Ivan Pantic/E+ via Getty Images

Ivan Pantic/E+ via Getty Images

February 27th was not a particularly pleasant day for shareholders of Henry Schein, Inc. (NASDAQ:HSIC). Shares of the company, which focuses on providing customers health and dental products, dropped nearly 4% after management announced financial results covering the final quarter of the 2023 fiscal year. Data for the quarter on its own was, admittedly, disappointing. However, guidance for the 2024 fiscal year was upbeat and indicates that the worst troubles for the company are likely over.

Given how difficult 2023 was and the fact that management was unable to achieve analysts' estimates toward the end of the year, it seems as though the market is not taking forward guidance all that seriously. But if the company can deliver on these promises, then the upside moving forward could be solid.

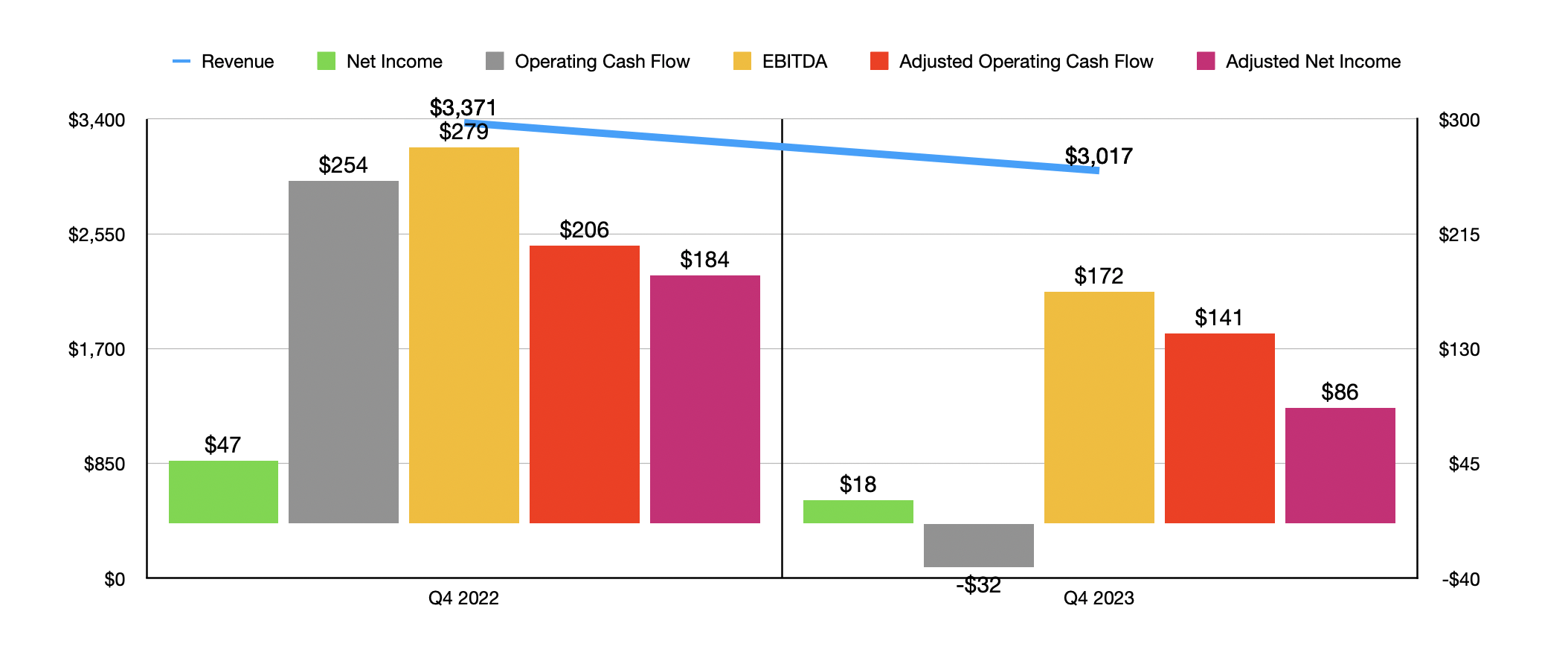

Before the market opened on February 27th, the management team at Henry Schein announced financial results covering the final quarter of the 2023 fiscal year. Revenue for the quarter came in at $3.02 billion. In addition to dropping 10.5% from the $3.37 billion generated the same time one year earlier, the sales figures reported by management were about $20 million lower than what analysts were anticipating.

