jetcityimage

jetcityimage

I've dedicated the last 5 years of my life to growing a dedicated dividend portfolio. Over that time, I've managed to grow my dividend income to a sizeable amount that I can now use to pay bills, buy groceries, or even fund portions of trips. These days I find myself gravitating to higher-yielding asset classes such as REITs (real estate investment trusts) or BDCs (business development companies). However, this is because I spent the majority of my early years establishing positions in solid blue-chip-rated companies that I believe deserved to be core positions.

Procter & Gamble

Procter & Gamble (NYSE:PG) has been a solid staple in my dividend growth portfolio for the last 5 years now. I have consistently added on dips and continue to drip the dividend. My thought process was to first prioritize companies that were known to be "sure things". While in practicality, nothing is a sure thing, I based my methodology on finding companies with a consistently long track record of success. PG was one of those companies due to the resilience through all economic cycles, the consistent dividend increases, and a portfolio of products so diverse that almost everyone one in their home.

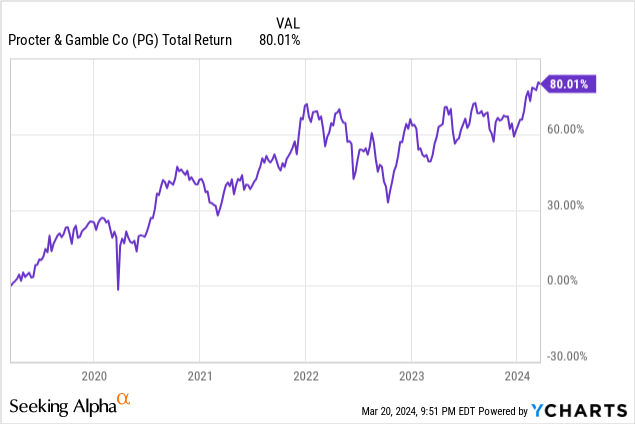

We can see that the price has appreciated by more than 80% over the last 5-year period. However, as we approach an all-time high the question is now whether or not PG is a buy. In short, although the company remains a solid dividend payer I believe that short-term headwinds caused by a decrease in product volume are likely to cause the price to come down as growth slows. Consumer shifts are contributing to lower sales volume. Prices are being increased to offset this but I don't think I will add more to my position until the price comes back down from this high.

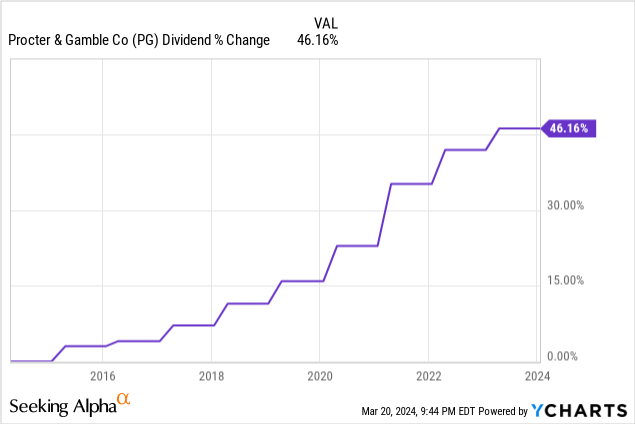

As of the latest declared quarterly dividend of $0.9407/share, the current dividend yield is 2.3%. PG has been an excellent dividend growth stock over the last few decades. PG has reached the milestone of Dividend King, which means that they have increased their dividend for over 50 consecutive years. More precisely, PG has increased its dividend for a whopping 67 consecutive years. There are currently only 54 other companies that have reached this incredible milestone.

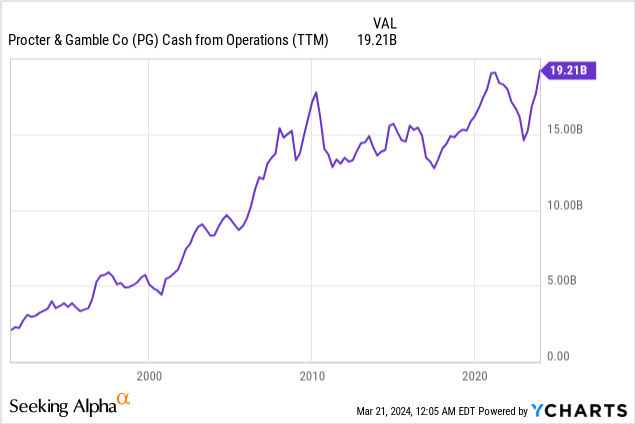

As you can see, the dividend has grown by a total of 46% since 2014. Over this ten-year span, the dividend grew at a CAGR (compound annual growth rate) of 4.57%. Even on a smaller time horizon of five years, the dividend grew at a CAGR of 5.58% compared to the sector median of 5.24%. In my opinion, the dividend has room for continued growth as the payout ratio sits at 58%. Not to mention, the current payout ratio of 58% sits below the 5-year average payout ratio of 61.32%. We can also see how cash from operations has consistently grown over time throughout different market cycles.

