msderrick/iStock via Getty Images

msderrick/iStock via Getty Images

The March Madness brackets aren't out yet, but college basketball enthusiasts are already making their bets.

What could be the most exciting matchups?

Who will take it all?

And how about Cinderella stories that could emerge along the way?

While March Madness spectators naturally want to nail their brackets…

There's just something about underdog upsets that can get us cheering.

Psychology Today published a piece about this mindset in 2010. And while we're almost a decade and a half down the road from its findings, they remain interesting, including how:

… [University of South Florida associate professor of psychology Josepth] Vandello and colleagues explored the possible reasons why people are so attracted to underdogs. In one study, participants rated underdogs as higher in effort, and in turn, this was related to support for the underdog… Put differently, people liked underdogs more because they thought they worked harder.

The article concluded that "we like to back the team that has its back against the wall, not because we like backing losers, but because we like to see a team beat the odds."

Maybe it's because we, ourselves, so often feel like we're battling big forces.

We appreciate reminders that we have a chance of succeeding.

Of course, in March Madness, top-seated teams do end up going all the way more often than not. But if we turn our attention to the world of real estate investment trusts (REITs)?

Some small-cap companies can definitely provide reason to cheer.

Again, nothing is decided as of this writing. Selection Sunday is March 17. But speculation began over a month ago.

Some people even began posting about it back in January.

One of the more recent articles on the topic was from ClickOnDetroit on March 9. Titled "Why Oakland Basketball Could Be This Year's Cinderella Story in NCAA Tournament," it notes that:

Mid-major teams are usually looked over going into March, but Oakland has potential to make some noise.

It further details how:

Oakland University's men's basketball is on the verge of an extraordinary run. With just two more wins, they're on the brink of punching a ticket to the big dance.

As March grows older, the anticipation for the NCAA tournament continues to increase. While the Michigan Wolverines will miss the postseason for the second year in a row, and the Michigan State Spartans are projected to land close to the 7-line once again, there is another team in the southeast Michigan area that could be dancing in a couple of weeks' time.

For those of you who don't care about college basketball - or basketball at all - I won't keep quoting the piece. But it does go into great detail about its Cinderella story prediction.

And it could be right.

A few weeks prior (on February 20), Bleacher Report published its own piece: "Dangerous Teams With Most Cinderella Potential in 2024 Men's NCAA Tournament." It defines the concept as a team "projected no higher than a No. 12 seed."

In which case, it starts its official list with the Green Bay Phoenix, calling them "an incredible turnaround" story.

Also mentioned are the:

We'll see how they all fare soon enough!

As I always say, I can't predict the future. Not about college basketball. Not about the larger stock market or individual assets.

I guess I got distracted when they were handing out crystal balls. So if you know where I could buy one, let me know.

But I do know how to do hard-core research on REITs. I know what it takes to create them. I know how they operate.

That's why I have no problem acknowledging the obvious: that small-cap stocks come with more inherent risks than their bigger, more well-established peers.

At the same time, they come with more inherent growth potential.

So, it's a tradeoff.

Kinda like the thrill of seeing a Cinderella Story succeed vs. the disappointment of them failing.

Only, in this case, you have significant money on the line.

It's more than just a rush of anti-establishment "righteousness."

That's why I always stress doing your homework. (And not just about small-caps. The larger companies too.) I want to know:

And everything in between.

What I found from that questioning with the following three REITs is compelling. Again, no Cinderella Story is ever guaranteed.

But these look like they have solid starts I'm willing to put my money on.

SELF is an internally managed real estate investment trust ("REIT") that specializes in the ownership, redevelopment, acquisition, and operation of self-storage properties across the United States. The trust has a market cap of approximately $46.5 million, making it by far the smallest company we are looking at today.

