InspirationGP/iStock via Getty Images

InspirationGP/iStock via Getty Images

In our view, The Simplify Health Care ETF (NYSEARCA:PINK) offers investors a compelling opportunity to invest with purpose. PINK seeks to provide long-term capital appreciation by investing in groundbreaking and innovative companies across the health care sector, including biotech, medtech, gene therapy, and other fast-growing areas.

At the same time, PINK is the first 100% pro bono ETF focused on health care, with net profits donated to benefit the Susan G. Komen Foundation in its fight against breast cancer. With current assets at $131.7mm, at a 50 bps management fee, Simplify is donating more than $650k annually to support the Susan G. Komen Foundation, providing investors an opportunity to generate positive social impact while pursuing attractive investment returns.

Michael Taylor serves as lead portfolio manager of the ETF and brings over two decades of experience managing long/short health care equity portfolios at leading hedge funds. Before beginning his investment career, Taylor also spent time as a virologist focused on drug development.

Albeit over a very short time period, PINK has generated attractive absolute and relative returns since inception, outperforming both its benchmark (the MSCI USA IMI Health Care Index) and the S&P 500 over the period. While we think the drivers of the fund’s returns have been fairly narrow, and we don’t love PINK’s relatively high exposure to biotech, we think Taylor’s pedigree coupled with the fund’s attractive valuation and orientation toward the “picks and shovels” businesses within health care position PINK nicely for continued success.

As such, we are currently holding a Buy rating on PINK.

PINK provides investors with a unique opportunity to align their investments with their values. As the first 100% pro bono ETF focused on the health care sector, PINK donates all net profits to support the Susan G. Komen Foundation's fight against breast cancer. In our view, the average impact investing strategy typically sacrifices performance in support of making a positive impact. However, because Simplify and Taylor are willing to run this fund pro bono, they’re able to parlay the success of the fund into generating a positive impact. We like this approach as it supports a good cause without sacrificing performance.

By investing in PINK, we think investors can support advancements in health care and cancer research via contributions to the Susan G. Komen Foundation, while pursuing attractive investment returns. We think this makes PINK a compelling option, particularly for purpose-driven investors looking to add health care exposure to their portfolios.

