SDI Productions/E+ via Getty Images

SDI Productions/E+ via Getty Images

Back in July of last year, I was on the hunt for some attractive players in the banking sector. This was because of a crash that was caused in March of that same year that was driven by the failure of multiple institutions. My bargain hunting led me to one firm appropriately named Preferred Bank (NASDAQ:PFBC). What made the enterprise interesting to me, besides the fact that shares were attractively priced, was the fact that it had a very specific emphasis on serving the Chinese American market. This emphasis had proven beneficial for the company in prior years, allowing it to grow. Eventually, I ended up rating the company a ‘buy’ to reflect my view at the time that shares would likely outperform the broader market for the foreseeable future.

It's important to note that any kind of upside should be considered positive in and of itself. Then, if the goal was to see the company outperform the broader market, I call so far has fallen short. Since the publication of that article, shares have seen upside of 9.6%. That's a bit below the 10.5% rise seen by the S&P 500 over the same window of time. Despite this underperformance, revenue and profits for the institution have been positive. Despite experiencing some weakness earlier in the year from a deposit perspective, the overall trend on that front has been mostly positive. And while shares are expensive relative to their book value, they are cheap relative to earnings and the institution has proven itself to be a quality operator. Given these factors, I’ve decided to keep the company rated a ‘buy’ for now.

