Darren415

Darren415

In this article, we provide an update on the PIMCO CEF (closed-end fund) suite. Specifically, we discuss the changes in leverage and distribution coverage. We also discuss the reversal of performance of the taxable funds so far this year, as well as changes in the funds' swap portfolios.

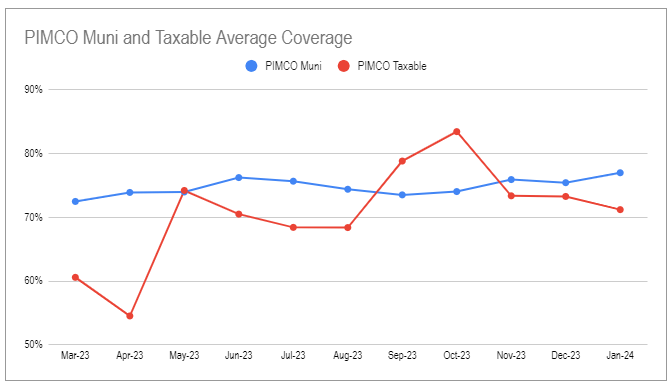

Muni distribution coverage renewed its climb from the September low, while taxable coverage fell slightly and remains in the middle of its 12-month range.

Systematic Income CEF Tool

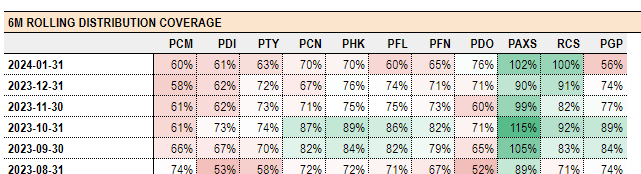

Both RCS and PAXS moved to a six-month coverage level 100% or higher, while the rest of the suite mostly fell or remained stable.

Systematic Income CEF Tool

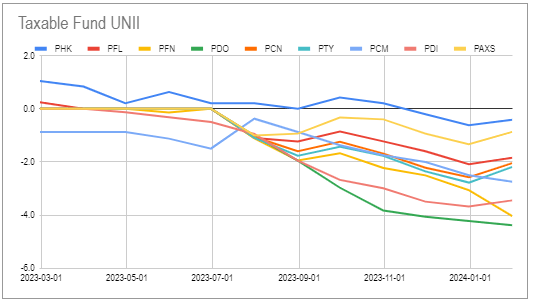

There were no major changes on the UNII front. Generally speaking, there has been a downtrend in this metric over the last 12 months.