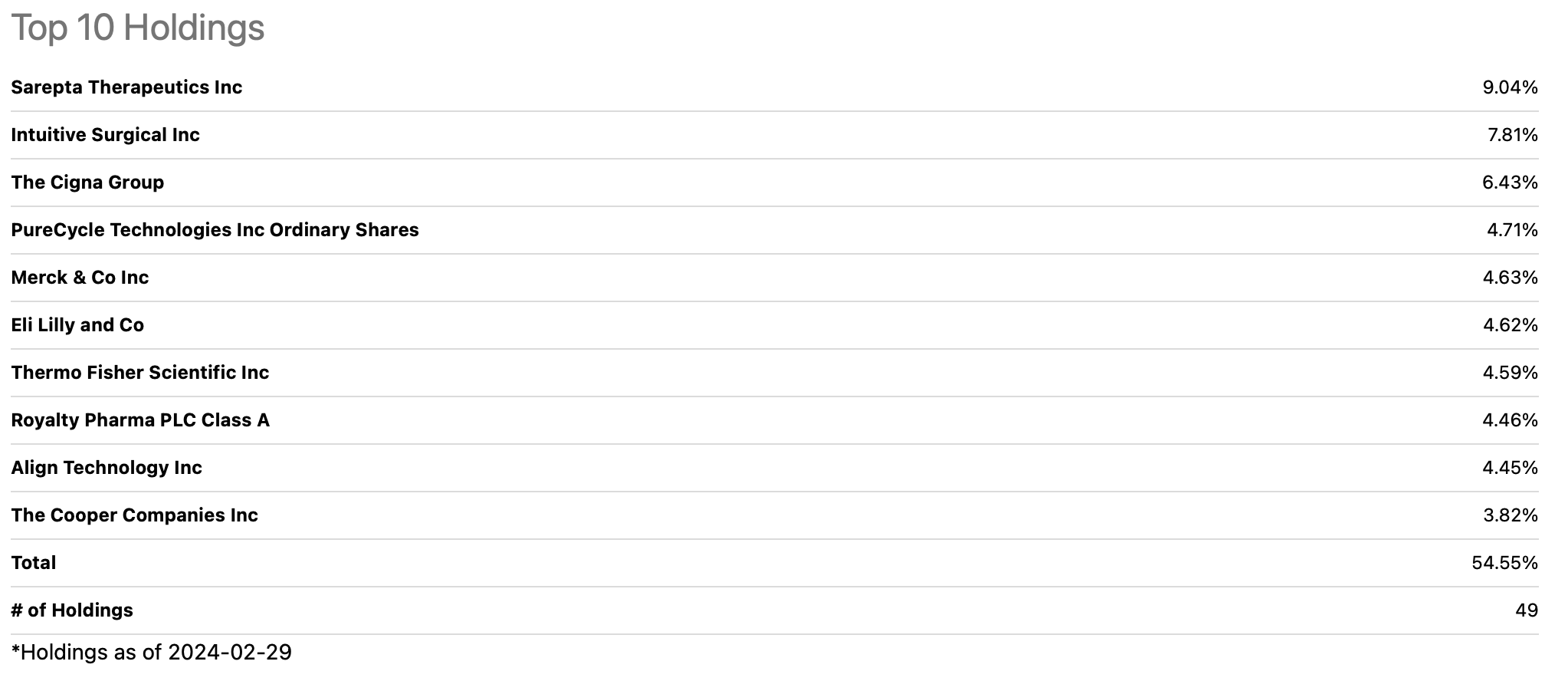

PINK takes a concentrated, actively managed approach to investing in health care. The fund typically holds 50 to 100 positions, with the top ten holdings often representing over 50% of assets. As of February 29, 2024, the fund held 49 positions with 50% of assets invested in the top ten holdings.

PINK's Top 10 Holdings (Seeking Alpha)

We believe PINK’s level of concentration (~50-100 stocks as opposed to 10-20 stocks) is appropriate given the fund's sector-specific focus and the experience of the portfolio manager. Moreover, we take confidence in PINK's research-driven investment process, which employs fundamental, bottom-up analysis to identify high-quality companies and compelling investment opportunities across the health care sector.