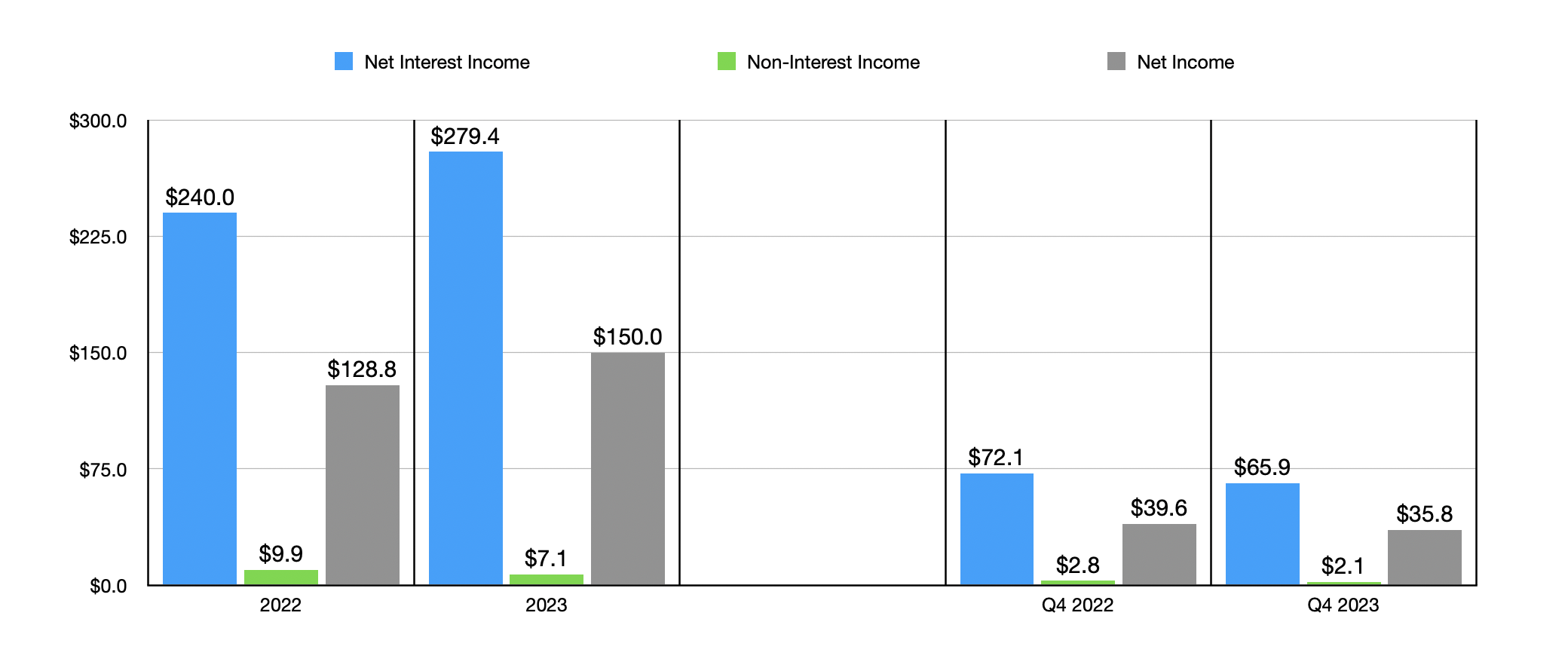

When I last wrote about Preferred Bank, we only had data covering through the first half of the 2023 fiscal year. Today, data now extends through the rest of that year. By pretty much every measure, 2023 ended up being a rather positive time for the company. As an example, we need only look at certain income statement items. In the chart below, you can see revenue and profits for the bank. Net interest income came in strong at $279.4 million. That's 16.4% above the $240 million generated one year earlier. In addition to benefiting from a continued expansion of its balance sheet, the institution also enjoyed a rise in its net interest margin from 4.09% to 4.49%.

Author - SEC EDGAR Data

There were, of course, other areas that the income statement to pay attention to. One weakness that the institution reported involved its non-interest income. This dipped from $9.9 million down to $7.1 million. But that didn't stop net income from shooting up nicely from $128.8 million to $150 million. As the aforementioned chart shows, there was a bit of weakness in the final quarter of the year. A drop in both net interest income and non-interest income pushed net profits down year over year. Much of that pain was driven by a contraction in the company's net interest margin from 4.75% to 4.24%. Only time will tell if this is a blip on the radar or a sign of something more problematic. But for now, the broader picture looks nice.

