Tony Anderson

Tony Anderson

Cavco Industries, Inc. (NASDAQ:CVCO) is a leading builder of manufactured and modular homes in the United States. Founded in 1965 and headquartered in Phoenix, Arizona, Cavco operates a network of manufacturing facilities across the country and offers a wide range of homes under various brand names, catering to different market segments and price points.

CVCO is a quality business, with a strong business model and considerable reach across the US. The company operates in key geographies in the US and has developed a broad offering for consumers. The company is a premier homebuilder in the US.

Importantly, however, the industry is enjoying considerable tailwinds which we do not expect to slow. There is an inherent shortage of homes across the West, which is unlikely to be rectified in the medium term. CVCO's performance during the last decade illustrates the combination of the two, as the company has consistently gained market share and grown well.

We expect current economic conditions to weigh on the company in the near term, which in combination with its share price run-up, reduces the scope for upside for shareholders. This said, we are bullish should the share price experience a correction.

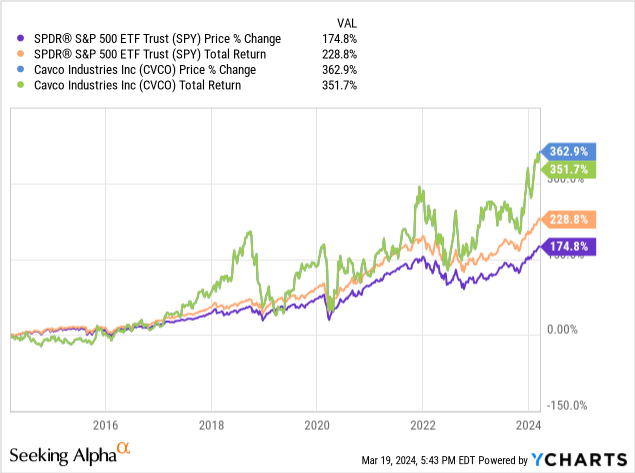

CVCO's share price performance has been impressive, gaining over 350% since 2015. This is a reflection of its strong performance and improving investor sentiment.

Capital IQ

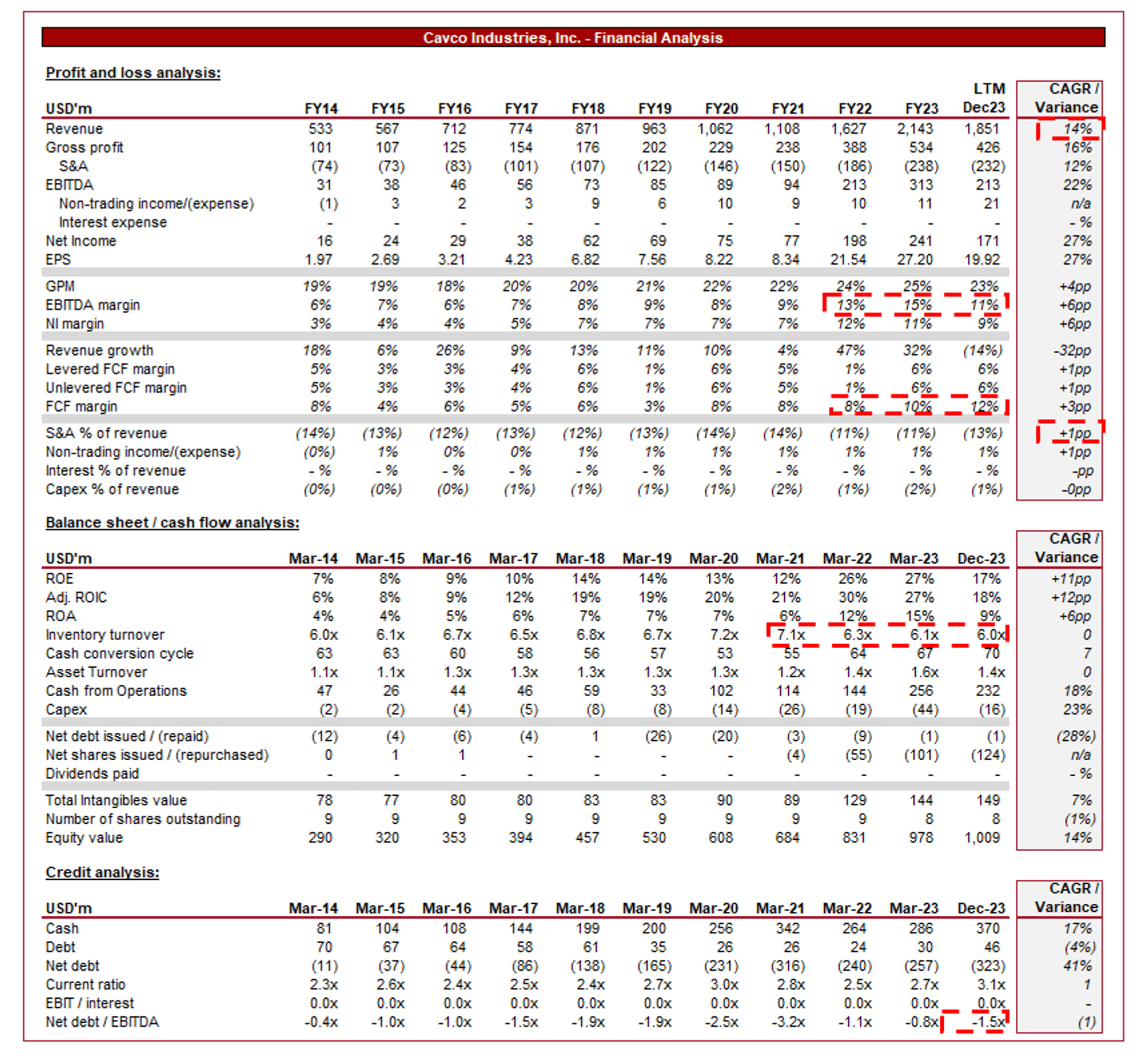

Presented above are CVCO's financial results.

