DarthArt/iStock Editorial via Getty Images

DarthArt/iStock Editorial via Getty Images

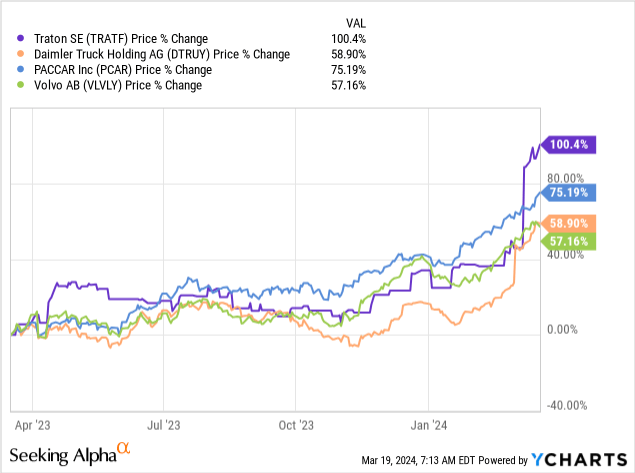

Traton Group (Traton SE) (OTCPK:TRATF; OTCPK:TRATY) has been a surprise I had not anticipated.

The company numbers among the major players in truck and bus manufacturing. Traton was spun off from Volkswagen which sold about 10% of its shares while keeping control of the remaining 90%.

Almost two years ago, I wrote an analysis on the company comparing it to the other two big spin-offs that happened in the industry in the past few years: Daimler Truck (OTCPK:DTRUY) and Iveco Group (OTCPK:IVCGF).

The industry has literally taken off in the past few months, but Traton has overperformed all its peers in the past year, doubling in price.

As said, when I covered the company almost two years ago, Traton was surely sporting a portfolio with many well-established brands, such as Scania, MAN, Navistar, and Volkswagen Truck & Bus. Yet, compared to the progress Daimler Truck had made in terms of profitability, Traton was still suffering from low margins that were just around 4%, dragged down mainly by MAN.

So, what happened in these two years, and, more importantly, what has turned the market bullish on Traton in the past few quarters?

Let's start with a few financial data about the company.

For fiscal year 2023, Traton reported almost 340,000 vehicles delivered, a record high and 11% up YoY. Even better growth was reported in sales revenue, €47 billion and +16% YoY. The return on sales (operating margin) was 8.6% for the whole company, with Traton's industrial operations already reaching 9.3%. Considering the 2024 goal for Traton is 9%, we can expect the company to easily beat this and, perhaps, target a double-digit margin. Traton also reported a strong bottom-line result with EPS for the year at €4.

To put these numbers into context, let's look at Traton's closest peer: Daimler Truck. It delivered 526,000 units, only 1% up YoY, with revenues increasing 10%. As a result, Traton seems to be growing at a faster pace than Daimler.