The company experienced pain across pretty much every category. For instance, global dental revenue dropped 10.9% year-over-year, driven by an 11.3% decline in merchandise sales and a 9.7% drop in equipment sales. The global medical picture was even worse, with sales plunging 17%. The only bright spot for the company, from a sales perspective, involved the Global Technology and Value-Added Services category that it engages in. Revenue for the quarter came in 7.1% higher than it did one year earlier.

Author - SEC EDGAR Data

This drop in revenue brought with it a decline in profits. Earnings per share totaled only $0.13. That's down from the $0.34 per share reported for the final quarter of 2022, and it fell short of analysts’ forecasts by a whopping $0.33. On an adjusted basis, the picture was a bit better. Adjusted earnings per share of $0.66 fell far short of the $1.35 generated in the final quarter of 2022. However, it still fell short of analysts’ expectations by $0.04 per share.

Obviously, the decline in revenue was partially responsible for this. However, the company also was hit by a rise in selling, general, and administrative costs. These went from 22.6% of sales in the final quarter of 2022 to 26.7% in the final quarter of 2023. Unfortunately, management did not provide any real detail on why this occurred. And we don't yet have the annual report at our disposal. But we do know that this has been a cost problem for the company for some time. And management has attributed much of that to higher operating costs associated with payroll and payroll related activities, higher facility related costs, and consulting expenses across both segments as the company seeks to cut costs in the long run.

As a result of these disappointing earnings, overall net profits came in at only $18 million, while adjusted profits were $86 million. These are both down from the $47 million and $184 million, respectively, that the company generated one year earlier. Other profitability metrics also took a hit. Operating cash flow went from $254 million to negative $32 million. If we adjust for changes in working capital, the decline was more modest from $206 million to $141 million. And lastly, EBITDA for the company fell from $279 million to $172 million.

