Nastco

Nastco

The purpose of this article is to evaluate the PIMCO Income Strategy Fund (NYSE:PFL) as an investment option at its current market price. PFL is a closed-end fund whose investment objective is to "seek high current income, consistent with the preservation of capital".

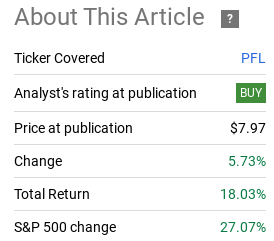

I wrote about PFL roughly a year ago when I had a favorable outlook for the fund. I thought high yield was going to get a broad boost and I saw some underlying value in this particular CEF. In hindsight, I was spot-on in that assessment as the fund has performed quite well since that time:

Fund Performance (Seeking Alpha)

While it is always fun to take a victory lap when calls turn out well, what is more important here is to decide if it still makes sense to buy PFL at these levels. Whenever I see run-ups in the 20% range, that triggers an automatic reassessment for any investment idea. That doesn't mean automatically sell (or change my tune), but it does mean to re-evaluate whether or not what once was a good buy should still remain one.

With this in mind, I have a more moderate stance on PFL today. The recent gain will be hard pressed to continue given the fund's premium to NAV, poor income metrics, and general headwinds surrounding high yield credit. Therefore, I am shifting my rating to "hold", and I will explain why below.

The first point to touch on is a quick one. As my followers know, valuation is always critical for me when considering any fund. This is true of equities as well, but especially when I look at CEFs because of the wild premiums (and discounts) some can trade at.

With respect to PFL, at this time last year the fund was trading near par value. I saw multiple supporting factors for why I thought this fund was poised to rise and the valuation did not concern me. Today, that story has shifted a bit, with PFL now sitting with a premium to NAV above 4%:

Quick Stats (PIMCO)

The fact is this is not "cheap", but it isn't really "expensive" either. While I don't love a 4% premium, to be fair it is not at an alarming level. So there isn't any need to be overly concerned if one already has a position. I certainly wouldn't sell it on this basis alone.

But for those considering new positions or buying for the first time, that case is harder to make. A premium to NAV is tough to justify, especially when so many options exist at discounts. With PFL's valuation getting a bit stretched, I see merit to getting more cautious and believe this supports my downgrade to "hold".

The next topic is one that has me scratching my head a bit. This relates to income production, with February figures coming out from PIMCO over the past week. In the case of PFL, these metrics are quite alarming to say the least:

Income Metrics (PIMCO)

As you can see, the fund continues to have a negative UNII balance and the coverage ratios are indicating a lot of income pressure. This is concerning and will need to be monitored extremely closely in the months ahead.

To be fair, I won't put too much stock in these numbers and wouldn't base buy or sell decisions on a PIMCO CEF based on one month's worth of data. These numbers can (and often do) swing wildly from month to month. So it is likely PFL is actually performing a bit better than meets the eye, especially given its distribution history.

Even still, it would be hard for me to come out and say this fund is still a buy with this headwind over it. Until I see some improvement, a "hold" call on this one will be my take - at a minimum. Simply put, this is a strong supporting factor for getting more cautious at these levels.

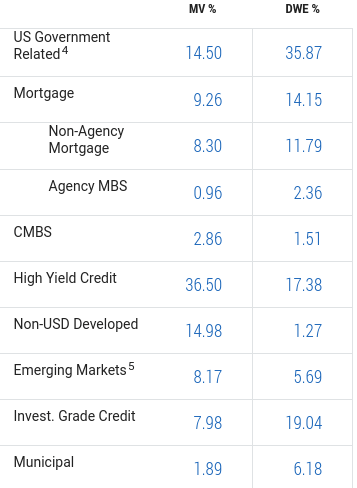

I will now shift to the underlying holdings of PFL. As followers of the fund surely are away, this is a big bet on high yield credit. A point of note, however, is that PFL is getting less reliant on this sector over time. During my 2023 review, this sector made up almost 43% of total fund assets. Today, high yield accounts for just over 36%, as shown below:

PFL's Holdings (PIMCO)

Now this is not inherently a bad thing. It depends on what exposure an investor is looking for, what their risk tolerance is, and what their own unique outlook is for this sector. Nobody knows for sure what the future holds, so whether or not high yield credit is right for you is truly a subjective decision.

