Dragon Claws

Dragon Claws

Written by Nick Ackerman.

Business development companies have been performing quite well for the last several years. This was thanks to a higher rate environment and the Fed raising rates at the fastest pace in decades. Further, defaults and bankruptcies remained relatively lower than historical averages. Defaults have been ticking up, and some business development companies, or BDCs, have been having a more difficult time than others. That said, the U.S. economy has remained incredibly resilient despite the much higher rate environment.

While rates are expected to go lower sometime in 2024 based on Fed and market expectations - which aren't exactly on the same page just yet on the exact number - BDCs can still perform well going forward. The environment won't likely be as favorable, and we could see a ticker lower in net investment income generation than many BDCs can produce.

A weaker economy also remains a risk overall in the space. BDCs often lend to small or mid-sized businesses that aren't necessarily the most financially stable. They can be more susceptible to economic conditions. They then employ leverage in an effort to boost performance and income generation. With that being said, rates aren't expected to go back to zero, barring another black swan event. That's especially true with inflation still running hotter and the economy remaining so resilient with a strong labor market.

The main reason why BDCs can perform so well, is because they often lend at floating rates while borrowing at fixed rates. One of those more "basic" BDCs is PennantPark Floating Rate Capital (NYSE:PFLT), though, with relatively higher exposure to floating rate borrowings, the fund hasn't done probably as well on the income-generation front. We'll discuss that a bit more below.

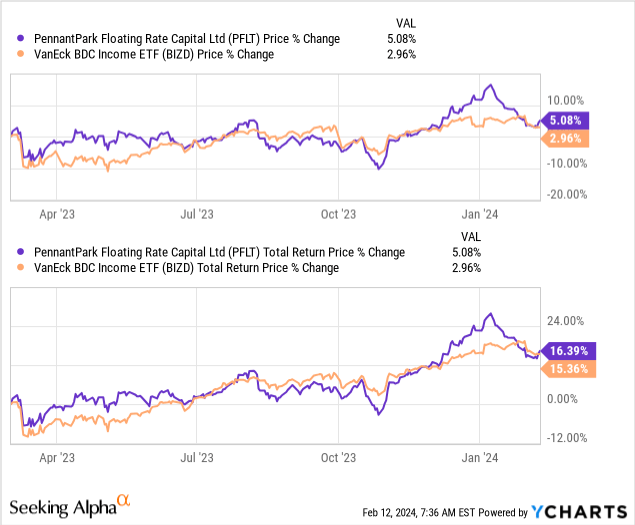

This is a name that we haven't touched on since last year but has been delivering attractive results and income through this period. It was around that time that I had picked up a position in this name. Since that article, PFLT has been able to outperform the VanEck BDC Income ETF (BIZD) by a touch.

Ycharts

BIZD is a passive ETF that is designed to track the MVIS U.S. Business Development Companies Index. PFLT last represented around 1.4% of this ETF.

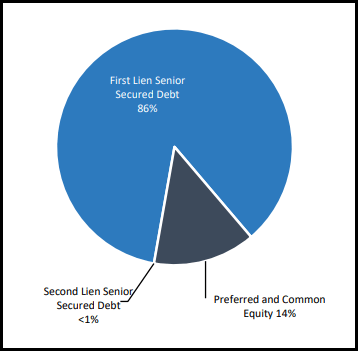

PFLT targets a diversified portfolio "primarily of floating rate loans by generally targeting an investment size of $5 million to $30 million in securities, on average, of middle-market companies." The floating rates they invest in are primarily first-lien senior secured, which represents 86% of their portfolio as of the last breakdown available. They then have 14% comprised of preferred and common equity investments.

PFLT Asset Breakdown (PennantPark)

To increase managed assets, they utilize several different forms of leverage. They have a credit facility that pays based on SOFR plus 236 basis points. The total borrowings here are a limit of $386 million, but at the end of their latest quarter end, December 31, 2023, they had $260.9 million outstanding.

The borrowings here took quite a step up from the prior quarter. Unlike the calendar, the fiscal year-end for PFLT is September. At that time, debt to equity came to 0.76x, but the larger borrowings on this facility brought their debt to equity up to 1.03x to end their Q1. That's still below the Q2 2023 level they have listed at 1.17x.

They then have another $185 million in notes, paying a rate of 4.25%. These are due April 2026, but for right now, this is part of their fixed-rate borrowing sleeve that has been beneficial in the rising rate environment. For comparison, the average borrowings of their credit facility discussed came to 7.7%.

