FatCamera/E+ via Getty Images

FatCamera/E+ via Getty Images

The Children's Place (NASDAQ:PLCE) is an American apparel retailer focused on children's apparel.

The company has had three terrible years after the pandemic, caused by what I believe are some terrible management decisions—this led to the company leveraging and facing bankruptcy risks just weeks ago.

The panic caused by the potential default made the stock price fall more than 50%, at this point, a strategic investor (a value fund from Saudi Arabia) quickly purchased up to 54% of the company's stock. In the meantime, it provided an interest-free loan, and the company renegotiated some financing. I believe that this investor will try to equitize the company further via share rights and potentially increase its stake to 75%.

The new controller already has 4 board members (out of 10), and replaced the Chairman, while another 4 members are expected to resign before the end of March, at which point the new controller will control the Board. Further, in the May shareholder meeting, the controller will probably succeed in electing 11 members and renovating the whole Board.

I firmly believe that PLCE's problems are not permanent but caused by wrong decisions that can be reverted (with some pain), mainly related to positioning and promotional activity. PLCE's strong brand has the customer connection necessary to recover profitability soon. In the meantime, the existence of a large shareholder with deep pockets reduces financing risk significantly.

I believe PLCE is a speculative buy now, with more to be deployed at lower prices and with better visibility. I rate with a Hold because I believe a Buy can only be issued for companies where a concentrated, high confidence investment can be made. PLCE does not exhibit those conditions because of its financially delicate situation, despite some promising signals.

Many apparel retailers after the pandemic boom, especially in the value/discount segment. But few are as leveraged and unprofitable as PLCE.

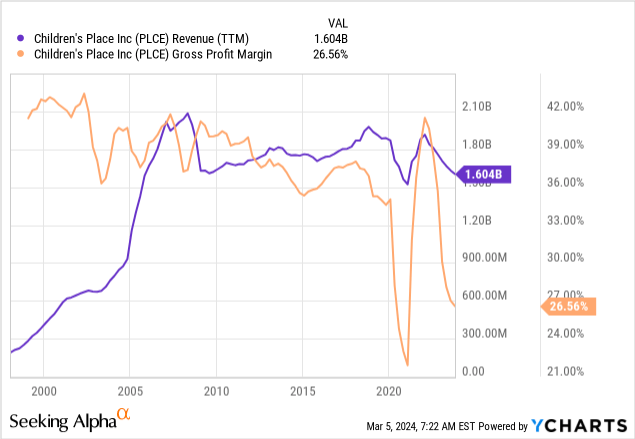

The company's revenues are at historic lows not seen since before the GFC, and its margins are at lows never seen before. At the operating level, losses are already mounting at 10% of net revenues (according to the 4Q23 earnings pre-release).

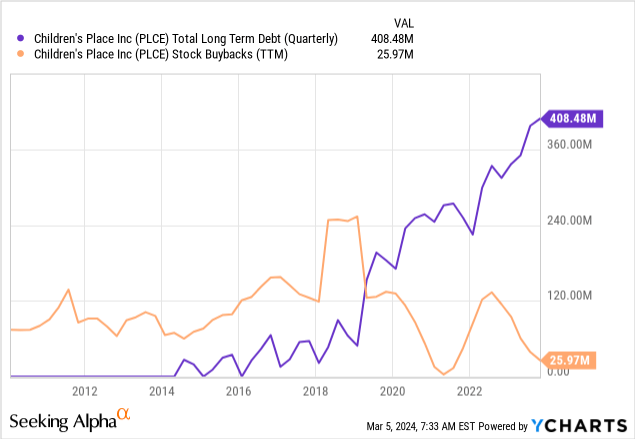

PLCE's high leverage aggravates this critical situation. The company consistently increased debt after the pandemic, drawing more and more from its credit facility. This happens to retailers when they are having margin problems: they ask for credit for the season, buy stuff that doesn't sell well, get a discount, and then can't repay the credit, so they must ask for more.

