Mark Wilson

Mark Wilson

With what has become an enjoyable annual tradition, I spent Saturday morning drinking coffee (in Florida this year!) and reading Berkshire Hathaway's (NYSE:BRK.A) (NYSE:BRK.B) 2023 Annual Report. After a heartfelt tribute to Charlie Munger, Warren Buffett went into his usual missives, this time centered around his younger sister Bertie, while describing Berkshire's 2023 Operating Performance.

While always entertaining, recent annual letters have been somewhat predictable in tone and outlook. This one struck me as different. His tone on some of Berkshire's largest businesses (BNSF and BHE) seemed far more sour than usual. Buffett also confirmed what I've been saying on here for the past few years, that it is nearly impossible for Berkshire to find value accretive acquisitions due to its now massive size.

There remain only a handful of companies in this country capable of truly moving the needle at Berkshire, and they have been endlessly picked over by us and by others. Some we can value; some we can’t. And, if we can, they have to be attractively priced. Outside the U.S., there are essentially no candidates that are meaningful options for capital deployment at Berkshire. All in all, we have no possibility of eye-popping performance.

I believe 2023 will be a high watermark for Berkshire's earnings for a long time.

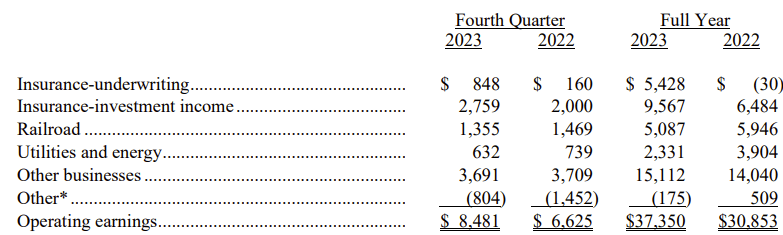

2023 operating earnings were up 21% from 2022, but the headline results are masking businesses that are not performing well.

Berkshire 2023 Operating Earnings (Berkshire Hathaway Website)

The strong results were more driven by circumstance outside of Berkshire's control: higher interest rates and higher insurance industry premiums. In fact, I had a hard time finding any businesses that were performing well outside the P&C Insurance Business (which is top notch.)

Most other businesses at Berkshire seem to be flatlining or going backwards, with many performing notably worse than competitors. (Note that "Other Businesses" above now includes Pilot; without that, it was only up 2% YoY.)

BNSF earnings dropped from $5.9 billion to $5.1 billion. As noted by Buffett in his letter, BNSF consistently spends more in CapEx than it has in Depreciation, so it generates less free cash flow for Berkshire to reinvest (on average $1.5 billion per year) than its stated earnings.

The entire rail industry had a tough start to 2023 with volumes down, but carloads gradually improved throughout the year. In Q4, BNSF carloads were up 4.2% YoY, yet profit still declined.

Buffett is honest in his assessment of why, namely wage pressures in a job that is tough and often dangerous. While he didn't call it out, it's worth noting that over 80% of BNSF employees are represented by a labor union, and labor unions across the country have been scoring big wins against employers lately.

Aside from the industry pressures, which I do not believe will get better anytime soon, Buffett also notes that BNSF profit margins have slipped relative to their competitors since Berkshire's purchase.

All is not well at BNSF, which earned less money in 2024 than it did in 2019 ($5.5 billion.)

Berkshire Hathaway Energy earnings dropped 40% year over year, primarily due to liabilities from wildfires. Buffett notes the regulatory environment of "fixed, reasonable return" for building complex power systems is in jeopardy. Buffett does not sound optimistic for future returns, ending the missive with:

I did not anticipate or even consider the adverse developments in regulatory returns and, along with Berkshire’s two partners at BHE, I made a costly mistake in not doing so.

This was not a confidence inspiring update for this business.

Berkshire's final price for Pilot was $13.6 billion over three purchases:

Pilot had net earnings of $603 million this year, for an earnings yield of 4.4%. I expect this number will be lower in future years.

Similar to crack spreads, gasoline station margins are significantly higher than pre-COVID, which I expect to moderate going forward. While I personally think EV penetration will disappoint many projections, it's almost certainly a long term negative catalyst for gas stations.

This was just a crazy number to pay for this business in 2023. I believe Berkshire was on the losing end of this deal.

The auto insurance industry posted record profits this year after a tough 2022. On the back of rate strength, GEICO swung from a $1.9 billion loss in 2022 to a $3.6 billion profit in 2023. Fantastic, right?

While the headline number is nice, digging in paints a less rosy picture.

GEICO lost 9.8% of its customers this year. While higher insurance rates drove much of the strength, underwriting expenses declined $752 million, much of which was lower advertising spend.

Buffett's bragging about GEICO's marketing budget and how he can't wait to spend more next year - a fixture of many past letters - is notably absent this year.

This is simply not a business that is being run well. Progressive (PGR) is eating their lunch with a 9% increase in policies and 22% increase in premium's earned, versus Berkshire's 9.8% loss/1% increase in premium's earned.

Auto insurance margins will normalize again, and probably quickly. But I doubt GEICO's customers are coming back.

Apple (AAPL), Berkshire's largest holding, barely got a mention, and had no discussion around it. I chalk this up to "if you can't say anything nice, don't say anything at all."

I think Apple is overvalued. My guess is, Buffett does too.

Yes, Berkshire has $167 billion in cash and treasuries. But it also has $128 billion in debt.