Finally, they also have asset-backed debt. These are through several different tranches, all on their own terms. Primarily, all of them are based on SOFR plus a spread, but there is a smaller one, Class C-2 at $8 million, that pays at a fixed rate. In total, that accounts for another $228 million with a weighted average interest rate of 7.2%.

That does leave PFLT at a bit of a disadvantage when compared to some other BDCs that have utilized more fixed rates in their leverage. In this case, around $480.9 million of the total $673.9 million in borrowings, as of their latest quarterly report, is exposed to floating rates. Said another way, that's roughly 71% of their borrowing capacity.

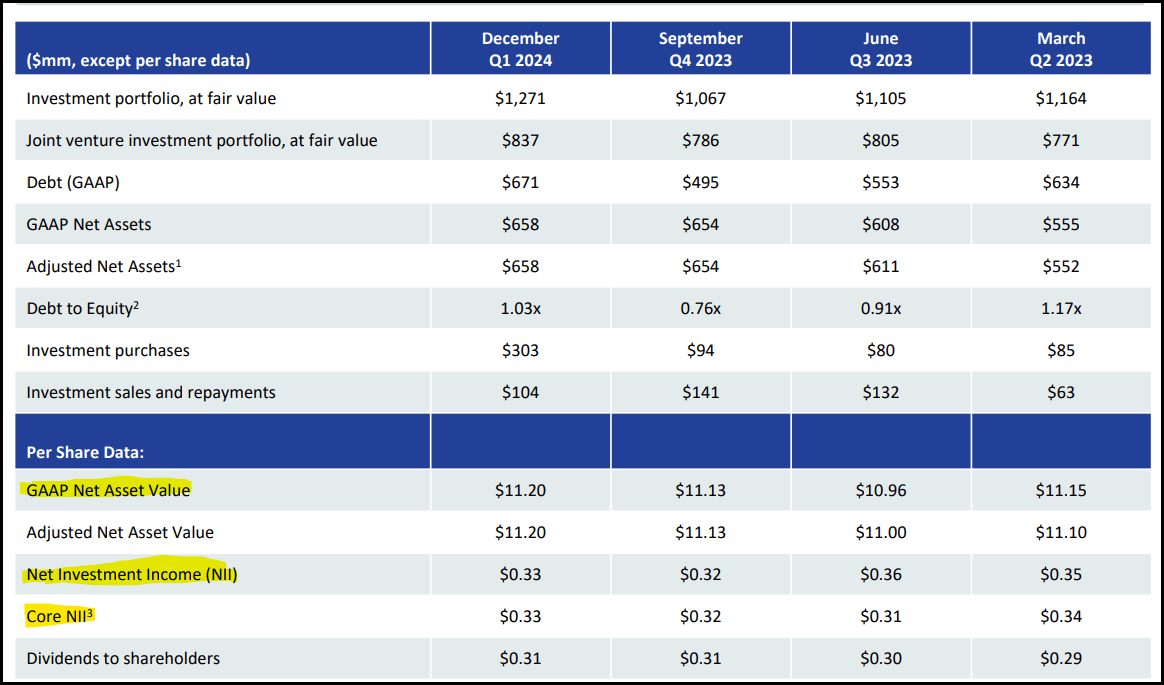

With the changes in debt utilization and given the higher exposure to floating rate debt, it has meant that PFLT didn't necessarily participate as some other BDCs had in terms of providing higher income generation through this period. In fact, the net investment income as of their latest presentation is nearly flat. That's whether we look at the NII or the Core NII that the management team presents.

PFLT NII and Core NII (PennantPark)

On a positive note, the fund's net asset value has also remained essentially flat through this last year as well. Of course, during this time, they also bumped up the dividend to investors twice, which was another positive.