Author - SEC EDGAR Data

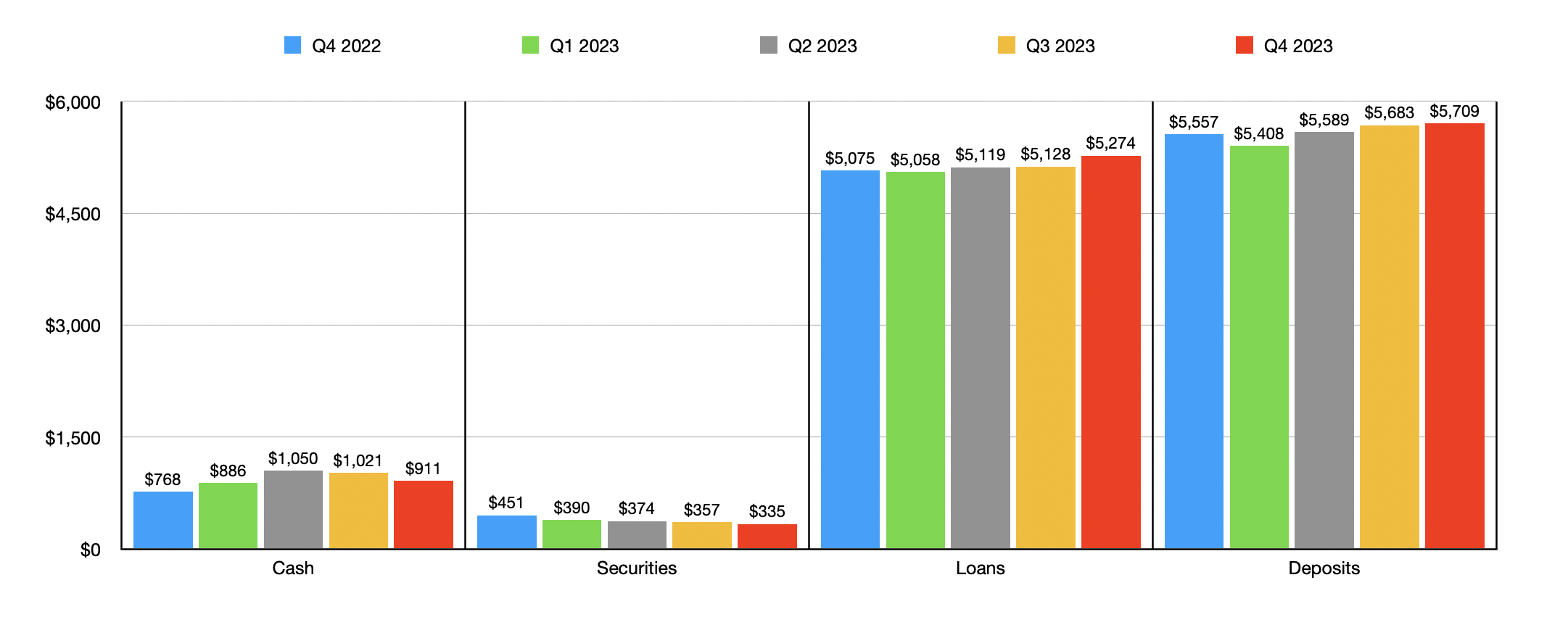

The overall improvement in top line and bottom line performance for 2023 was driven by a continued growth of the enterprise. As an example, let's start off with deposits. These ended the 2023 fiscal year at $5.71 billion. That's up from the $5.56 billion that the company had at the end of 2022. And it's a decent improvement over the $5.41 billion that the institution had at the end of the first quarter of 2023 as the banking crisis was spreading. Over this same window of time, the value of loans that the bank has also increased. It had just under $5 billion worth at the end of 2022. But by the end of 2023, loan values had grown to $5.27 billion.