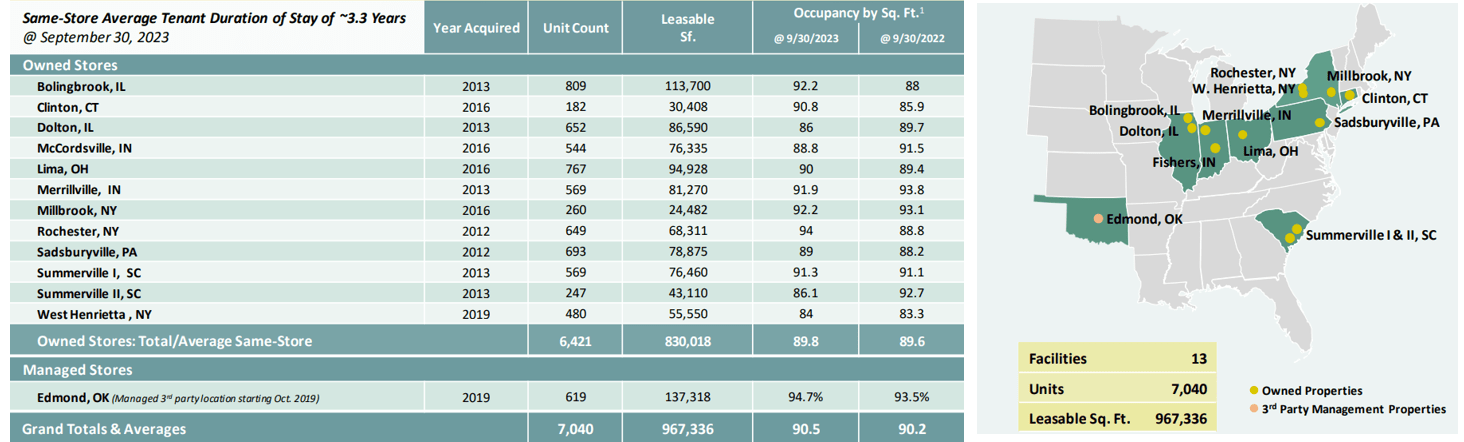

The company's portfolio consists of 13 self-storage properties totaling 967,336 sq. ft. that it either owns and/or manages. SELF has properties located in New York, Pennsylvania, Connecticut, Indiana, Illinois, Ohio, and South Carolina that in total contain more than 7,000 self-storage units.

It targets properties that are located in tertiary or secondary cities and its portfolio is largely concentrated in the Northeast, Mid-Atlantic and Midwest regions of the country.

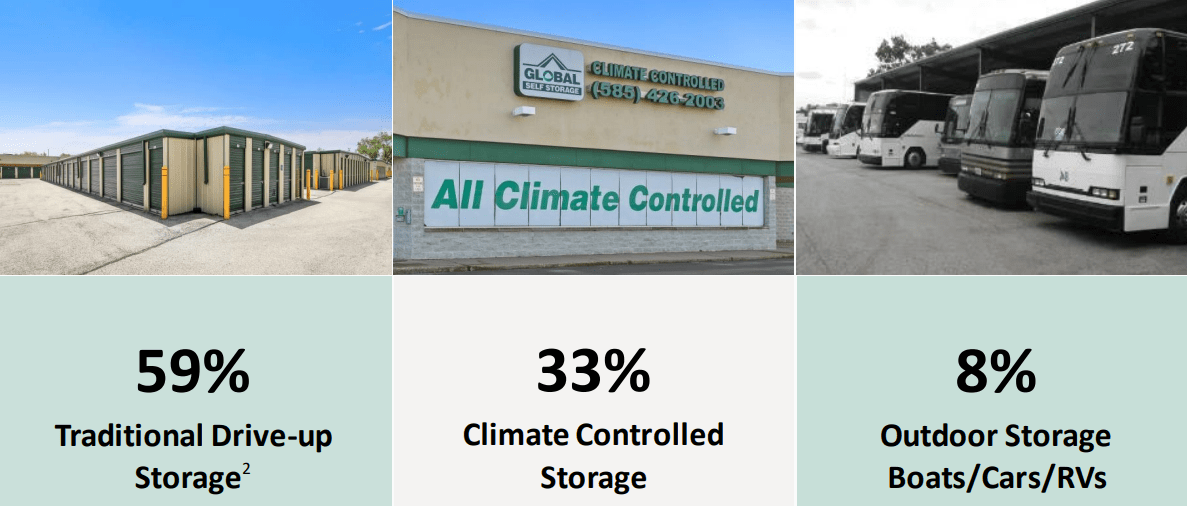

It leases space to both residential and commercial customers and offers multiple types of units including personal & business storage, climate controlled storage, and storage for boats, cars, and recreational vehicles.

As of the end of the third quarter in 2023 the company reported a portfolio occupancy of 90.5%, and same-store average tenant stay of roughly 3.3 years.

SELF IR

As of its most recent update, 59% of its properties are traditional storage, 33% are climate controlled, and 8% of its properties are outdoor storage designed for large vehicles and vessels.

Its properties offer secure, clean, and easily accessible facilities with modern amenities such as 24/7 security monitoring, touchpad gate entry, customer service call centers, and self-service kiosks to make rentals and payments more convenient.

