Future Publishing/Future Publishing via Getty Images

Future Publishing/Future Publishing via Getty Images

Photronics (NASDAQ:PLAB) recently reported Q1 ´24 results, which disappointed investors by missing on EPS and revenue, while providing soft guidance. The stock plummeted on the day, so I wanted to take a look at how the company performed since I last covered the company back in August. PLAB has performed relatively decent over the last year, so in my opinion, the overreaction to the results is a blessing for people who are looking to start a position at prices not seen since August of last year, as the long thesis is still intact. The company is performing well and should recover and reward patient shareholders over the next 3-5 years; therefore, I am reiterating a buy.

As of Q1 ´24, the company had around $521m in cash and equivalents, against just $2m in debt. Like many semiconductor companies I covered, the financial health is immaculate. No debt means the cash flow can be utilized to further the company's growth, which will reward shareholders in the long run. Furthermore, the debt went down by $15m since Q4 ’23; even then, it was an insignificant amount. If that debt stays on their books forever, it wouldn’t be an issue for me. It’s safe to say the company is still at no risk of insolvency and should weather any further downturns in the semiconductor industry and macroeconomy overall.

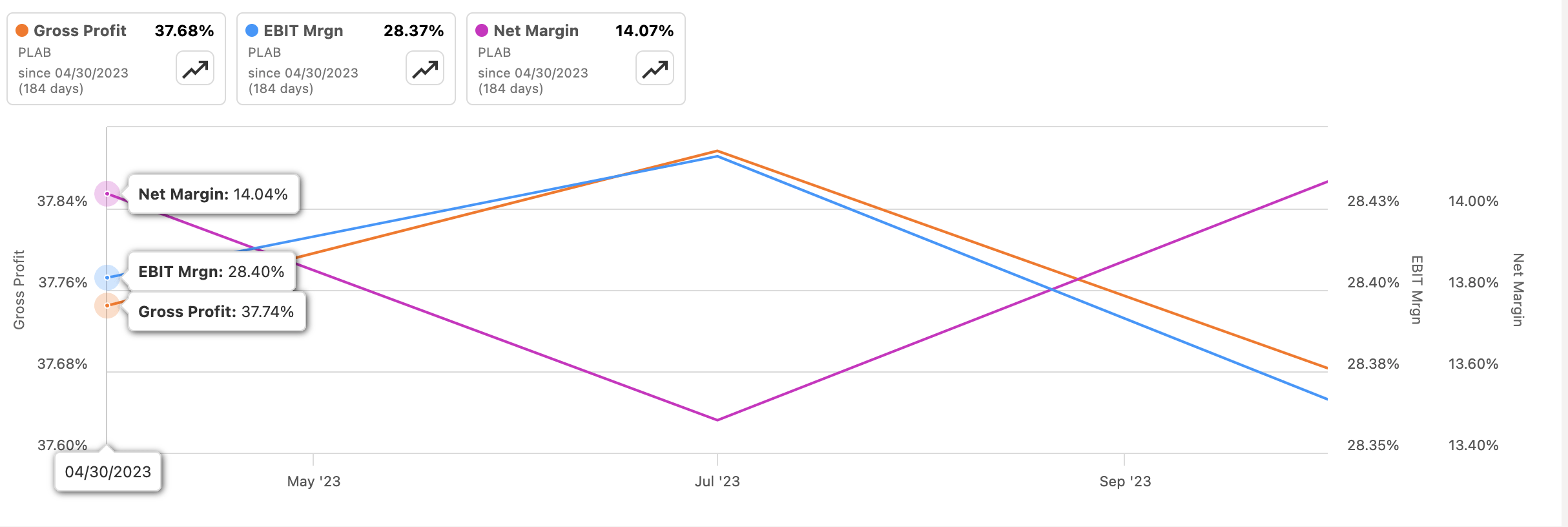

Let’s see how the company’s efficiency and profitability progressed through the end of FY23. PLAB’s margins have been relatively stable over the last year, even though it may look like they have fluctuated quite a bit, but these fluctuations were a few percentage points. Comparing the end of the year margins to the latest quarter of gross margins of 36.6%, and EBIT margins of 26.6%, while net margins stood at around 18%, we can see that gross and EBIT margins saw a little decline, while net margins are a little higher. Q4 margins were much higher than the latest quarter, but that is understandable, as the management said the first quarters are always worse than Q4s.