Author - SEC EDGAR Data

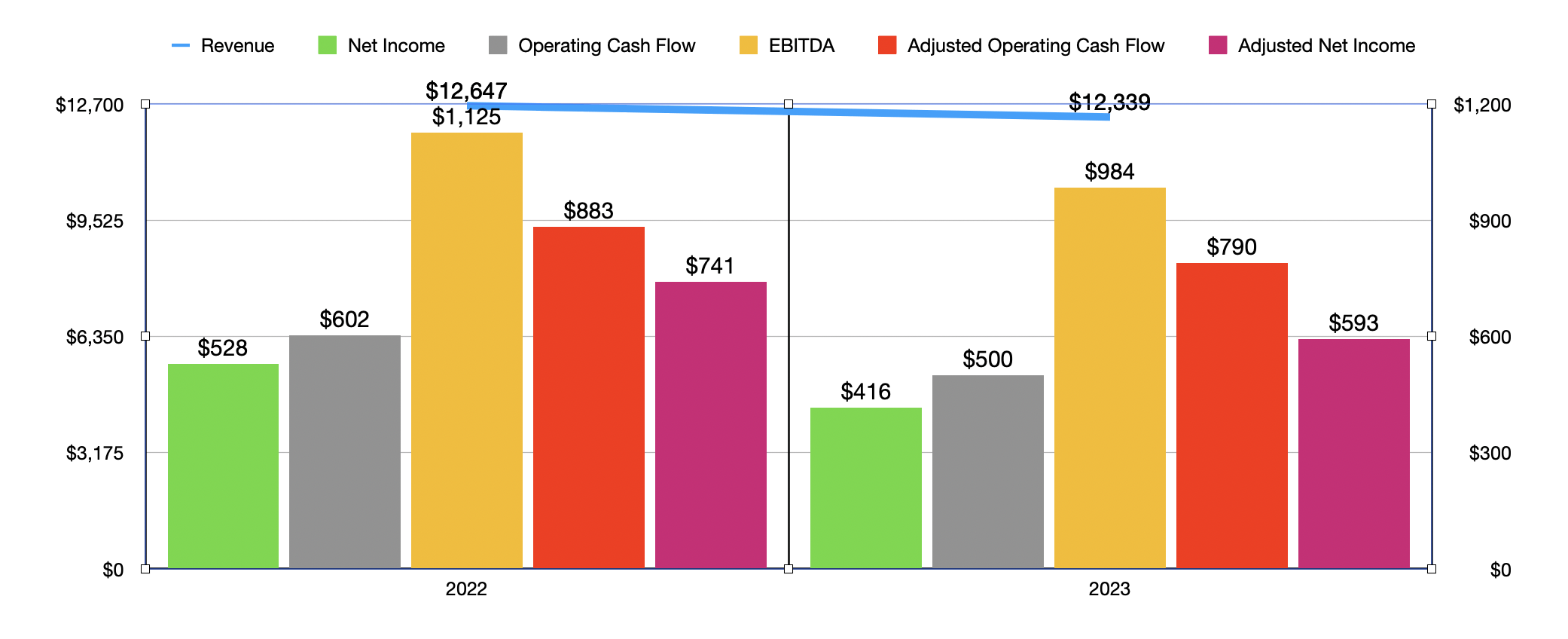

I would say that the final quarter of 2023 was the most brutal for the company. But as a whole, 2023 was not pleasant. In the chart above, you can see revenue, profits, adjusted profits, and certain cash flow metrics for the company for that year relative to the year prior. By every measure, the picture worsened year-over-year.

This is why I feel like investors should be a bit happy, but also cautious, about current expectations for the future. You see, in the earnings released for the final quarter of the 2023 fiscal year, management said that revenue this year should be between 8% and 12% higher than it was in 2023. At the midpoint, that would imply sales of $13.57 billion.

In terms of profitability, management is forecasting adjusted earnings per share of between $5 and $5.16. That would be well above the $4.50 per share in adjusted earnings reported for 2023. That would imply net profits, assuming no change in share count, of $664.2 million. In addition to this, management said that EBITDA should be at least 15% higher than it was in 2023. If we take the low end of that scale, that would imply a reading of $1.13 billion. No guidance was given when it came to operating cash flow. But if the adjusted figure for it rises at a rate of 15% as well, that would imply $908.5 million.

