DNY59/E+ via Getty Images

DNY59/E+ via Getty Images

By Seema Shah, Chief Global Strategist

A much-flagged risk for this year is that, due to the Fed’s 2022-23 hiking cycle, the wall of maturing debt will face significantly higher refinancing costs, potentially triggering a spike in defaults.

However, assuming the economy remains fairly robust, a deeper look into the refinancing dynamics shows that, except for the lowest-quality segments of the credit spectrum, the broader credit space should be able to climb the wall relatively unscathed.

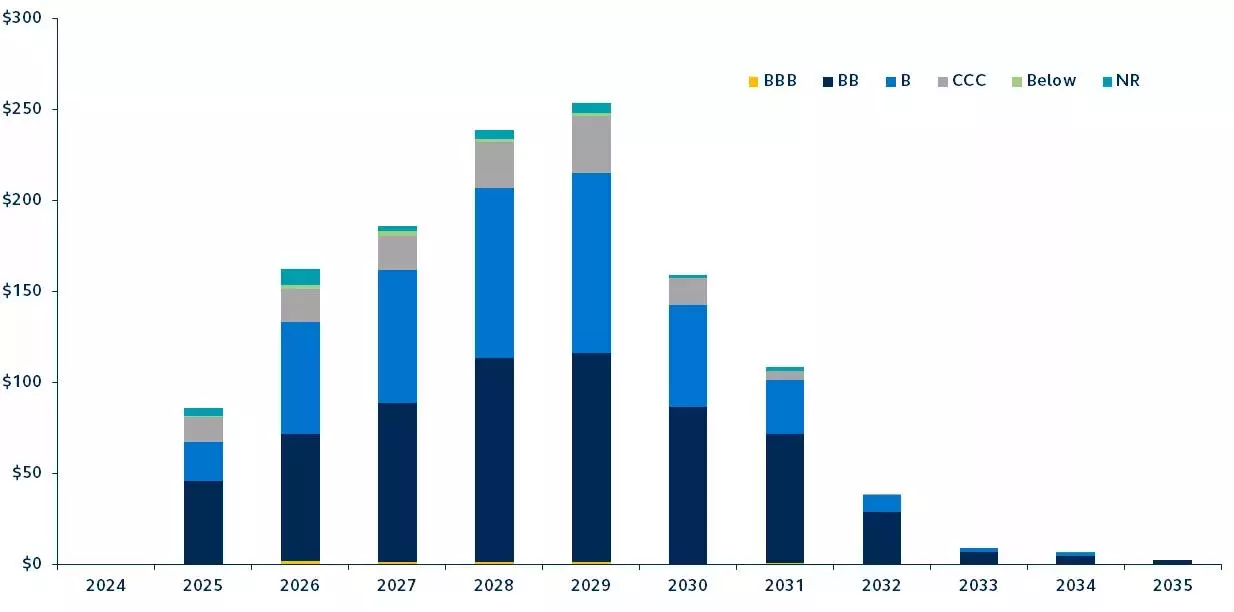

High yield maturity wall by credit quality

$billions of debt scheduled to mature per year

Source: Bloomberg, Principal Asset Management. Data represents the U.S. High Yield 2% Issuer Cap index. As this index excludes bonds that mature within the next year, the chart does not include any bonds maturing in 2024.

A record number of bonds issued during the pandemic at very low interest rates are set to mature over the next six years. In fact, within the next three years, a quarter of all U.S. high-yield debt will need to be refinanced at rates higher than what corporations have been accustomed to in recent years.

Although the elevated interest rate environment has spooked some investors into fearing that higher refinancing costs will lead to a sharp spike in defaults, a closer look reveals several factors that suggest most companies are in a good position to climb the debt maturity wall relatively unscathed:

While the maturity wall presents initial concerns, upcoming rate cuts and solid corporate balance sheets suggest most companies should be able to digest the higher interest rate costs without too much strain.

Still, lower-quality corporates may face tougher challenges, underscoring the importance of active management in the period ahead.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.