Tiffany Rose/Getty Images Entertainment

Tiffany Rose/Getty Images Entertainment

Dave & Buster's Entertainment, Inc. (NASDAQ:PLAY) is a leading American restaurant and entertainment business that operates a chain of entertainment and dining venues. The company's goal is to "be a customer's first choice for frequent fun through the best combination of the latest and greatest games, ultimate sports-viewing, extraordinary food, and remarkable drinks." The company is designed to appeal to a wide demographic, targeting families, young adults, and corporate events.

The company operates in the highly competitive restaurant and entertainment industry, facing challenges from changing consumer preferences, economic conditions, and evolving trends in leisure activities.

As such, Dave & Buster's faced significant challenges during the COVID-19 pandemic with temporary closures and capacity restrictions. Despite the challenges, Dave & Buster’s was able to tread water and now post-pandemic has had impressive growth.

This report looks at analyzing Dave & Buster’s turnaround story, fueled in large part by new management decisions, unique market position, and improved operational efficiencies. Based on these factors, along with projected cash flows, I have given a “Buy” rating to Dave & Buster’s stock.

Dave & Buster's occupies a unique position in the market by offering a comprehensive entertainment experience that combines dining, sports, and arcade gaming under one roof. This differentiation sets it apart from traditional dining establishments and standalone entertainment venues, potentially attracting a diverse customer base.

As of mid-2023, Dave & Buster's had a 90% brand recognition awareness among consumers. The company's strong brand recognition and the loyalty of its customer base contribute to its competitive advantage. Building on this foundation, Dave & Buster's can explore additional avenues for customer retention and expansion.

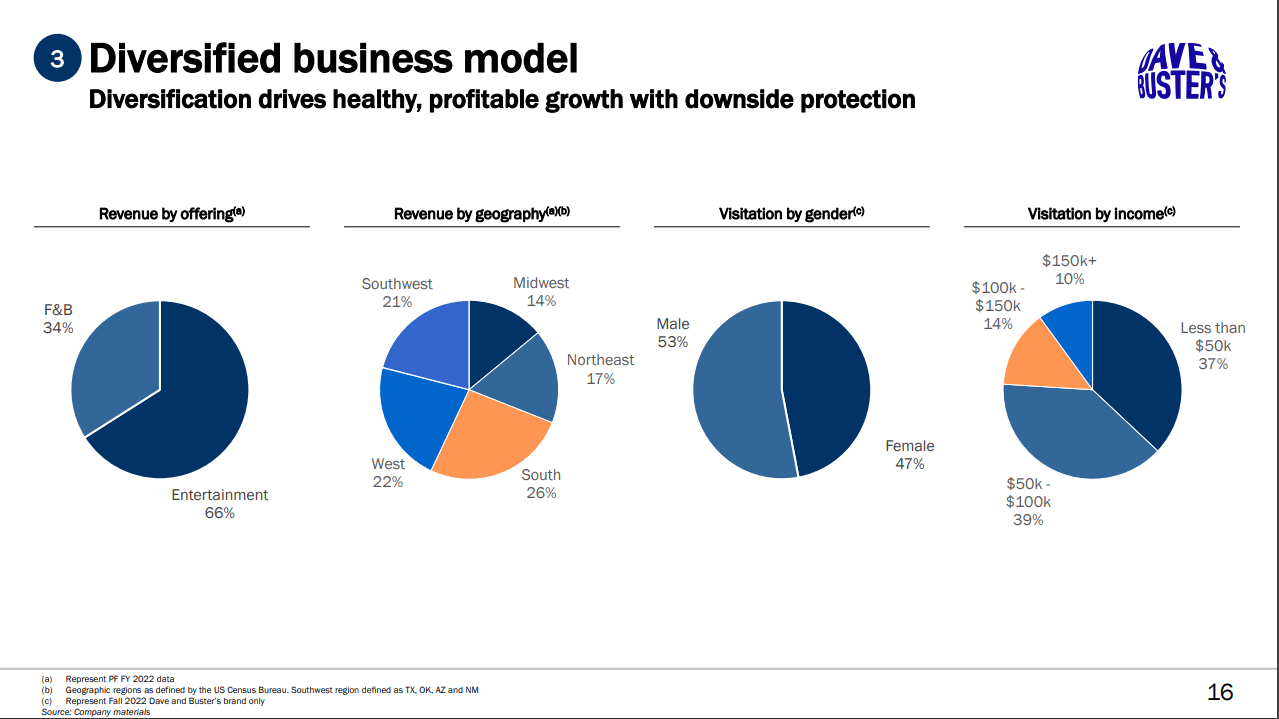

Due to this unique market position and brand recognition, Dave & Buster's is able to generate revenue through a combination of food and beverage sales, game sales, and private event bookings. The interconnectedness of these revenue streams helps create a diversified income model, reducing dependence on any single source but still behaving in a predictable, projectible way.