Systematic Income CEF Tool

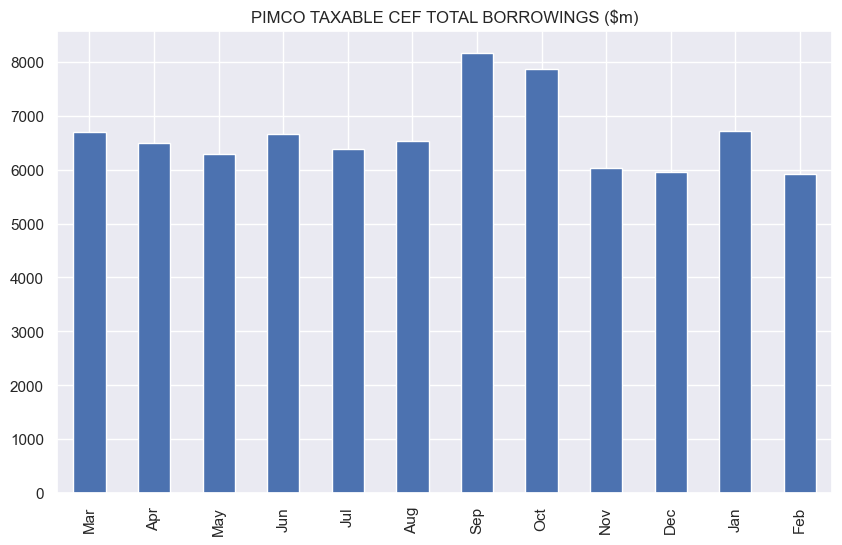

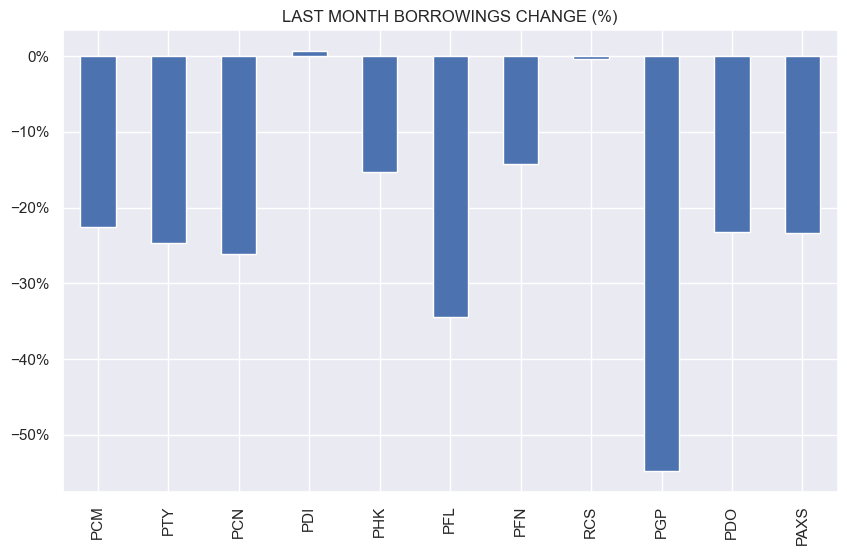

PIMCO taxable borrowings fell in February to what looks to be a new low.

Systematic Income

While all but one fund cut borrowings, PGP shed by far the most amount, cutting by more than half.

Systematic Income

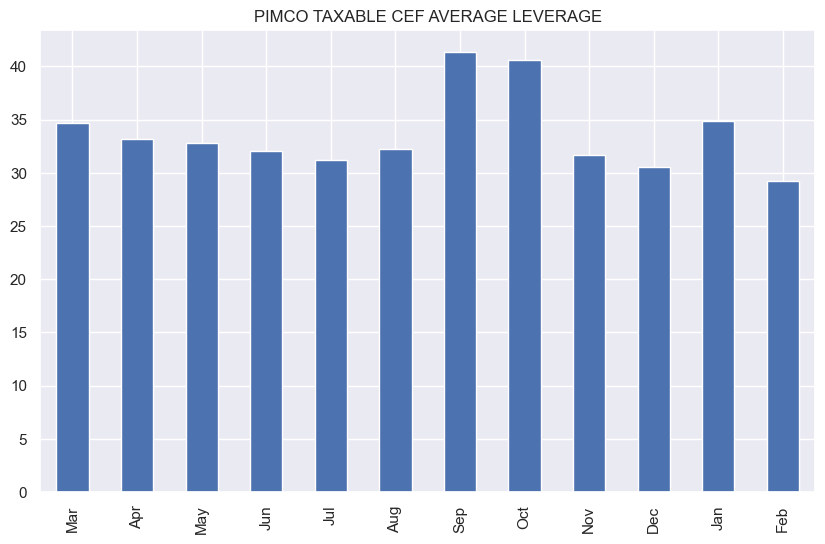

As a result, the average taxable leverage fell below 30% - an unusually low level for PIMCO.

Systematic Income

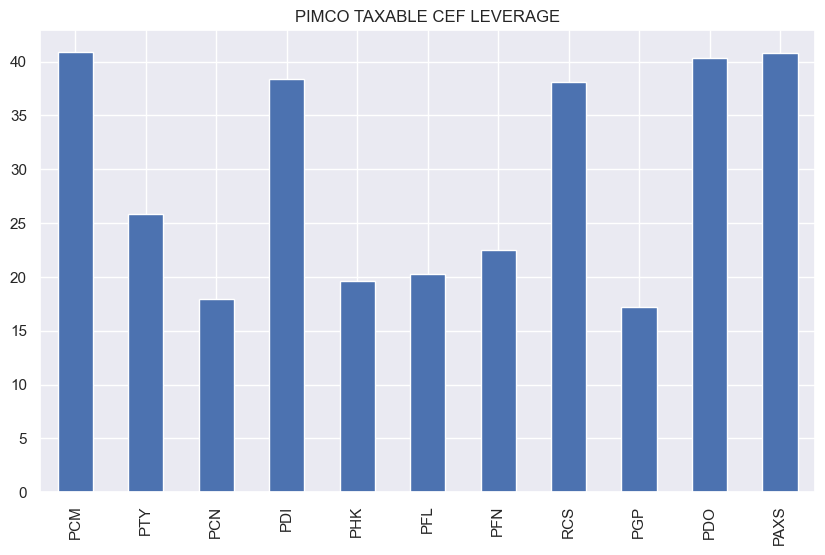

PCN and PGP both have leverage in the teens - less than half of what is typical of the suite and significantly below PIMCO's higher-leverage funds.