The problem was made worse by the decision to repurchase close to $300 million in shares while leveraging.

When the company pre-released 4Q23 data a month ago, it announced that it might breach its credit facility covenants (the assets backing the loans are insufficient or EBITDA coverage ratios are not high enough), and the market dumped the stock in panic.

While the market was panicking, a fund called Mithaq Capital rapidly made block purchases at prices averaging $11. In weeks, the fund moved from an ownership not mentioned in the FY22 proxy to 54% of the company's stock.

Mithaq Capital is a public/private-equity fund from the family office of the AlRajhi family, one of the wealthiest in Saudi Arabia. In its presentation to PLCE shareholders via press release, the fund described itself this way: 'Mithaq follows a disciplined value investing approach with margin-of-safety as a principle. Mithaq is a strategic long-term shareholder with a history of owning high-quality businesses, supporting first-class management teams, and championing long-standing partnerships based primarily on trust.' Music to my ears.

The most pressing issue to resolve was the financing situation. The company announced that the breach of the covenants information release had already caused problems with suppliers not extending payables credit. The change in control, which was effective when Mithaq crossed the 50% ownership threshold, caused more covenant breaches.

Mithaq announced it would lend $78 million in interest-free loans to PLCE. Additional terms for the loan (like warrants or discounts to principal that would amount as interest, or convertible options) have not been disclosed.

The company also announced the term sheet for an additional $130 million loan from a private credit fund with experience in distressed retailers (Gordon Brothers), yielding SOFR + 9%.

The company's situation is dire, and the spread over SOFR reflects that. The company's breached credit facility yields only 1.5% above SOFR.

The situation seems to have stabilized. A waiver of the change of control breach was announced, but the credit facility will probably be renegotiated at higher spreads. More on this later.

When the interest-free loan was announced, PLCE also announced that Mithaq had requested to replace the Chairman with a member of the fund's family, plus replacing another 3 directors. In addition, when the second portion of the loan was distributed, 4 directors from the Board should resign, leaving the seats at 6, and Mithaq in effective control. Mithaq has already announced that it plans to propose 11 directors for the May 2024 shareholder meeting. They will probably succeed in this vote.

Mithaq also requested the implementation of a rights registration for $90 million. A right allows each shareholder to purchase a share at a prespecified price. Issuing rights is raising capital from current shareholders without tapping the external market. This equity will probably be used to strengthen the company's balance sheet.

The rights also allow Mithaq to continue investing in the company and increase its stake. If the company wants to raise $90 million, considering a share price of $15, it would have to issue 6 million rights. At 13 million shares outstanding, each shareholder would receive about one right for every two shares.

If all shareholders exercise their rights (paying the $15), the company receives $90 million and issues 6 million shares, but the relative weights of each shareholder are unchanged. However, if only some shareholders use the rights, or if some shareholders sell the rights to others, then the relative stakes are changed. In the limit, if Mithaq exercised all of its rights and no one else did, it could purchase 3.2 million shares, increasing its stake to 63%. If it bought rights from other shareholders, it would grow its stake even more, potentially to 75%.

These figures are illustrative and depend on the effective terms of the rights issued (specifically, how many rights per share and the exercise price). The terms of the rights are not public (the Exhibit D of the Letter Agreement regulating their registration was not released).

One thing is sure in my view: Mithaq likely wants to invest more money in the company directly into equity and refinance the balance sheet, inviting others to join or have their stakes diluted.

The question is, can PLCE recover? Was the company having structural problems, or did a lack of skill cause this?

The company's operations for most of the pre-pandemic decade were profitable, with operating margins averaging 5%. Further, the company did not grow, but between 2013 and 2022, it closed more than half of its store fleet, shifting to a more digital-centric model. This means that it was able to restructure without much pain.

However, as seen above, things started becoming more volatile and trending south after the pandemic. The debt problem was already analyzed. As mentioned, the culprits of debt accumulation were arguably irresponsible share repurchases and the gross profit deterioration seen above.

