Justin Sullivan

Justin Sullivan

The Utilities sector continues to struggle amid much higher interest rates today compared to years ago. The benchmark 10-year US Treasury yield (US10Y) is set to end the week above 4.3% for the first time since November 2023.

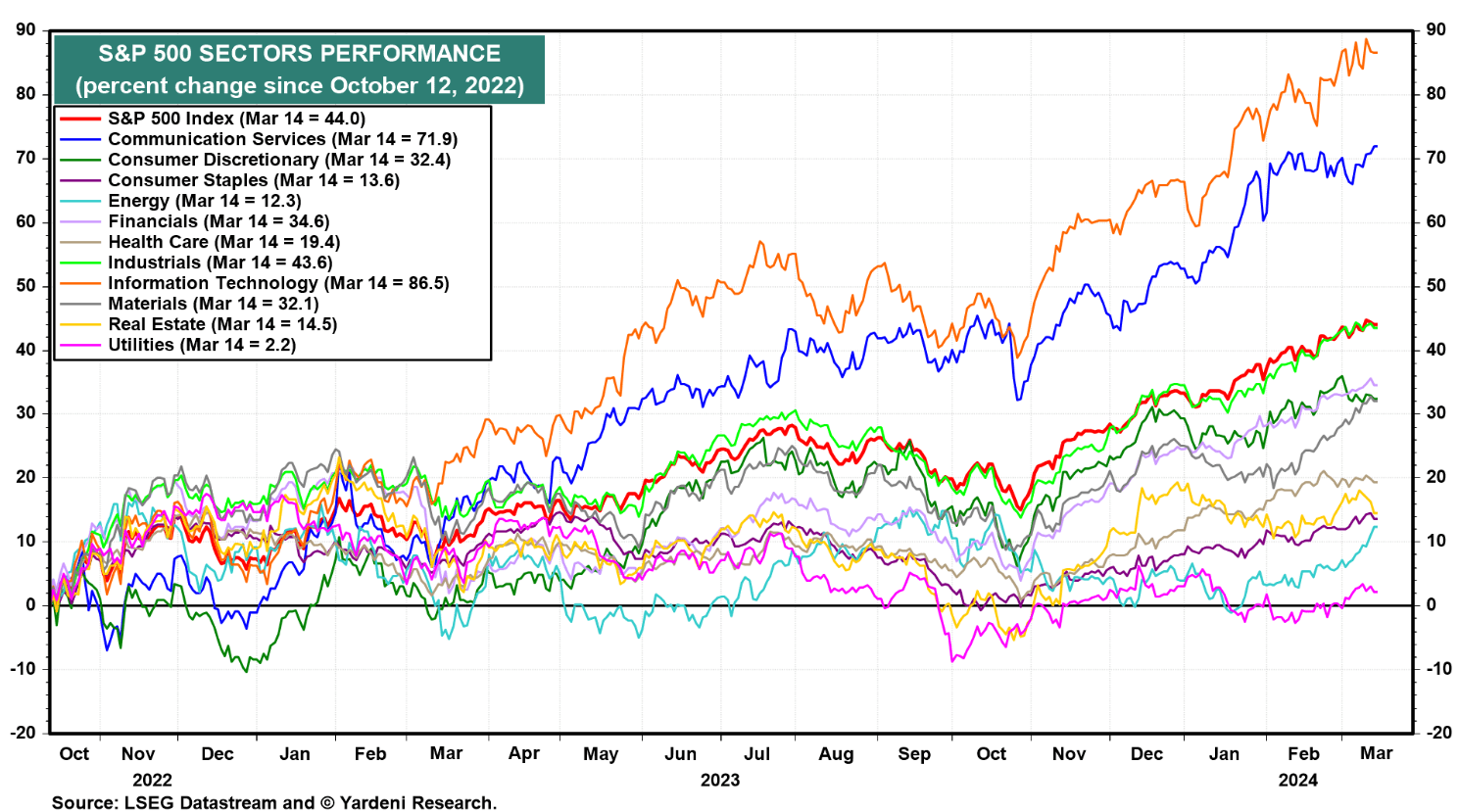

Bigger picture, the domestic Utilities sector is about flat since the market bottomed out way back in October of 2022. That leaves the group with a much more attractive collective valuation, currently in the mid-teens.