All other metrics seem to reinforce that the dividend growth is at no threat. Revenue growth has averaged about 3.75% over the last 5-year period. Additionally, PG has a net income margin of 17.6% and cash from operations totaling $19.21B. Lastly, the interest on their debt is at a healthy level with an interest coverage ratio of 22.37 compared to the sector median interest coverage ratio of only 7.02.

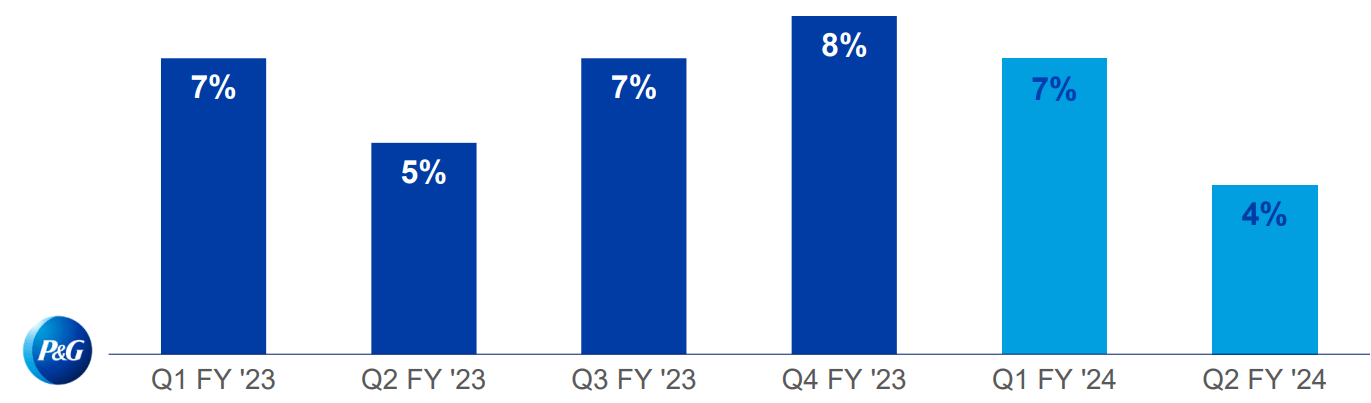

As a quick breakdown, PG's growth can be measured within five different segments of their business. Those segments and their respective growth numbers as of the latest earnings report are as follows:

Over the Q2 earnings as a whole, organic sales growth averaged 4%. Core EPS (earnings per share) growth averaged 16% over the prior year while organic volume growth shrunk by -1%. We can that this quarter's sale growth was lighter than the last 5 quarters.

PG Q2 Presentation

While volume seems to be the cause of the decrease here, management has actively tried to offset this by implementing price increases. While this serves as a short-term solution, I wouldn't bet on it being a sustainable practice in an environment where consumers are being more money-conscious with their purchases.

However, overall growth still seemed to continue because of these price increases across North America, Europe, and Latin America. The growth across different regions of the globe was shared on the earnings call.

Organic sales in North America grew 5% with four points of volume growth. Europe focused markets were up 7% with three points of volume growth. As expected, both regions saw a step down in pricing contribution to sales growth as a large portion of price increases from last year have annualized. Latin America delivered another very strong quarter with 17% organic sales growth, continued strong results in these regions.

There are some targeted issues affecting other markets. Greater China organic sales were down minus 15% versus prior year. Underlying market growth was down mid to high single digits as consumer confidence weakened further. The SK-II brand in Greater China was down 34% due to soft market conditions and a temporary headwind for Japanese brands in the market. - Andre Schulten, CFO

The rising cost of groceries and necessities during shopping has taken a toll on most people. Several studies have shown us that the majority of people are opting for store-brand items over national brands such as PG. In fact, 54% of shoppers say they'll choose the store-branded items. This comes as no surprise with the rise of most shopping categories.

US Bureau Of Labor

With the extreme levels of inflation we saw in 2022, consumers likely already become accustomed to shifting their dollars toward cheaper alternatives. The decision affects a lot of the different product categories that PG operates within. For example, why grab the $20 Tide laundry detergent when the store-brand alternative costs $12 and cleans your laundry just as well? Why buy the PG-owned Gillette razors when the store brand is just as efficient? You can make this exact decision throughout an entire store and this is exactly what large bulks of people started doing as costs increased.