Author - SEC EDGAR Data

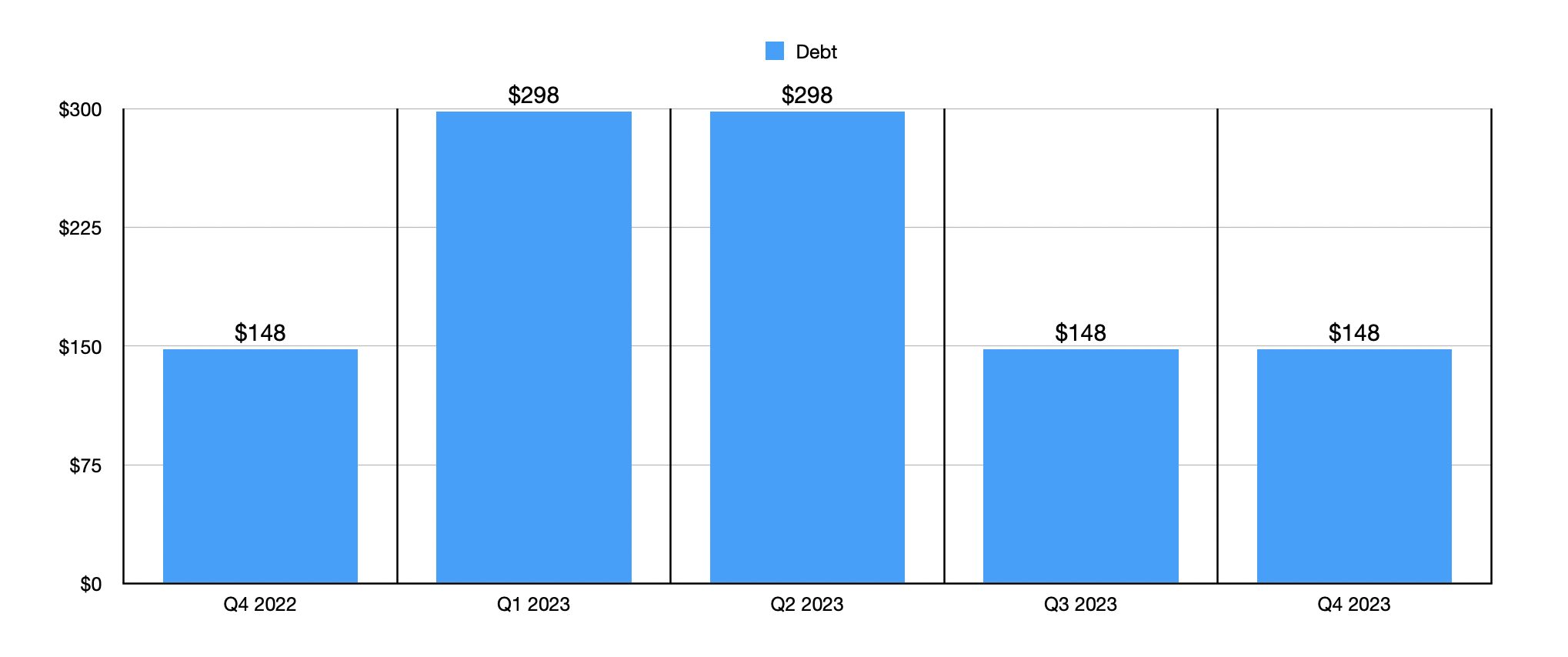

Another important balance sheet item would be the securities that the institution owns. Unlike the deposits and loans on its books, securities actually fell quarter after quarter from the end of 2022 through the end of 2023. During this window of time, they dropped from $450.8 million to $335 million. Securities often help widen the net interest margin. So that helps to explain some of the weakness toward the end of the year. Cash, meanwhile, grew from $767.5 million to $910.9 million. This also has the negative side effect of impairing the net interest margin in most cases. The good news is that management could easily use this cash to pay off debt if it were so inclined. After rising from $148 million in 2022 to $298.1 million during the earlier part of 2023, the value of debt managed to pull back down to $148.2 million by the end of last year.