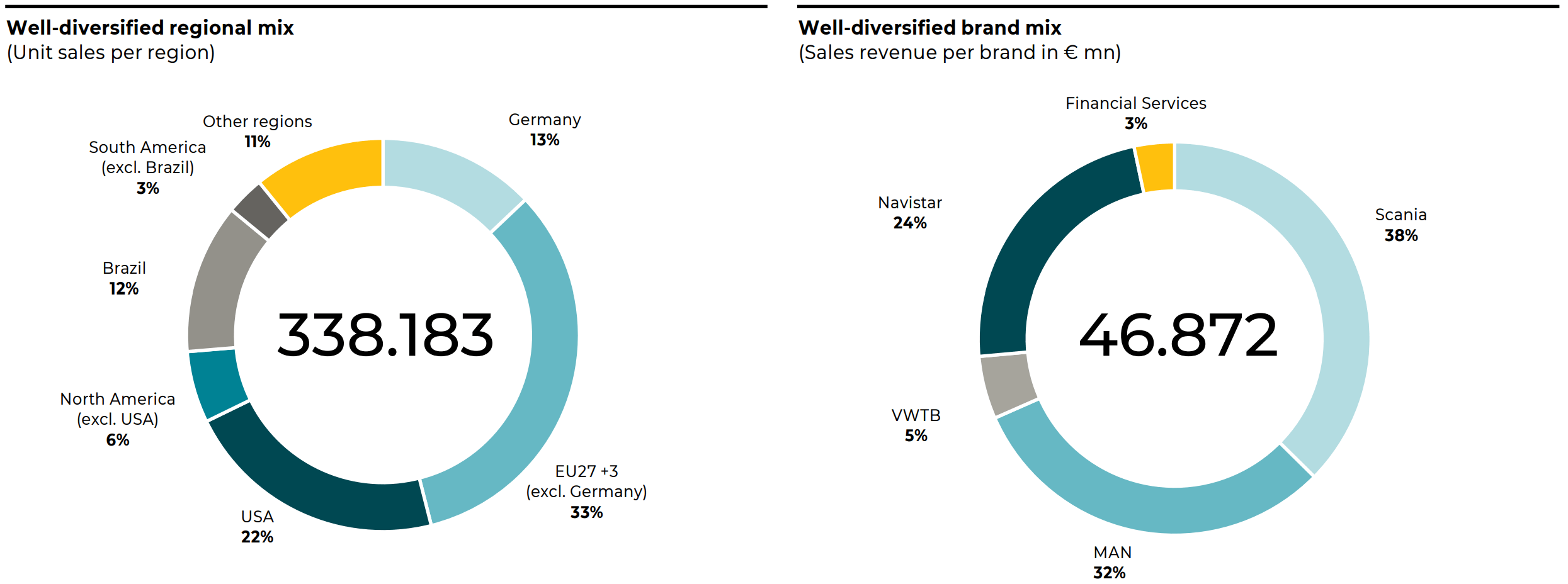

If we look at the sales revenue breakdown by brand, we can see below that Scania is the largest contributor to Traton's sales, with Man in second place and Navistar in third. This is also true when we look at margins since only Scania performs in line with the industry leaders - Paccar (PCAR) and Volvo (OTCPK:VLVLY) - achieving a double-digit margin. At the same time, Man has improved greatly and reported a 7.3% operating margin. Navistar shows a mixed picture. On one side, being a North American brand, it should report a higher margin. On the other, Traton is focusing on enhancing its profitability and, as a result, we can expect Navistar's performance to improve significantly in the next few years. This could contribute to the overall turnaround Traton is putting into action.

TRATON 2023 Annual Results Presentation

We can look at the brand mix also through the pie chart below on the right. It shows the weight of each brand on Traton's overall sales. Scania makes up 38% and MAN another 32%. Navistar comes in third with 24%. Something that distinguishes Traton in the industry is its well-diversified regional mix (Iveco, for instance, is mainly a European company). Of course, Europe still makes up 46% of total sales, with Germany alone having a 13% weight. But having 28% of its sales in North America and another 15% in South America puts Traton in a good position to mitigate any local slowdown in a particular market.

TRATON 2023 Annual Results Presentation

While Traton is picking up speed and improving rapidly its operations, it seems the real laggard of the industry is Iveco, which reported a profit margin of 5.8% even after these past two outstanding years. This is why I think Iveco may be an M&A play: it is a strong regional player in Europe, but it lacks the strength to compete worldwide.

So far, we have seen a company whose growth has been strong and has gone along with improved profitability.

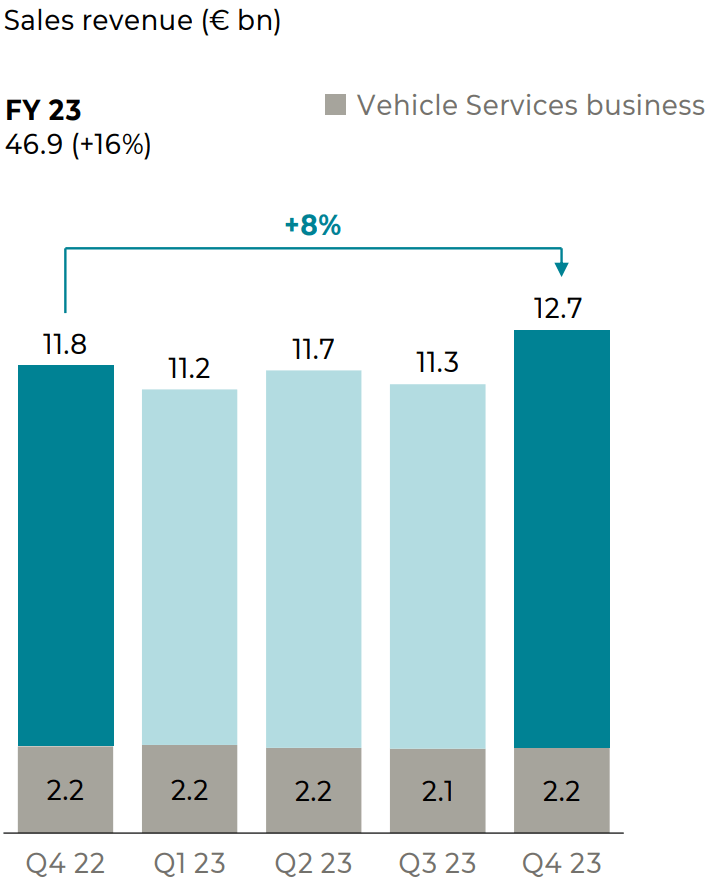

But there is one more thing we should be aware of when we consider Traton's sales revenue. We can see it in the bar chart below.

