stockstudioX

stockstudioX

I should first say that if you're expecting another 10% to 14% yielding PIMCO CEF, which is sort of the norm for their multi-sector credit/bond funds, then you might be disappointed to learn that the PIMCO Dynamic Income Strategy fund (NYSE:PDX), $20.41 closing market price, only yields a current +6.6%.

And that's after PIMCO raised PDX's distribution twice in the same declaration earlier this month in this press release. But before you write off PDX due to its pedestrian market yield, you might want to learn a little history on the best performing CEF over the last few years and why PDX has probably not seen its last distribution increase.

Over the next month or so, PDX should continue to transform its portfolio from a mostly energy and energy MLP equity fund to a multi-sector bond and credit fund while retaining a 25% or so allocation in energy investments.

I'll get more into that below but the important takeaway is that PDX will soon become the newest member of the PIMCO multi-sector bond CEF club, which includes some of the most popular CEFs for income investors.

That includes the PIMCO Corporate & Income Opportunity fund (PTY), $14.50 closing market price, the PIMCO High Income fund (PHK), $4.92 closing market price, the PIMCO Dynamic Income fund (PDI), $19.01 closing market price, the PIMCO Corporate & Income Strategy fund (PCN), $13.67 closing market price, the PIMCO Income Strategy II fund (PFN), $7.26 closing market price and the newest PIMCO fund, the PIMCO Dynamic Income Opportunities fund (PDO), $12.80 closing market price.

Now I specifically wrote out each PIMCO fund above, its ticker symbol and closing market price as of March 15, 2024, because if you're a PIMCO shareholder of one of these popular funds, there's a good chance you are a shareholder of another one or maybe all of them.

That's how popular the PIMCO name is in bonds. Now I don't know how many shareholders of any of the PIMCO taxable bond/credit funds mentioned above also own, or even know of PDX, but you might want to take notice of the new kid on the credit block when you see how the fund has performed compared to the rest of the PIMCO bond funds.

Now granted, it's been a tough few years for pure fixed-income bond funds and only in the last six months or so have we started to see a recovery in bond prices. But PDX also had a credit component to its portfolio even when its focus was in energy and energy MLPs.

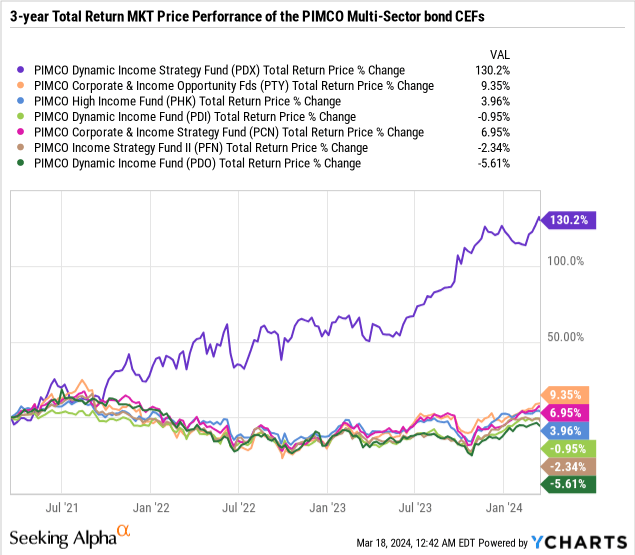

In any event, here's how PDX stacks up against the other PIMCO multi-sector bond funds at total return market price over the past three years:

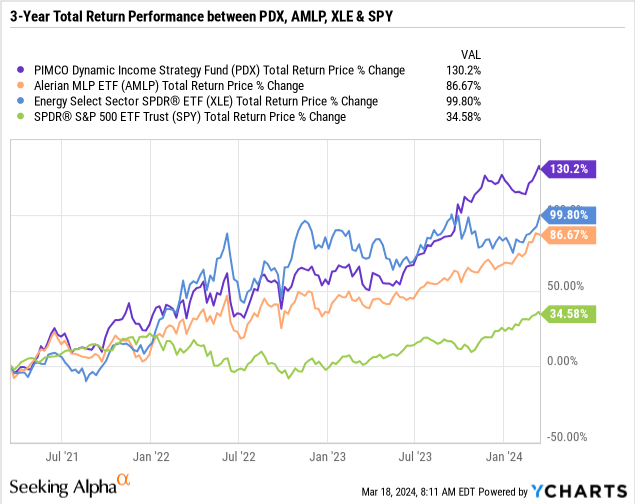

And if you think that's just because PDX was a mostly energy and energy MLP equity fund with 80% of its 15% leveraged portfolio in energy related stocks and bonds, then how do you explain how PDX also crushed the Alerian MLP ETF (AMLP), $46.63 closing market price, the SPDR Energy Select ETF (XLE), $91.56 closing market price and as a general index, the S&P 500 (SPY), $509.83 closing market price:

The bottom line is that PDX has been the best performing CEF out there over the past one to three years, but there also may be a temptation to think that PDX's best days are behind it.

