Tippapatt

Tippapatt

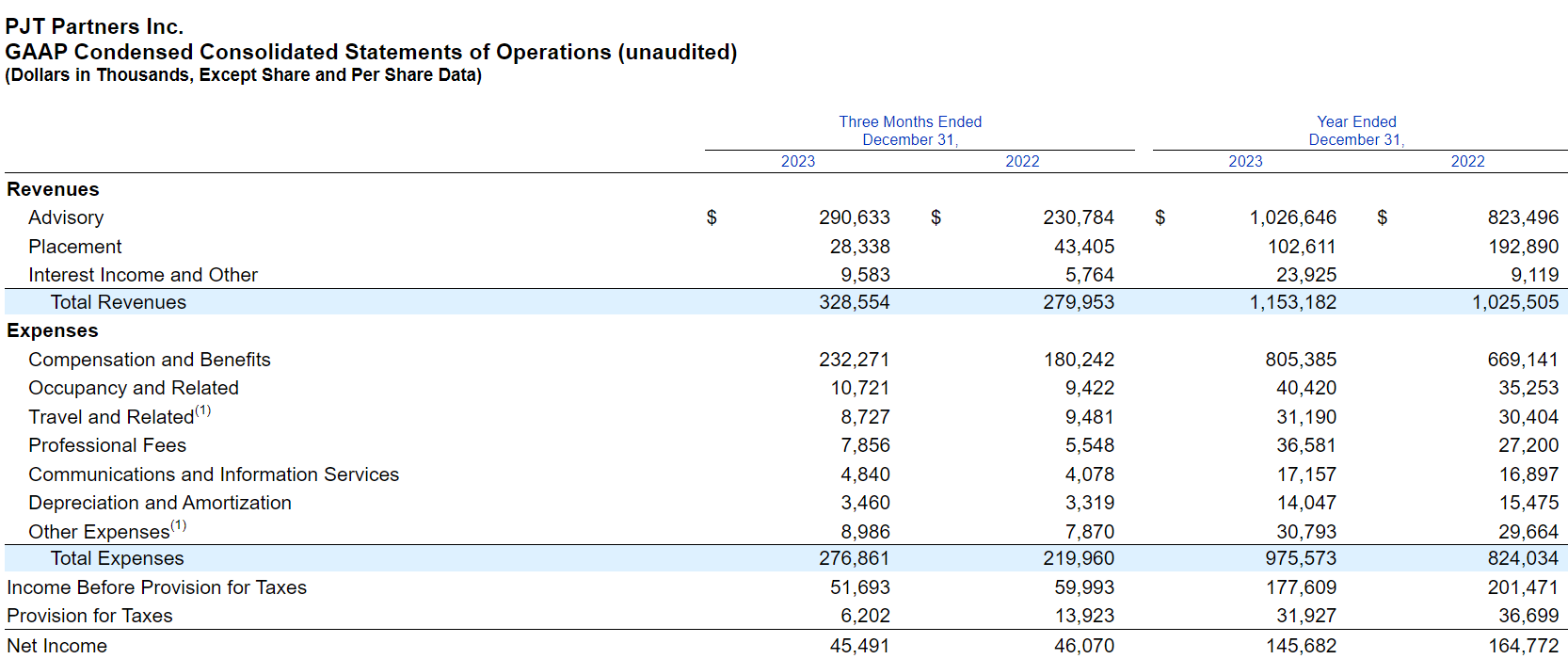

PJT Partners (NYSE:PJT) is a useful touchstone in the coverage of boutiques since it always seems to be the one that is going to be leading on restructuring activity, which is a must-ask question at every advisory earnings call. While we are seeing some liability management engagements pick up at other banks, PJT is getting that as well as more major in-court restructurings going, and it is driving overall growth. We think that strength in that business is long overdue. EPS is also compressed still due to headcount additions. When they become more productive in general M&A, PJT will start to grow into its currently pretty steep valuation since the run-up. Nonetheless, management feels that they can do a 10% buyback accretively. We might pass on PJT, since we're not that optimistic about their M&A and placements business, but we do respect their performance.