Margins (SA)

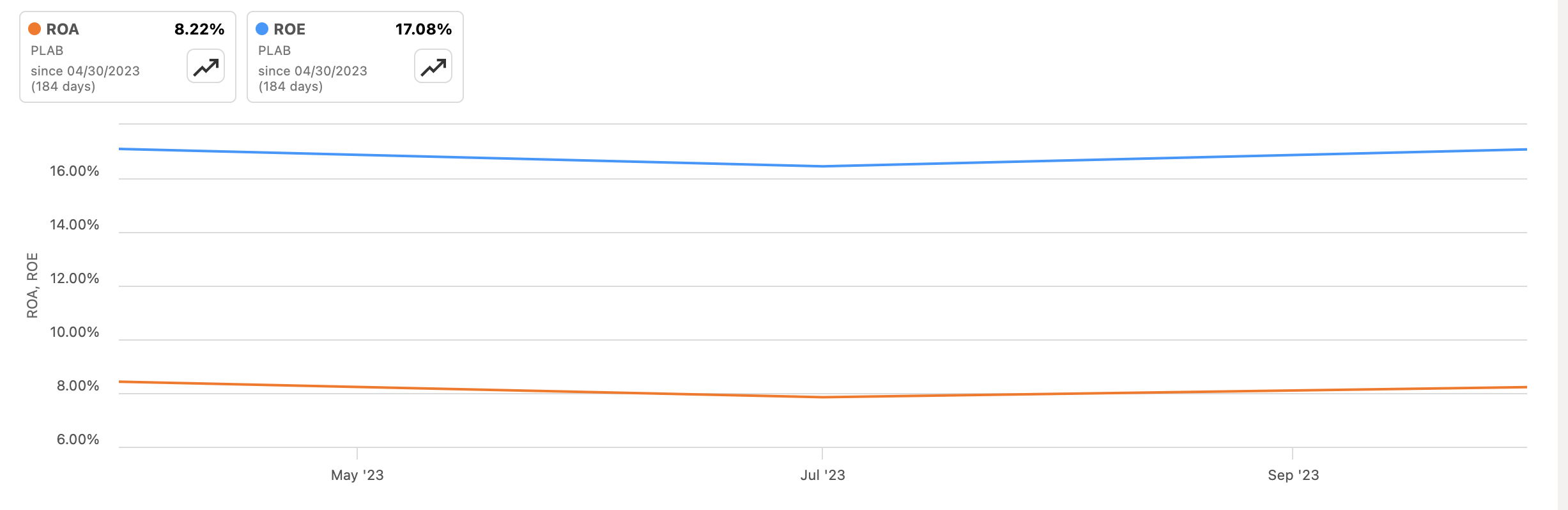

The company’s ROA and ROE have been relatively stable over the last year, which is not a bad thing, considering how high these are. The company continued to utilize its assets and shareholder capital rather efficiently and should have created value.

ROA and ROE (SA)

