Aleksandr Zyablitskiy

Aleksandr Zyablitskiy

PGT Innovations (NYSE:PGTI) revenue has grown by about 5-fold over the past 10 years. However, this growth was driven more by acquisitions than organic growth. Moreover, the growth was at an unsustainable Reinvestment rate. At the same time, while bigger, there were hardly any improvements in the operating efficiencies.

The result is that while there was profit growth over the past 10 years, there was hardly any growth in the operating return and ROE. As such, when growth slows down because of funding constraints or lack of target, we will not have a wonderful company.

PGTI is now being acquired by Miter Brands at USD 42 per share to be paid in cash. I estimated that at this price, there is a margin of safety for Miter Brands. Unfortunately for the shareholders of PGTI, you can only benefit from the upside that came from the USD 42 share price.

PGTI pioneered the US impact-resistant window and door industry. It is today the leading US manufacturer and supplier of residential impact-resistant windows and doors.

The company has approximately 3,400 employees, five locations, and hundreds of products across its seven brands.

On 18 December 2023, Masonite International Corporation and PGTI announced a definitive agreement under which Masonite will acquire PGTI for a combination of cash and Masonite shares with a total transaction value of USD 3.0 billion.

PGTI shareholders will receive USD 41.00 per each PGTI share they own, comprised of USD 33.50 in cash and USD 7.50 in common shares of Masonite. The per-share consideration represents a premium of approximately 24% to PGTI's 30-day volume weighted average share price.

Upon completion of the transaction, Masonite shareholders will own approximately 84% of the combined company, with PGTI shareholders owning approximately 16%.

However, on 2 January 2024, PGTI said that it had received an unsolicited proposal from Miter Brands to acquire all outstanding shares of PGTI's common stock for $41.50 per share in cash.

Then on 8 January 2024, the Board of PGTI stated that if Miter was able to improve several aspects of its proposed acquisition, it would be a superior proposal to that of Masonite.

Subsequently, on 17 Jan 2024, Miter and PGTI announced that they had entered into a definitive agreement for MITER to acquire all outstanding shares of PGTI for USD 42.00 per share in cash. The purchase price represents a premium of 60% over PGTI's unaffected closing share price on October 9, 2023.

I was curious to see why Miter would be offering such a high premium for PGTI.

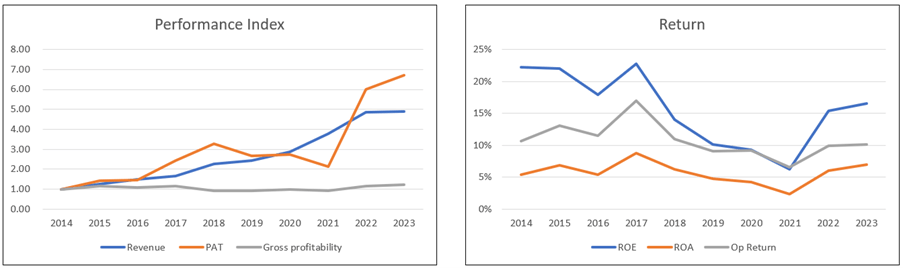

Over the past 10 years, PGTI revenue grew about 5-fold, while the PAT in 2023 was about 6.7 times that of 2014. You may think that this is an exceptional growth. But you have a different picture when you look at one operating efficiency metric - gross profitability (gross profits/total assets).

According to Professor Novy-Marx, gross profitability has the same power as Price Book Value in prediction cross section returns of stocks.

The gross profitability in 2023 was only 1.24 times that of 2014. Refer to the left part of Chart 1. It is not a fantastic improvement. This is reflected by the operating return (NOPAT/total capital employed) of 10.1% in 2023 compared to 10.6% in 2014.

We see a similar dismal picture for the ROE with the 2023 ROE of 16.5% being lower than the 2014 ROE of 22.2%. The only improving return was the ROA with 7.0% in 2023 compared to 5.4% in 2014. Refer to the right part of Chart 1.

Looking at both parts of Chart 1, I would deduce that:

Chart 1: Performance Index and Return (Author)

Note to Performance Index chart. To plot the various metrics on one chart, I have converted the various metrics into indices. The respective index was created by dividing the various annual values by the respective 2014 values.

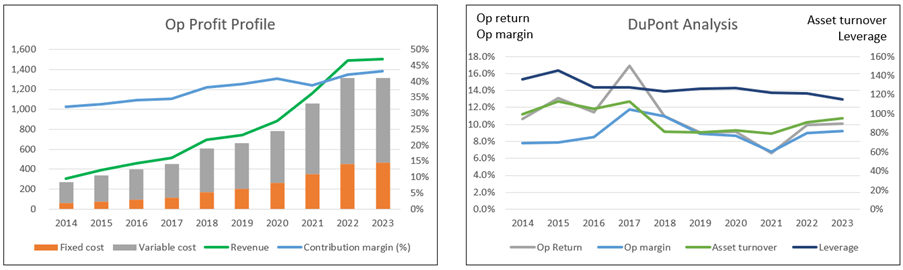

To verify that it was not a productivity or efficiency-led growth, I carried out a DuPont Analysis of the operating return and a breakdown of the operating profit. Refer to Chart 2.