Systematic Income

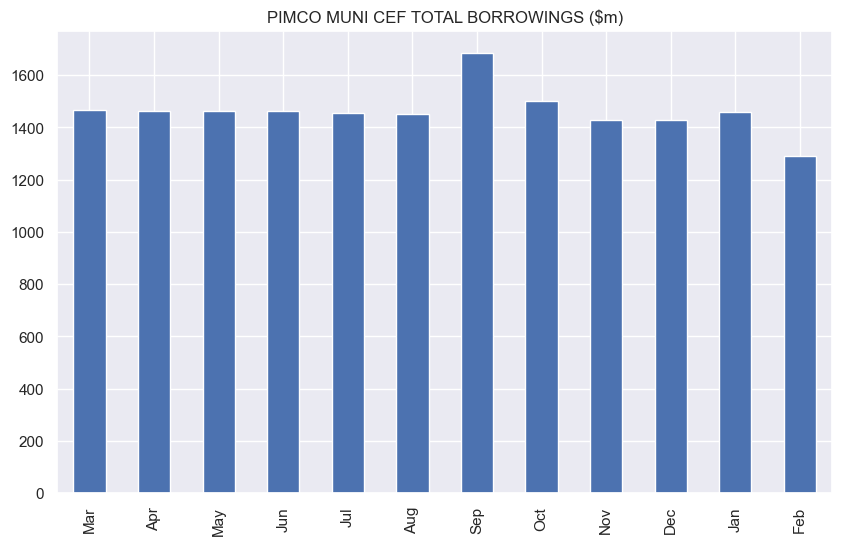

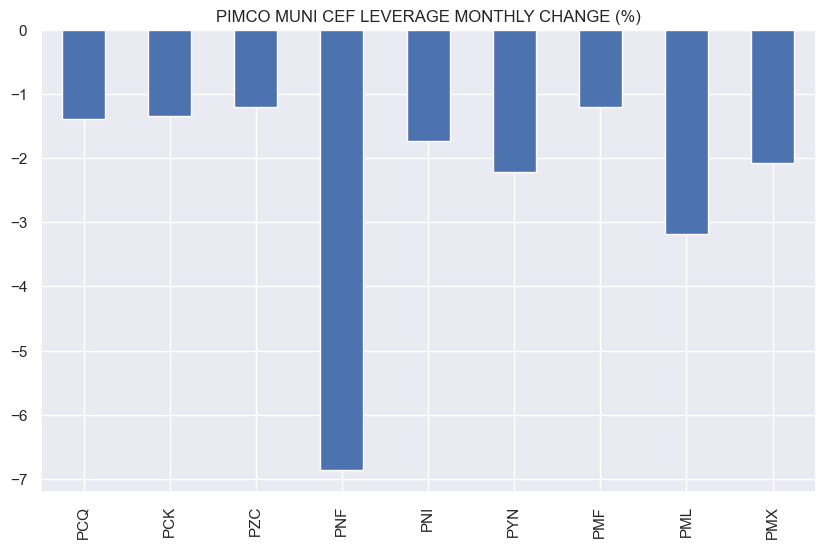

Muni funds borrowings tend to be more stable, which is why it was interesting to see a significant drop in borrowings there as well.

Systematic Income

The national fund PML and New York fund PNF shed the most amount of borrowings.