2023 PLAY Investor Day

Dave & Buster's also does an effective job at entertaining at a budget, with ~76% of visitors making less than $100,000 a year.

In June, Dave & Buster’s announced the acquisition of Main Event, a bowling, virtual reality, and laser tag company, from Coast Entertainment Holdings Limited. (ASX:CEH) In a subsequent move, they announced that the former CEO of Main Event, Chris Morris, would be the CEO of Dave & Buster’s. The CMO, COO, and CIO all similarly came over from Main Event.

With the Main Event acquisition and recent store developments, Dave & Buster's now operates 216 stores as of December 2023.

ScrapeHero

Dave & Buster's primarily operates in high-population dense areas in the states above. Management commentary has stated plans to achieve 252 by the end of 2025 with the long-term potential of 550+ stores. I feel this is too bullish of a projection unless Dave & Buster's were to show aggressive action toward this goal. In 2023, they opened 16 stores. For my bullish valuation, I applied a growth rate of 15 stores per year until 2030 resulting in a terminal value of 321 stores.

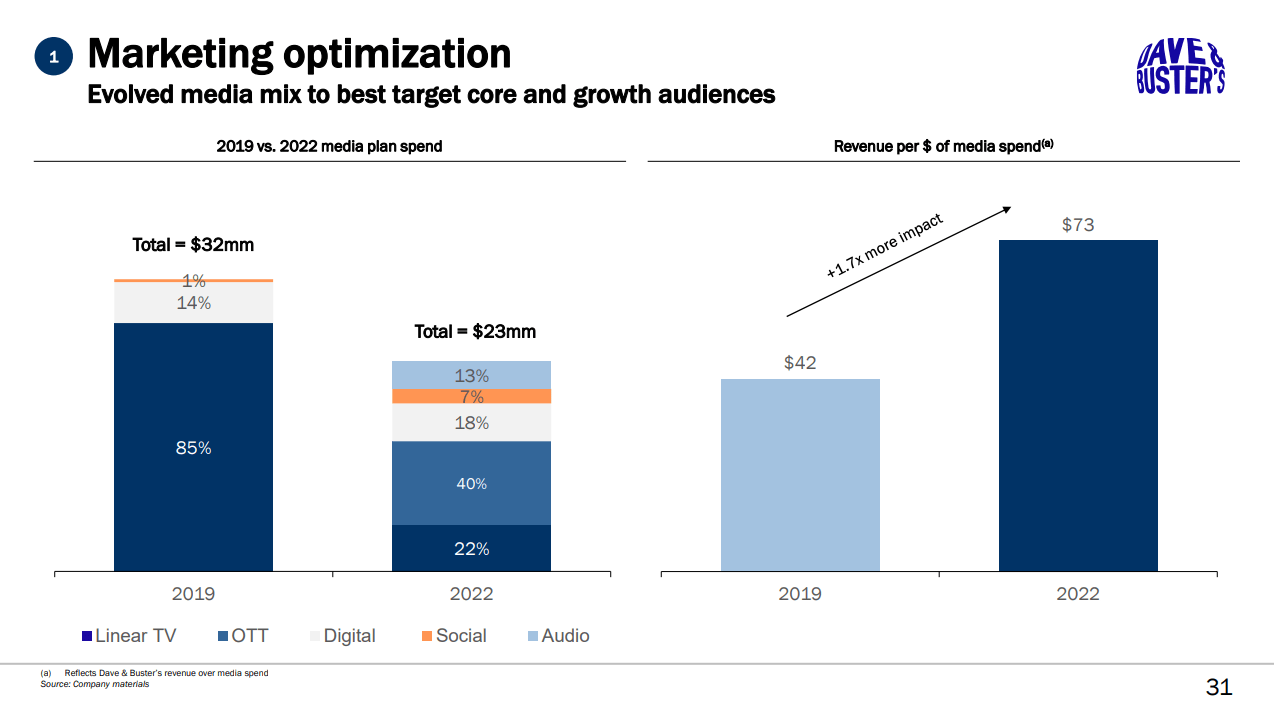

When new management took over its primary focus was marketing optimization for the brand.

2023 PLAY Investor Day

Previous marketing channels were more expensive and less impactful for their target demographic.

"Boomers are the biggest audience watching linear broadcast TV, as adults 50+—the Boomer and Gen X generations—dominate linear TV viewing... Young adults, ages 18-34, are the generation that’s least likely to watch linear TV."