I don't think that's the case, particularly when PDX still trades at a wide -13.3% discount when most of PIMCO multi-sector bond CEFs trade at premiums.

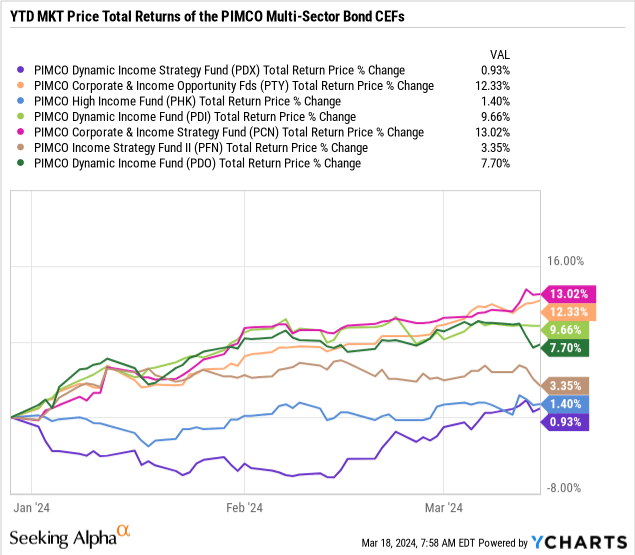

But it's true that if you look at the PIMCO bond CEFs over a shorter-term year-to-date total return performance, then PDX trails the group. I'll get into the reasons why a lot of shareholders became impatient on PIMCO's slow changeover on PDX and at one point this year, PDX was down -8%:

But there's a lot of reasons why PDX may just be going through some growing pains and why it should still be considered extremely undervalued when you compare it to some other bond/equity CEFs that may have a high market yield, but don't have the NAV performance to back up their ultra-high valuations.

In fact, I recently wrote a negative article on one of those funds, the Guggenheim Strategic Opportunity fund (GOF), $14.63 closing market price, and went from a Buy (in October of last year at $11.16) to a Sell due to GOF's ultra-high NAV yield and eroding NAV.

That article from March 5 is here.

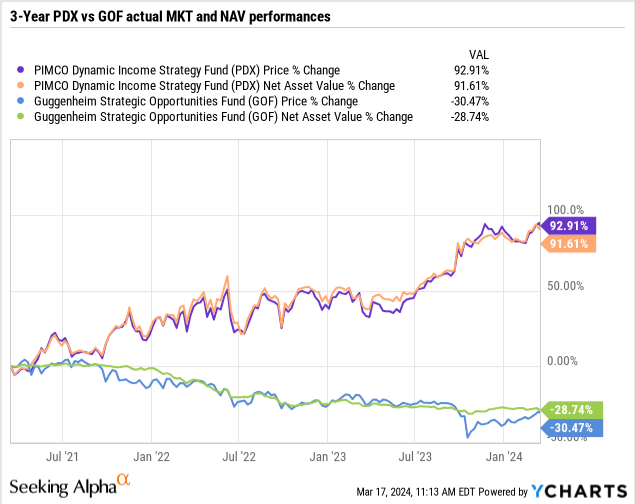

Because if you look at the performance and valuation comparisons between PDX and GOF, you would come to the conclusion that PDX is still the far more undervalued fund of the two, even though it crushes GOF over just about every time frame.