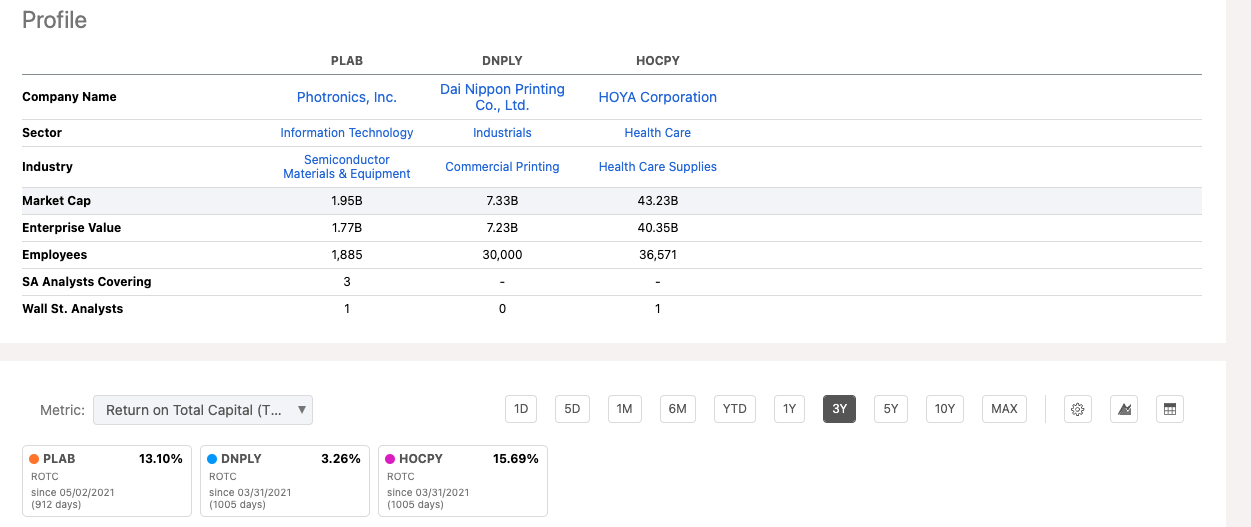

In terms of competitive landscape and advantage, it is hard to find any companies that would be publicly traded, but many companies in China, Taiwan, and Japan provide similar services and products as PLAB, so don’t consider the list of the peers I found to compare PLAB to exhaustive because it certainly isn’t. The company’s ROTC is still very decent in my opinion and is above my minimum of 10%. Furthermore, in terms of available competition, it is not fair since the companies below are much larger and do a lot in many different industries.

ROTC vs Peers (SA)