CVCO's revenue has grown impressively during the last decade, with a CAGR of +14% and a linearity of 0.9, reflecting supreme consistency. Alongside this, EBITDA has grown at a CAGR of +22%.

CVCO primarily operates in the manufactured housing industry, specializing in the design, production, and distribution of factory-built homes. The company manufactures various types of homes, including single-family residences, multi-section homes, modular homes, and park-model RVs.

CVCO offers a diverse range of housing products that are specifically tailored to meet different customer needs and preferences (# of rooms, specifications, etc.). This includes entry-level homes, mid-range homes, luxury homes, and specialty homes for specific market segments such as retirees or vacationers. This broad approach has allowed the company to considerably scale in recent years.

CVCO is vertically integrated, controlling all the key stages of the manufacturing process, including design, engineering, fabrication, assembly, and finishing. By vertically integrating its supply chain, the company maintains greater control over quality, costs, and the production schedule, resulting in operational efficiencies over time.

One of CVCO's key competitive drivers is its prioritization of innovation in its product design, construction techniques, and manufacturing processes to enhance the quality, durability, and energy efficiency of its homes. CVCO's offering is highly regarded in the industry, where quality and capabilities are just as important as price.

Underpinning this is CVCO's brands. CVCO owns and operates several well-known brands in the manufactured housing industry, including Cavco Homes, Fleetwood Homes, Palm Harbor Homes, and Nationwide Homes, among others. Each brand targets specific market segments and geographic regions, allowing for reach and visibility.

Alongside its own function, CVCO sells its homes through a network of independent retailers, dealers, and distributors located across the United States and Canada. The company's brands and notoriety allow CVCO to operate an extensive dealer network that enables it to maximize its reach.

The manufactured housing industry has experienced favorable tailwinds, including low mortgage interest rates, favorable lending conditions, and government support for affordable housing initiatives. These macroeconomic factors are the primary reason for CVCO's consistent growth over the last decade, in conjunction with its strong competitive position.

We expect CVCO to benefit from robust demand for affordable housing solutions in particular, but wider demand as a whole, driven by demographic trends, population growth, urbanization, and changing consumer preferences. The US, like much of the West, is experiencing a housing shortage due to historical underinvestment and decades of immigration. This is a tailwind that we do not believe will slow in the medium term.

As CVCO continues to expand its market presence and geographic footprint through organic growth initiatives and strategic acquisitions, we believe the company is primed to enjoy growth and further gain market share.

CVCO competes with other manufactured and modular home builders such as D.R. Horton, Inc. (DHI), Lennar Corporation (LEN), PulteGroup, Inc. (PHM), and Skyline Champion Corporation (SKY).

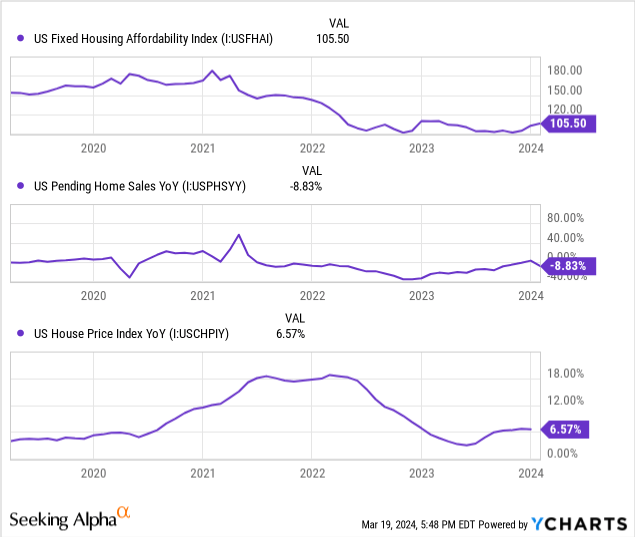

Current economic conditions represent near-term headwinds, following a decline in the US housing market. With elevated interest rates and inflation, the cost of home ownership and moving home has considerably increased, deterring activity.

As the following illustrates, US affordability has declined (metric assessing the average household's ability to afford home ownership), only slightly increasing over 100 again. This reflects the significance of the impact of the cost of living crisis, likely a major reason for a reduction in activity.

This reduction is reflected in the second graph, with a considerable decline in pending home sales relative to prior years and essentially flat growth (following a period of negative growth).

Looking ahead, we expect activity to remain muted so long as rates remain high. The positive for the US market is that inflation is decelerating rapidly, meaning rates could begin declining imminently.

Whilst there will be damage to the housing market from this, we expect the bounce back to be reasonable. The reason for this is the resilience we are seeing in the market, likely due to the tailwinds discussed above offsetting some of the downside. As the final graph illustrates, prices have broadly remained flat rather than declining, implying consumers are retaining equity in their properties, priming activity to increase.