SELF IR

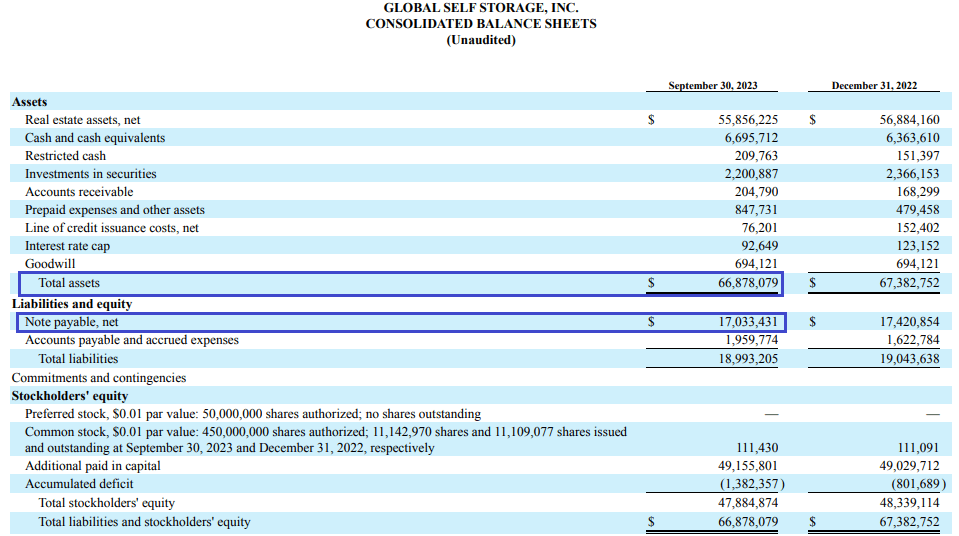

The company's balance sheet is in great shape with $66.9 million in assets compared to approximately $17.0 million of debt, for a debt to asset ratio of 25.47%. Similarly, its long-term debt to capital ratio stands at just 26.07%.

The company has a net debt to EBITDA ratio of 2.09x and an EBITDA to interest expense ratio of 5.95x and as of 3Q-23 it reported total capital resources of $24.1 million, consisting of almost $7.0 in cash and equivalents, $2.2 million of marketable securities, and $15.0 million of availability on its revolving credit facility.

SELF IR

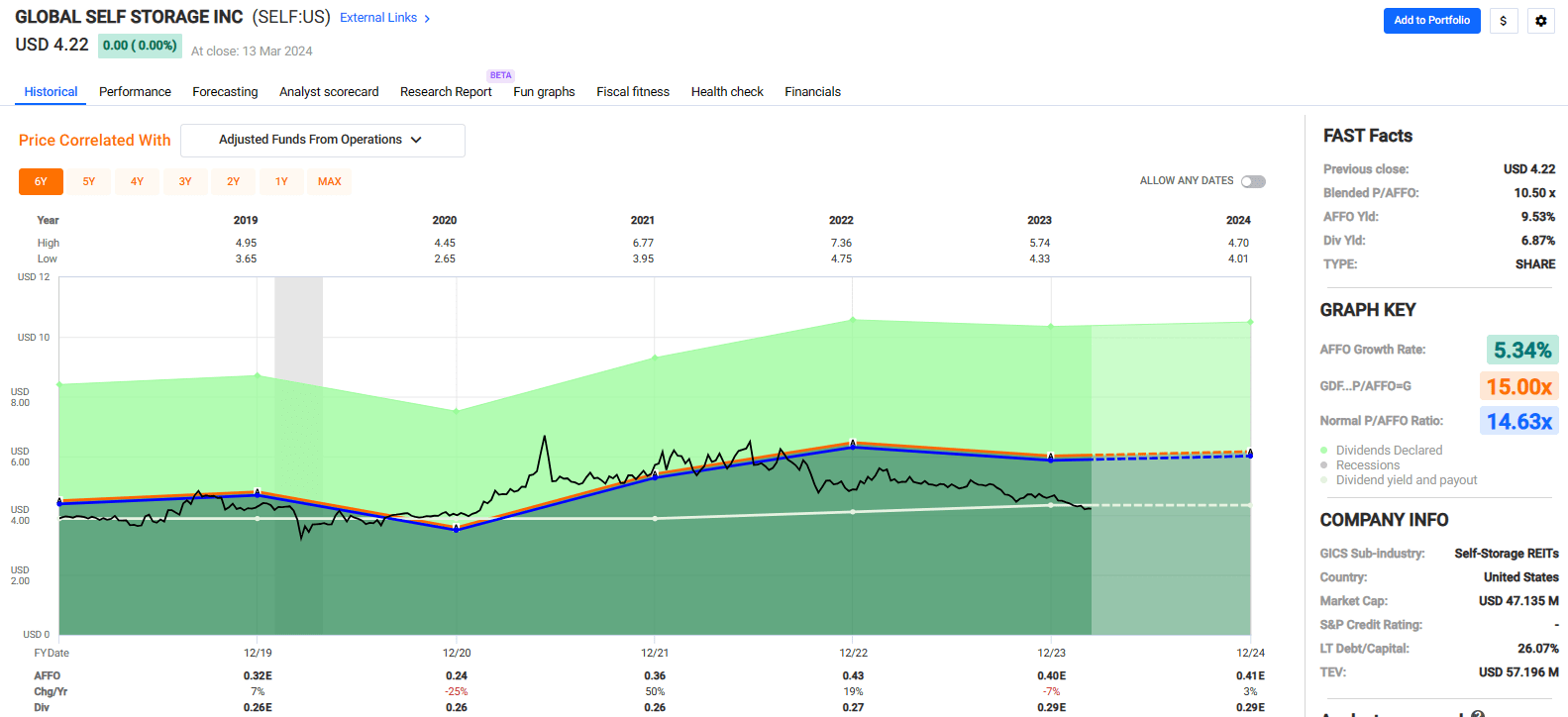

Since 2019, Global Self Storage has delivered an average adjusted funds from operations ("AFFO") growth rate of 5.34% and an average dividend growth rate of 2.24%.

The company has not yet released its 2023 full-year operating results but analysts expect AFFO to fall by 7% in 2023 but then increase by 3% in 2024.