From 2014 to 2023, revenue grew at 19.3% CAGR while total assets grew at 20.0% CAGR. You should not be surprised to see a declining asset turnover. This meant no improvement in capital efficiency. This was a capital-driven growth.

While there was an improving contribution margin (refer to the left part of Chart 2), there was hardly any improvement in operating margin (refer to the right part of Chart 2). This was because of increasing fixed costs, especially the Selling, General, and Administration (SGA) expenses. SGA margin (SGA/revenue) increased from 18% in 2014 to 24% in 2023.

Leverage or the equity multiplier also reduced from 2014 to 2023. While a reduction in leverage is good from a financing perspective, it is not desirable if it leads to lower returns.

The growth strategy seemed more about just getting bigger rather than seeking also operating improvements. There was no evidence of benefits from economies of scale despite being about 5-times bigger in revenue and total assets.

A pessimistic interpretation for the lack of operating improvements was that management overpaid for the acquisitions. Alternatively, management was not able to reap the synergies of the acquisitions. Whatever the interpretations, it does not present management in good light.

Chart 2: Operating Profit Profile and DuPont Analysis (Author)

Note to Op Profit Profile. I broke down the operating profits into fixed costs and variable costs.

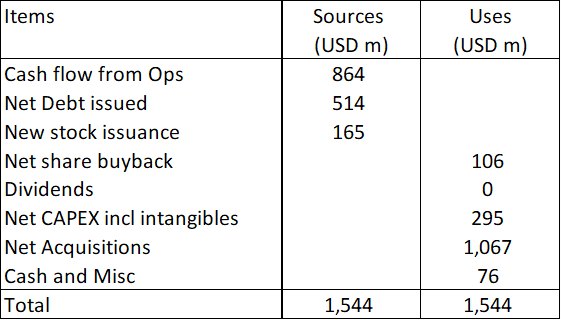

From 2014 to 2023, PGTI spent about USD 295 million on net CAPEX (after deducting for sales of PPE) compared to USD 1,067 million on net acquisitions (after deducting for dispositions). In other words, net CAPEX accounted for only 22% of the total investments (CAPEX plus acquisitions).

To give you a sense of the size of the CAPEX and acquisitions, the average total asset from 2014 to 2023 amounted to USD 900 billion. This meant that the amount spent on acquisitions was more than the average total assets. This was an investment driven growth.

The company did not give a breakdown of the growth due to organic growth and acquisitions. But looking at the ratio between the amount spent for CAPEX and acquisitions, I would say that more of the growth was due to acquisitions.

To fund the growth, the company had to rely on some debt issuance. Refer to Table 1. You can see that the cash flow from operations over the past 10 years was not sufficient to fund the acquisition.

Table 1: Sources and Uses of Funds 2014 to 2023 (Author)

There is another perspective on how the growth was funded. Growth can be determined from the fundamental growth equation of Growth = Return X Reinvestment rate.

Return = NOPAT/total capital employed.

Reinvestment rate = Reinvestment/NOPAT.

Reinvestment = Net CAPEX + Net Acquisitions - Depreciation & Amortization + Net Changes in Working Capital.

I estimated that from 2014 to 2023, the total Reinvestment amounted to USD 1,160 million. Its total NOPAT for the same period amounted to only USD 725 million. In other words, the Reinvestments to grow the company were greater than the profits generated. It is not a sustainable growth strategy.

What are the key takeaways?

Extrapolating from here, there would be a significant drop in growth when there are no further acquisitions due to either a lack of funding or a lack of reasonably priced targets.

I also have concerns about PGTI's financial position, as there were more negative than positive points.

In valuing PGTI, I took account of the following:

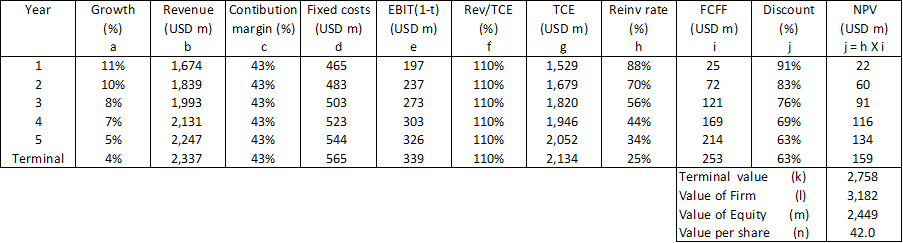

I thus adopted a multi-stage growth model where:

Based on this valuation model, I estimated the intrinsic value of PGTI to be USD 70 per share.