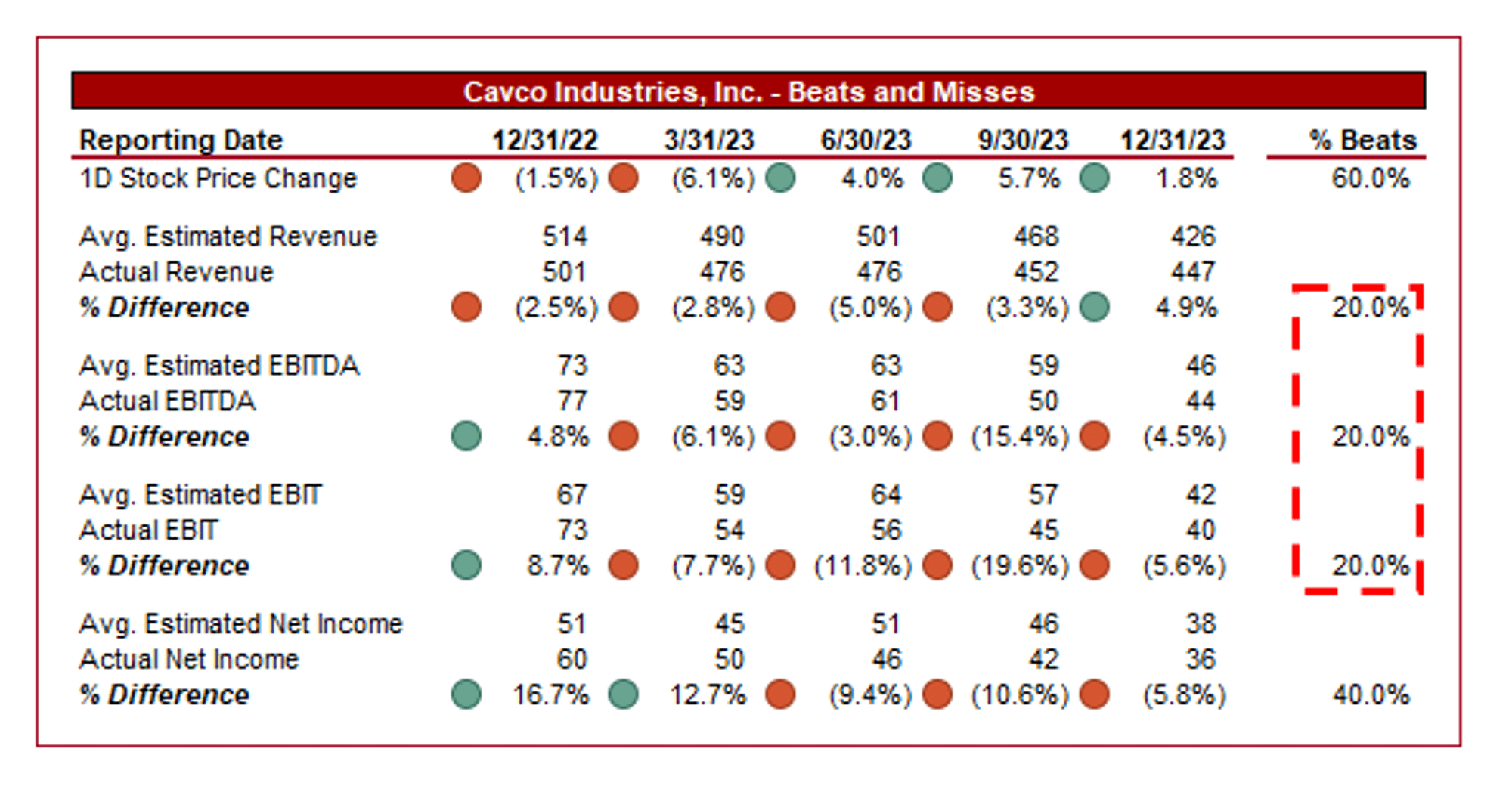

CVCO's recent performance has been weak, reflecting the near-term headwinds experienced. The company's top-line growth in its last four quarters was (5.8)%, (19.1)%, (21.7)%, and (10.8)%.

In Q3, Management has seen an improvement in orders, with the highest levels for six quarters. We attribute this strength to the reduced uncertainty around interest rates, with greater confidence that rates will begin to soften and the lending market will improve.

This said, it is worth highlighting that revenue per home has declined (5.3)% in Q3, with a consistent decline in margins. Whilst we do expect this to normalize, there is a risk of a continuation of this trend.