Author - SEC EDGAR Data

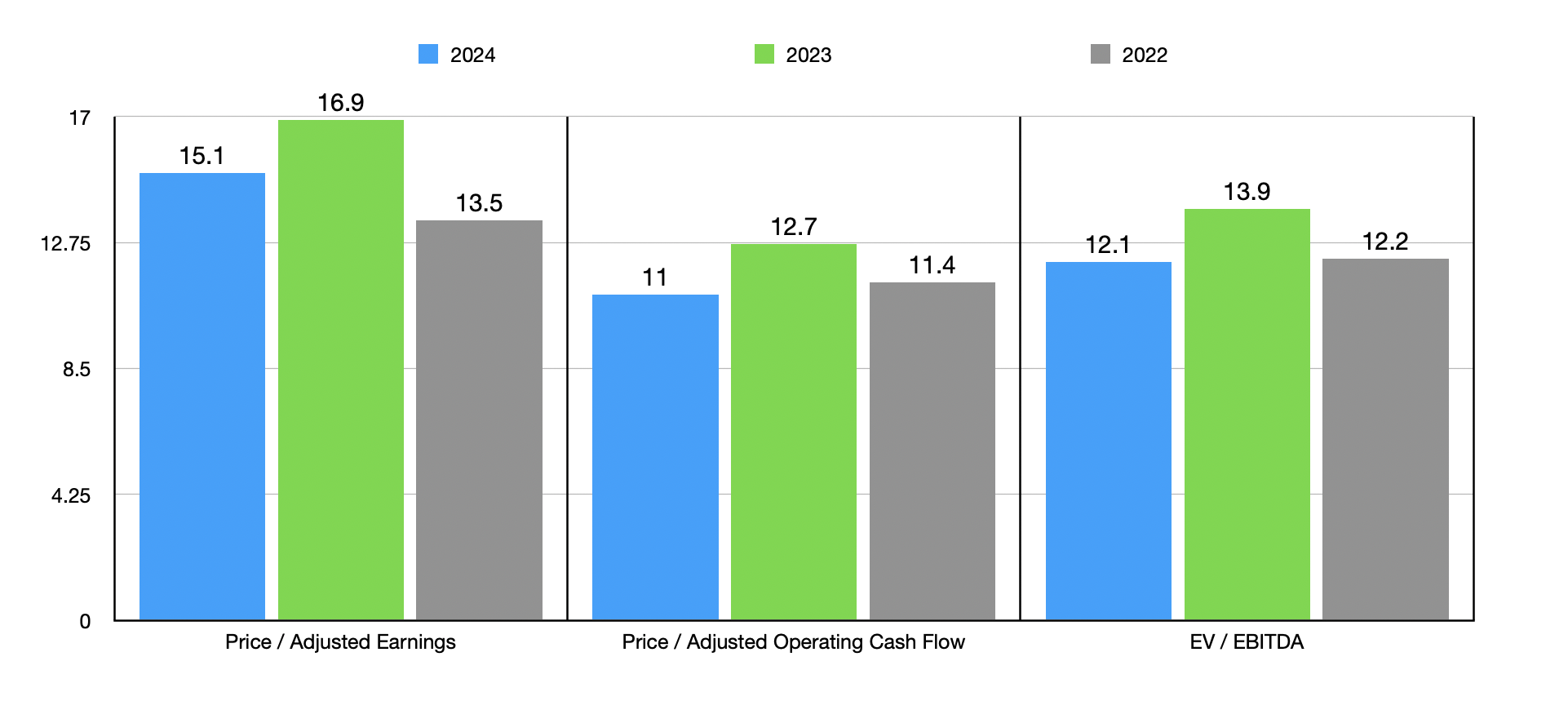

Using these figures, valuing the company becomes fairly simple. In the chart above, you can see how the stock is priced using historical data from both 2022 and 2023, as well as using estimates for 2024. On a forward basis, the stock does look particularly attractive. I wouldn't exactly call it a home run prospect. But the stock does look just cheap enough to justify some upside.

Of course, we should also pay attention to how shares are priced compared to similar firms. In the table below, I compared the company to five similar enterprises. On a price to earnings basis, only one of the five ended up being cheaper than it. When using the price to operating cash flow multiple, three of the five were cheaper. And when using the EV to EBITDA approach, only two of the five ended up being cheaper.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Henry Schein | 16.9 | 12.7 | 13.9 |

| Cardinal Health (CAH) | 43.2 | 7.0 | 14.3 |

| Owens & Minor (OMI) | 50.4 | 2.5 | 9.4 |

| Patterson Companies (PDCO) | 13.9 | 38.9 | 8.3 |

| Cosmos Health (COSM) | 96.7 | 16.2 | 41.6 |

| AdaptHealth (AHCO) | 75.8 | 3.2 | 44.4 |

Another thing to be bullish about is that management is so optimistic about the future that they are not afraid to allocate large amounts of capital toward buying back stock. Although I would prefer capital allocated in other ways, especially because shares are not incredibly cheap, this is a vote of confidence that has management saying the future will be brighter and the stock price will be higher. In 2023 as a whole, the company bought back 3.2 million shares. That cost $250 million in all. And with $265 million left under the share buyback program, it wouldn't be surprising to see further material purchases this year.

All things considered, I will say that Henry Schein, Inc. appears to be a solid company. Yes, 2023 was not pleasant. But current expectations call for attractive growth in 2024. Shares are not the cheapest out there, but they are affordable enough to warrant some degree of optimism. This is true on both an absolute basis and relative to similar firms. Due to all of these factors, I believe that a soft "buy" rating for Henry Schein, Inc. makes sense at this time.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.