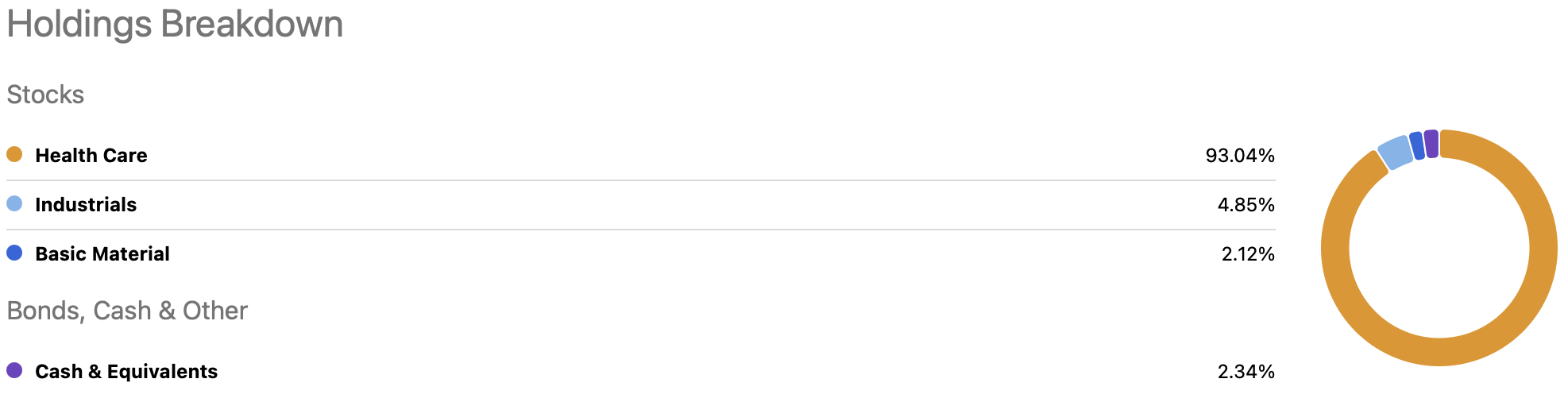

PINK's Sector Exposure (Seeking Alpha)

At the industry level, the fund’s largest exposure (37%) is within health care equipment and supplies. We view this exposure favorably, as we generally prefer greater exposure to the “picks and shovels” businesses (the companies that provide the goods, services or technology needed for an industry to produce a final product) which we believe involve significantly less binary risk than companies reliant on drug development.

That said, PINK’s second-largest industry exposure (20%) is to Biotech. In general, these companies are focused on drug development. In our view, the success of these businesses is highly dependent on the successful development and approval of new drugs – a capital intensive business model (high research and development costs) with a binary risk/reward profile. While we would typically prefer less exposure to these types of businesses within health care, we think this risk is partially mitigated by the portfolio manager’s background and expertise. As previously mentioned, prior to his career in investing, Michael Taylor was a virologist who worked in drug development, giving him a strong understanding of the scientific, regulatory and investment considerations involved with investing in drug development businesses.