The stock pays a 6.87% dividend yield that is well covered with an expected 2023 AFFO payout ratio of 72.50% and currently trades at a P/AFFO of 10.50x, compared to its average AFFO multiple of 14.63x.

We rate Global Self Storage a Spec Buy.

FAST Graphs

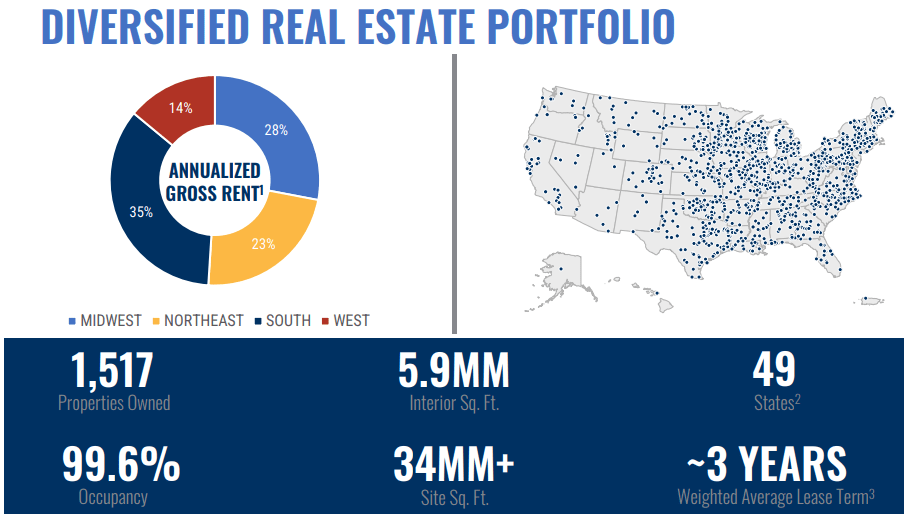

Postal Realty is an internally managed REIT that specializes in the acquisition and management of properties that are leased to the United States Postal Service ("USPS").

The company has a market cap of approximately $314.6 million and a portfolio comprised of 1,517 properties located across 49 states. In total PSTL's properties cover 34.0 million site SF and contain almost 6.0 million SF of interior space.

PSTL structures its leases as modified double net leases which makes USPS responsible for property taxes, utilities, and certain property maintenance. The leases are typically for 5 years which allows flexibility in the REITs ability to execute renewals at market rents, and most of its recently renewed leases contain annual rent escalations.

As of its most recent update, the company had a portfolio occupancy of 99.6% with a weighted average lease term ("WALT") of approximately 3 years.

PSTL - IR

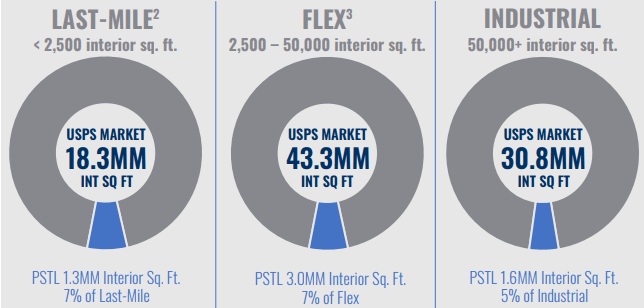

The company's portfolio includes Last-Mile offices which are under 2,500 interior SF, Flex facilities which range from 2,500 to 50,000 interior SF, and Industrial properties that total more than 50,000 interior SF.

As a percentage of annualized base rent ("ABR") the company's largest property type is flex properties which makes up approximately half of the portfolio's total interior square feet and generates around 64.20% of its ABR.

The company has 963 last-mile properties that total 1.3 million SF and make up approximately 25.68% of its ABR, and 5 industrial properties that total 1.6 million SF and make up roughly 10.13% of the company's ABR.

PSTL - IR

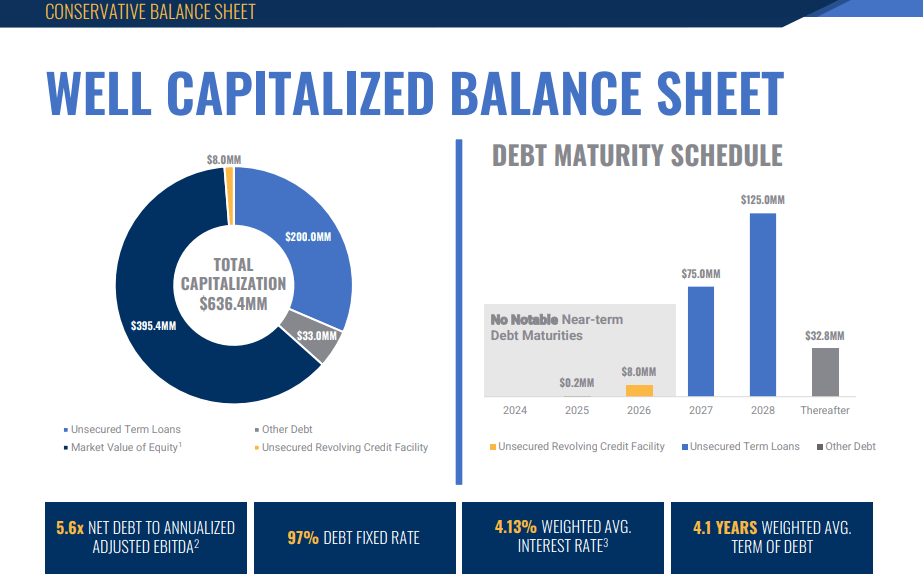

The company's debt schedule is nicely positioned with no debt maturities in 2024 and no significant debt maturities until 2027.

