatility and improve margin predictability:

According to the terms, the SC6 pricing will be determined by a formula-based mechanism linked to average market prices for lithium hydroxide monohydrate throughout the term of the agreement. The pricing received by Piedmont under the agreement with Tesla will be determined by market prices at the time of each shipment.

Source: Piedmont Lithium.

company presentation

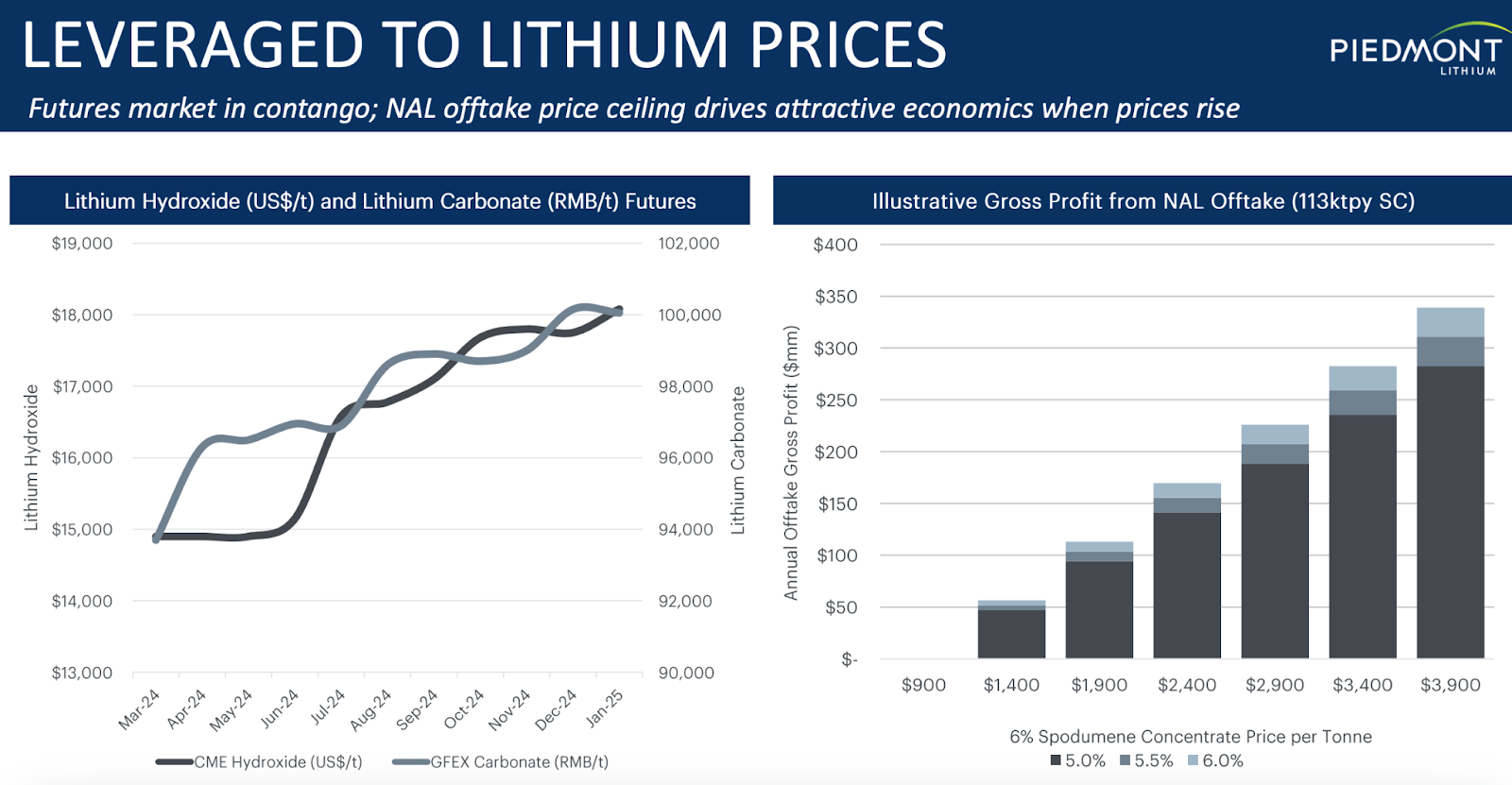

Furthermore, there are early signs of potential industry recovery in 2024, with the futures market remaining in contango, meaning that there is a broader market expectation of higher prices in the future for LiOH and Lithium Carbonate. This should also positively affect the SC6 market price, which could be close to bottoming out at $900 / tonne today. With offtake ceiling price set at that level at least for the rest of 2024, PLL could unlock higher growth with significant gross profit upside in case a rebound happens earlier, in my opinion.