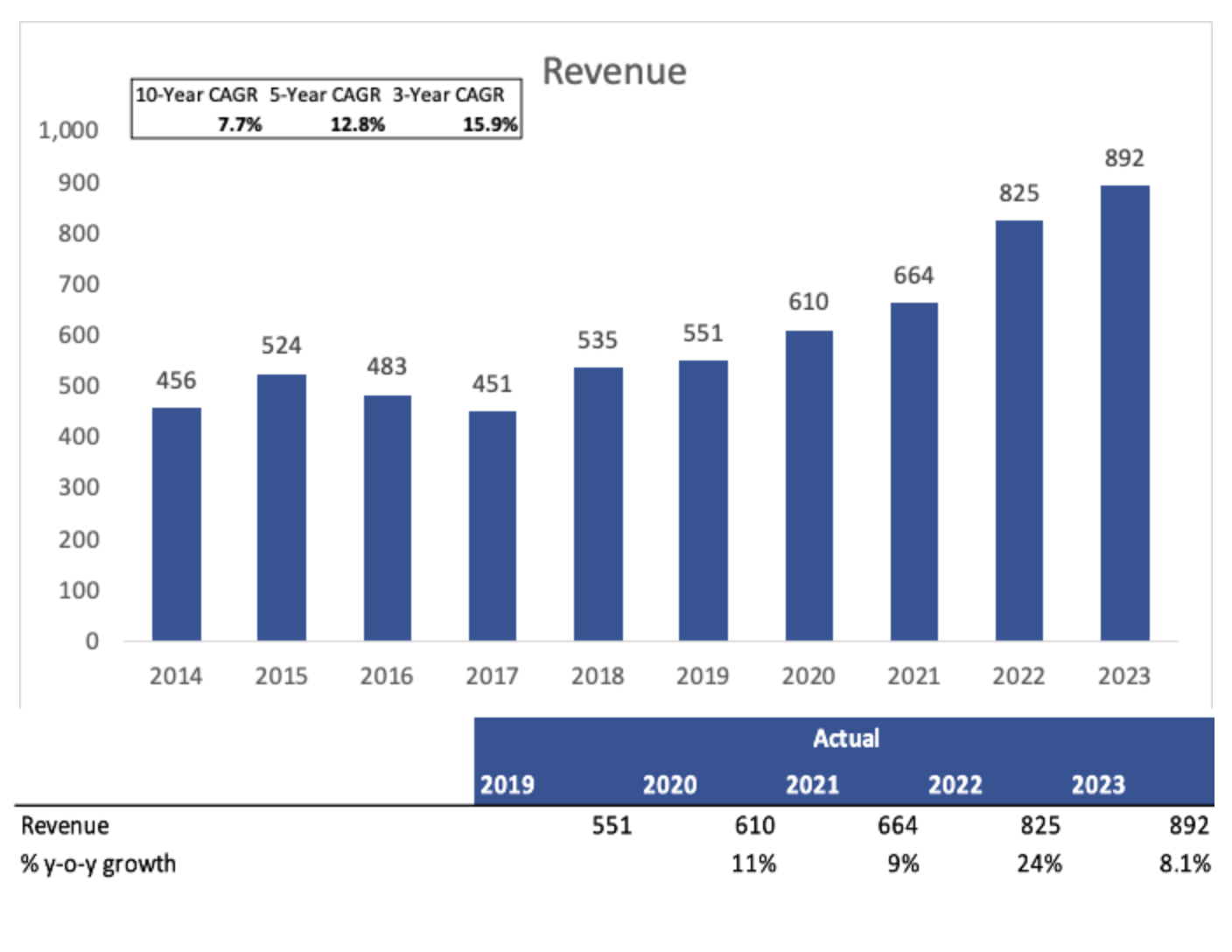

In terms of revenues, the company saw some growth, although not as robust as in previous years, but still is growing, even in the tough market that we experienced in 2023, regarding cyclicality. Furthermore, we can see growth accelerating in recent years in terms of CAGR, however, can that growth be sustained? Q1 ´24 saw a growth of barely 2.5% y/y, which is quite a slowdown. I usually don’t pay attention to quarterly reports too much because they tend to fluctuate, and I prefer seeing the full picture.

Revenue Growth (Author)

Overall, the company has been doing rather well over the past year, with margins keeping somewhat steady, as well as revenue. The company is just as efficient as it was at the beginning of last year, and revenues have been still growing, albeit at a little slower pace than before, but I think it is just temporary.

The company released its Q1 ’24 numbers, which missed on both counts, revenues and EPS. Revenue went up only 2.5% from the same time last year, missed by $3.67m, while non-GAAP EPS came in short, a cent at $0.48. IC revenues were up 1%, while FPD carried the top-line forward with an 8% y/y increase while being down 7% sequentially. These results are already not great, but I don’t think it warranted such a plummet in share price (down 14% as of writing the article). What I believe happened is the company’s guidance was poor. The company guided for Q2 ´24 EPS of a very wide range, $0.50 to $0.58 a share, which at the midpoint is $0.54 against analyst estimates of $0.56, and at the midpoint of revenues, which is $231m is higher by $1m than analyst consensus. So, what I think about this is that the market overreacted big time here. Sure, the misses are not great, but the guidance was not too bad in my opinion, and the results and guidance put together don’t justify wiping out 14% of the company’s value in one day. Quarterly reports are very volatile, as I mentioned earlier, and I believe this overreaction is a good opportunity to start a position for the long term or accumulate a full position if you are already invested.

I believe that the company’s long-term outlook is still intact, and I am treating this drop in share price as a good opportunity to start a position. The management is still sticking to the company’s 38% gross margins for the long run, which is a good sign that the team there can manage costs to keep delivering on efficiencies and higher profitability. The team is guiding for an improvement in margins from Q1.

I think the company will see a lot of success going forward in the AMOLED space. The demand for AMOLED is continuing to grow steadily and is projected to grow at a rather impressive growth of 11.85% CAGR from ’24 to ’31. This growth should translate into improving the company’s top-line growth, and CEO Frank Lee mentioned in the latest transcript that the company is looking to focus its attention on the AMOLED segment more going forward.

We all know the smartphone and the PC markets have seen softer years in 2022 and 2023 when the two markets saw a 12% and 15% decline, respectively in 2022, while the smartphone market projected a decline of 5% in ’23 while the PC market was relatively stable. When these two markets start to exhibit growth, I would expect the company’s revenues to pick up, and seeing that the declines are not as bad as they were, the bottom might have set in, and cautious optimism is warranted.

Overall, the semiconductor outlook is also positive. The negative sentiment and cyclicality are shifting to a positive territory and analysts are expecting growth to return, with projections ranging from 9% to a whopping 20% in 2024 and beyond. The need for semiconductors in the long run remains the same. There will not be a year when semiconductors are not needed due to ongoing technological advancements, digitization, and more and more devices becoming connected. Additionally, the company hasn’t even mentioned the buzzword AI yet! I jest, of course, the company doesn’t need to jump on that bandwagon.