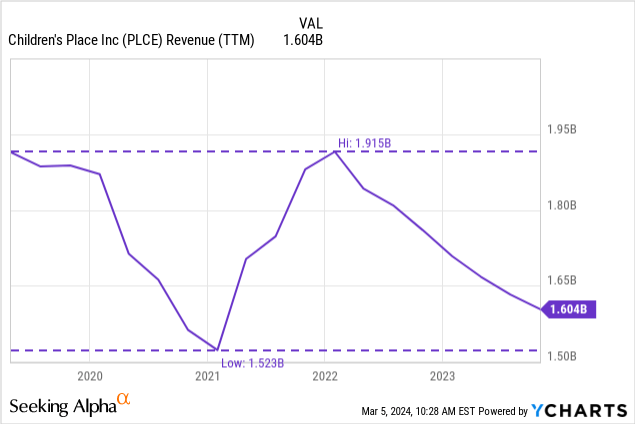

Between TTM figures and the all-time high achieved in FY21, PLCE's revenues fell 16% ($1.6 billion today compared to $1.9 billion in FY21).

Management has consistently attached the problem to inflation and a high promotional environment. This language can be found in the MD&A from FY22 and the 3Q23 reports. For example, from the FY22 MD&A: 'The decrease in gross margin resulted primarily from higher cotton and inbound supply chain costs, and lower merchandise margins due to a highly promotional environment'. Or in the company's 3Q23 earnings call: 'These results were in the face of continued macroeconomic challenges, including persistent inflation, a highly promotional retail environment.'

I believe promotions, and not the macroeconomy, are the cause of the low margins and also of the lower revenues. The demonstration requires some arithmetic.

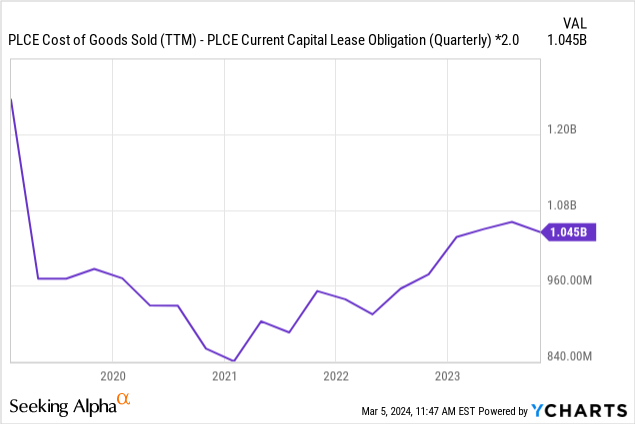

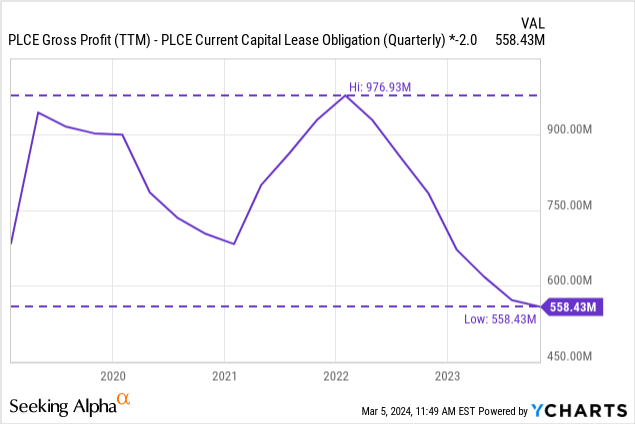

First, PLCE records its lease costs as parts of CoGS. We need to remove this figure from CoGS and add it back to gross profits to get an idea of the contribution margins that PLCE has obtained from its more variable costs (supplies, deliveries, etc.).

PLCE's annualized lease costs amount to close to $120 million. This figure is unavailable directly in my charting software, so I will use current capital lease obligations (recorded as $66 million because they represent minimum payments) by 2.