PSTL has solid debt metrics including a net debt to adjusted EBITDA of 5.6x, a long-term debt to capital ratio of 51.10%, and an EBITDA to interest expense ratio of 3.13x.

Plus, 97% of its debt is fixed rate with a weighted average interest rate of 4.13% and a weighted average term to maturity of 4.1 years.

PSTL IR

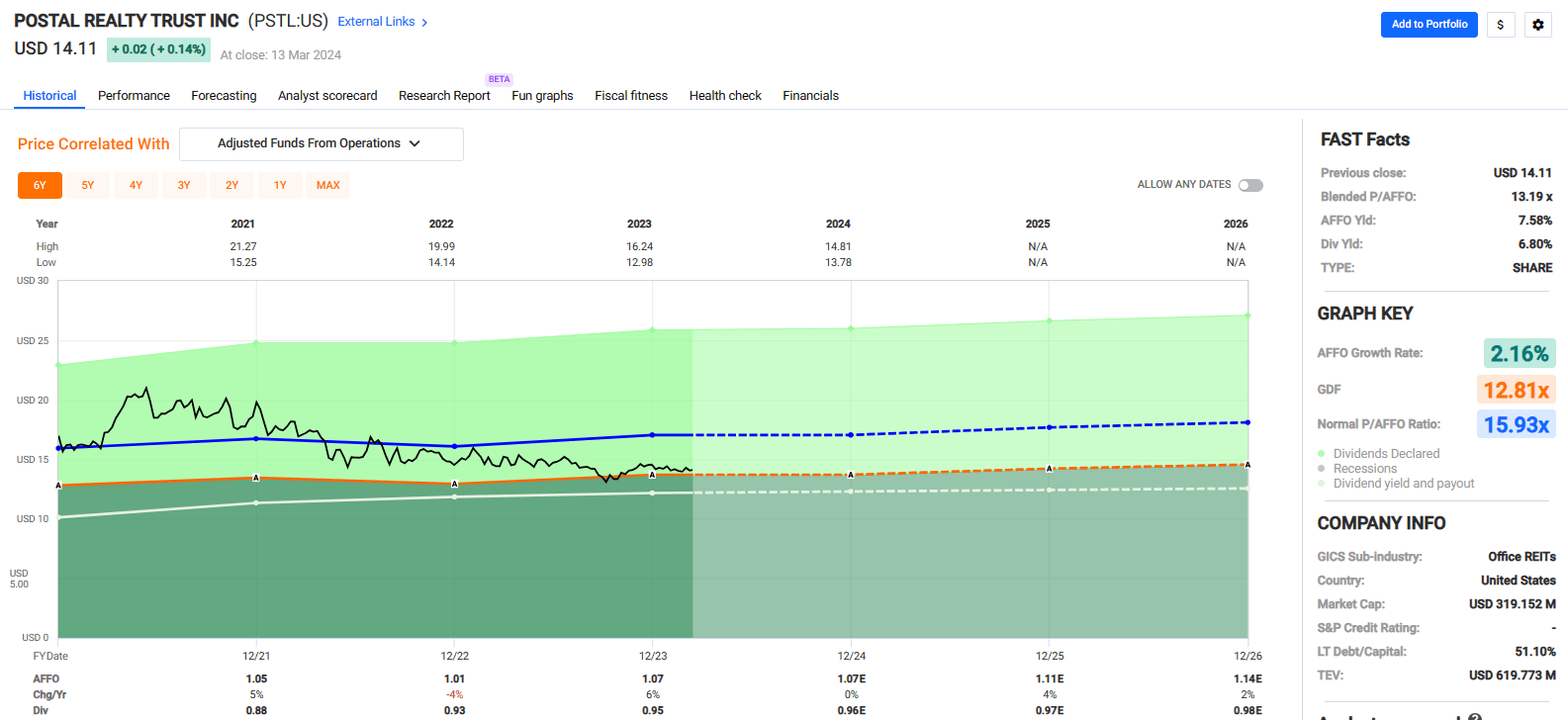

Since 2021, PSTL has had an average AFFO growth rate of 2.16% and an average dividend growth rate of 6.42%. Analysts expect AFFO to remain flat in 2024 but then to increase by 4% in 2025 and by 2% the following year.

The stock pays a 6.80% dividend yield with a 2023 AFFO payout ratio of 88.79%. That's a little on the high side, but it is an improvement over its AFFO payout ratio of 91.58% in 2022.

As the company moves forward, I'd like to see it maintain an AFFO payout ratio under 85% but as it now stands the REIT can adequately cover its dividend.