For the valuation model, I looked back at my previous assumptions, which were already on the conservative end, and decided to be even more conservative this time around. This way, I can beat down the company’s outlook even more, which will act as a stress test to how low can the company go and still be a good buy. The first time around, I went with an 8% CAGR for the base case, now I decided to lower it to around 6% CAGR over the next decade, while the optimistic case will be the base case from the first article. Furthermore, a conservative case is really conservative in my opinion. Below are those assumptions.

Revenue Assumptions (Author)

On margins and EPS, I decided to decrease gross margins by around 400bps yet again, while decreasing EBIT margins by around 900bps from FY23. These will gradually improve to close to FY23 numbers, while net margins will see a 600bps improvement over the next decade. Below are those estimates as compared to FY23.

Margins and EPS Assumptions (Author)

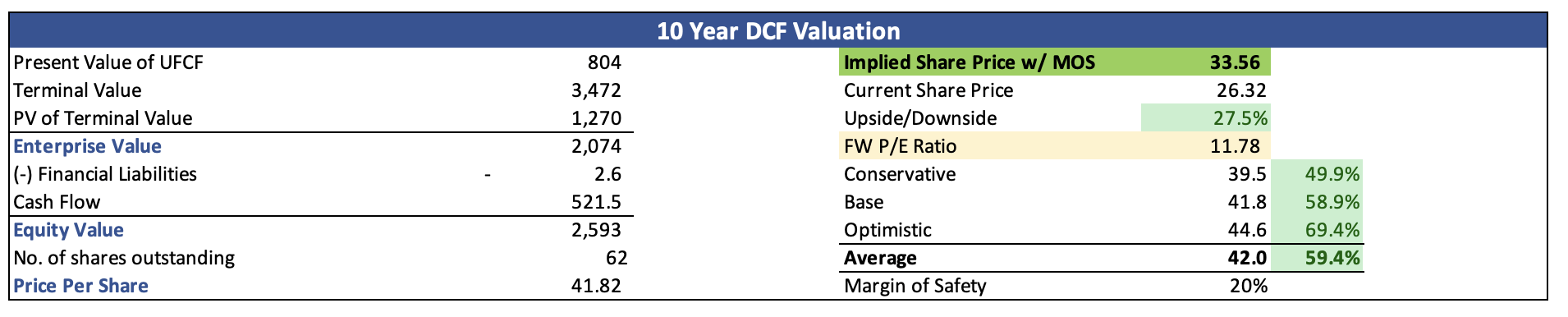

For the DCF model, I went with the company’s WACC of 10.6% as my discount rate and a 2.5% terminal growth rate. Furthermore, I added another 20% discount to the final calculation just to give myself even more room for error in the estimates above. With that said, PLAB’s intrinsic value is $33.56 a share, meaning that even after such conservative estimates, the company is trading at a discount to its fair value, and the recent plummet in share price presents a good opportunity.

Intrinsic Value (Author)

The same risks remain as I mentioned in my first article. A lot of the company’s revenues come from China and Taiwan, which, as we all know, are geopolitical risks that no one wants to touch right now. I do think this risk is overstated, and I doubt there will be anything happening any time soon. The company’s revenues are safe in my opinion.

The softening in the main end markets may continue to deteriorate the company’s top-line growth potential, which will affect the company’s share price further as we saw in the latest report, however, cycles end and the company will see its top-line growth rejuvenate. Maybe not in the next couple of quarters, but in the long run for sure. I prefer to look at this from the long-term perspective, and such short-term issues will present a good buying opportunity.

I believe the company’s problems will be short-lived, and such large pullbacks should be viewed as good entry points to start or accumulate a full position in a company that in my opinion will be around for a while longer. The company’s immaculate balance sheet will protect it from any further downturns in the economy and its specific industry hiccups, but considering the worst is behind, the downside risk right now is minimal, and only an irrational market sentiment may pull the stock further down, which has nothing to do with the company’s fundamentals. These remain solid; therefore, I am sticking with my buy rating from the previous time, and if the company’s share price continues to go down while the bullish thesis remains intact, I may have to upgrade my rating in the future and make it a full position.