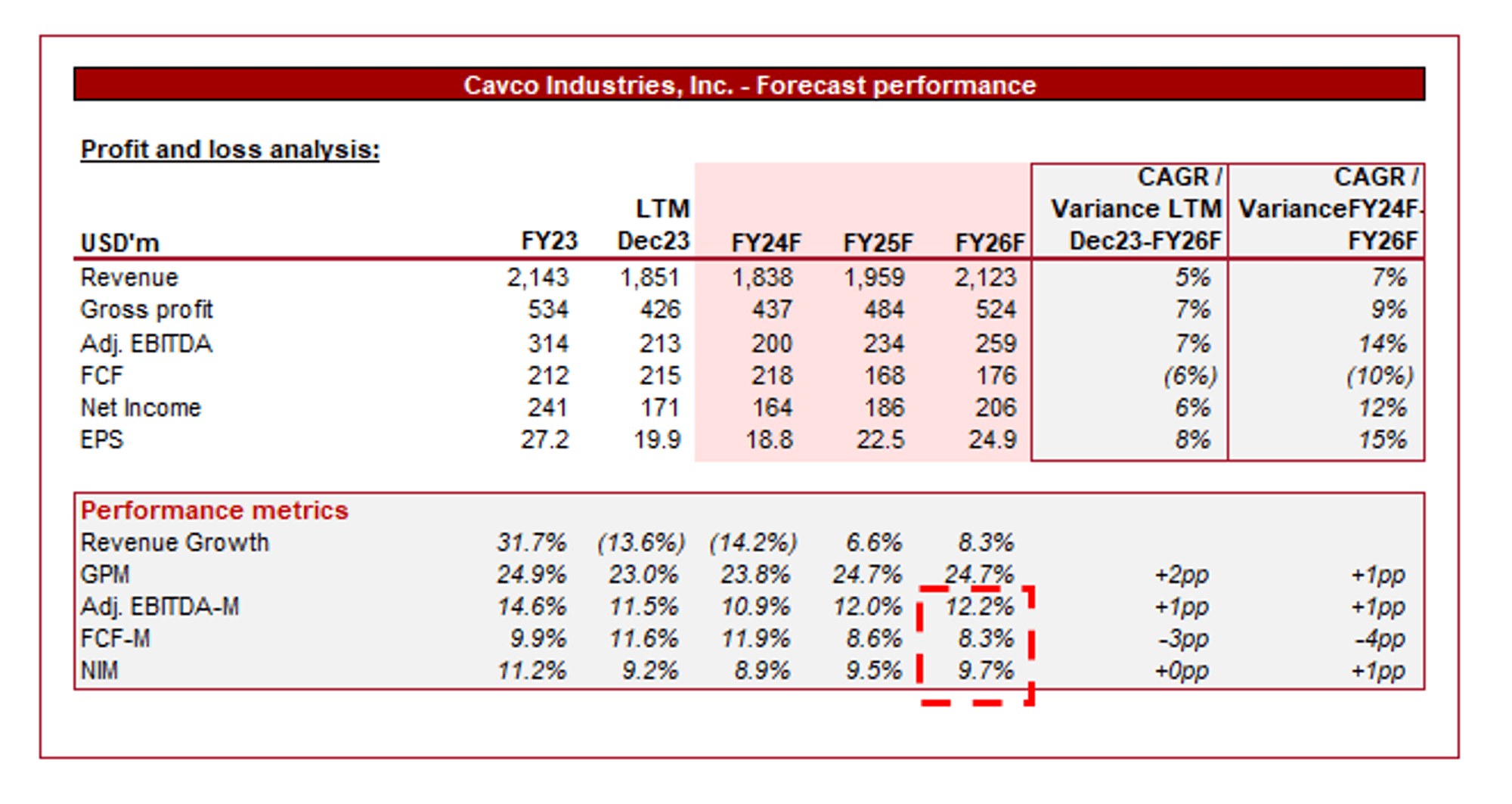

Capital IQ

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting reasonable growth in the coming years, with a CAGR of +5%. In conjunction with this, margins are expected to improve but remain below its FY22 levels.

We concur with these estimates, albeit expecting worse growth in FY25F and better in FY26F, as the housing economy recovers from the current bear market. Further, given the expected boom post-pandemic, we believe it is unlikely the margins achieved in FY22-FY23 are sustainable at its existing scale.

Capital IQ

The rapid deceleration in CVCO's performance is reflected above, with quite considerable misses. Interestingly, this has not impacted its share price, which implies investors have expected this and priced in the weakness. This provides a degree of comfort for any near-term uncertainty.