Systematic Income

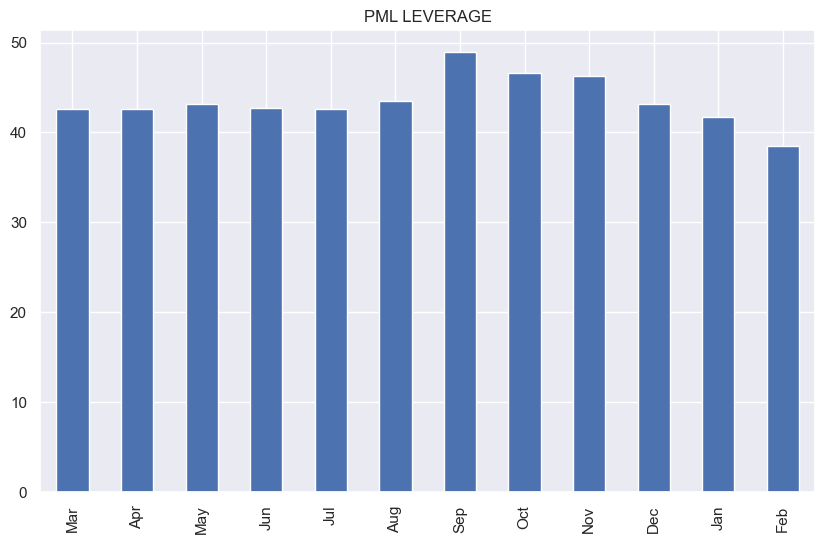

PML is now running sub-40% after touching nearly 50% leverage in September.

Systematic Income

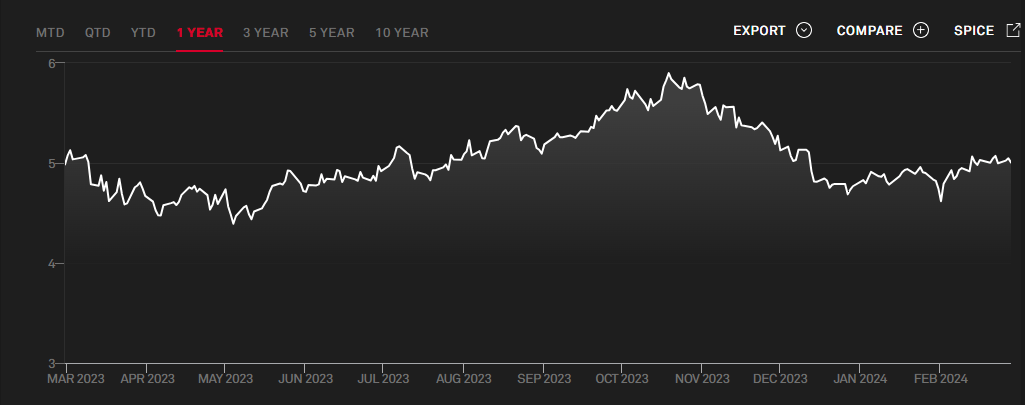

The shift in leverage appears to coincide with Muni yields, as shown below. PML leverage peaked close to the peak in Muni yields around October and has steadily deleveraged as Muni yields have fallen. If yields reverse higher we would expect leverage to increase as well.

S&P

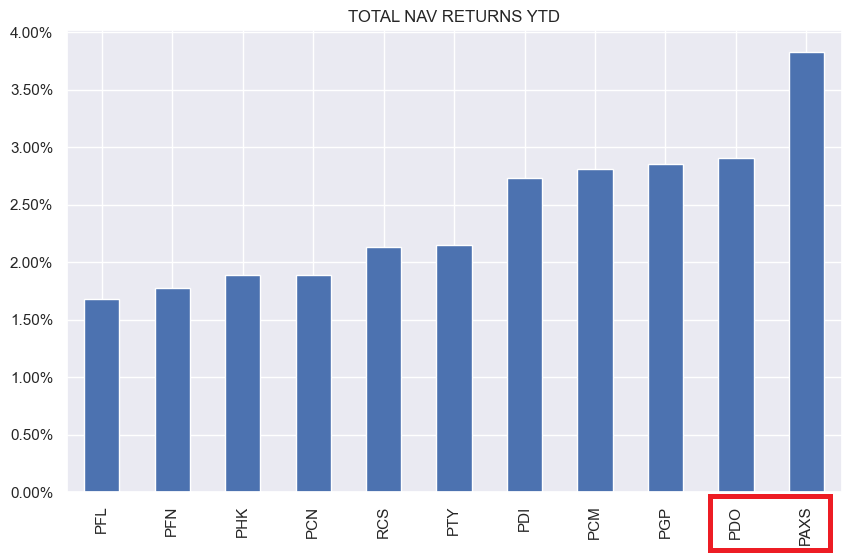

There are two market themes worth highlighting for the taxable suite. One is the reversal of performance this year from that of last year. Specifically, last year we saw an underperformance of CMBS-overweight funds like PDO and PAXS. However, this year the funds are in the lead.