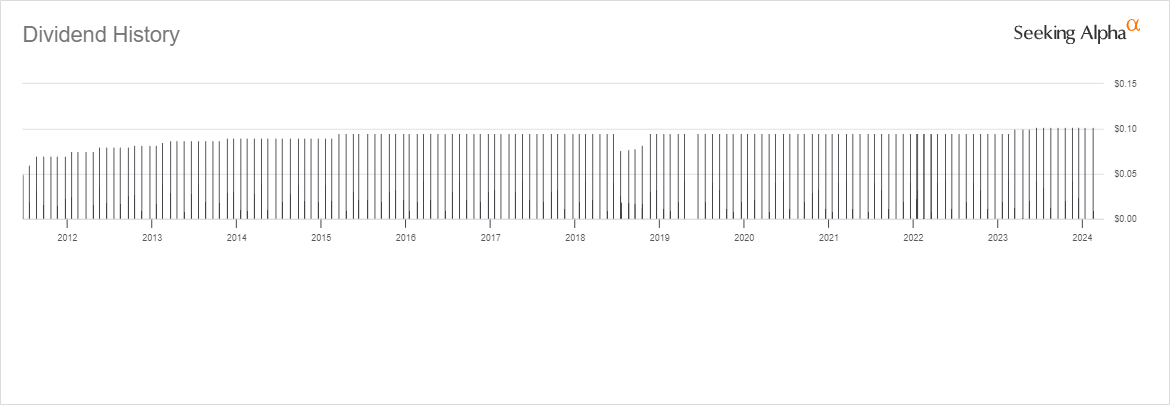

For a number of years, they had paid $0.095 per month, which they took up to an even $0.10 and then $0.1025. Given the latest NII, we can see that dividend coverage comes to over 107%. A nearly 11% dividend yield is certainly nothing to complain about.

The NAV's stability is thanks to the management team, which has shown a rather strong track record of avoiding losing bets. They only have 1 company on non-accrual status out of the 141. That works out to 0.1% of the portfolio cost and 0% at fair market value.

In fact, they went on to mention in their latest earnings call that they've invested in "481 companies, and we have experienced only 18 nonaccruals" since their inception 13 years ago. It also noted that it was over $5.6 billion in invested capital over that period.

I think that's quite a feat, given that PFLT tends to run a more diversified portfolio. Some BDCs take the more concentrated route, running with 20 to 30 companies that they can really get to know. PFLT might make investments across 141 companies, but they've clearly shown a solid track record. Higher diversification can also be a positive in that one or two companies that become nonperforming won't wreak too much havoc across the entire portfolio. Things can stay relatively stable, and that is reflected by the latest non-accrual that worked out to only 0.1% of the portfolio cost.

Going back to the rate discussion, the impact of their fixed and floating rate leverage relative to their portfolio is quite important at this time. BDCs have been performing well due to primarily the higher rate environment benefiting their interest income while seeing historically low defaults. Now, with rates looking to head lower in the next year or two, the forward outlook might not look as rosy. That doesn't mean that investments in BDCs aren't still worthwhile, but it is something to be cognizant of.

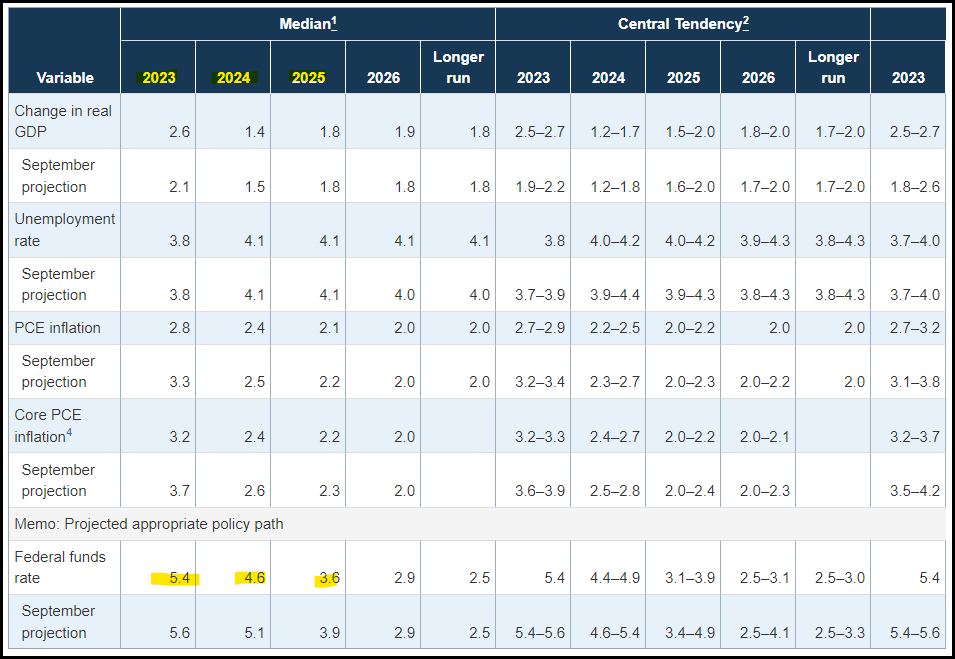

The latest projection from the Fed was that 2024 would see rates cut three times for 25 basis points each. Going out to 2025, rates are expected to come down even further. We'll get the new projection material with the next Fed meeting in March. Given that inflation remains above the Fed's target as well and the unemployment rate is not rising yet, that could have some implications.