Author - SEC EDGAR Data

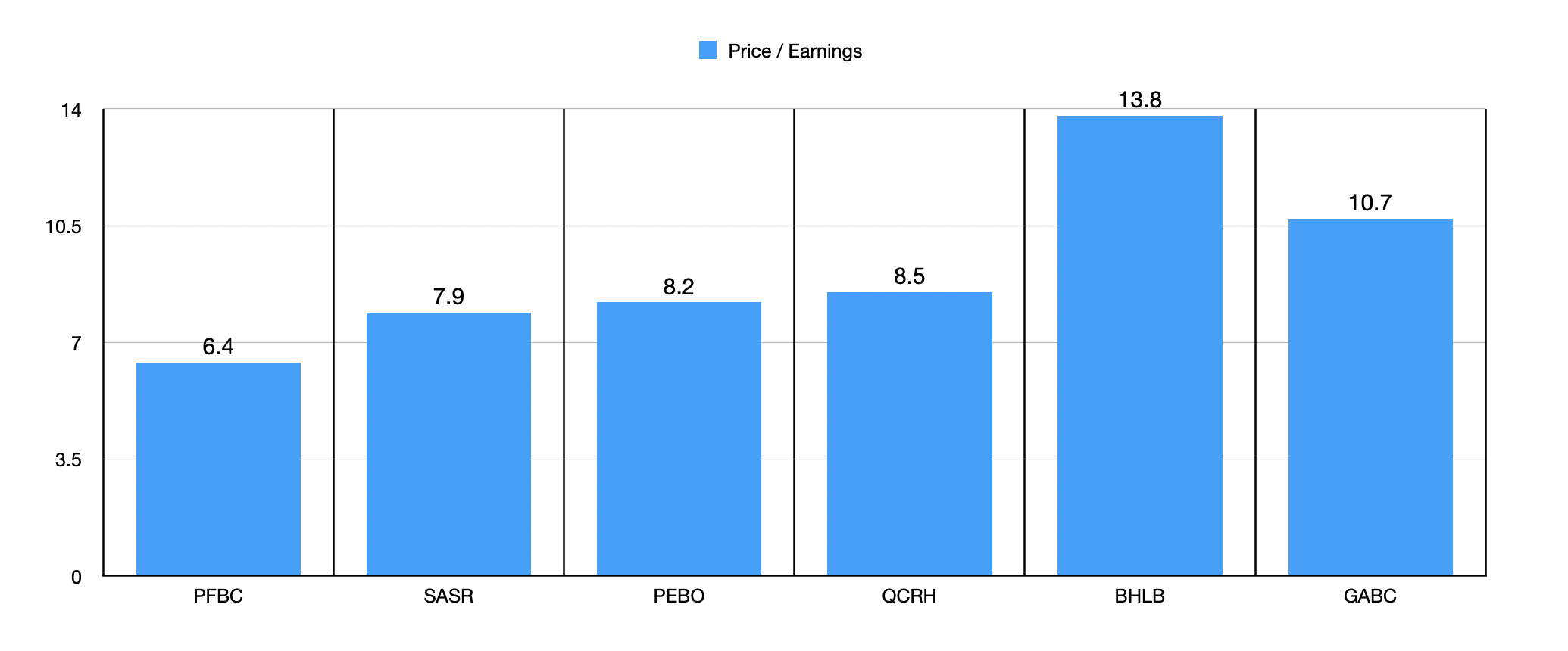

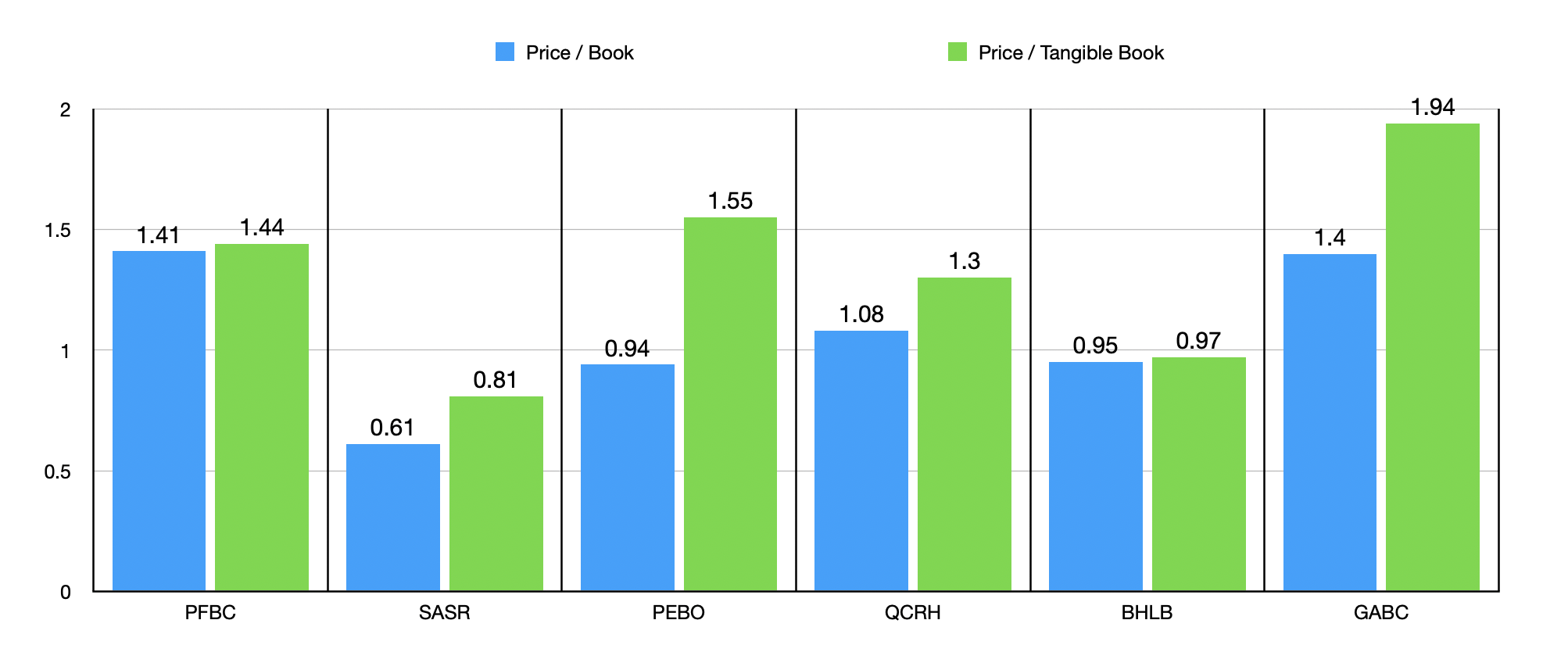

In terms of valuing the bank, there are a few different ways that we can do this. First and foremost would be using the price to earnings approach. Using the data from 2023, Preferred Bank is trading at a price to earnings multiple of 6.4. That's toward the lower end of the spectrum from what I have seen over the past year or so. In the chart above, you can see how the price earnings multiple of the bank stacks up against five similar firms. Undoubtedly, Preferred Bank is the cheapest of the group. In the table below, meanwhile, you can see how shares are priced using the price to book approach and the price to tangible book approach. In this case, instead of being the cheapest of the group, Preferred Bank is one of the more expensive. Using the price to book approach, our prospect is the most expensive of the group. And when it comes to the price to tangible book multiple, only two of the five companies was more expensive than it.