This change is due to an overly pessimistic appraisal of the sector at the end of the year, as well as a broader market rally this year. PDO and PAXS have even outperformed PGP, which is a Hybrid (i.e. holding both stocks and fixed-income) fund that tends to outperform in a rising market. This is not to declare an all-clear in the CRE space, but it does highlight the frequently shifting dynamics in credit.

Systematic Income

Another theme worth highlighting is the sizable increase in the swap portfolios of the taxable funds. Recall that while swaps are more typically used to manage duration exposure or hedge floating-rate leverage facilities (i.e. by turning them from floating-rate into fixed-rate facilities) PIMCO also uses swaps to generate income.

Below is an extract of the three new swaps in the PDI portfolio, which represent most of the recent increase. What we see here is that PIMCO receives the floating-rate on these swaps (1-day SOFR of around 5.31%) and pays fixed coupons of 1.75-2%. Net net PIMCO receives 3.45% on $201.8mm or about $7m per annum from these swaps at the moment.

PIMCO

These swaps are not "par swaps" i.e. they are not executed at a "fair" level. If they were, the fixed coupons would most likely have been above 4% - roughly where 10-30Y fixed rates were trading in the second half of 2023 when they were executed.

Because they were executed at fixed coupons that were below market, PIMCO had to pay a premium to the counterparty. As we can see from the table, these premiums totaled about $38.5m (a par swap on the other hand requires no premium payment). This is the discounted value of how much "extra" PIMCO will receive through the swap coupons over time.

If we divide the $7m annualized interest received on the swap at the present moment by the $38.5m premium required to structure them, we get a yield of around 18%. The alternative to the $38.5m of capital may have been an HY bond with a yield of 7%+ or a bank loan at a yield of around 8%+. However, unlike the swap, these assets carry credit risk.

So what we see is that the swap not only provides a much higher "yield", it also does it without PIMCO taking any risk. Technically, there is duration risk, but it is easily hedged out with a par swap that goes the other way (i.e. on which PIMCO pays the floating-rate and receives the fixed-rate).

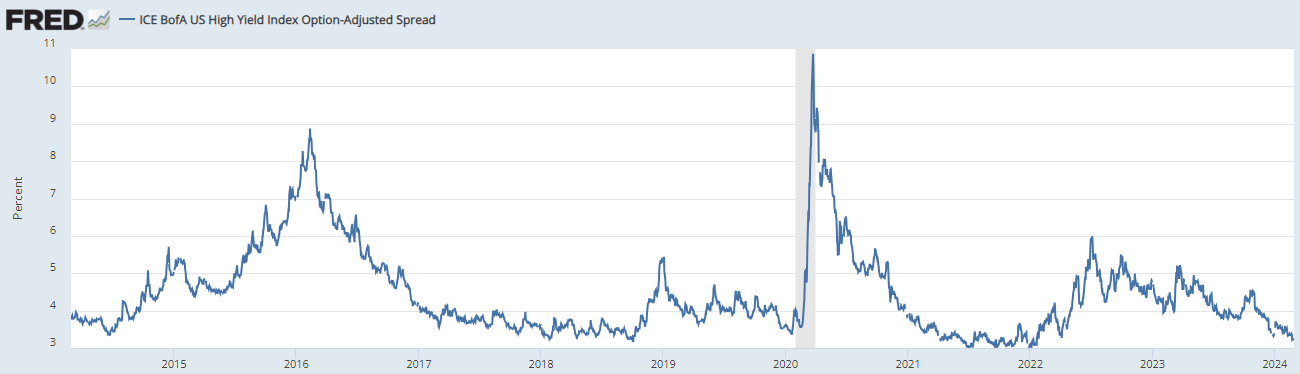

However, there is a catch which is that, unlike actual credit assets, the swaps don't really generate any new capital. PIMCO is simply getting back its $38.5m premium it paid in the form of an annuity. Why is it doing this? Perhaps it's not finding many attractive assets to buy at the moment - after all, credit valuations are very expensive as this chart of High Yield corporate bond credit spreads shows. At the same time, it doesn't want to lower the income it generated had it simply moved into cash. So it could simply be using the capital that would normally go to buy actual credit assets with a higher-"yielding", risk-free alternative, perhaps waiting for a better entry point.