Fed Projections (Fed)

In the case of PFLT, we can see that the implications of a stronger economy and higher inflation are positive, as it should translate into fewer potential rate cuts.

Still, cuts are expected, even if it isn't looking like the Fed will need to cut as aggressively. The outcome for PFLT is still listed as a negative hit on income. They have outlined how they could theoretically be impacted, given their current portfolio. This is listed in their latest quarterly filing, showing the impact of a change in interest rates.

PFLT Interest Rate Change Impact (PennantPark)

Rates going down by 1% could have a $0.11 cent impact, and that is expected to happen over the next two years. Again, based on the latest projections, rates could come down nearly 200 basis points.

On the other hand, even though it seems unlikely, an increase in rates could have a positive impact on PFLT. If the economy continues to perform well and inflation once again starts rising, it certainly could be possible. That's mostly what we saw in the last couple of years.

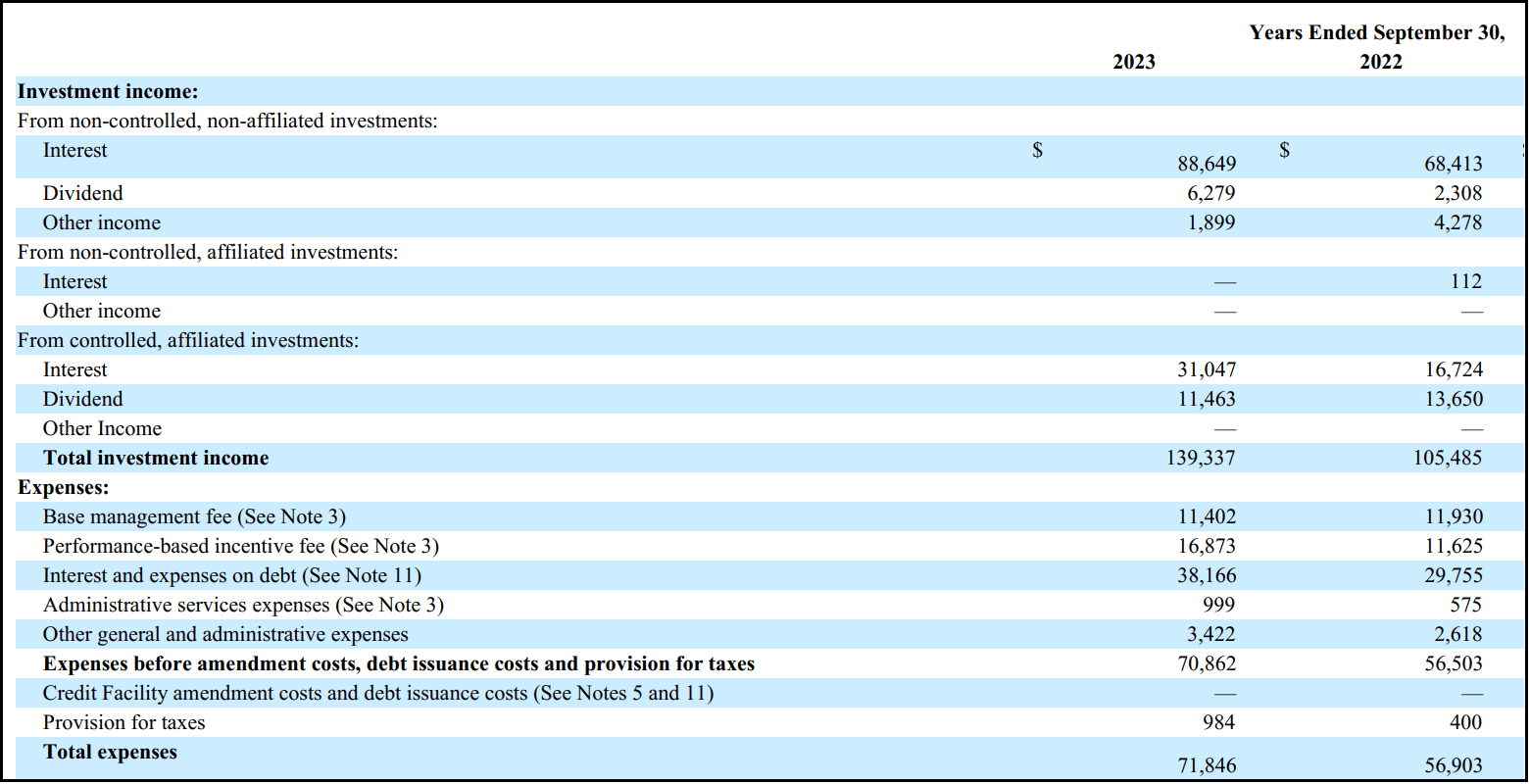

Fiscal 2023 saw total investment income reach $139.337 million. That was up from the $105.485 million in FY 2022. However, expenses also rose from $56.903 million to $71.846 million. That ~26.3% increase in expenses came primarily as a result of interest on their borrowings increasing. Performance-based incentive fees also had risen year-over-year.

PFLT Annual Report (PennantPark)

The end result was still positive NII year-over-year. Even if the last rolling 4 quarters have seen NII remain relatively static. For the last FY, NII per share worked out to $1.33, up from the $1.18. The current annualized dividend from PFLT comes out to $1.23.

