SlavkoSereda/iStock via Getty Images

SlavkoSereda/iStock via Getty Images

In this report, I will spend more time on the semi-annual reports and valuations more than anything else. In summation, the funds have a lot of moving parts with some relying on the at the market offering to issue new shares and bring in new capital in order to make up the shortfall between earnings and the distributions. Others have to rely on capital gains.

Valuations across the board are rich, and I've lightened up across the board and even gotten out of several funds. PHK and PFN are my favorites here, and I've sold most or all shares of PAXS, PDO, PCN, and PDI.

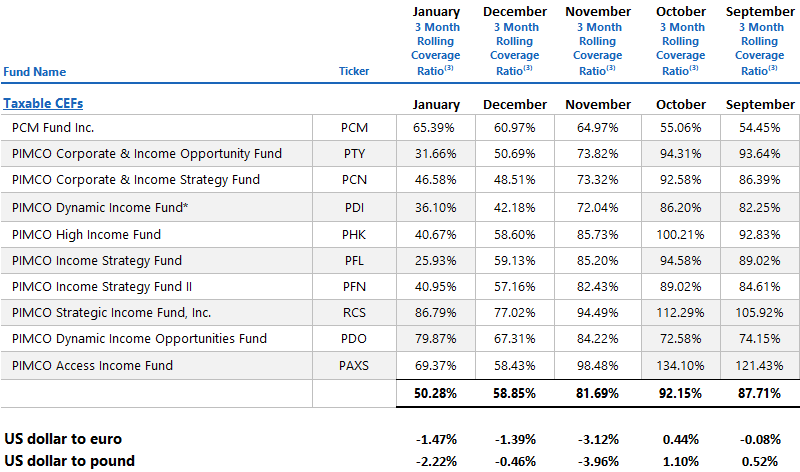

In January, coverage levels for the taxable funds fell, on average, going from 58% to 50%. The dollar was one of the main culprits here, as it had a moderate decline against both the euro (-1.5%) and the pound (-2.2%).

Coverage for a few funds like PIMCO Income Strategy (PFL) and PIMCO Corp & Inc (PTY), and PIMCO Dynamic Inc (PDI) are downright awful. Those ratios are down to 25%, 31% and 36%, respectively. PFL, for instance, has fallen from 95% in October to that 25% figure in January. That's a dramatic fall.

PIMCO, AGC

What's the driver of that?

The primary one is likely the dollar. This is simply a mark-to-market of the currency forward contracts that hedge the foreign bond holdings in the portfolios. As the U.S. dollar falls, those get repriced each day but the underlying bonds may not trade for many days, weeks or longer creating a mismatch in value change.

The funds are fairly neutrally positioned on rates but their secular outlook suggests that they think rates will fall over the coming months and quarters. Instead, they are focused on special situation investment within corporate credit and residential mortgages.

Additionally, they are cautiously entering the commercial mortgage market given the massive disruption that is occurring in that sector. Emerging markets have been the largest detractor to the primary taxable closed-end funds, or CEFs, as that trade has failed to work and PIMCO has been high on it for a couple of years.

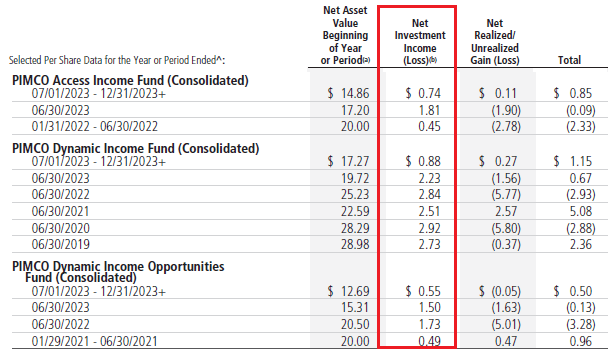

Net investment income ("NII") production has been in decline for several years now.

I have highlighted below three funds' NII production. For PDI, that production has been in decline since 2020 when it peaked at $2.92 per share for the fiscal year (ending 6/30). Last year, fiscal 2023, NII per share was $2.23, or down about 23% since that peak year in 2020.

PIMCO

Remember, PDIs distribution is set at $0.2205 per month or $2.65 per year. In other words, since 2021, the fund has not earned "income" over the distribution.