In my opinion, uncertainties remain high in 2024. For instance, though PLL’s forecast suggests that lithium prices could remain steady at the current level, the recent industry developments have suggested otherwise.

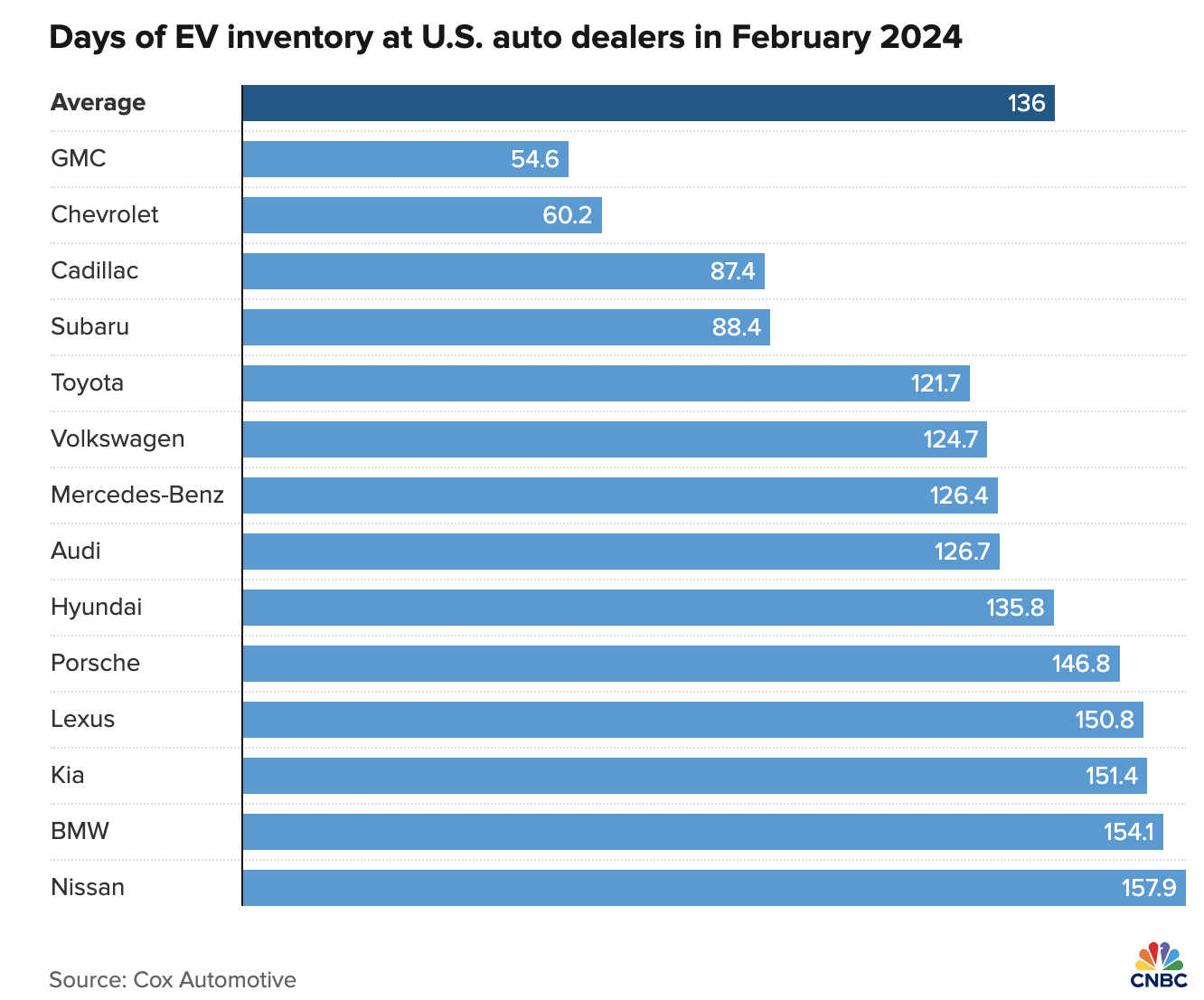

CNBC / cox automotive

A report by CNBC last week points to potentially slower EV demand growth as many major automakers are struggling with higher inventory days in the US as of late. On a more important note, this recent data point implies that it could probably take some time before we can see accelerating EV demand that would help push up prices of raw materials, such as lithium. The weakness in the US EV market could then considerably impact PLL’s top-line growth, since PLL only generates revenue from its NAL / North American Lithium site at least for the time being.

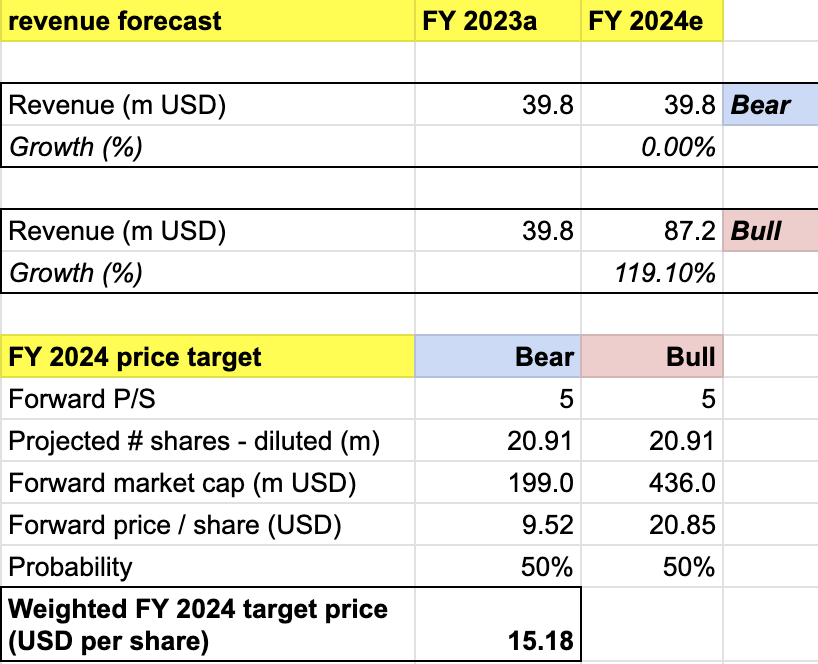

My target price for PLL is driven by the following assumptions for the bull vs bear scenarios of the FY 2024 projection:

Bull scenario (50% probability) assumptions - PLL to achieve an FY 2024 revenue of $87 million, a 119% growth, at the mid-end of analysts’ estimates. I assign PLL a forward P/S of 5x, which implies a share price appreciation to $21. In this scenario, I would expect PLL to successfully complete more shipments at a market price average, with lithium market recovery happening possibly towards the end of the FY.