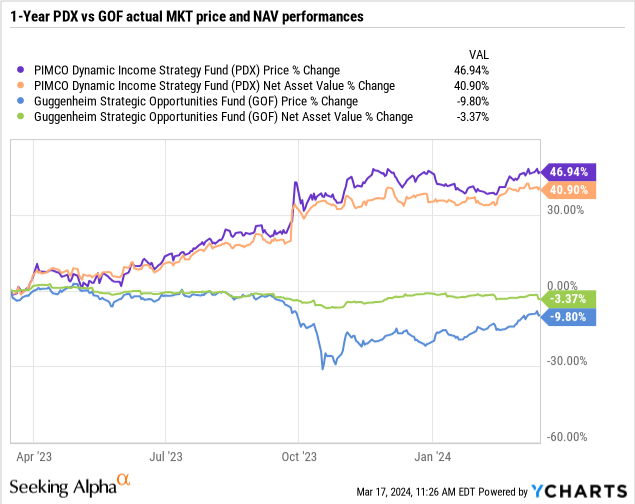

So even though GOF has risen back up to a +21.4% market price premium while PDX trades at a -13.3% discount, here's how the two fund's actual market prices and NAVs have performed going back three years:

Now, actual MKT price and NAV performance means that the fund's distributions are not included, and that certainly would change the total return comparison since GOF distributes a much higher NAV yield at 18.1% while PDX's NAV yield is only 5.8%.

But GOF would still pale in comparison and the point here is to show you how a low, and much more reasonable, NAV yield has allowed PDX's NAV (and market price) to grow over time, while GOF's NAV, and actual market price, have declined.

And if you think I'm cherry-picking time periods, here's a one-year comparison of actual market price and NAV prices:

Now I'm not trying to pick on GOF and if you notice the -30% market price line in the graph above around late October of last year, that's when I told my subscribers to buy at $11.16.

So I'm perfectly happy buying GOF when the timing is right. But this is clearly not the time. The biggest problem for GOF going forward is that it's going to have a tough time covering its current 18.1% NAV yield, and if it can't cover that NAV yield, then it's going to continue to erode its NAV.

And though many income investors seem to think that a fund's market price can go up or down based more on yield than the fund's NAV value, I can tell you for certain it's only a matter of time before a fund's market price will follows it NAV up or down. So you better pay attention.

Getting back to PDX. If you want to know why PDX has such a low NAV yield, currently 5.8%, it has nothing to do with PIMCO trying to keep it that low.

It's mostly due to PDX's rapid NAV growth over the years, which just brings the NAV yield down as the NAV goes up. Normally, that would mean one or more distribution increases, but it appears PIMCO had other plans for its PIMCO Energy and Tactical Credit Opportunities Fund (NRGX) when it released this press release on Sept. 22, 2023: PIMCO Energy and Tactical Credit Opportunities Fund to Change Name and Investment Strategy.

And thus, the PIMCO Dynamic Income Strategy fund (PDX) was born, though it would take almost six months to get to where we are today. But why did PIMCO want to change the fund's strategy in the first place after having such a successful run?

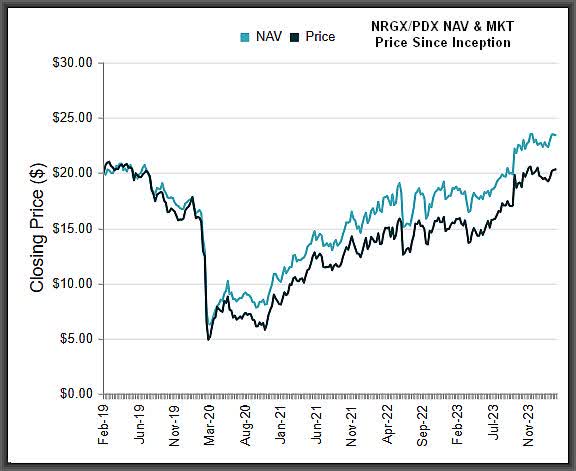

I'm guessing two reasons. One, PDX (NRGX at the time) came public just a year before COVID-19 hit and was already coming down before the bear market really got started in March of 2020. All energy and energy MLP funds got decimated that year and I'm sure it was a tough period for the portfolio managers to watch their fund go from a $20 inception price (both at market and NAV) down to mid single digits in a little over a year:

CEF.Connect

So one reason might be because PIMCO wants to stick with what they know and that's the bond and credit markets.

The other reason may be due to one big energy investment PIMCO made early on that doubled in value over a very short period in 2023. NRGX's position in Venture Global LNG (liquid natural gas) represented about 12.2% of the portfolio value as of 6/30/23 but grew to 22.6% by the third quarter holdings release at the end of September. In fact, that one position added $100 million in assets to PDX's NAV overnight on Sept. 26 when PDX's NAV jumped from $19.98 to $22.03.