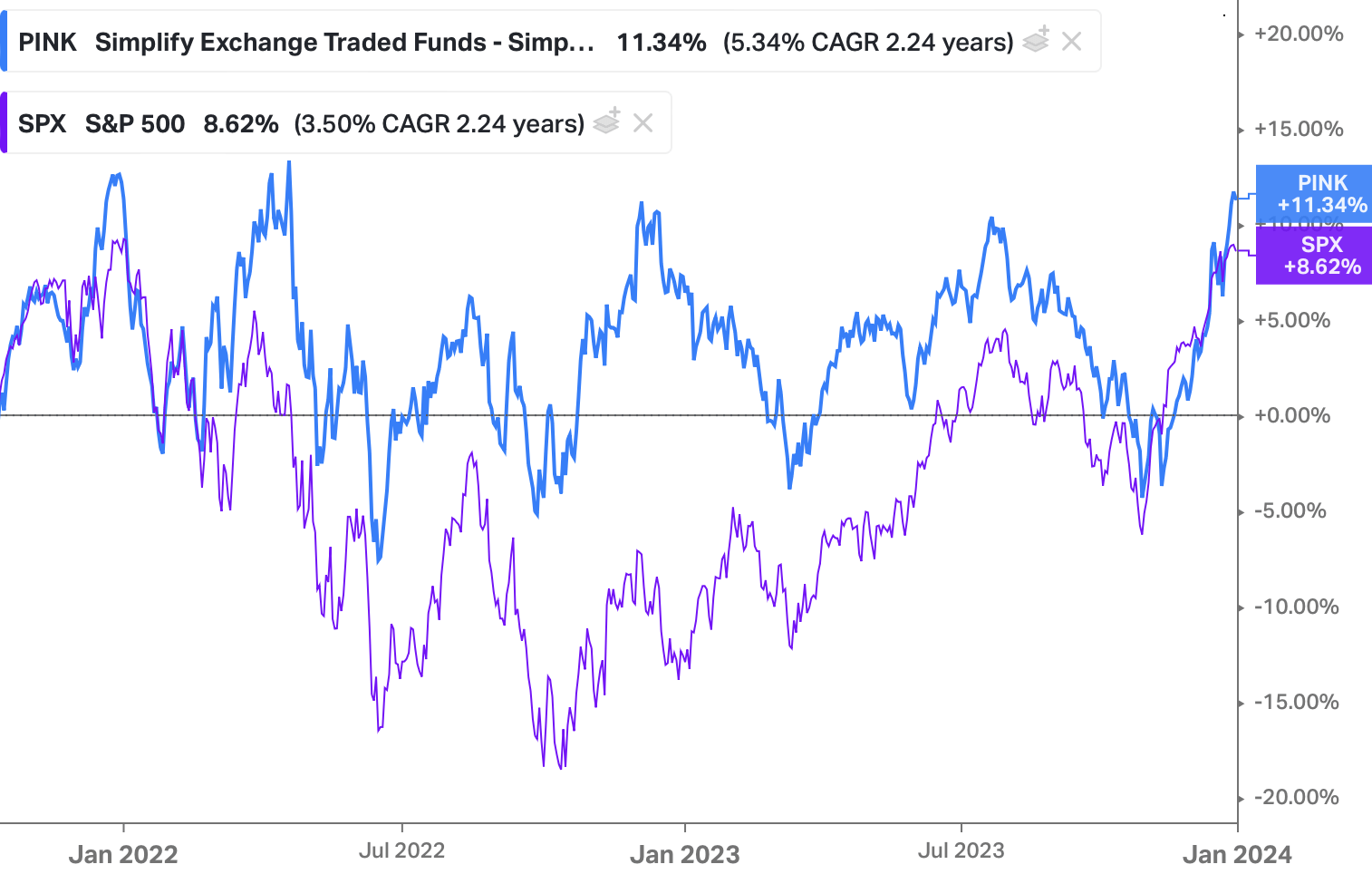

Since its October 2021 inception, PINK has delivered compelling absolute and relative performance. Since inception (through 12/31/23), PINK has generated a cumulative net return of +11.3% (+4.9% annualized), outperforming both the fund’s benchmark, the MSCI USA IMI Health Care Index, which returned +3.6% (+1.6% annualized) over the same period, as well as the S&P 500 which rose +8.4% (3.4% annualized) over the period.

PINK - Since Inception Returns vs. S&P 500 (as of 12/31/23) (Koyfin)