Author - SEC EDGAR Data

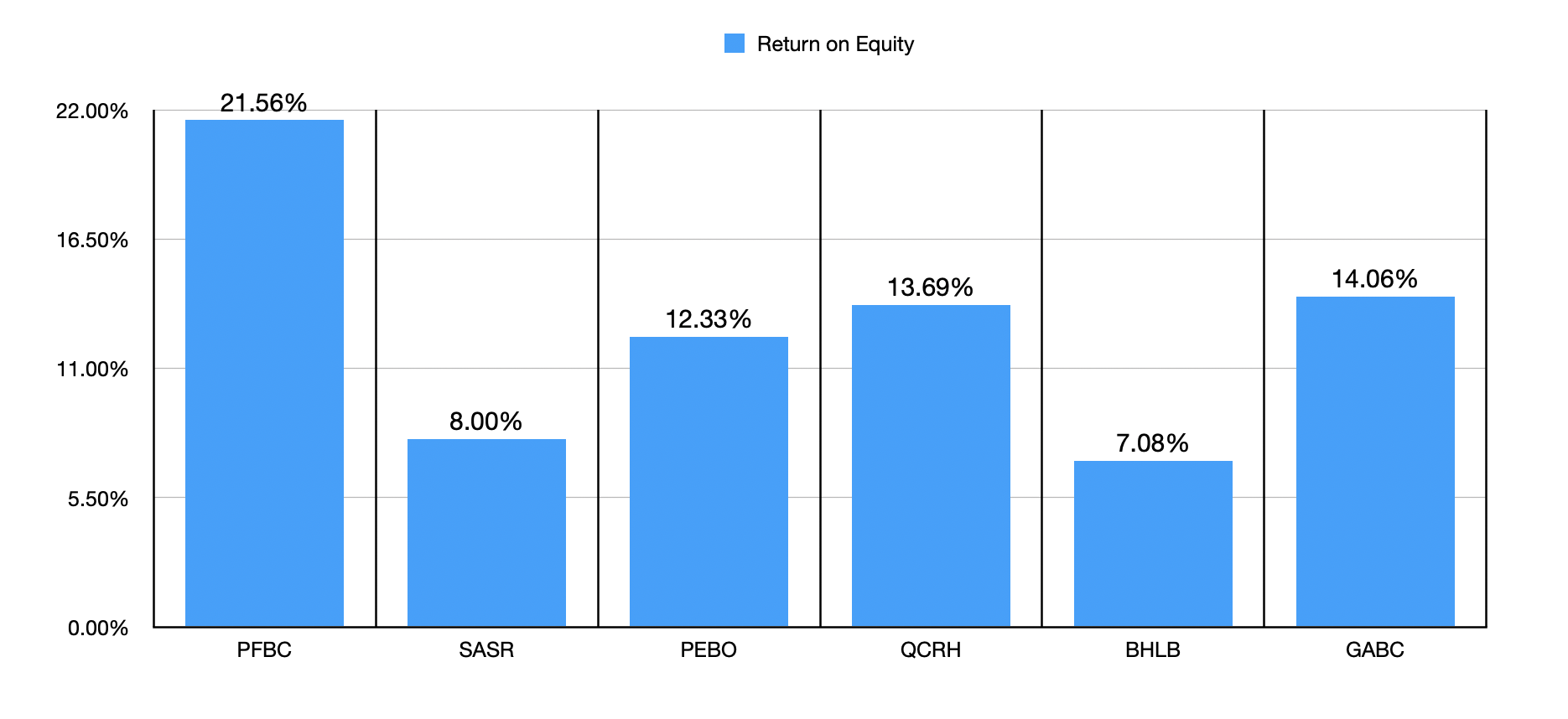

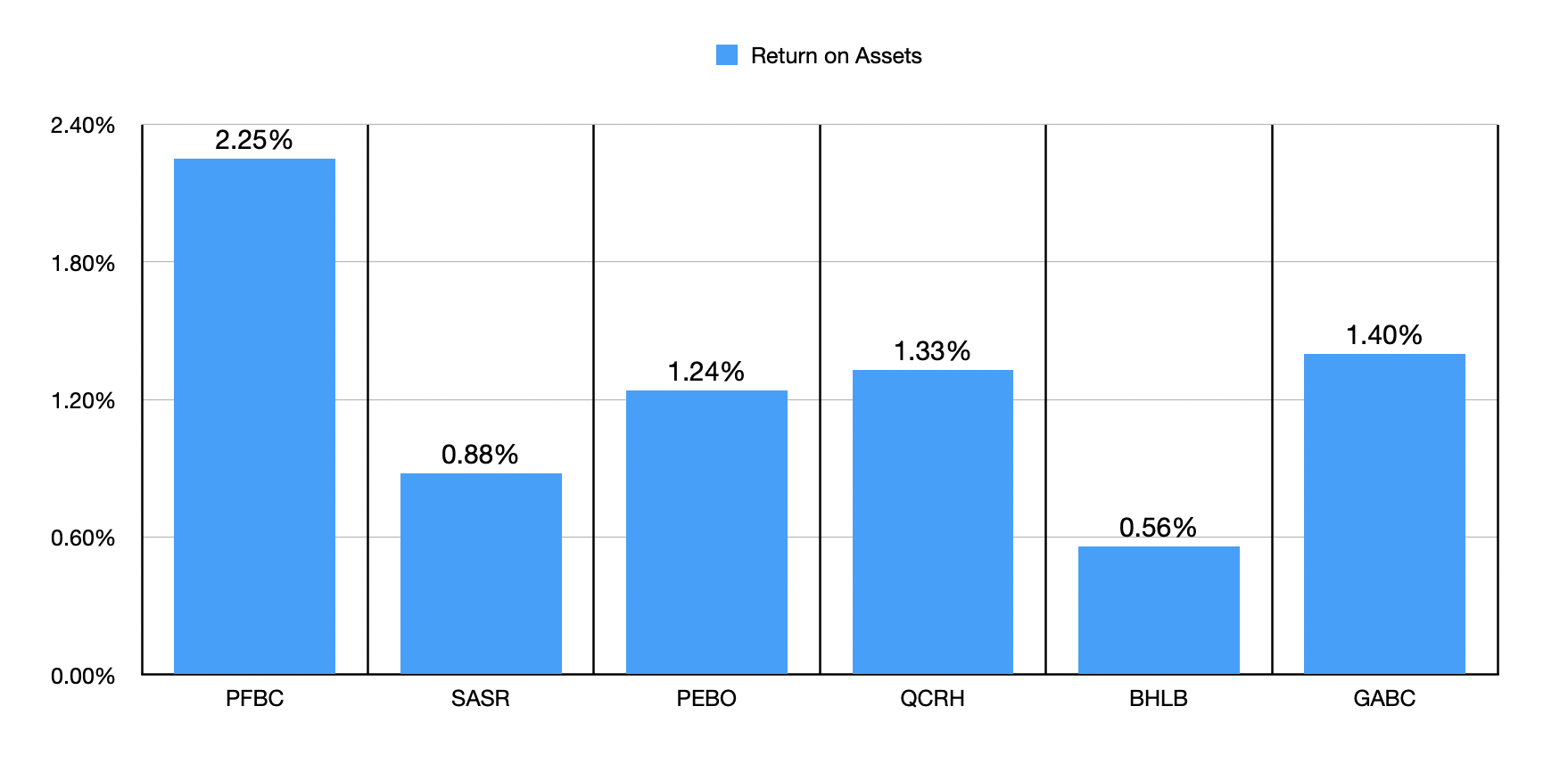

From a valuation perspective, we clearly have a bank that is rather mixed. It's cheap relative to earnings, and it's expensive relative to book value. Relative to tangible book value, it's close to the middle of the pack. To see which direction our sentiment should go, the next thing we need to do is see the quality of the earnings the institution generates. I did this using two different approaches. In the first chart below, you can see the return on equity, not only for Preferred Bank, but also for these same five companies I compared it to already. With a return on equity of 21.56%, it's at the top of the list. And in the chart below that, you can see the other method, which is the return on assets. Once again, Preferred Bank looks to be at the high end of the spectrum.

Author - SEC EDGAR Data

Author - SEC EDGAR Data

To be clear, Preferred Bank is not a prime prospect. There are many ways in which the institution looks positive, and there are some ways in which it looks negative. Pricing is confusing because of how much it jumps around from one metric to the other relative to similar firms. But on the whole, the bank continues to expand and the quality of its assets is undeniable. At the end of the day, the good outweighs the bad to me, and that led me to keep the company rated a ‘buy’ for now. If the price to book value of the business were lower and/or recent revenue and earnings had come in stronger, I would certainly upgrade the stock. It's close to the point of deserving an upgrade, but not quite.