Cutting expenses in this marketing channel and increasing exposure to OTT, digital, and social channels should have long-term benefits in reaching Dave & Buster's younger target demographic.

In response to evolving consumer trends, Dave & Buster's has invested in digital initiatives to enhance the overall customer experience. This includes a new and improved mobile app that allows customers to explore the menu and track game credits.

The app not only facilitates interactions for customers but also opens avenues for targeted promotions, loyalty programs, and data-driven insights that can enhance the overall customer experience. Users of their loyalty program currently sit at 5.4 million.

They have also made deals with the UFC (Q1 2022) and Dallas Cowboys (Q3 2023) to enhance the audience's viewing experience in an attempt to popularize the sports bar aspect of their business.

Any re-imposition of restrictions or a slowdown in the economic recovery could negatively impact foot traffic, consumer confidence, and overall revenue for Dave & Buster's. While I see this as an unlikely scenario, it has to be addressed due to the severity it would have on Dave & Buster's.

Consumer behaviors may continue to evolve as a result of the pandemic, impacting preferences for in-person entertainment and dining experiences. Dave & Buster's must be aware of changing trends and adapt its offerings accordingly.

The restaurant and entertainment industry is highly competitive, with numerous alternatives for consumers. Increased competition from traditional dining establishments, entertainment venues, and emerging trends in experiential offerings may pose challenges for Dave & Buster's in attracting and retaining customers. Top competitors consist of Topgolf Callaway Brands (MODG), Six Flags Entertainment Corps (SIX), and Bowlero Corp. (BOWL).

The company's performance is closely tied to economic conditions, including disposable income, consumer spending, and employment levels. Economic downturns or uncertainties could result in reduced consumer discretionary spending, impacting Dave & Buster's revenue.

Dave & Buster's also has 1281.3m in long-term debt making the company quite levered. Its interest coverage ratio is currently 2.51 so if rates were to climb any higher this could be a further cause for concern.

There has been a strong rebound in consumer spending on entertainment and dining experiences. The recent positive trends in revenue suggest a gradual recovery trajectory, indicating the company's resilience.

The enforced restrictions during the pandemic created pent-up demand for out-of-home entertainment experiences. As consumers seek social interactions and leisure activities, Dave & Buster's is well-positioned to capitalize on this demand with their unique offerings.