I reiterate a buy rating on PG&E Corporation (NYSE:PCG). After reinstating a dividend last year, the firm shows solid profitability trends over the quarters ahead while its valuation is depressed compared to both the S&P 500 (SP500) and its sector.

Yardeni

Finvz

According to Bank of America Global Research, PG&E is the owner of the Pacific Gas & Electric Company, a regulated utility servicing 13 million people in a 70,000 square mile service area in Northern and Central California. The utility has businesses in electric and natural gas distribution, electricity generation, procurement, and transmission, as well as natural gas procurement, transportation, and storage. Pacific Gas & Electric manages over 5 million electric and 4 million natural gas customer accounts.

Shares are negative on the year and now trade at a more than 20% discount to its peers despite EPS growth that is close to 10% in the year ahead. Depressing the valuation are regulatory overhangs, including a delay in the sale of a minority interest in PacGen and a challenge to a cost of capital increase, though BofA notes that it's not expected to result in a lower rate by the CPUC. Recent concerns include risks from wildfires, including the Smokehouse Creek Texas wildfire and a cautious tone in Berkshire Hathaway Inc.'s (BRK.A) annual letter regarding utilities prone to financial liability due to wildfires.

It was also disappointing to hear about a mixed shelf equity offering last month despite increased earnings guidance. I'd like to see better shareholder-friendly activities, including a bigger dividend now that one is finally in place.

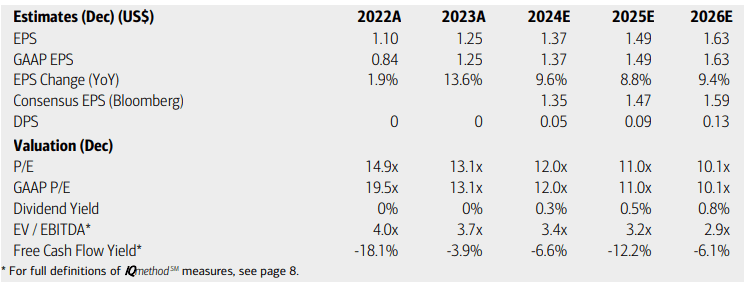

On valuation, analysts at BofA see earnings rising close to 10% this year with continued high-single-digit operating EPS growth in the years ahead. Seeking Alpha's consensus figures reveal similar increase rates while PCG's top line is forecast to increase at a modest clip. Dividends, meanwhile, are expected to gradually rise, though the yield may remain under 1% for the next several quarters.

BofA Global Research

If we assume normalized EPS of $1.40 over the coming 12 months and apply a modest 15 multiple, then shares should trade near $21. That is plenty of upside, so I reiterate a buy rating on valuation. While PCG has a low 5-year average forward non-GAAP price-to-earnings ratio, I assert that with the bulk of wildfire litigation risks behind them, a more normalized sector P/E is in the offing.