Capital IQ

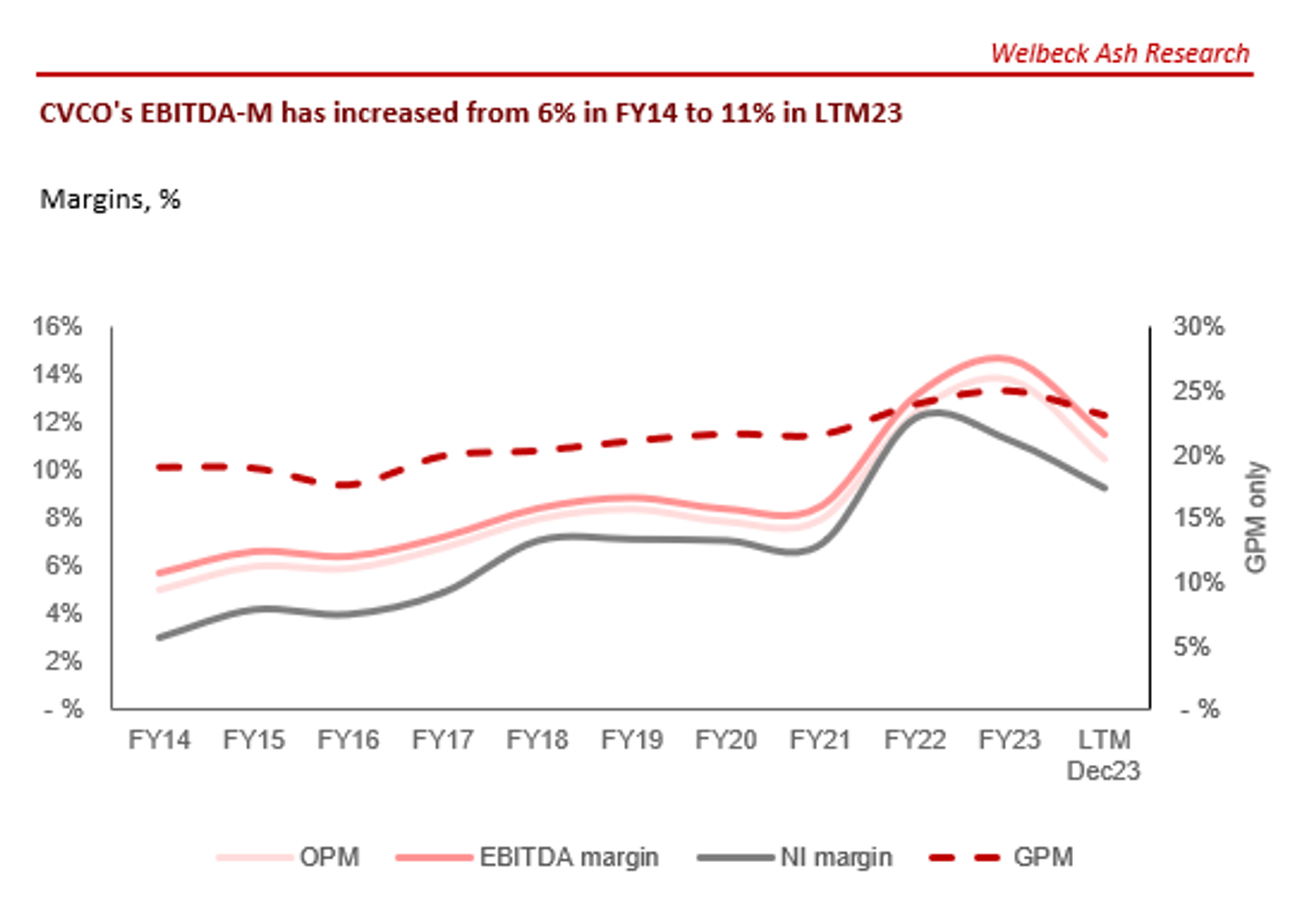

CVCO's margin improvement has been strong, almost wholly delivered through an uplift in GM%. This is a reflection of economies of scale and superior production techniques, while Management has continued to invest in growth through its S&A cost base (only 1ppt of dilution).

We suspect gradual improvements are possible, with the eventual goal being to dilute S&A spending and optimize as the company reaches maturity.

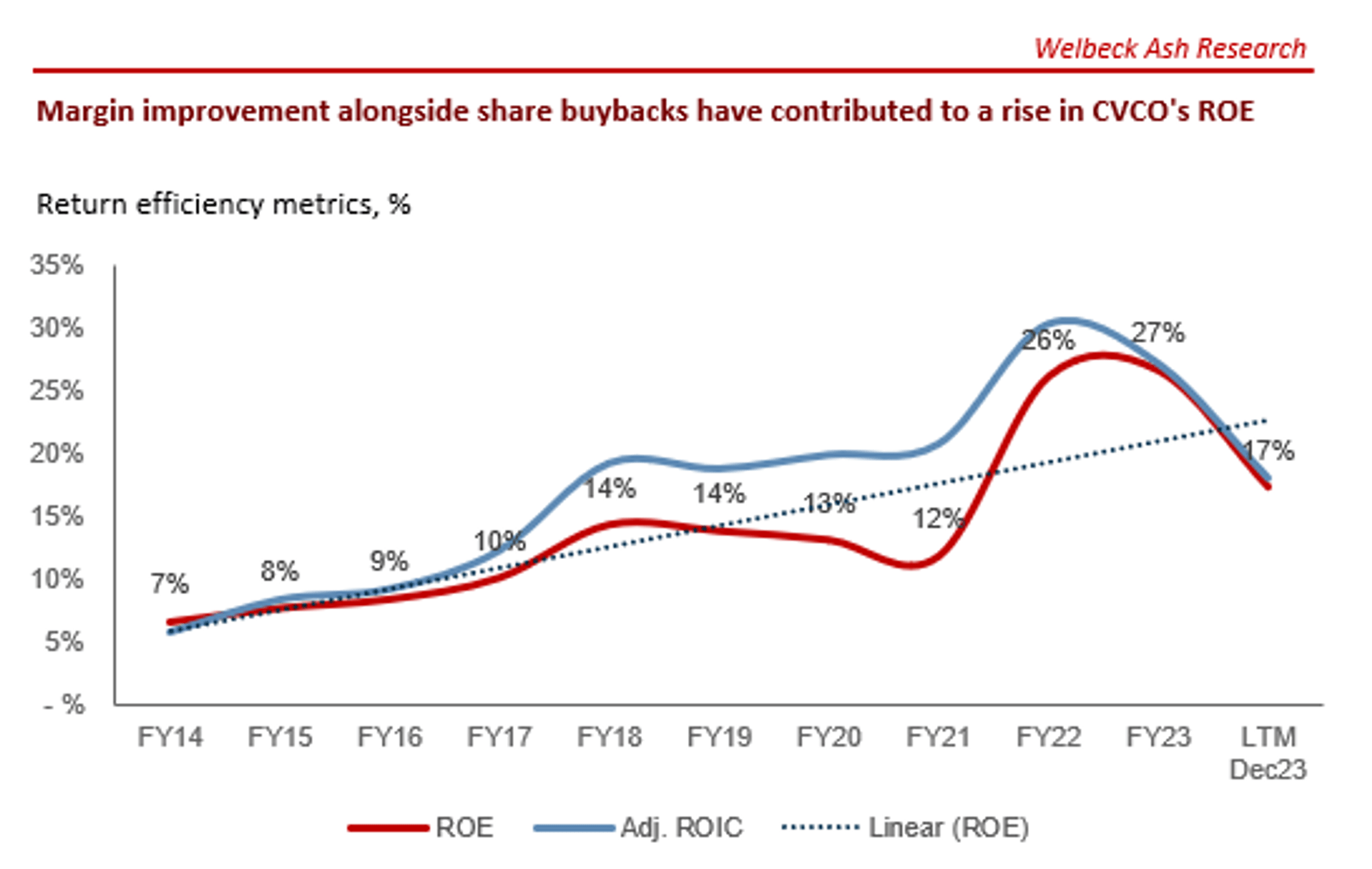

CVCO is conservatively financed, with a strong net cash position providing the company with the flexibility to reinvest in growth and distribute to shareholders. This has been facilitated by its FCF expansion, which has broadly tracked margin growth.