Using the same model with the starting annual growth rate of 11.3%, I would obtain an intrinsic value of USD 42 per share. This is equal to the Miter offer price.

I valued PGTI based on a multi-stage Free Cash Flow to the Firm (FCFF) model where the revenue would be reduced from a high growth rate to a terminal growth rate of 4% over 5 years.

Value of the firm for the year or NPV for the year = FCFF X Discount rate.

FCFF = EBIT(1-t) X (1 - Reinvestment rate)

To derive the EBIT, I used the financial model based on the operating profit model illustrated in the left part of Chart 2.

EBIT = Revenue X Contribution margin - Fixed costs.

The Reinvestment rate was determined from the fundamental growth equation where Growth = Return X Reinvestment rate.

Return = after-tax operating profit / total capital employed.

The total capital employed was derived based on capital turnover ratio.

Value of equity = Value of firm + Cash - Debt - Minority interests.

Table 2 illustrates the calculation for PGTI.

Table 2: multi-stage valuation model (Author)

Notes to Table 2:

a) Straight-line reduction in the growth rate.

b) Starting revenue based on 2023. Pegged to the growth rate.

c) Assumed 2023 rate and there is no improvement.

d) Starting based on 2023 cost. Assumed growth at the terminal rate.

e) Revenue X Contribution Margin and after accounting for Fixed costs.

f) Starting based on 2023. Assumed no improvement.

g) Revenue X (Revenue/TCE) ratio. TCE = total capital employed.

h) Based on the growth equation.

i) EBIT(1-t) X (1 - Reinvestment rate).

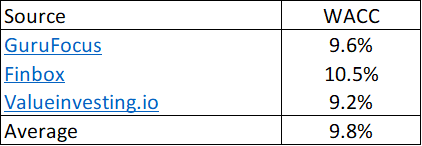

j) Refer to the WACC table.

Table 3: Estimating the WACC based on the first page results of a Google search for "PGTI WACC" (Various)

k) Terminal for the year / (WACC - 4%).

l) 5 years NPV + terminal value.

m) Inclusive of any excess TCE. Non-operating assets, MI, and Debt based on end Dec 2023.

The value of PGTI depended on the valuation model. If I had used a single-stage growth model, the intrinsic value would not go beyond USD 15 per share.

I was able to get a value that was more than Miter's offer price because of the multi-stage valuation model. But I had 2 key assumptions in this respect:

A 5-years reduction is a short one given its history of aggressive acquisitions. It is obvious that if it takes a longer period for the growth rate to be reduced, the intrinsic value would be higher.

Secondly, I could vary 2 key operating metrics in my multi-stage model - contribution margin and capital turnover ratio. I had shown earlier that PGTI was able to improve its contribution margins over the past 10 years. Also, its asset turnover (a proxy for capital turnover) declined.

A sensitivity analysis assuming a 10% improvement in contribution margin and a 10% reduction in capital turnover resulted in USD 87 intrinsic value.

The results of the above meant that you could take the USD 70 per share as a conservative one.

I would not consider PGTI a wonderful company. While it had gotten bigger in terms of revenue, profits and total assets, it was an asset-driven growth. Furthermore, it was driven more by acquisitions than organic growth.

The troubling point was that while it got bigger, there were no improvements in operating efficiencies. As such, over the past decade, there was a decline in the ROE and operating return.

The favorable thing (from Miter perspective) is that even without improvements in the operating efficiencies, there is a margin of safety compared to the offer price of USD 42 per share.

If Miter has the financial resources to support further acquisitions as well as management expertise to improve the operations, there would be upside for shareholders' value creation. It would thus be acquiring PGTI "cheaply".

What would you do if you were an existing shareholder of PGTI? The share price over the past 5 years before the offer (both by Masonite and Miter) could not even get to half my estimated intrinsic value. So, any offer at 60% of the intrinsic value looks good.

Rejecting the offer will mean a continuation of the same Board and management team that had not delivered the operating improvements.

Having said that, I must commend management for driving PGTI to such a size that it became an acquisition target. But on the downside, I suspect that it was a target because there seemed to be a lot of synergies that can be extracted.

If there was an alternative, a shareholder would be better to be paid for part cash and part share of Miter. Then he can still enjoy part of the upside post-acquisition.

I hope you can understand why I think the Miter offer is not good enough, as there is a good upside without even looking at operating improvements. The Board has left money on the table.

But in the absence of another offer, this is the best for shareholders. If the deal does not go through, I worry about management being able to deliver the USD 70 shareholders' value.

I am a long-term value investor and my analysis and valuation are based on this perspective. This is not an analysis for those hoping to make money over the next quarter or so.