Clearly, Venture Global didn't double in price over night but because it's a restricted security, it may only be valued periodically. Still, it was shocking to see PDX's NAV go up that much without some sort of offering. And by the end of 2023, which is when the latest holdings report for PDX came out, Venture Global still represented a 21% holding.

But because Venture Global is a restricted security, this may not be a position that can be easily sold or reduced, and right now, appears to represent most of the lowered 25% allocation to energy.

In other words, I'm guessing PIMCO changed the strategy (and name and ticker) because they didn't want to take the risk of having that much energy exposure and felt it was a good time to make the transition to what they know best after hitting the jackpot in energy over the last few years.

So is this a smart decision? Time will tell but, if you believe, like I do, that bonds are a safer investment now after the run stocks have had, then that should further bolster PDX's change to a mostly bond and credit fund.

But so far this year, PDX's market price is only up +0.9% even as its NAV is up +5.6%. Why hasn't PDX's market price performed better this year? It's probably due to the slow changeover that PIMCO has taken to implement the new strategy and as of the end of the 2023, PDX's portfolio still looked very much like the portfolio it had on Sept. 30.

In hindsight however, I think it was an advantage to keep the high equity exposure until year end. But we won't know of any more updates to PDX's portfolio until the first quarter holdings are released sometime after March 31.

But what probably weighed on PDX's share price the most since the changeover was announced was that there was no information or updates provided about what PDX's new distribution might be or if PIMCO would change PDX's distribution frequency from quarterly to monthly, like all of the rest of the PIMCO multi-sector bond funds.

So when January distributions were declared and there still was no news, a lot of shareholders we're clearly getting impatient after 3+ months and even a contributor here on Seeking Alpha wrote a negative article on Jan. 26 titled PDX: Not The Credit Fund We Had Wished For (Rating Downgrade).

I, on the other hand, kept recommending to add on any weakness, such as on Jan. 22. Basically what I said was:

The PIMCO Dynamic Income Strategy fund (PDX), $19.25 real time market price, -0.75%, continues to slowly bleed downward due to impatience from shareholders it seems, who are expecting a solid increase in PDX's distribution. The question is when, and January didn't bring an answer and we may not know anything until early March.

Well guess what? On March 1, we did get an update from PIMCO and they did indeed raise PDX's quarterly distribution from $0.22/share to $0.26/share for March. But more importantly, PIMCO then added in the Press Release that PDX would start a monthly distribution schedule and at a further distribution increase of $0.1133/share.

So in essence, PIMCO made not one, but two distribution increases for PDX in one declaration announcement. From $0.22/share to $0.26/share in March and then from $0.26/share to $0.3399/share beginning in April and paid monthly over three installments instead of quarterly.

How's that for progress? Well, not shockingly, there was still some disappointment that PIMCO didn't go even higher with the distribution increase. After all, most of the PIMCO multi-sector bond funds offer 10% to as high as 14% market yields paid monthly, while the monthly distribution increase for PDX to $0.1133/share only gets it up to a 6.7% market yield based on a $20.41 current market price.

But here's why this is actually creating an opportunity for investors who haven't yet discovered the best performing CEF over the last several years. If you go to PDX's Fund Card or Semi-Annual Report, both reflecting PDX's portfolio and statistics as of December 31st, 2023, you'll see that PDX had virtually no leverage on at the time.

Why is that important? Because when PDX was NRGX, the fund typically carried about 15% leverage on its equity and fixed-income portfolio. So the first step in tearing down the old NRGX portfolio was to remove the fund's leverage.

And what that means now, particularly after PIMCO announced PDX's distribution increases on March 1, is that the portfolio re-make is probably in high-gear and may be complete by the time that PDX goes ex-dividend on its first $0.1133/share monthly distribution on April 10.

So PDX is probably looking more and more like a PIMCO multi-sector bond and credit CEF every day, while maintaining roughly 25% of its portfolio in energy related positions. The big question right now is what will PDX's new portfolio look like when its mostly complete and how much leverage PIMCO plans on using for PDX.

But one thing is for sure. The more leverage PDX uses on its new fixed-income credit portfolio, and many of the other PIMCO multi-sector bond CEFs use upwards of 40% leverage, the more likely we haven't seen the last of the fund's distribution increases.

Which is why I believe the new and improved PDX is not even close to being done with its No. 1 market price performance.