Seeking Alpha

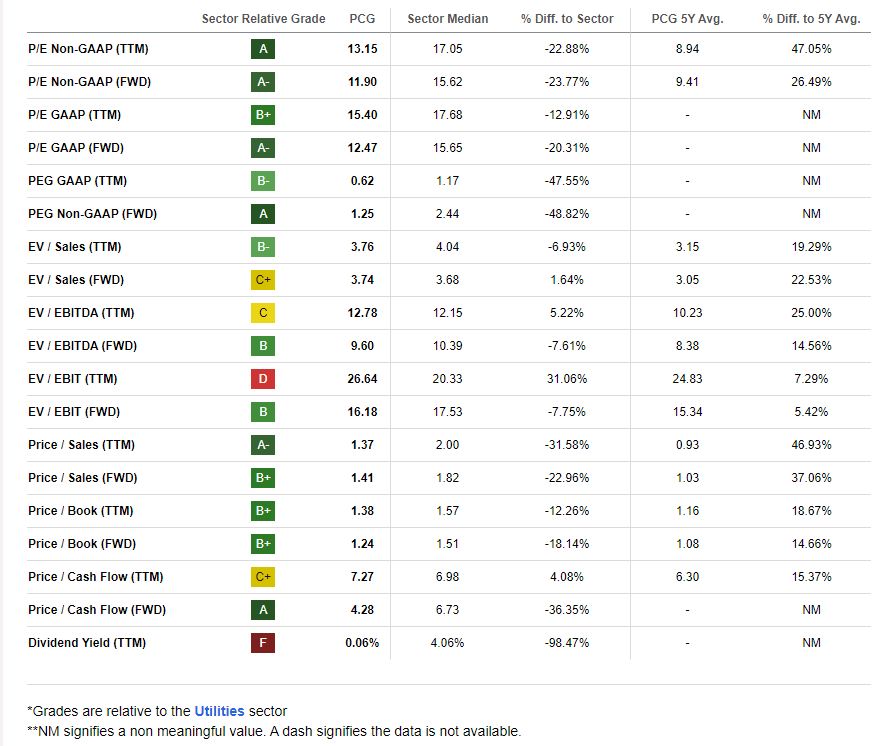

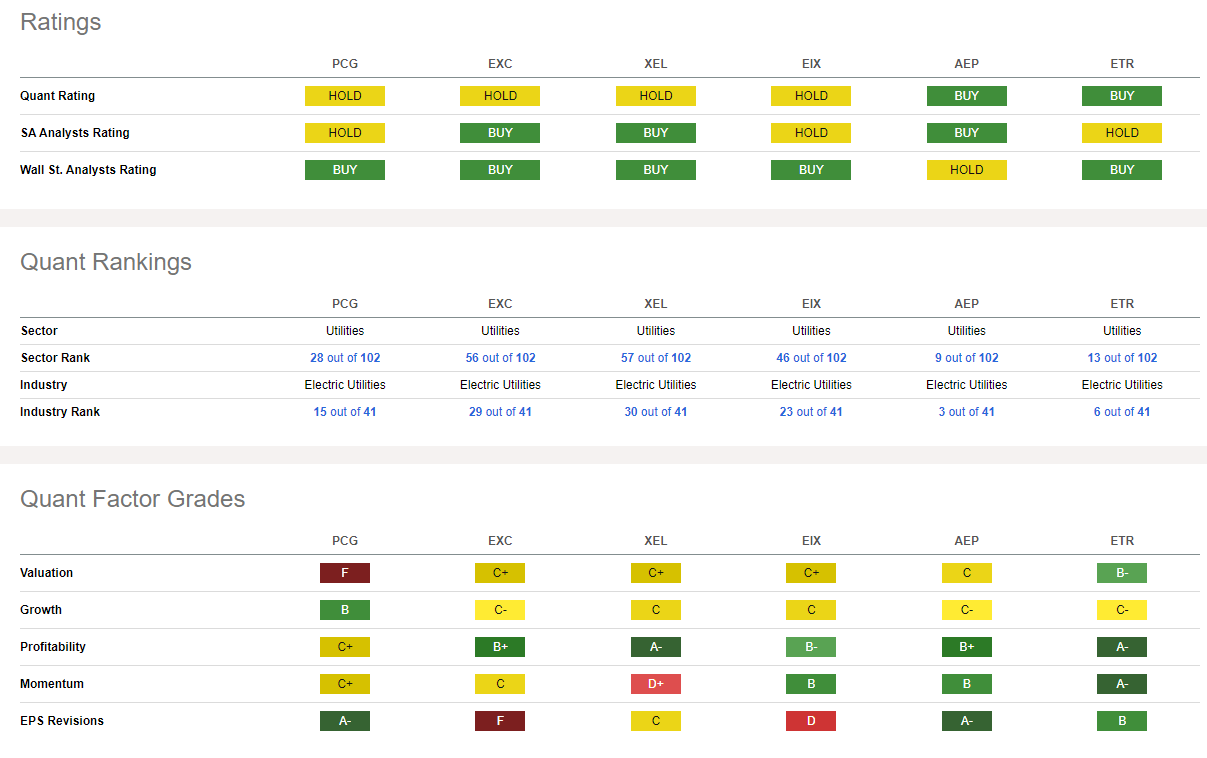

Compared to its peers, PCG features a soft valuation grade, though, once again, I see its low P/E today as an opportunity while EPS growth trends ahead are favorable. Profitability is also seen improved on a look-ahead basis and EPS revisions have been solidly to the positive side over the past three months. Finally, share-price momentum has been particularly weak over the past six months after a strong run by the stock - I will highlight key price levels to watch on the chart later in the article.