I'm not talking about insurance liabilities or other balance sheet liabilities. It has $128 billion in Notes Payable. Everyone knew that, right?

Buffett has trained the media well. Nearly every other company on the planet gets reported on net cash, but we report Berkshire's as gross cash.

Most of this debt is fixed at low rates, but some of it is maturing. Berkshire paid off $4.3 billion in 0.75% notes in 2023, rather than refinance them.

Often I see investors justifying Berkshire's valuation by subtracting out the value of the equity book and the treasury holdings, and assigning a multiple to the OpCo earnings, while just ignoring the debt entirely. I'm not sure that's the right treatment.

As a thought exercise, think of Berkshire's "second most successful" acquisition, and the "second most successful" major stock purchase since 2012.

The first question is very hard, because I don't think any major acquisition in the past 12 years has been good. I believe Berkshire vastly overpaid for Kraft Heinz (KHC), Precision Castparts, and Pilot. Some smaller tuck-in's may be OK, but Berkshire doesn't break out their results.

Ok, now stock. We all know the Berkshire/Apple story. It's the one investment that has made Berkshire's performance in the past decade okay instead of terrible.

So what's the second best equity investment Berkshire has made in a 12-year span that's had the S&P 500 triple? Probably the five Japanese companies, an $8 billion (as in, less than 1% of the current market cap) pre-tax winner.

Nothing else I can think of in over a decade.

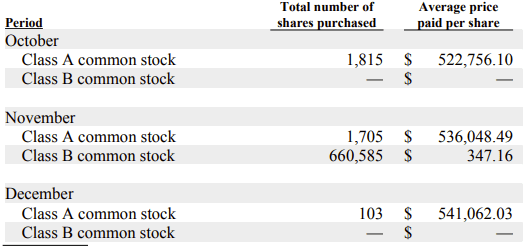

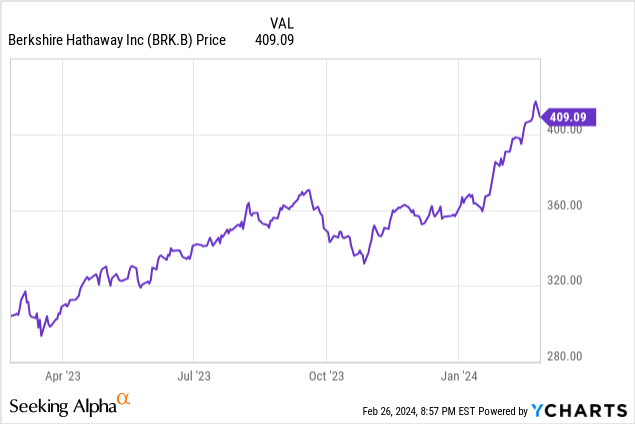

Berkshire only repurchased $2.2 billion in Q4-23 quarter, at an average price around $350. With the cash pile at record levels, I believe the tepid repurchases in Q4 reveal Berkshire's view on the Q4 valuation versus staying in Treasuries.

Berkshire Q4 Repurchases (Berkshire 2023 10-K)

The current price is ~17% higher than it was in Q4.

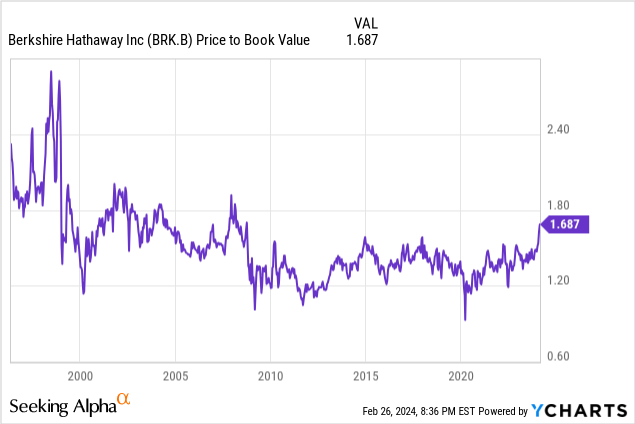

Price to Book Value is currently at levels not seen since well before the GFC, when Berkshire was 1/4 of the size and Buffett was 15 years younger. Some may argue that this is no longer relevant; I disagree, especially in light of the future challenges for the wholly owned businesses.

Thinking like an owner, Berkshire's current $900 billion valuation buys you:

The last thing I wanted to do was sell Berkshire and write a big tax check to various governments. Actually, that's the second to last thing I wanted to do. The last thing I want to do is give back a significant portion of a big gain, and I think that's a likely outcome from here.

I can deal with a stretched valuation. I can deal with some structural business headwinds. But the combination of both usually leads to capital loss.

Conglomerates usually trade at a discount for good reasons, and I believe Berkshire's "extreme decentralization" model is showing some large cracks.

Do we think GEICO would be better run as a standalone company with a focused CEO and Board of Directors? Todd Combs is currently the CEO of GEICO to go along with his portfolio management responsibilities. His last experience in the insurance world was as a pricing analyst for Progressive in 2002. As a standalone company, do we think the market would have forced change here by now?

I believe that we were approaching a full valuation at $350, and don't see anything that justifies the recent run from $350 at the start of the year to $425 where I sold Monday morning. I think it is likely Berkshire's earnings and share price go backwards from here.

I hope to be a Berkshire shareholder again in the future, but the margin of safety isn't here for me right now.