Now there are other factors that can make up the difference including gains on swaps or certain securities. In addition, PDI has an at-the-market offering ("ATM") which we described in detail a few months ago in our update.

Essentially, so long as PDI shares trade at a premium to NAV, they can issue new shares and "earn" the distribution. However, as I noted in that report, should the premium of the shares go away, they could be in trouble.

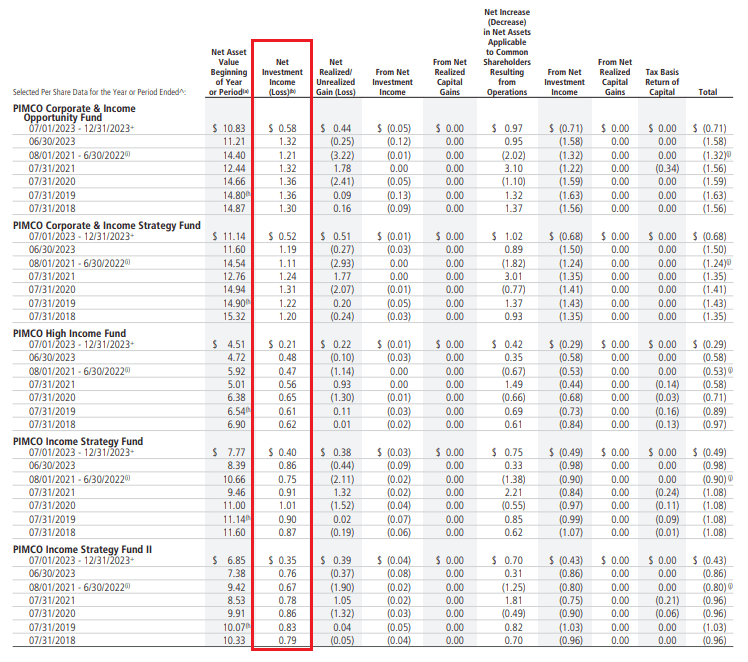

Here are the other five funds (PTY, PCN, PHK, PFL, and PFN):

pimco

There are no funds that are up over the prior three-year period. The funds with the worst decline in NII are PDI, RCS, PDO, and PCM. The funds down the least are PFN, PFL, PTY, and PCN.

The funds are overdistributing relative to their payouts which means that the NAVs are being dragged down. The issue is that credit spreads are really tight here. The NAVs on the taxable funds are going to be driven by those spreads since these funds are now, in large part, credit vehicles.

That means that it will be hard to make up that shortfall between fund earnings and fund distributions by rising asset values.

Does that mean that they will have to cut the distribution? Not necessarily since they can make up the shortfall with sales of new shares.

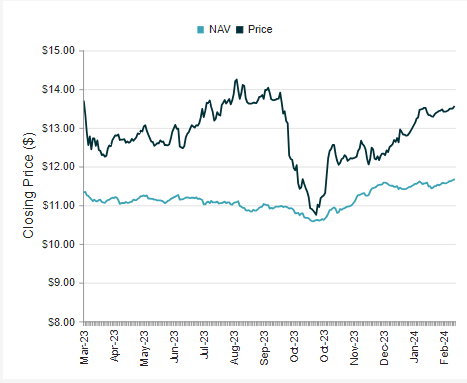

For instance, looking at PTY to start with. In the six months ending December 31st, the fund generated $83.5m in net investment income, had a net realized loss on assets (capital gain/loss) of $82m, and a net unrealized gain of $148m.

Distributions totaled $103.3m which means that they didn't cover the yield from earnings on the holdings in the portfolio. However, their ATM transactions totaled $103.4m which, alone, covered the distributions.

Page 22 of their semi-annual report details the formula that calculates the overall change in net assets. I have said for a long time that the NAV holds all the information.

The formula is [net investment income + net realized gain + net change in unrealized asset price - distributions + ATM offering] = net change in total assets.

Alpha Gen Capital

The takeaway from above is the following:

Overall, you have to at least remain in balance, or, over time, your NAV will be in permanent decline. It can be out of whack for a little while and fall, but eventually, it needs to be rectified or you risk heading into a downward spiral where assets continue to fall, forcing a reduction in leverage, and increasing the over-distributing environment, which exacerbates the problem further and further.