Even still, it is important to understand what one owns. I have heard people refer to PIMCO CEFs as "black boxes" and that PIMCO "knows what they are doing" and thus they do not pay much attention to what is actually in the fund they own. This is not prudent investment management in my view, and followers of PFL need to understand this fund skews towards being a very risk-on play. It has been this way for a long time and continues to be one today.

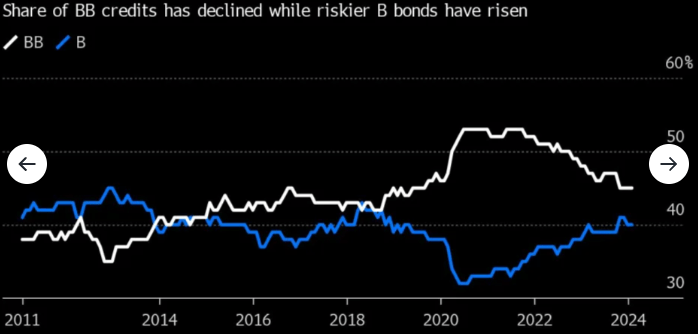

With that said, why am I concerned? One reason is that the high yield market continues to get riskier. What I mean is, the lower rated bonds and loans that make up the sector are becoming more dominant in the broader high yield index. For example, over time the percentage of BB-rated debt has come down, while B-rated (which is of lower quality) has gone up:

Make-Up of High Yield Market (Global) (Bloomberg)

My takeaway here is again not one of alarm. This is a trend that has been going on for a few years now and things have gotten along just fine. In fact, lower rated issues are actually out-performing since 2023, so perhaps this is the type of exposure investors want. But regardless, it should be understood by followers of PFL - or the broader high yield sector as a whole - that this is an area that is riskier than it used to be.

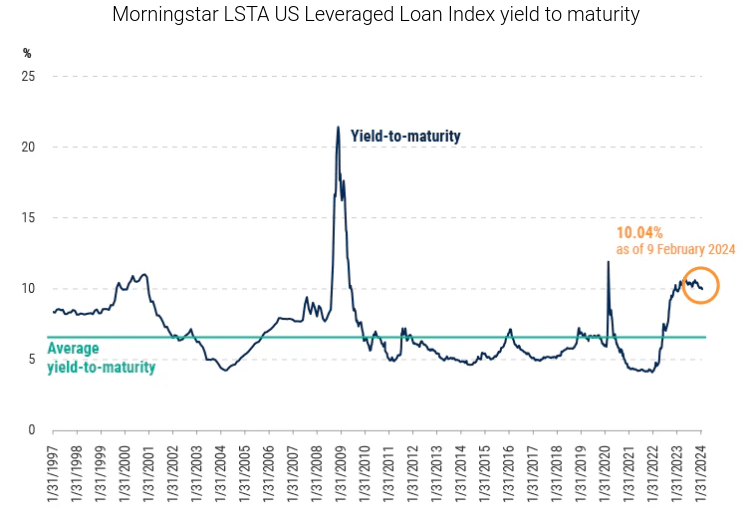

But here the story is not all bad. As mentioned, I am not a "bear" on this sector or PFL by extension. And there are legitimate reasons for this. One is that as the risk profile has been elevated, so too has the broader sector's yield. Let us look to the leveraged loan market (which makes up a good chunk of PFL's exposure) as an example. While yields have backed off their recent highs, they are still above their longer term average:

Leveraged Loan Yield Curve (US) (Morningstar)

What this shows me is that with risk comes reward. Investors are taking on a lot of risk here to be sure. While some may feel it is excessive, the fact is they are being paid for it. Yields are up - and they need to be given the Fed's risk-free rate and inflation figures - but they are up all the same. This is something income-oriented investors are surely happy about and it is helping PFL maintain its double-digit payout.