The general belief when margins fall in the retail industry is that it is caused by deleveraging. That is, the margins over variable costs (the contribution margin) are fixed but spread over lower volumes, which leads to not covering fixed costs.

However, if that were the case, we should see CoGS, excluding fixed costs (rent expenses), go down, consistent with a fall in volume. The chart below shows that this is not the case. PLCE's CoGS ex-rent went up, indicating that either volumes are fixed and input costs are up (possibly given the inflationary context) or that volumes are going up and inputs are fixed. This is an indication that PLCE is not selling fewer units.

When we look at the total contribution from variable costs (approximately revenues minus cost of apparel minus freight and distribution), we see that it falls significantly, more than $400 million, between the peak and the current low. Further, looking at the second chart below, this is approximately how much revenues have fallen from the same peak ($300 million).

This data indicates that PLCE is not selling fewer units but that each unit is contributing less profits. The reason, I believe, is heavy promotions.

One indication is obviously that management blames the margin falls on the 'heavy-promotional environment,' another way of saying 'if we don't discount, customers go to other stores.'

The second indication is a visit to the company's website. When I visited the webstore in early March, the home page offered 80% off on clearance, 30% on any $100 purchase, $10 back for every $20 spent, and free shipping on orders of $20. It's almost as if the company is basically giving its product away.

The situation is repeated at the store level, as almost any Children's Place storefront picture from Google Images shows inventory clearance and big discounts on the front windows.

In apparel retailing, and particularly in strong brands, discounting is almost a sin. The problem with promotions is that it is a race to the bottom, where the only winner is the customer. Further, it alienates customers from expecting promotions before purchasing and cheapens the brand. The company is not selling more units because it is running promotions (clear from COGS minus lease costs), only earning less money per piece.

Another culprit of promotions is bad merchandising. If the company's designers and buyers are not good, they may have too much inventory by the end of the season, and promoting it is the only way to regenerate cash to purchase products for the following season. This last point is made worse by leverage.

The good thing is that this problem can be solved.

The first step is to strengthen the company's balance sheet. This allows the company to extend its cash cycle, reducing the pressing need to get rid of old inventory to purchase new inventory.

The second aspect is running fewer or no promotions. This is akin to withdrawal syndrome for a drug addict. Customers can feel they no longer find value in Children's Place because they were taught to purchase based on price. Sales can fall until the company can rebuild its trust and image with customers based on suitable products and emotional aspects. We will work with several scenarios later.

I believe PLCE has a brand that can be purchased on value and not on price alone. The company has been running an inconsistent strategy, mixing rock-bottom prices and promotions with heavy aspirational advertising.

Last year, the company spent $50 million on advertising. This included hiring the expensive help of stars like Mariah Carey, Snoop Dog, and the Jonas Brothers to run campaigns for the company. Hiring these superstars to promote your brand on TV while running 30% discounts, free shipping, and 80% off clearance is inconsistent marketing in my view.

However, this inconsistency can be corrected by maintaining the advertising and branding efforts and elevating the price to a reasonable level with those expectations.

The company has signs of customer goodwill. For example, its apps have 150 and 60 thousand ratings in the App Store and Play Store, respectively, with 4.8 stars on average. The company's website boasts 5 million monthly visitors on Semrush. 80% of its sales are done via its loyalty program or its private label credit card program.

I believe PLCE has great assets, but it has failed to make use of them, falling victim of the promotion drug. As a final example, the company posts excellent photos of children with their products on the Investor Presentation, but its webstore grid is plain. Why not use good assets on the webstore?

PLCE's stock photos from Holidays catalog (PLCE Investor Presentation)

PLCE is only an opportunity if it can survive.

For that, it must recover operational profitability in FY24 and generate enough profits to pay interest and, ideally, repay loans.

We have to start with the financing situation.

On its 4Q23 earnings pre-release, the company said it would end the quarter with $277 million in debts ($50 million on its term loan, $230 million on its credit facility, at about SOFR + 2.5%).