Seeking Alpha

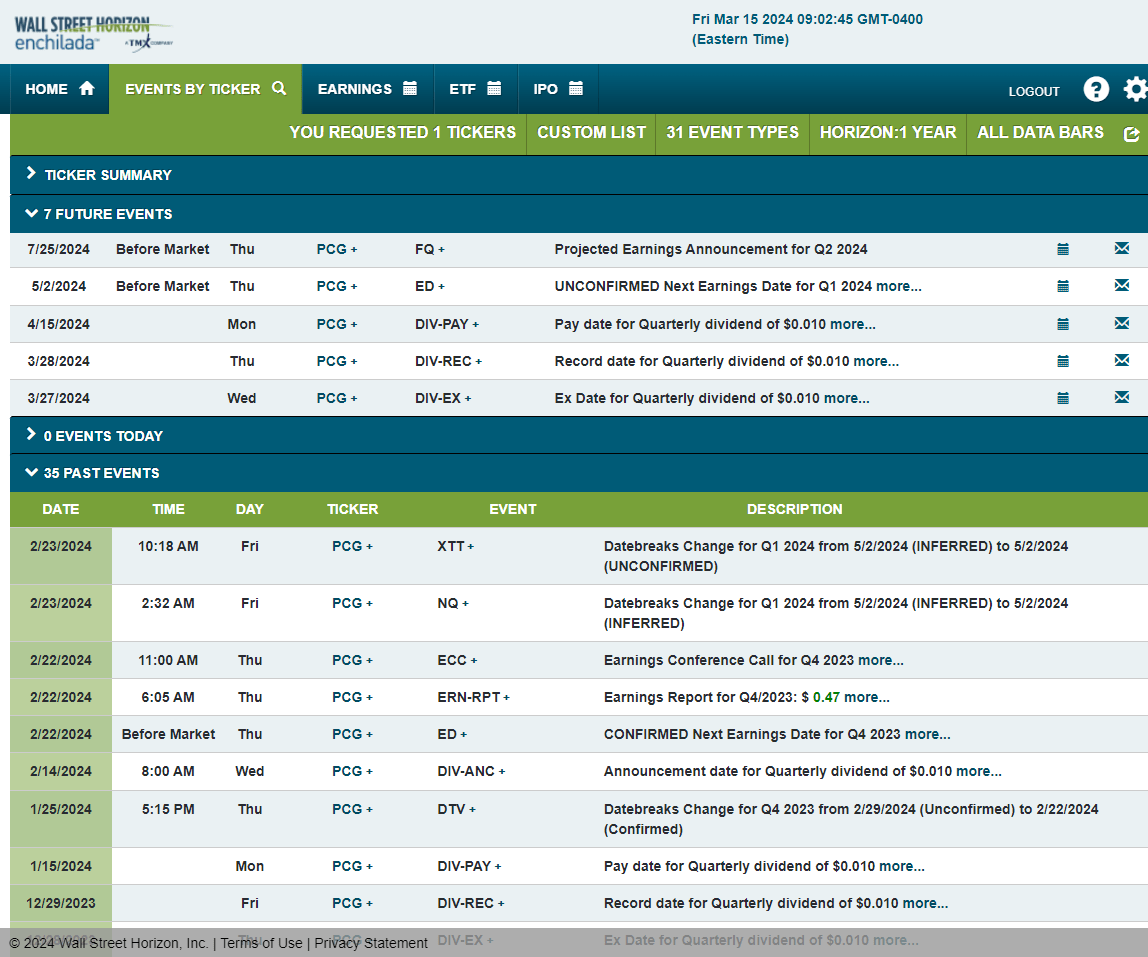

Looking ahead, corporate event data provided by Wall Street Horizon shows an unconfirmed Q1 2024 earnings date of Thursday, May 2 BMO. Shares trade ex a $0.01 dividend on Wednesday, March 27.