Capital IQ

Seeking Alpha

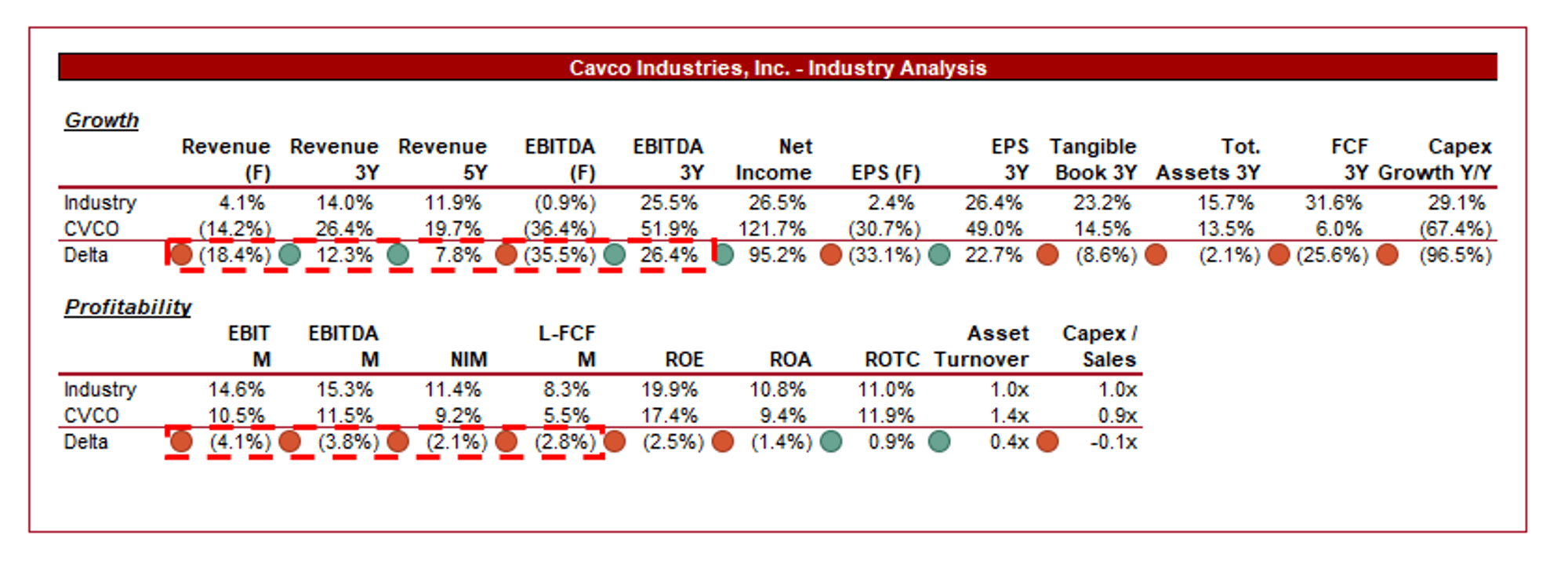

Presented above is a comparison of CVCO's growth and profitability to the average of its industry, as defined by Seeking Alpha (23 companies).

CVCO's performance relative to its peers has been good, although does not necessarily wholly stack up. Its growth has been its clear value driver, which is likely a reflection of its segment's outperformance due to the considerable demand/supply housing disparity.

Its margins are lagging behind, however, which is a key factor in its valuation assessment. If growth can be maintained, CVCO can justifiably trade at a premium while a deceleration in growth will quickly contribute to a discount being warranted.