FRED

Net net it's not something to get much excited about. The size of the swap transactions is fairly small in the context of the broader PDI portfolio. The notional of the new swaps is around 2.4% of the fund's total assets, and the impact of their yield is around 0.14%. If this strategy continues, it might lead to a rise in coverage, however, that rise would be entirely phantom as it would be due to a kind of non-ROC ROC.

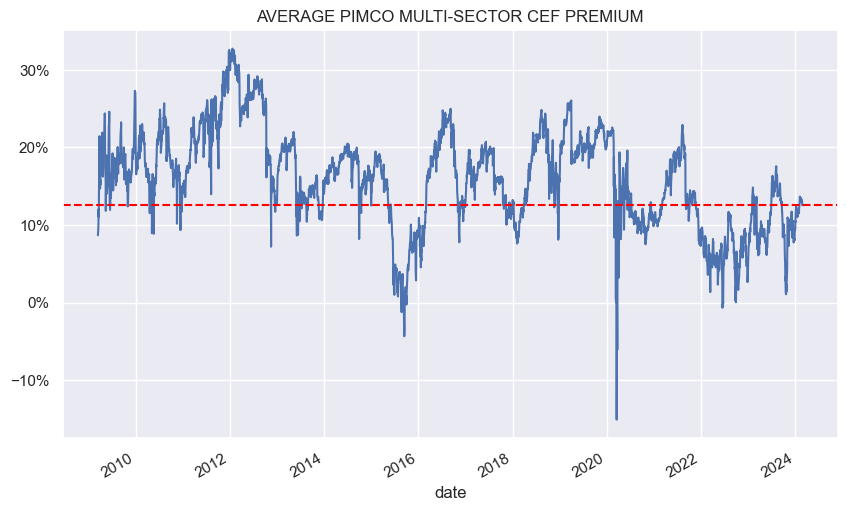

Taxable PIMCO CEF valuations have recovered from their weakness along with the rest of the market.

Systematic Income

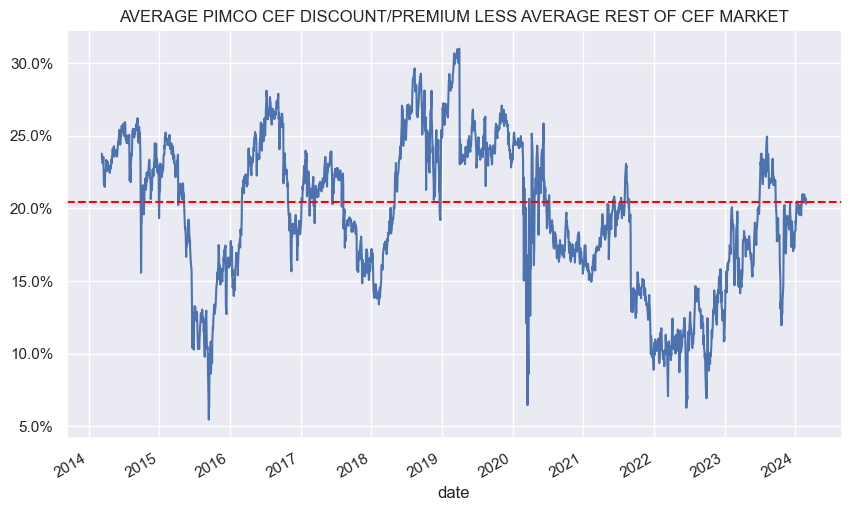

Relative to the rest of the CEF space, taxable PIMCO funds are trading at a 20% premium - roughly in the middle of their historic 10-30% range.