Bear scenario (50% probability) assumptions - PLL to deliver FY 2024 revenue of $39.8 million, assuming a flat YoY growth. In this scenario, I expect PLL to have a 5x P/S with a price correction to $9.5. I would also expect a stagnant or even worsen lithium market outlook into 2024.

own analysis

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of $15.2 per share, presenting a potential upside of 38% from the current level. At this point, I would give the stock a buy rating.

As an important note, it is relatively challenging to project PLL’s revenue growth due to the lack of visibility into the mechanics of its sales contracts and lithium price forecast. In light of that, I resort to project conservatively across both scenarios. My price target model is already more conservative than the market’s, as highlighted by the assumption of flat revenue growth in the bear case with lower P/S multiple than 5.5x, where PLL is trading on a TTM basis today. My bull case projection also uses the average of the market’s revenue estimate instead of the high end one.

I conclude that PLL remains an attractive long-term opportunity due to its solid assets and execution track record. Despite the temporary headwinds, PLL is also in a good position to stay resilient, given its strong balance sheet. At $11 today, PLL appears undervalued, and is also far off from its 1-year high of $60. As such, I believe the recent pullback as a result of the temporary headwinds and potentially weak sentiment present a viable entry point for long-term investors. I rate the stock a buy, with a conservative 1-year price target of $15.