Currently the stock is trading at a P/AFFO of 13.19x, compared to its average AFFO multiple of 15.93x.

We rate Postal Realty Trust a Spec Buy.

FAST Graphs

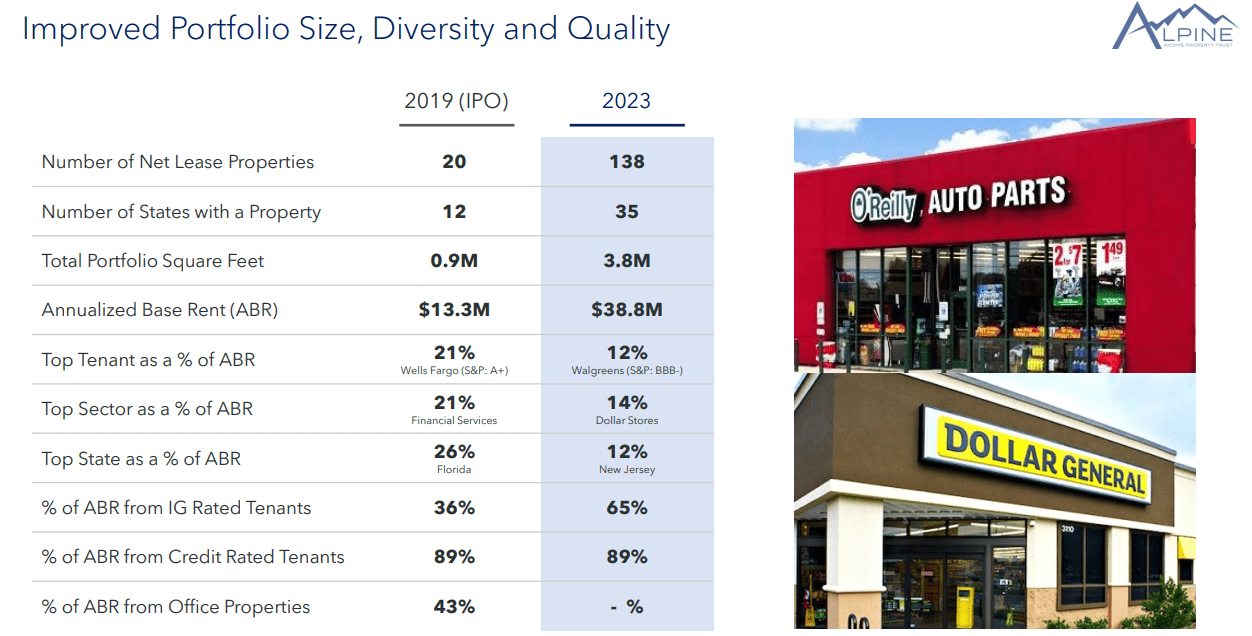

PINE is an externally managed REIT with a market cap of approximately $208.0 million and a 3.8 million SF portfolio made up of 138 net lease properties located across 35 states.

The net-lease REIT is externally managed by CTO Realty Growth (CTO), and while I normally have reservations about investing in externally managed REITs, there appears to be high-alignment between the companies as the external manager owns a 16% interest in PINE.

(Although, I would like to see PINE sold to unlock value for CTO investors.)

The properties PINE owns or has an interest in are generally subject to long-term, net-leases which require the tenant to pay for operating expenses related to the property including taxes, property insurance, utilities, and maintenance.

In addition to its net-leased properties, the company engages in the acquisition and origination of commercial loans which are typically secured by commercial real estate.

Since its IPO in 2019, the company has grown its property count from 20 to 138, its number of states from 12 to 35, its portfolio square feet from 0.9 million to 3.8 million, and its ABR from $13.3 million to $38.8 million.

While the company has grown its portfolio at a rapid clip, it has also improved the diversity of its portfolio on several fronts. In 2019 PINE's top tenant made up 21% of its ABR, compared to 12% in 2023. Similarly, the concentration in its top sector improved from 21% in 2019 to 14% last year.

The company has also improved the quality of its portfolio since its IPO. In 2019 the net lease REIT derived 36% of its ABR from investment-grade ("IG") tenants, compared to 65% in 2023. Plus, the company reduced its office exposure from 43% of its ABR in 2019 to 0% of its ABR in 2023.

At the end of 2023 the company's portfolio was 99% occupied and had a WALT of 7.0 years.