Systematic Income

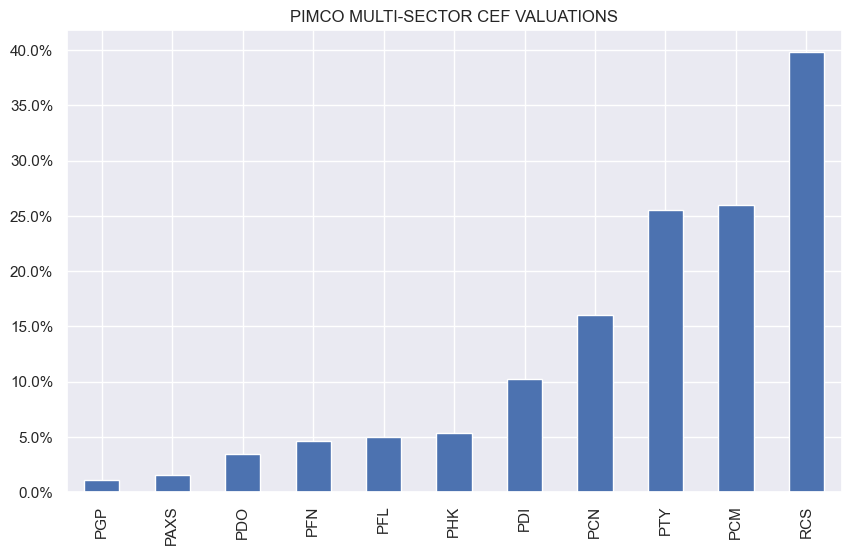

All taxable PIMCO funds outside of PDX are trading at a premium. Despite their recent outperformance, PAXS and PDO remain at the lower end of the stack.

Systematic Income

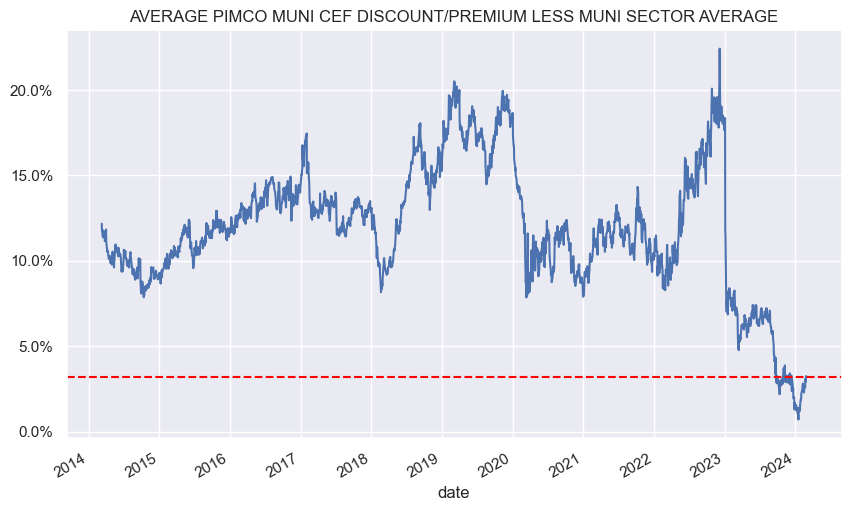

PIMCO Muni CEF valuations have nearly converged with the rest of the sector after their distribution cuts

Systematic Income

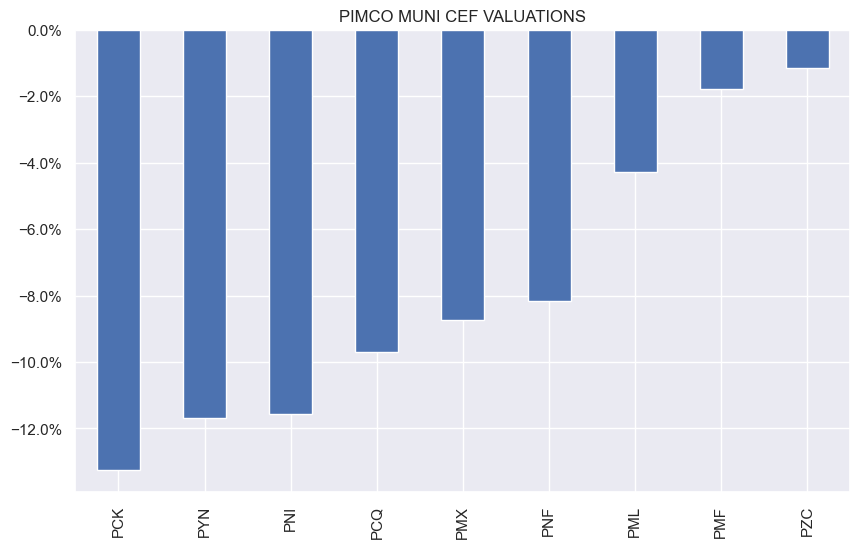

Some of the PIMCO state funds are trading at double-digit discounts and are worth a look.

Systematic Income

Overall, we continue to maintain a small position in (PDX) which we reduced recently due to continued uncertainty around its largest position in the Venture Global private equity position.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.