As we noted above on the last quarterly NII figure, coverage was quite solid. This also indicates that coverage was quite solid at 108%. That's important because it leaves some room for those rate cuts to come before coverage gets too pressured. PFLT had been able to consistently deliver a monthly dividend that they've never had to cut.

I believe they are probably hoping to keep that track record alive.

PFLT Dividend History (Seeking Alpha)

PennantPark Floating Rate Capital has been able to benefit from a higher-rate environment. They've been able to perform well against their BDC peers despite having some relatively higher exposure to leverage based on floating rates. It wasn't anything that their underlying portfolio of primarily floating rate exposure wasn't able to offset, and we saw TII and NII rise over the last couple of years.

The outlook is for the expectation that rates are going to come down sometime in the next year or two. That would have a negative impact on PFLT in terms of the income generation ability of its portfolio. Still, the dividend coverage has some wiggle room here. I believe that barring rates being cut too aggressively on the back of a black swan event, the current monthly dividend should be rather safe.

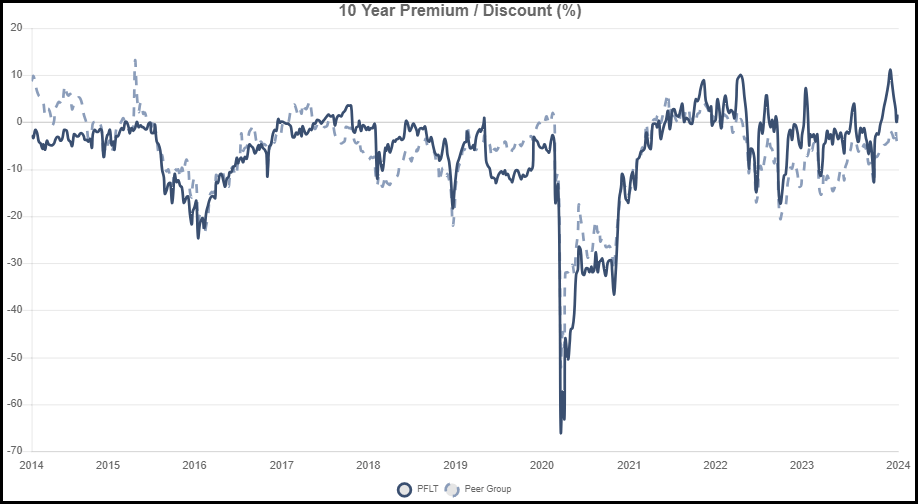

The shares began to trade at a sharp premium more recently, but after coming back down some, we are at near parity with the NAV per share last reported. PFLT can often be picked up at a discount to its NAV if history is any guide.

PFLT Discount/Premium History (CEFData)

That could mean that PennantPark Floating Rate Capital is around fair value. Though it isn't necessarily the most richly priced, either. A long-term investor could choose a dollar-cost average approach to leg into a position while waiting for a better bargain.