After the quarter, we announced the Mithaq loan ($78 million, interest-free) and the Gordon Brothers loan ($130 million, SOFR + 9%).

The original term loan will be repaid with the proceeds from the Gordon Brothers loan. The lenders probably requested this, as it is obviously not convenient for the company to replace SOFR + 2.5% debt with SOFR + 9% debt.

Further, the credit facility will probably be refinanced, I would believe, conservatively, at SOFR + 5/6%. If the riskiest lender (Gordon, unsecured) obtained SOFR + 9%, the credit facility is negotiated in better conditions and is asset-backed. Further, the current debt level reflects the inventory-low end of 4Q. The yearly average probably requires PLCE to draw $350 million.

I believe the company will only use the GB loan as a bridge because of its high-interest cost. It will probably get repaid with Mithaq's interest-free loan plus the proceeds from the rights offering and subsequent share issuance.

Still, if we consider $350 million at SOFR + 5.5% (10.5%) from the credit facility, plus $130 million at SOFR + 9% (14%) from the term loan, we arrive at $55 million in yearly interest costs. This is the worst scenario, where no money lent by Mithaq or raised via rights is used to repay debt.

A better scenario is one where the money raised from shareholders plus Mithaq is used to repay the most expensive loan. In that case, the credit facility still runs at $350 million and 10.5%, or $37 million annually.

These are the first hurdle rates the company has to cross to stay in the game, either $37 or $55 million in operating profits to pay interest.

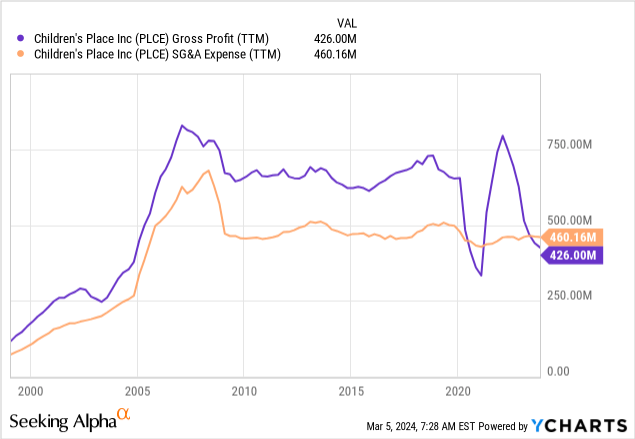

PLCE currently records $460 million in TTM SG&A expenses. We need to add $120 million in rent expenses, which are currently included in CoGS. These are the company's fixed expenses, amounting to $580 million. Add between $40 and $55 million in interest to reach a minimum gross profitability ex-rent of $620/630 million. Can the company pull this off?

Well, if we go back to almost any time before FY23, the company was able to produce these numbers. This is even true of the already bad FY22, which closed with contribution profits (gross ex-rent) of more than $650 million.

In my opinion, the way to do this is by raising effective prices, or alternatively, lowering or eliminating the promotions. The balance is between losing sales and each sale contributing more to margins.

We can start with the best scenario: no volumes lost, but total prices charged. This happened in FY21. The contribution profits were almost $1 billion for $1.9 billion in sales or a 52% contribution margin. Today, the contribution margin is at its historic lowest 35% ($560 million over $1.6 billion in revenues).

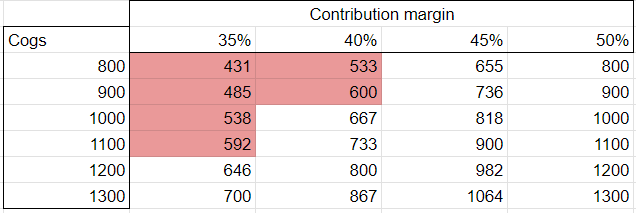

The table below plays with these contribution margins and different volume sale scenarios represented by CoGS. If CoGS goes down it is a bad sign, it means the company lost unit sales because of increasing prices. At the same time, it wins by making more money of the remaining sales.