The valuations have changed quite a bit over the last nine months going from expensive too cheap to expensive again. Right now, the overall valuations are quite elevated as these funds can rally along with an equity market rally. The current risk-on environment is likely causing some exuberance in the CEF market which is why the overall taxable bond CEF space is more expensive than it has been in a couple of years.

Right now all of the funds are overvalued relative to our fair value estimate. However, some are extremely overvalued and some are modestly so. The best options today if one wants to add are PIMCO Income Strategy (PFL), PIMCO Income Strategy II (PFN), and PIMCO High Income (PHK).

For those that are buy and hold, I wouldn't make much of any moves. PIMCO Dynamic Income (PDI) remains overvalued but well within its normal valuation range. I would say that if the premium were to rise above 16%, then even the most ardent buy-and-holders should consider a swap or sell. If you want to add, I would wait until that premium deflates at least 5 points from here to a premium of 6%, or less.

The large position I had in PIMCO Corp & Income Strategy (PCN) is mostly gone now with the price blowing through my dream sell limit orders. The premium is now back above 16%, a few points above our fair value, and continues to rise. If it hits 20%, I will likely blow out my remaining shares but those that are tactical should consider taking some gains off the table. This one is up $2.5 in the last 5 months. Not a bad return.

CEFConnect

PIMCO High Income (PHK) is the closest to fair value. PHK and PFN are my two largest PIMCO positions and I'm largely out of my prior largest positions - PDI, PCN, and PDO. I like the NAV performance recently and the price has oscillated up and down quite a bit over the last few months allowing me to leg into my position as I sold down PCN and PDI.

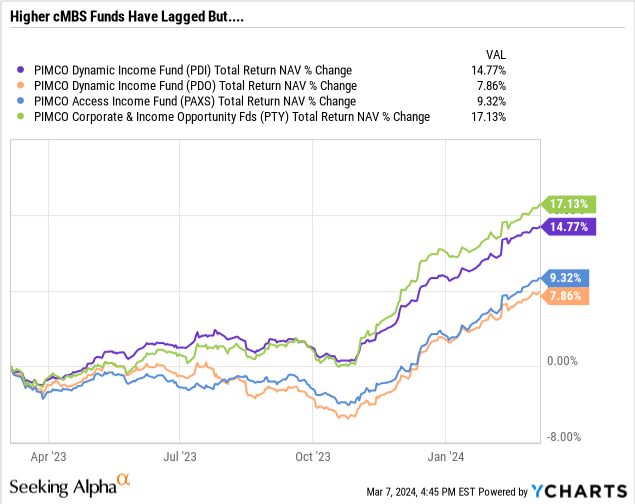

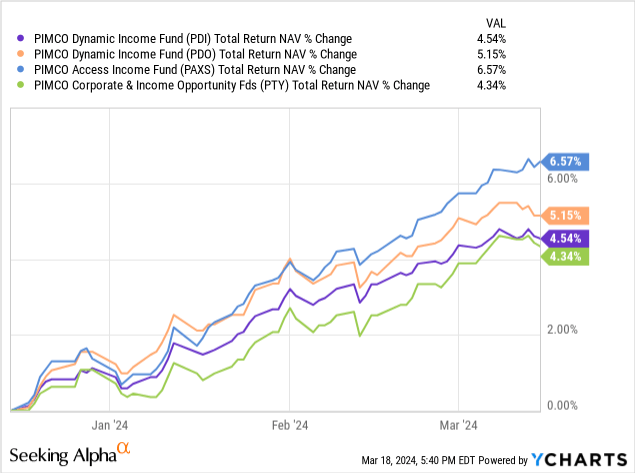

PAXS and PDO, the newer funds, which have more cMBS (commercial mortgages) in them than the others, have lagged over the last year thanks to those allocations weighing down the fund.

But PAXS and PDO have made up ground recently.

yCharts

Overall, the funds are expensive so the tactical CEF investor should be looking at trimming and selling more than they should be buying. Swaps typically only make sense if the fund they are swapping is cheap, not just cheaper.

Today, there are no cheap funds, but that hasn't stopped me from adding some PHK. This was solely because I see no other value in the rest of the taxable bond CEF sector as a whole, and PHK, the fund I have bought in the last month, remains close to fair value, just not under it where I prefer to buy shares.