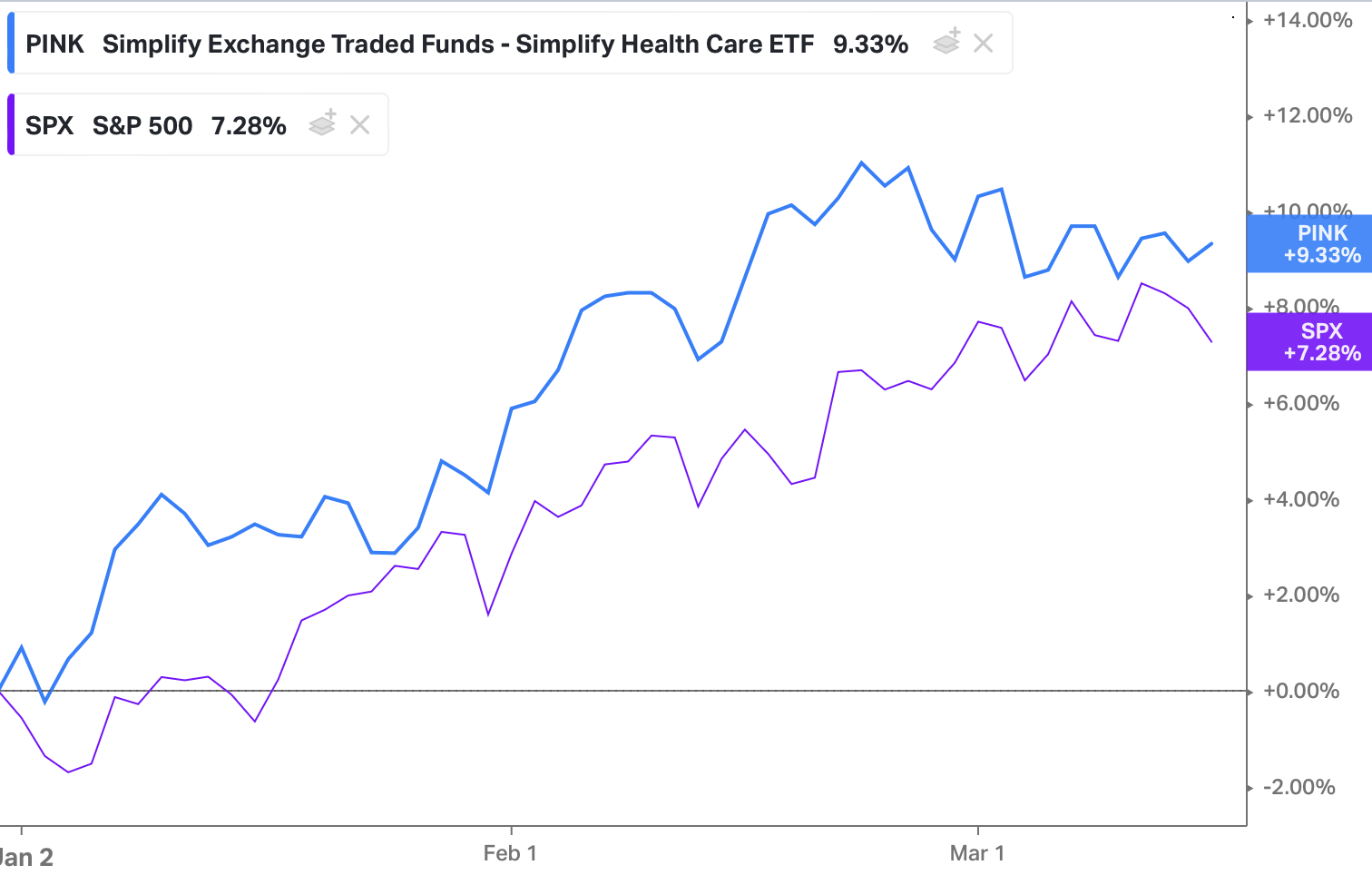

PINK's strong performance has continued into 2024. Year-to-date through 3/15/24, PINK has returned +9.3% versus +7.3% for the S&P 500.

PINK vs. S&P 500 - Year-to-Date Returns (as of 3/15/24) (Koyfin)

Notably, PINK has generated this outperformance despite trading at a discount to the broader market. As of March 15th, according to analysts' estimates, PINK had a forward price-to-sales ratio of 2.2x compared to 2.8x for the S&P 500.

While concentrated funds can have a few large drivers of returns relative to more diverse funds, over the last year, PINK’s performance has been largely driven by just four stocks – Intuitive Surgical Inc. (ISRG), Eli Lilly and Company (LLY), The Cigna Group (CI) and Fulcrum Therapeutics Inc. (FULC) – which have accounted for ~96% of the fund’s +24.9% return over the last year. It is possible that the fund’s breadth of return drivers increases over time, but this narrow breadth is almost “VC-like,” and raises questions about the sustainability of the fund’s outperformance.

In our view, PINK provides an attractive vehicle for investors to gain actively managed, concentrated exposure to innovators across the health care sector while directly supporting the fight against breast cancer. While the fund's "VC-like" return profile and biotech exposure present potential risks to the sustainability of the fund’s go-forward, long-term returns, we believe these risks are at least partially mitigated by the experience and expertise of lead portfolio manager Michael Taylor.

Taylor's experience, coupled with the fund's strong absolute and relative performance since inception, its attractive valuation, as well as its compelling "invest with purpose" angle and exposure to the "picks and shovels" of health care, lead us to maintain a Buy rating on PINK.