2023 PLAY Investor Day

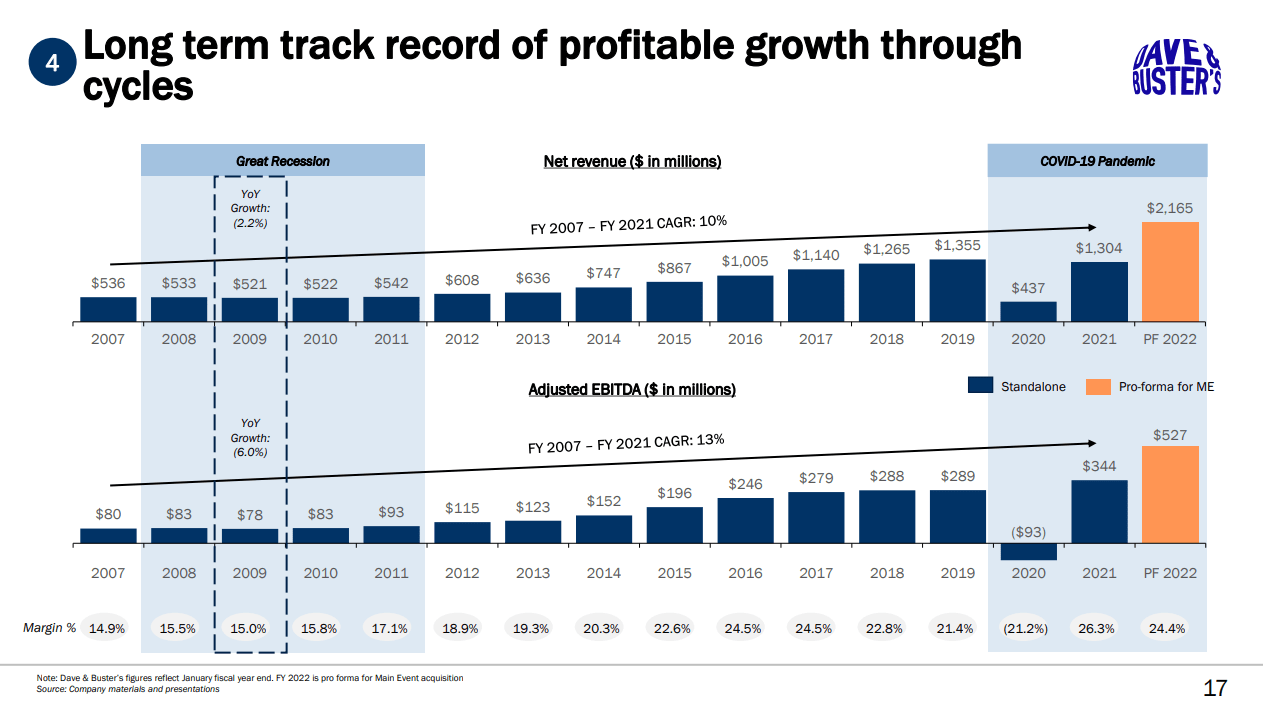

Dave & Buster's has shown strong revenue growth, improving year-over-year since 2007 except for distressed times in 2009 and during the economic shutdown in 2020. Their 10% CAGR over this period is impressive, however, the last 2 years with new management have shown even stronger promise for the company.

| Revenue (in millions) | YOY Growth | |

| Q1 2022 | 451.1 | 70.03% |

| Q2 2022 | 468.4 | 24.05% |

| Q3 2022 | 481.2 | 51.32% |

| Q4 2022 | 563.8 | 64.33% |

| 2022 Total | 1964.4 | 50.63% |

| Q1 2023 | 597.3 | 32.41% |

| Q2 2023 | 542.1 | 15.73% |

| Q3 2023 | 466.9 | (2.97%) |

| Q4 2023 (Est.) | 610.2 | 8.23% |

| 2023 Total (Est.) | 2216.5 | 12.83% |

Utilizing these values, since pre-pandemic levels in FY 2020 where revenue was 1354.7, Dave & Buster's has grown at a CAGR of:

13.19% FY 2020-FY2022 (1354.7-1964.4)

13.10% FY 2020-FY2023 (1354.7-2216.5)

Author's Note: When projecting free cash flow I created 3 scenarios: bearish, base, and bullish for projecting revenue growth into the year 2035. Depreciation + Amortization and Net Working Capital were calculated using historical % of sales rates of 9% and 1-2% (decreasing over time) respectively.

Historical values were also used for EBIT margins but were adjusted for the different scenarios with 14.75%, 14.6%, and 14.5% being used for the bullish, base, and bearish scenarios respectively.

A weighted average cost of capital of 7.982% and a terminal growth rate of 3.5% were used.

For the bullish projection, a revenue growth rate of 12.5% was used for the first 5 years. Annual growth is then lowered to 11% for the final 7 years. The CAPEX rate was raised to 14% of revenue for the first 3 years, 13% for the following 2, and lowered to 8% in the final 7 years. The increased CAPEX and revenue numbers are used to account for more locations being built in the upcoming years. Once this reaches maturity, the pace of revenue slows down along with the capital required to maintain these locations. Calculated fair value: $95.55.

In the base scenario, a revenue growth rate of 11% was used for the first 3 years before falling to 10%. CAPEX was 14% for the first 3 years before lowering to 8%. This trajectory follows a similar pattern as the bullish scenario but will occur if growth isn't as strong as expected, leading to fewer locations being built beyond 2025. Calculated fair value: $85.42.

The bearish scenario operates under the assumption that much of the recent growth experienced by the company can mainly be attributed to pent-up demand and that demand halting in a significant way. If management ends up not performing as expected, this is an unfortunate possibility. This scenario prices in revenue growth of 7% for the first two years as demand slows, before increasing to 10% to fall back in line with company trends. CAPEX is kept at a constant 12% throughout. Calculated fair value: $35.75.

Applying a 33% weighted probability to all of these outcomes, a fair value share price is calculated as follows: (.33*$95.55) + (.33*$85.42) + (.33*$35.75) for a fair value of $71.52.

Dave & Buster's has navigated through challenging times during the pandemic and has emerged with a strong recovery strategy. The company's unique market position, strong brand recognition, and diversified revenue streams have contributed to this and set it up for growth in the future.

The acquisition of Main Event and the infusion of new management, led by CEO Chris Morris, showcase strategic moves to enhance the company's offerings and market reach. Quickly expanding to 216 stores in 2023 and aiming for further growth to 252 by the end of 2025 demonstrates ambitious plans.

The shift in marketing focus to digital channels, the introduction of a revamped mobile app, and strategic partnerships with the UFC and the Dallas Cowboys underline the company's commitment to adapting to evolving consumer trends and enhancing the overall customer experience.

Revenue growth showcases promising figures, with a strong performance in recent years. The bullish, base, and bearish scenarios provide a comprehensive valuation perspective, yielding a fair value estimate of $71.52 per share when applying an equal probability weighted to the three outcomes.