PINE - IR

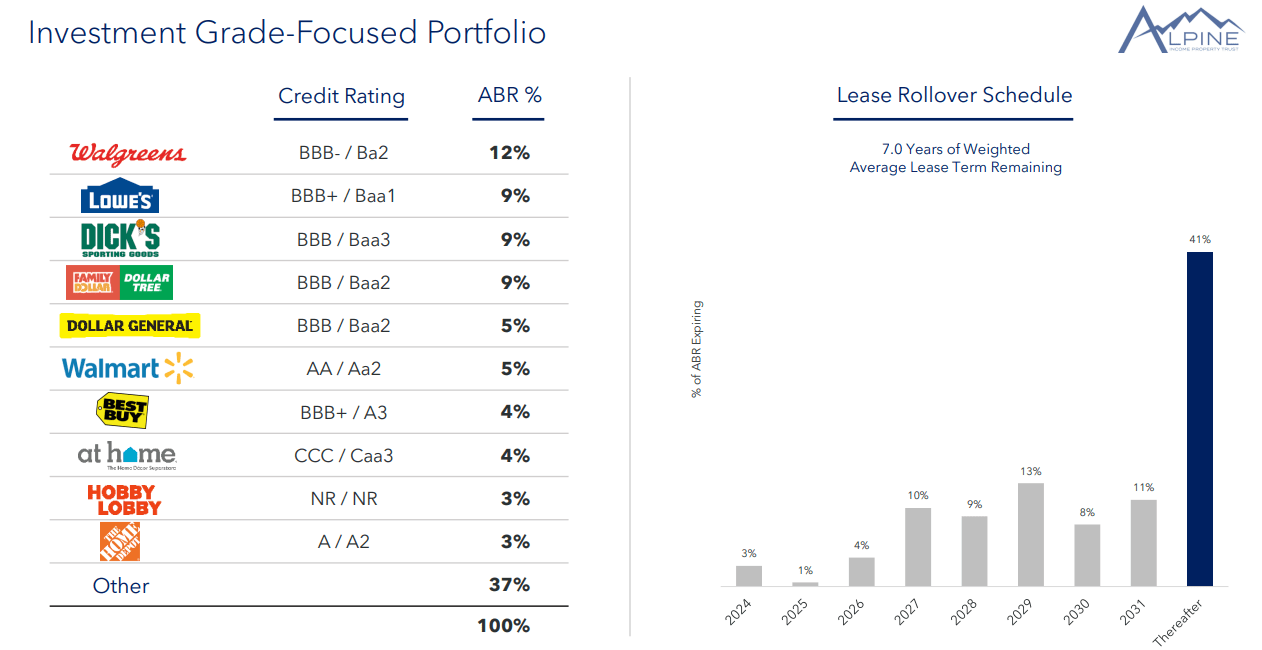

PINE's top tenants are a good reflection of the high-quality nature of its portfolio. Its top tenant is Walgreens, which made up 12% of the company's ABR, followed by Lowe's, which made up 9%.

Other notable tenants include Dollar Tree, Dick's Sporting Goods, Walmart, and Home Depot. Out of its top-10 tenants, only one is not credit rated (Hobby Lobby) and 8 out of its top-10 tenants are investment-grade rated.

Plus, as previously mentioned, the company's W.A. lease term is roughly 7.0 years with the majority of its leases set to rollover after 2031.

PINE IR

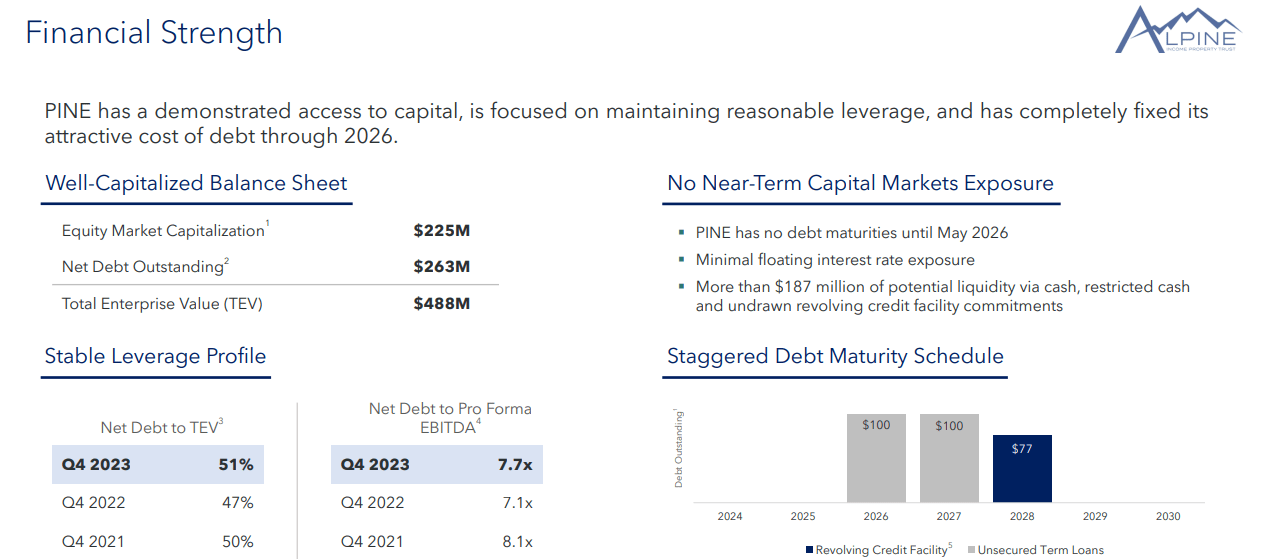

Alpine has reasonable debt metrics such as a long-term debt to capital ratio of 52.94% and a total debt to total assets ratio of approximately 50%.