I bring this up to help balance out the review. Sure, PFL has some flaws and risk. But there is potential for more gains too. The recent year has showed how well this fund can perform in the right environment and there is no guarantee that will suddenly stop. So weigh the good with the bad in any analysis.

My final thought takes a look at how the USD has been performing and why this continues to be a thorn in the side of international (non-US) bonds and debt. When interest (or dividends) are paid in a local currency to US investors, they must then be converted into USD here at home. This means that currency fluctuations are an important consideration for bond and loan buyers in the US when they branch out overseas. As with all things investing, this comes with the potential for gains - but also losses.

But wait, you may ask - what does this have to do with an American fund like PFL? Well, the answer is that PFL does not just hold American assets. As the holdings chart (shown above) illustrated, there is emerging market and developed market debt in this fund. In fact, non-US holdings account for roughly one-quarter of total fund assets - not a small amount!

Similar to the junk debt discussion, this is not an inherently bad thing. But the strength of the USD is pressuring this type of asset for US investors. Those payouts in local currency are worth less when the USD is appreciating, and it has done so over the past couple of years. This extends to PFL's distribution because if the interest it earns is worth less in USD, then maintaining that USD payout to investors in the fund gets harder.

The challenge in 2024 is that the Fed has kept rates high and is not expected to make any major movements this year. While markets were predicting (or perhaps just hoping) for aggressive rate cuts as early as last summer, they have not materialized and the Fed reinforced its more hawkish message this afternoon (3/20).

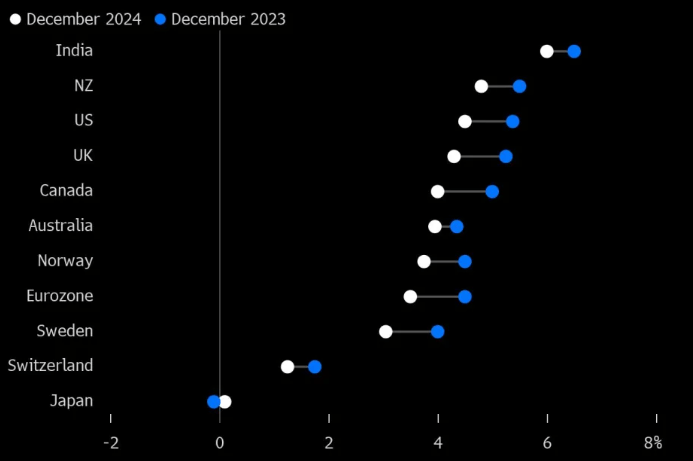

The practical implication is that other central banks are likely to be more aggressive, or at least on-par, with the Federal Reserve. This will maintain strength in the USD and continue to challenge non-US debt holdings. For specifics, look at where the benchmark US rate is set to finish 2024 compared with other major global economies:

Central Bank Policy Rates (And Projections) (By Country) (Yahoo Finance)

The conclusion I draw from this is that US-denominated debt will remain in favor for me in 2024 - at the expense of non-US debt. With PFL's heavy inclusion of overseas debt, I will have to pass on it for the time being. Of course, the benefit of diversification is a perk, but it isn't one that I really want exposure to in the short-term.

PFL really delivered since my last article on it (a year ago) and this momentum is certainly a welcomed sign for holders of the fund. Looking ahead, I think it is more likely this CEF will market-perform, as opposed to out-perform. The premium, weak income metrics, and reliance on non-US holdings are all factors that present challenges for PFL going forward. As a result, I believe a downgrade to "hold" makes sense, and I would caution my readers to be very selective with any entry points at this time.