There is no doubt PJT is doing really well.

IS (PJT PR)

Other companies like Moelis (MC) are also posting good quarters with jumps in restructuring revenues. But PJT has done well throughout the year on its leading restructuring franchise.

Dynamics that are important are that of course there are higher rates, and also the maturity walls start in 2024 and include 2025. Major refinancings are going to happen, which creates activity in liability management, which is sort of the first resort in restructuring activity that typically leads more laborious mandates. What makes PJT a little different is just how pronounced the activity is in in-court restructurings as well, and how much more consistent their results have been since the beginning of the year driven by the restructuring franchise, where others have at best only had restructuring pickups in the Q3, not sooner.

They also have an M&A business within advisory, which isn't broken out specifically, but we know has generally a smaller representation in the mix than a typical shop. That apparently has run for the most part flat YoY, which isn't saying much considering that 2022 was a weak year for general M&A.

They added a lot of people in the high ranks of the company this year as well, 20% increases in MD headcounts and 12% increases overall, which weighed meaningfully on the income figures as a consequence of those elevated comp ratios. It typically takes some time for new MD hires to become fully productive, so we wait for a possible J-curve in income, which remains flat YoY despite the strong sales growth on a 3m basis.

Park Hill, which is the placement business, is really not doing well owing to the very low level of sponsor activity on markets. On a year-end basis, the figures are down almost 50% in sales. It's not that much better on a 3m basis either. There are a myriad of reasons for this. Inability to use the IPO markets clogs the pipeline. Inability to exit means inability to service redemptions and raise new capital. Uncertainty around exit opportunities makes allocators more reticent to place capital, since it's unsure when and to what extent they can make a return, also because the rate outlook is still very uncertain for sophisticated and leveraged investors. Higher for longer will make these issues persist until a real end to inflation and the policy situation is visible.

Park Hill is likely to continue to have issues. Sponsors can't act yet, and we think that higher for longer is inevitable. That's not great for M&A either, which should recover from abysmal levels but will do so slowly, and will not come roaring back, which has been the opinion of a lot of advisory shops but not all.

We are pretty confident about PJT and restructuring, whose strength has been long overdue. We think that the maturity wall situation is definitely going to create business. A higher for longer environment will only create more need for restructuring. Disruption of all kinds, including from AI, may also create unexpected avenues for business. However, we do see things possibly freezing up around election cycles because of the geopolitical and supply chain considerations. The can will be kicked down the road in the summer 2024, at least outside of necessary liability management which should be strong given the timings of maturities.

More than happy to revisit it. But as I've said, that here's the paradox of the business. When M&A is going gangbusters and it's easiest financially to absorb new investment, it's hardest to attract the new investment. When M&A markets are dislocated and it's the worst possible time to absorb that investment into your P&L, is when you get the best opportunities to build the franchise.

Paul Taubman, CEO of PJT

A lot of the headcount additions were actually in M&A. They're not productive yet, and probably they will stay that way for some time. This will probably limit how quickly net incomes will be restored. Management is doing a ~10% buyback program since they probably have some faith in further price growth as earnings grow too, but we feel that at current PEs of around 25x on a forward basis, boost in new MD productivity is likely to be a means to grow into valuations.

M&A weakness persisting and a pretty disruptive and likely close 2024 US election could harangue the realisation of major productivity gains on recent human capital investments. That's not great considering that the valuation is quite stretched and seems to depend on it. 25x PE is a 4% forward earnings yield, which is not great against risk free rates. TTM levels are around 32x. The growth from recovery looks quite assumed. We think PJT should deliver, they're a great company, but we're not compelled at current prices as sponsor activity is not getting better in our view anytime soon, and neither is M&A.