One of the most attractive features of the company's credit profile is its debt maturity schedule which has no debt maturities until May of 2026.

Additionally, the company has fixed its cost of debt through 2026 and has approximately $187.0 million of liquidity as of its latest update.

PINE has a net debt to pro forma EBITDA of 7.7x as of 4Q-23. While this is an improvement over its leverage ratio at the end of 2021 and 2022, it is still higher than I'd like to see.

PINE IR

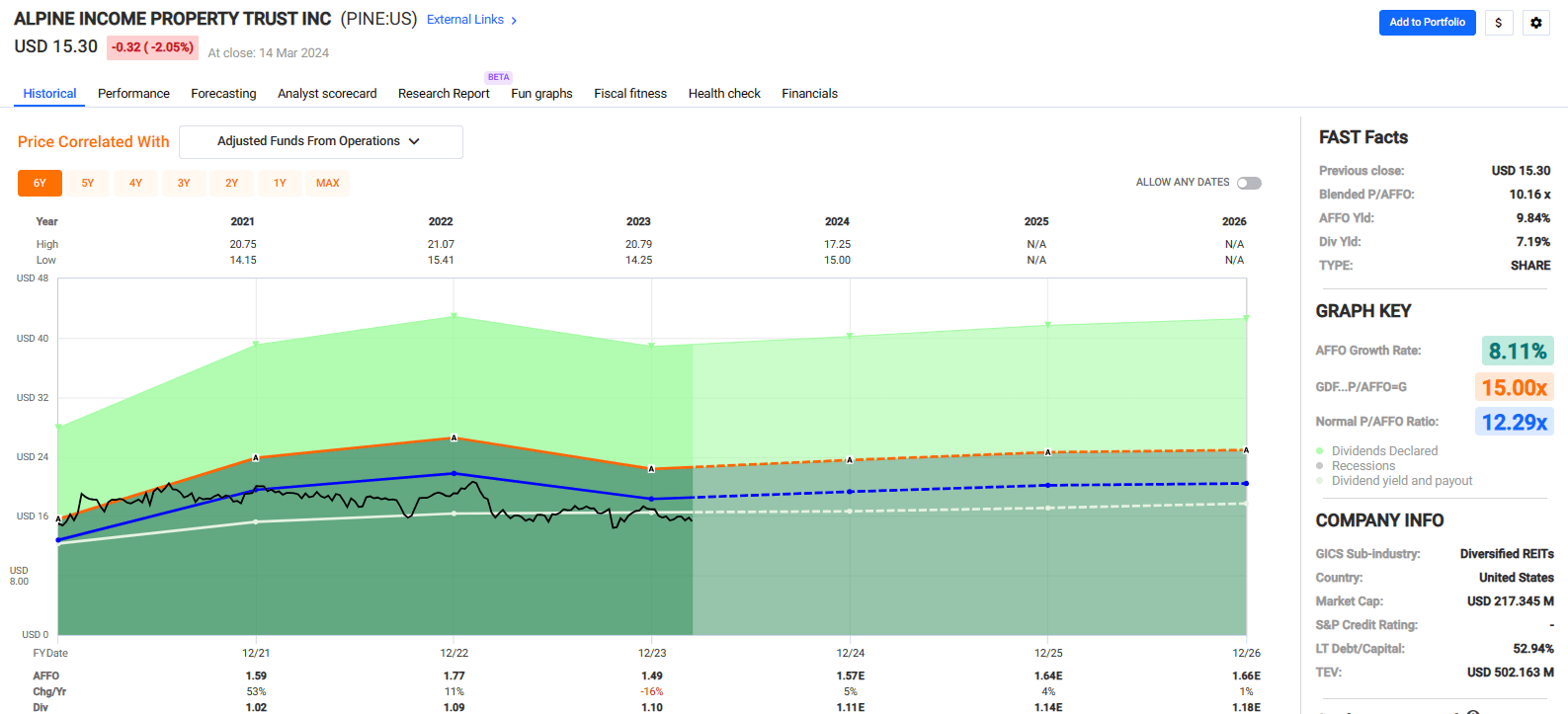

Since 2021 the company has had an average AFFO growth rate of 8.11%. This number is somewhat inflated due to the 53% growth rate in 2021. In 2022 the company's AFFO per share increased by 11%, but then fell by -16% in 2023.

Analysts expect AFFO growth of 5% in 2024 and then AFFO growth of 4% and 1% in the years 2025 and 2026 respectively.

The stock pays a 7.19% dividend yield that is well covered with a 2023 AFFO payout ratio of 73.83% and trades at a P/AFFO of 10.16x, compared to its average AFFO multiple of 12.29x.

We rate Alpine Income Property Trust a Spec Buy.

FAST Graphs

I hope you enjoyed my "Cinderella picks" and I look forward to your comments below.

I have a few others that I plan to share along with our "Sweet 16 REITs".

Always remember to diversify and not just "bet the farm" on one stock.

Over the years (and due to some valuable life lessons) I must always stress the importance of diversification, which is in itself, is the simplest way to obtain a margin of safety so you can sleep well at night.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.