Ralf Hahn

Ralf Hahn

My recommendation for Procore Technologies (NYSE:PCOR) is a buy rating, as I continue to see PCOR performing strongly with improving profitability in the coming years, driving PCOR valuation upwards. PCOR should also have no issues meeting FY24 guidance, given the growth momentum so far. Note that I previously gave a buy rating for PCOR because I believed in the long-term fundamentals of the business. I thought that the weak share price movement in late October 2023 to early November 2023 was due to near-term uncertainties stemming from the deceleration in current RPO growth, and it did not matter if one were to look over a longer time horizon.

For 4Q23, PCOR reported a decent set of results. Revenue grew 5% sequentially and 29% annually to $260 million, beating the high end of guidance ($249 million) and consensus estimates ($248.3 million). While non-GAAP gross margin came down a bit by 60bps to 85.1%, adj. EBIT expanded by 380 basis points to 6.9%. FCF also grew accordingly, from $22.5 million in 3Q23 to $29 million. As a result, for FY23, total revenue grew 32% y/y to $950 million, adj. EBIT margin expanded from -10.3% in FY22 to 2% in FY23, and non-GAAP FCF went from -$36.8 million in FY22 to $47 million in FY23.

Before I get into my bullish view, I think it is best to address the main concern that I flagged out previously: deceleration in implied current booking growth. 4Q23 proved that I was right and that it did not represent a negative trend. In this quarter, PCOR accelerated its current bookings growth from 20% in 3Q23 to 23% in 4Q23, boosted by strong bookings growth of 30% (1300bps sequential improvement vs. the 17% seen in 3Q23).

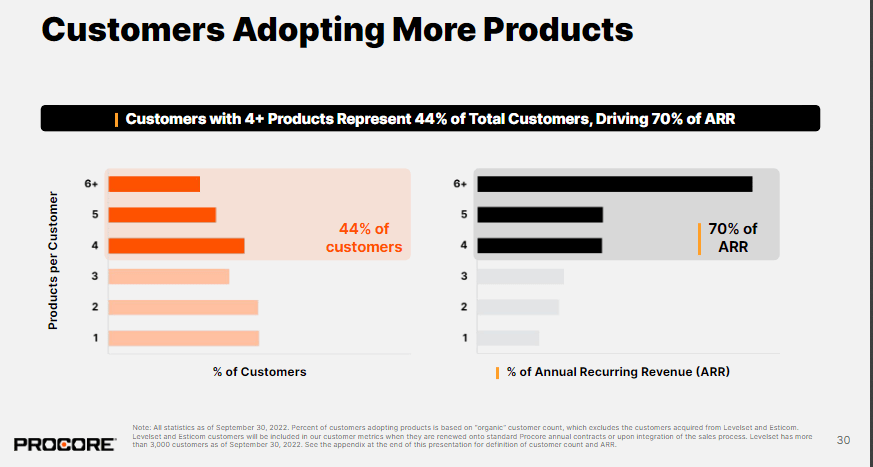

I believe the bull case for PCOR has turned more attractive, especially with management continuing to guide for 20% revenue growth at the midpoint in FY24 ($1.14 billion at the midpoint implies 20% growth), indicating that there have been no signs of demand slowdown since 3Q23 (they also guided for 20+% growth for FY23 during the 3Q23 earnings call). Just by looking at the 4Q23 results, I’d say the growth momentum is clearly strong, which makes me believe the PCOR should easily meet or beat its guidance. To reiterate, 4Q23 revenue grew 29%, beating management guidance (high-end: 23% growth expectation), and ARR grew sequentially and reached $1B for the first time in company history, indicating strong underlying demand. In addition, PCOR FY23 performance also showed very positive signs of penetrating larger customers. The number of customers with >$100k ARR grew 27% in FY23, while customers with >$1M ARR grew 33%. The growth of both groups of customers outpaced the total number of customers count by 14 and 20 points, respectively. The implications for growth are huge here because larger customers also meant more opportunities for PCOR to upsell or cross-sell products. Since these customers are already paying a lot, it would make sense for them to consolidate their vendors (if they have multiple) to save money. If we look at the FY23 results, around 75% of ARR is coming from customers using >4 products, and ~50% is coming from customers with >6 products. This is a huge improvement since the last Investor Day’s presentation in 2022. PCOR efforts on this front have not dampened customer satisfaction either, as the gross retention rate remained at a comfortable 95% while the net retention rate remained steady at 114%. I expect PCOR to continue gaining momentum on this front, especially with the hiring of Larry Stack as CRO, whose enterprise experience should be beneficial to PCOR.

PCOR

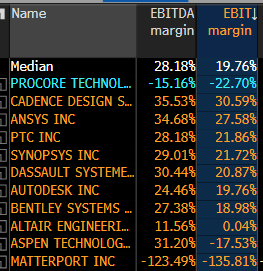

Another key highlight for PCOR is the improvement in profitability. To reiterate, PCOR reported adjusted EBIT margins of 6.9% for 4Q23, and this implies huge incremental margins in the business. To give one good example of operating leverage, PCOR grew 4Q23 revenue by 29%, but the number of employees only grew by 4%. I believe this is a key inflection point in PCOR business—accelerating profitability. Management FY24 guidance reinforces this point, as they expect an adj. EBIT margin of 7 to 8%, implying 5 to 6 points of margin expansion. This should anchor the expectations in the market that PCOR is on its way to meet peers’ margin levels.

Bloomberg

Author's valuation model

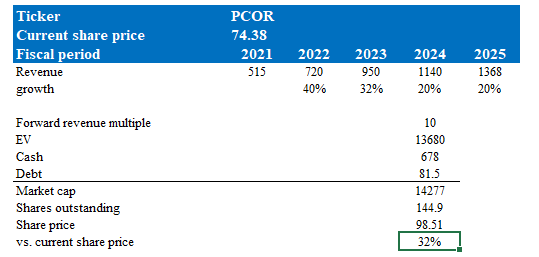

According to my model, PCOR is valued at $98.5, representing a 32% increase. This target price is based on my growth forecast of 20% over the next 2 years, using management FY24 guidance as a baseline. That said, I do think that PCOR could beat its guidance (just like it did for 4Q23) if the macro situation turns for the better. I have also increased my valuation multiple expectation to 10x as PCOR is now a much more profitable business (and is going to be more profitable); hence, PCOR should now trade at a premium to peers because it is pacing well towards the same level of margin and is growing faster.

Bloomberg

The downside risk here is that management still expects CRPO growth to continue to decelerate in 1H24 to below 20% due to a challenging demand environment. If the macroeconomic environment becomes more challenging, it could impact 2H24 bookings, which may lead to the absence of FY24 guidance.

PCOR continues to exhibit strong business fundamentals with improving profitability, evident in its robust 4Q23 results and positive FY23 performance. The accelerated current bookings growth in 4Q23 dispels concerns raised earlier, reflecting the company's resilience and continued demand momentum. Management's guidance for FY24, anticipating 20% revenue growth and a 7-8% adjusted EBIT margin, underscores the positive trajectory. The company's focus on larger customers, as reflected in the growth of >$100k and >$1M ARR customers, positions PCOR for upselling opportunities. Notably, the hiring of Larry Stack as CRO enhances enterprise expertise. In addition, I think PCOR is now at an inflection point in profitability. All in all, I believe PCOR remains a buy.