The best scenario is margins going up and volume sales not decreasing, meaning that revenues go up; this is the bottom-right corner scenario. The worst scenario is keeping the margins as they are today, even if sales increase significantly (which is not happening). These are the red scenarios for 35% margins. There are some mixed but still negative scenarios where the company raises prices but sales fall (40/45% with $800/900 million CoGS).

Contribution profit based on CoGS (volume sales) and contribution margin (Own)

Still, by increasing the contribution margin to 45%, the company can sustain a 20% volume decline and still be more profitable than today.

In order to grow the contribution margin to 45% from the current 35%, effective retail prices (after the promotions) should go up 20%. This could very well lead to more than 20% volume sale losses, but I believe it will be temporary until customers get used to the fact that promotions are not as continued.

I believe an adjusted version of EV is necessary for a company with so much leverage that could potentially repay debts and increase equity. The current EV is not useful because debts have been announced but not included in the balance sheet yet.

Regarding the first topic, by 1Q24, debt should be around $500 million ($350 million credit facility, plus $130 million term loan, plus $78 million Mithaq loan, minus $50 million from the repaid old term loan).

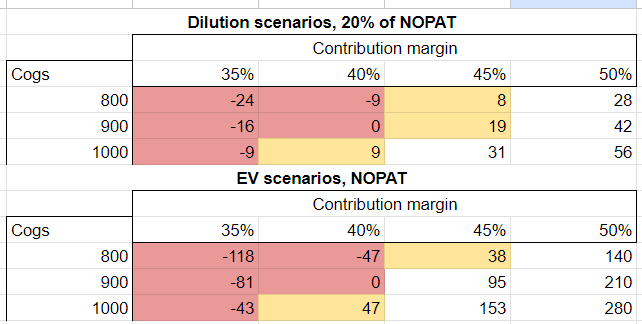

At current prices close to $18, the company must issue 27 million shares to repay all debts. That would triple its share count or dilute the current shareholders to 1/3 of their shareholding. The dilution would be even worse at lower prices necessary to entice so many funds. For example, at $12, 41 million shares are needed, or diluting current shareholders to 20% of the company.

Considering the $12 issuance scenario, today's investor pays a $230 million market cap for a 20% stake in the after-dilution company's NOPAT. That 20% of NOPAT (assuming 30% income taxes) is calculated below for each scenario above. We also consider the valuation from EV without dilution, therefore full NOPAT.

No interest is paid in these scenarios, as debt is equitized (first case with dilution) or included as capital (second case with EV). The scenarios in yellow are those where the company breaks even, but the returns to the capital base (diluted shareholder or EV) are below a 10% earnings yield.

The scenarios of growing sales were removed to focus on the likely scenarios of growing margins and falling sales

PLCE's return scenarios (Own)

The returns look very enticing if the company can raise its contribution margin and lose volume sales, but not too many. Further, this exercise is a single period, considering, for example, FY24, where prices are raised and sales fall, but there is no recovery into 2025 and beyond. Finally, in the first scenario, there is no liquidation risk for equity, as debt was equitized. The price used for dilution is relatively conservative (30% discount to current price).

These look like attractive returns to me. However, they rely on the company following a price increase policy, which is not defined, and some assumptions around sales not falling significantly more than 20% of volumes. I believe the company could still be on the brink of failure, wiping out most of its equity value in its current situation.

I believe for that reason, PLCE is not a conservative investment, in a concentrated portfolio. It could qualify for a speculative buy in a diversified portfolio. That is why my rating is a Hold and not a Buy. I believe a Buy can only be issued to companies where a concentrated, high-confidence investment can be made. Despite some promising signals, PLCE does not show those conditions because of its financially delicate situation.

However, I am excited about PLCE's prospects and will follow the managerial comments closely. If the stock drops further, especially after a refinancing, and new management plan is put in place, I would be very interested on the stock.