My thought is that once inflation cools and interest rates come down a bit, it's a possibility to think that consumers will shift back into their old habits of buying national brands like PG. In fact, this problem isn't really unique to PG as some peers experiencing a similar decrease in volume due to the same thing.

Parallel companies like Hormel (HRL), Kimberly-Clark (KMB) and General Mills (GIS) are losing marketshare to the store brand. I wrote a separate analysis for all the mentioned companies: Hormel, Kimberly-Clark, and General Mills if you're interested in checking those out. On the other end of the spectrum, we have companies like Kroger (KR) that have benefitted from the consumer shift since they have the logistics and manufacturing sources to do so.

Procter & Gamble

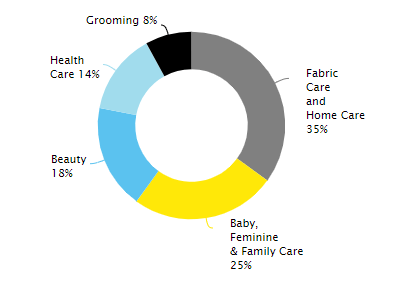

Thankfully, the revenue PG receives from each segment is diverse in weighing. The largest portfolio of their income comes from the fabric care and home care segment at 35%. This is followed by baby, feminine & family care at 25%. Additionally, approximately 50% of their net sales come from the North American market while the second largest portion of net sales come from Europe at 21%. Therefore, I believe that revenue streams are diverse enough to ride out any future headwinds if this consumer shift continues to lean toward store-branded alternatives.

In terms of valuation, PG does seem a bit expensive at the moment. For reference, the average Wall St. price target sits at $169/share. This represents a modest upside of only 4.3%. The price targets range from as low as $138/share to as high as $180/share. However, Seeking Alpha grades PG a D- in terms of valuation. I tend to agree with this based on a few different metrics.

For example, the current P/E (price-to-earnings) ratio sits at 25.86x in comparison to the sector median P/E of only 18.26x. PG's average price-to-earnings ratio over the last 5-year period has been 24.60x. Therefore, the current P/E can be referenced to show that PG currently sits at a bit of a premium valuation after the recent price run-up. In addition, PG also currently trades at a price/book ratio of 7.98 in comparison to the 5-year average of 7.28.

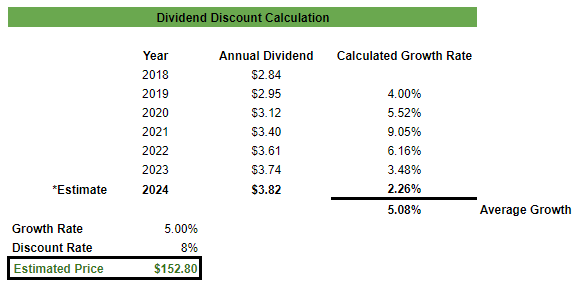

Running a Dividend Discount Calculation also shows us that PG trades at a premium to an estimated fair value of $152.80/share. As a result, I decided to continue to reinvest my dividends only and will not be deploying additional capital until the price retracts a bit.

Author DDM

In their last earnings call, management stated that they intend to continue returning value to shareholders by allocating more than $9 billion towards dividends and initiating $5B - $6B towards share repurchases throughout 2024. We shall see if this holds the price levels at the premium it currently trades at.

If the consumer shift to store-brand products becomes the norm, PG will have to continue to offset this loss of volume with further price increases. However, increasing prices can also result in even more customers shifting to cheaper alternatives. Unlike companies such as Kroger that can benefit from this shift in buying, PG has to ride out the wave or innovate a new product that is affordable. PG also is still vulnerable to other market cycles such as continued high inflation or a recession. We could enter another cycle where inflation begins to rise once again and sales volume continues to suffer. On a positive note, interest rates are anticipated to be cut in the latter half of 2024. This could have a positive effect on consumer spending and benefit PG.

Although Procter & Gamble is a world-class dividend king, I believe that the price currently trades at a premium to fair value based on the current valuation metrics. After all, the stock sits near an all-time high. Even though I do not plan on deploying additional capital into my PG position, I plan to continue reinvesting the dividend as I believe future raises are still likely. The dividend payout ratio currently sits below its 5-year average and dividend growth has averaged 5.58% over the same time period.

The headwinds faced can be attributed to the consumer shift in spending. Due to higher inflation, increased interest rates, and a rising cost of living, consumers seem to be more willing to buy store-brand alternatives. Therefore, sales volume has decreased in certain business segments. However, this issue isn't unique to PG as similar peer companies like Kimber Clark have faced the same headwind. Time will present a better entry opportunity so I plan to hold for now.