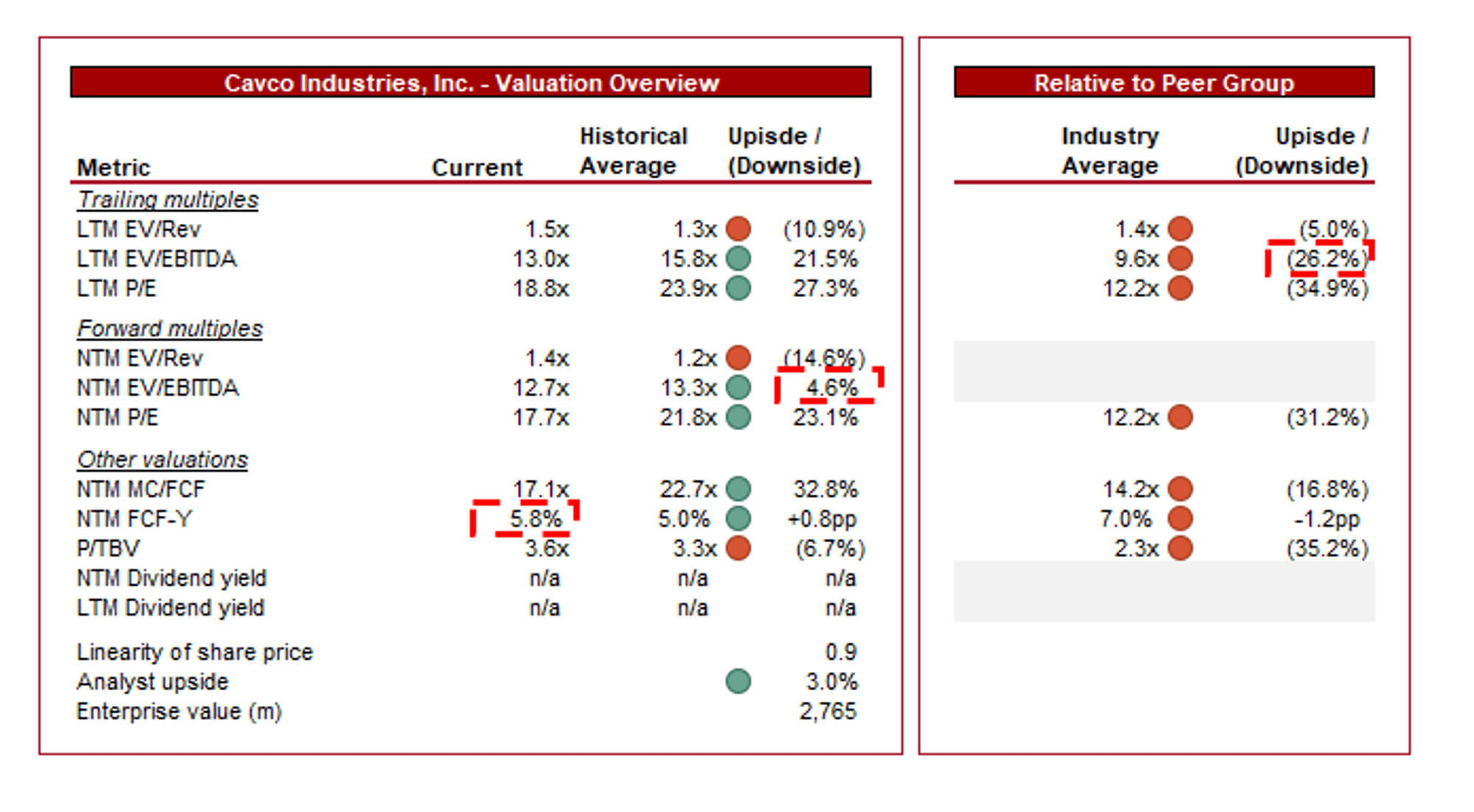

Capital IQ

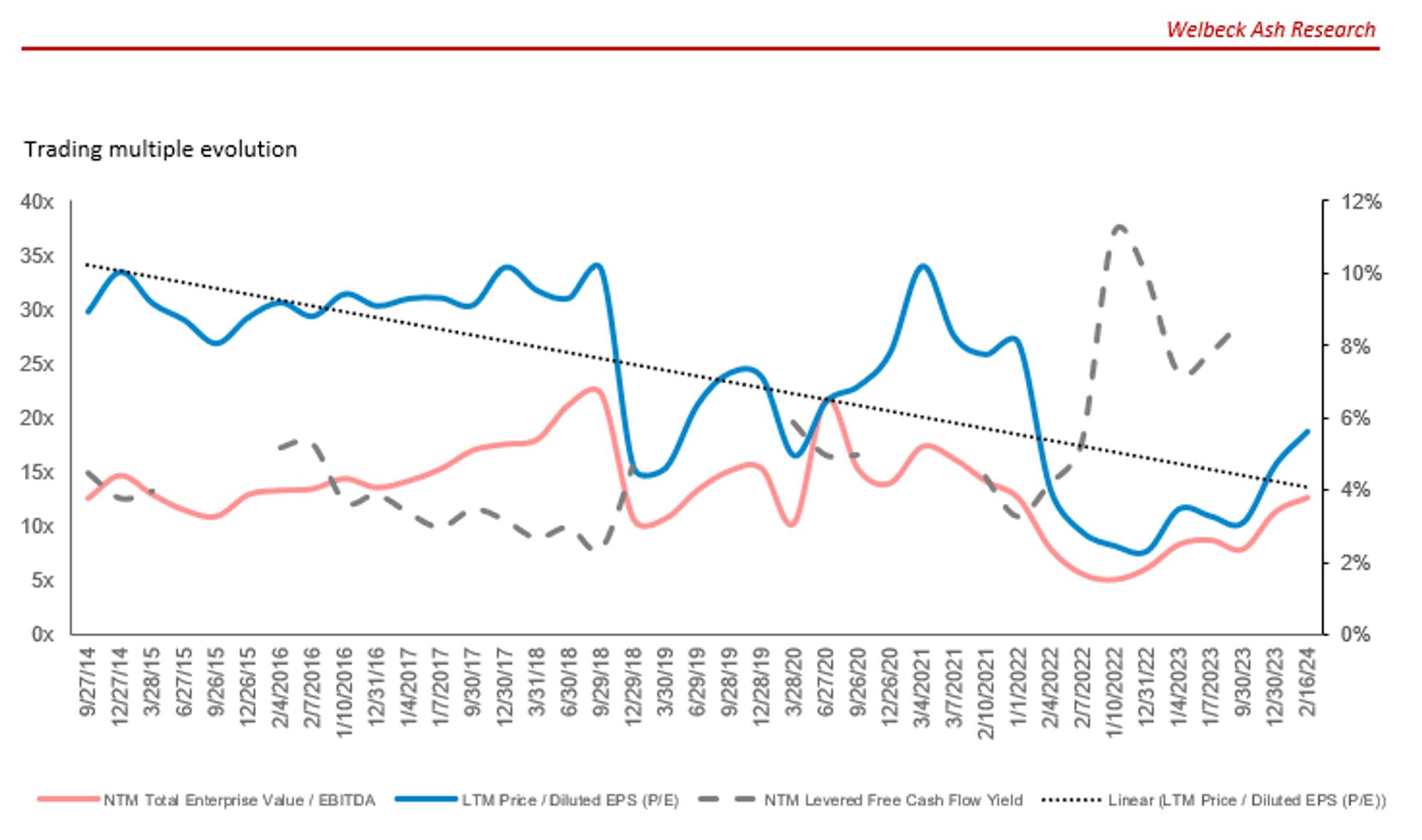

CVCO is currently trading at 13x LTM EBITDA and 13x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average implies CVCO is undervalued in our view. The company's margins have improved considerably, as has its market notoriety and growth potential. This should be rewarded against its valuation. This said, its historical valuation has broadly been fair, suggesting investor hesitancy which could explain the discount.