Wall Street Horizon

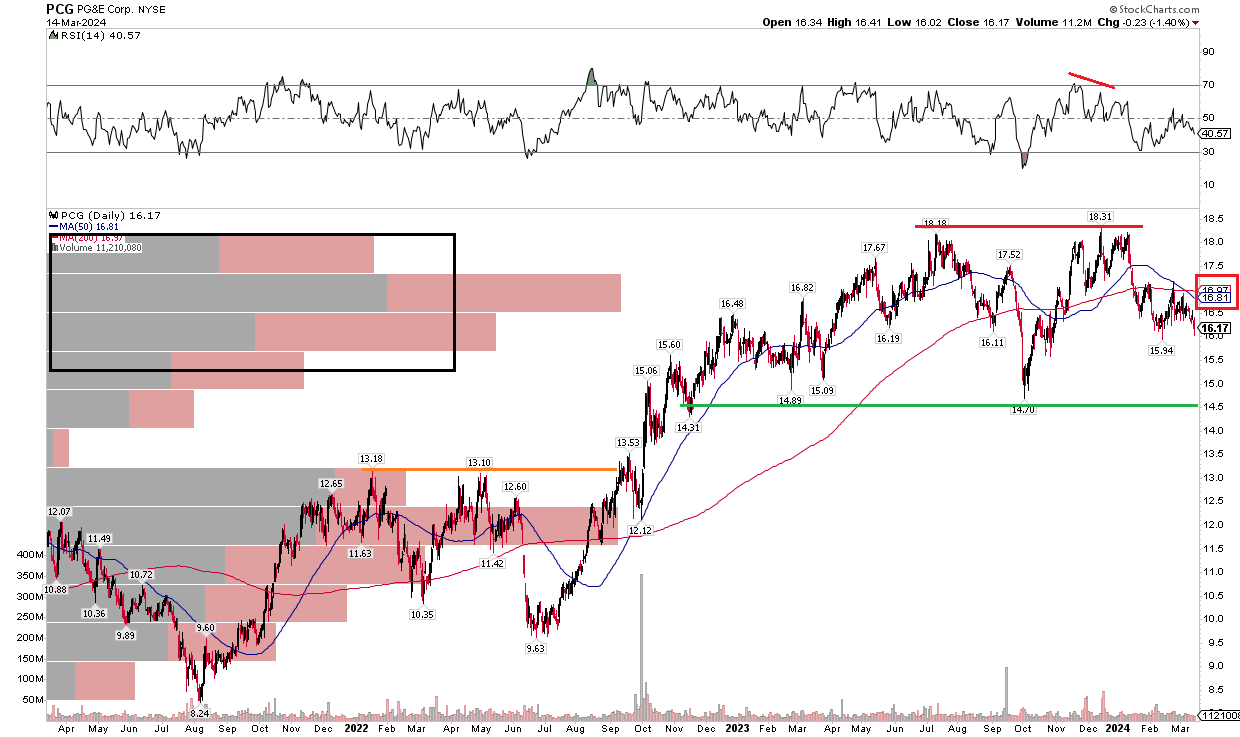

With PCG undervalued and a dividend now in place, we need to see the stock act better with respect to its momentum. Notice in the chart below that shares have traded sideways for quarters on end. A strong rally took place from mid-2022 through July last year, and I last reviewed PCG in Q2 2023. While the stock has been about unchanged since then, support has emerged between $14 and $15. Resistance is seen, however, at a double top level just above $18. I would like to see PCG hold the mid-teen zone and break out above the dual highs from 2023. If that happens, then an upside measured move price objective to near $22 would be in play.

Take a look at the RSI momentum gauge at the top of the graph, though. It showed a bearish divergence with price at the end of 2023, portending a slow start to 2024. Moreover, both PCG's short-term 50-day moving average and longer-term 200-day moving average are now negatively sloped, indicating that the bears have reasserted their control over the stock. With a high amount of volume by price between $15 and $18, it could be tough sledding for the bulls in the months ahead. Finally, PCG has been a relative laggard in the market - another bearish factor.

Overall, the technicals are not encouraging, but buying just above $15 could be a favorable risk/reward idea.

StockCharts.com

I reiterate my buy rating on PG&E Corporation despite the technical weakness. Shares appear undervalued in the sector and broad market, while earnings growth should be impressive this year and next.