TRATON 2023 Annual Results Presentation

Here, Traton shows the percentage of its services revenue on the overall revenue. What seems to be beautiful is that, no matter if sales increase or decrease, Traton's services revenue is a steady €2.2 billion quarterly inflow.

In other words, this is recurring revenue. In the industry, while most players do talk about their services, it is only Traton and Paccar that report the numbers to understand what percentage of the overall revenue comes from this. In Traton's case, Services make up between 17% and 19% of total quarterly sales. This business line already doesn't yet report its operating margin, but it should be a high-teens one, if not already in the low twenties. Moreover, Services see strong tailwinds because of aged truck fleets and high utilization rates.

Let's look at a few other financial data before we move on.

Traton's strong profitability and leaner operations led the company to report a net cash flow: of €3.6 billion, with €1.2 billion coming in during Q4 of 2023.

For 2024, Traton expects this number to be in a lower range, between €2.3 and €2.8 billion.

Since Traton was able to generate so much cash, the company's board has proposed a dividend payout of €1.50 per share, corresponding to a payout ratio of 31% and an attractive 7% yield.

A few words on the balance sheet.

Traton reported it reduced its industrial debt by €2.0 billion to €5.8 billion by year-end 2023. This makes the company's operations well protected, financially speaking. So, where do most of Traton's €13.3 billion in LT debt come from? Mainly it comes from the financial branch, as is typical for automakers and truck manufacturers. An industrial debt of €5.8 billion is less than last year's EBITDA, which came in at €6.3 billion. As a result, I see Traton in a healthy financial position.

Also important to note is the dividend payout for fiscal year 2022, amounting to a cash out of €350 million in the second quarter. By further reducing our industrial debt, the company openly admitted it wants to achieve two important effects; first, increasing its equity value; and second, reaching a standalone investment-grade rating for more flexibility in its financing efforts.

So, I clearly missed the chance to make a nice 2x. This is a particular situation because it is where FOMO or revenge trading can kick in, leading us to unwise decisions. Let's then stick to the usual way to assess a stock. After we have understood that Traton's profitability is rapidly improving, let's see what we can expect for this year and beyond.

First of all, it is unreasonable to expect demand for trucks to be as high as it was in 2021 and 2022. This doesn't mean the market is idle, but that we should expect a normalization of demand. During the last earnings call, Traton's management disclosed it expects high demand in certain areas around Europe and North America, especially because there could be pre-buys before the emission regulations expected to be ruled between 2025 and 2027.

Traton reported 265,000 incoming orders, which is a 21% decline YoY, but still shows a good level of demand which could even increase if fears of a recession get swiped completely away.

In any case, Traton's guidance is quite wide because it sets unit sales and sales revenue in a range between -5% and +10%. In terms of operating margin, the company guided for 8%-9% margins in 2024.

My take is that Traton's being deliberately vague and conservative so that it will be easier for the company to report a beat. Though orders are down, so are commodity prices, while vehicle prices have not yet come down (will they ever, I ask as a consumer?).

First of all, Traton is a stock listed in Frankfurt and Stockholm. As a result, North American investors might find liquidity issues when buying their shares over the counter.

More inherent to the industry, Traton faces the risk of a sudden drop in orders due to a cooling economy. But its portfolio is well-balanced

Traton currently has a market cap close to €16.5 billion and trades at €33.70 a share. Its 2023 EPS came in at €4.90, which gives a TTM PE of 6.9. Paccar, on its side, trades around a 12.5 PE and so does Volvo. Daimler trades a little bit below, around a PE of 10.

We can take Traton's TTM PE also as the fwd PE since the company's guidance could make us think 2024 will post flattish growth. Is this a good valuation? Is Traton still a good buy?

I think the answer won't be found in Traton's PE. Of course, it shows we are in value territory. But the real question is whether Traton can generate significant cash flows for years to come.

Traton talked about net cash flow. But let's use the more common metric of free cash flow, calculated as operating cash minus capex. This gives us around €1 billion in FCF for the last fiscal year. This is equal to €2 of FCF per share, giving us a 6% FCF yield. This is interesting, especially in the case we are among those who believe Traton can improve its operations and start printing more than a billion in FCF per year.

As for me, since every quarter the company does over €2 billion in vehicle service revenue, I think the likelihood for Traton to generate €1 billion in FCF per year or more is high. As a result, I am changing my stance from what I wrote two years ago and rate Traton as a buy. The fact it is trading at its ATHs is not a concern for me because the company's fundamentals are clearly driving a multiple expansion and a re-rating of the overall business. As we have seen, it is deserved.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.