Further, CVCO is trading at a premium to its peers across all metrics, reflecting the market's view that CVCO can maintain its current growth trajectory and close the margin gap. This creates execution risk, albeit we do believe CVCO is well placed.

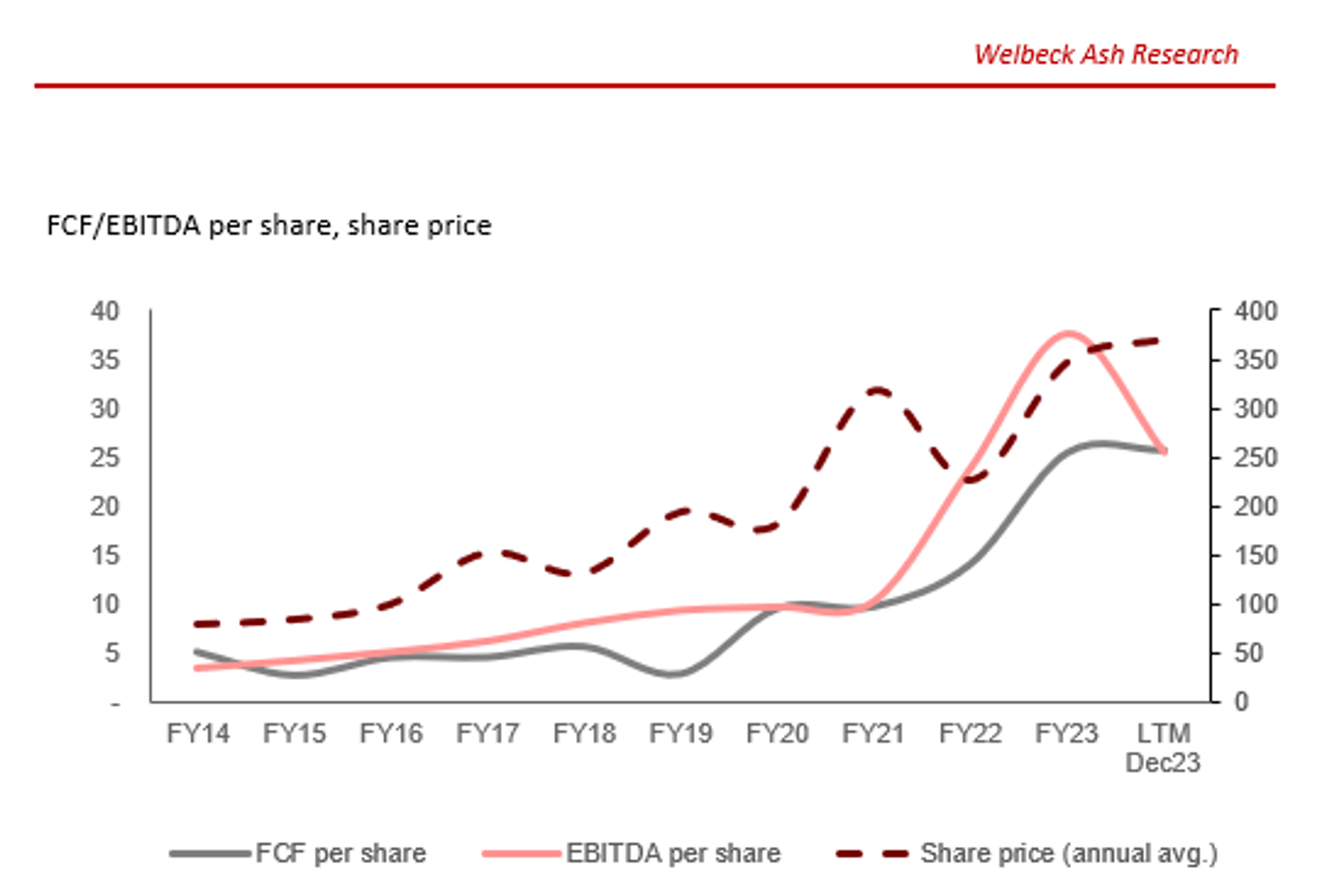

As the following illustrates, its share price has broadly tracked FCF/EBITDA per share, implying no immediate upside from mispricing. This said, if FCF/EBITDA continues to decline, we could see the opposite.

Capital IQ

Overall, we believe CVCO is likely priced correctly. The company could quickly have an upside if it can return to growth quickly, however, we see considerable equal downside risk due to the current uncertainty in the market. With such execution risk, we have this conclusion.

Capital IQ

The risks to our current thesis are:

CVCO is a fantastic business in our view. The company has a solid and ever-evolving business model, enjoying considerable tailwinds that Management has grasped to a better degree than its peers.

We believe there is a good chance CVCO can maintain its trajectory going forward, although faces risks currently due to the macroeconomic environment. We see this as a reset period, where growth and margins will decline. The key for CVCO is to maintain market share and continue to execute its long-term strategic goals.

While this is occurring, we rate CVCO a hold.