Peshkova/iStock via Getty Images

Peshkova/iStock via Getty Images

We previously covered Petrobras (NYSE:PBR) in November 2023, discussing its mixed FQ3'23 earnings call, as the volatile spot prices and elevated expenses triggered its impacted profitability and dividend payouts.

We had also believed that FQ4'23 might bring forth some uncertainty, with the expanded Free Cash Flow from reduced capex and raised output guidance negated by the lower spot prices and forex headwinds.

However, thanks to its inherent undervaluation, the stock still offered a compelling forward dividend, resulting in our reiterated Buy rating then.

In this article, we shall discuss why we are maintaining our Buy rating for PBR, with the market over-reacting to the supposedly lower FQ4'23 dividend payouts, since it is mostly attributed to the one-time impairment and contractual charges.

Anyone concerned about the lack of extraordinary dividends must also note that the management has established that a future disbursement is still a possibility at the right moment, with the stock currently offering a compelling forward dividend yield of 11.9%.

For now, the pessimism surrounding the PBR stock is attributed to the supposedly disappointing FQ4'23 dividend payouts amounting to 14.2B reais (the equivalent of $2.9B) or 1.10 reais/ per share (the equivalent of $0.22 per share), worsened by the lack of extraordinary dividends for the full year.

These numbers may appear to be underwhelming indeed, if compared to the FQ3'23 overall payout of 17.5B reais or 1.34 reais/ per share (the equivalent of $0.36 per share) or FQ4'22 overall payout of 17.7B reais or 2.75 reais/ per share (the equivalent of $0.74 per share).

Then again, readers must also note that PBR has introduced its new dividend policy in July 2023 with a guidance of lower dividend payouts ahead, as the management shifts their long-term focus to renewable energy sources and offshore oil explorations.

In addition, readers must note that the oil/ gas producer's top/ bottom lines are inherently tied to the volatile commodity prices, with FQ4'23 bringing forth lower realized Brent crude prices of $84.05 per barrel (-3.1% QoQ/ -5.2% YoY) and Natural gas prices of $10.56 per MMBtu (-5.3% QoQ/ -18.4% YoY).

Combined with the relatively stable FQ4'23 consolidated sales volume of 3.072 Kbpd (+0.003 Kbpd QoQ/ inline YoY), it is unsurprising that PBR has reported lower sales revenues of $27.1B (+6% QoQ/ -10.1% YoY).

The optics are also temporarily worsened by the higher operating expenses of $6.63B (+84.6% QoQ/ +91.6% YoY), partly attributed to the hefty one-time impairment and contractual charges amounting to $4.2B (+281.8% QoQ/ +452.6% YoY).

However, we believe that PBR's sell off post FQ4'23 earnings call has been overly done, with it triggering a dramatic -11.8% stock price plunge and -$15.59B in Enterprise Value correction.

This is because most of the additional expenses affecting the oil/ gas producer's Free Cash Flow generation of $8.07B (-3.4% QoQ/ -13% YoY) are attributed to the one-time impairment/ contractual costs, which are unlikely to be replicated moving forward.

In addition, the oil/ gas producer has followed its new dividend policy fairly closely, of which shareholder returns (including share repurchases and dividend payouts) comprise 42.5% of its FQ4'23 Free Cash Flow generation, based on the $538M of share repurchased and $2.9B of dividends to be paid out.

While there has been some noise surrounding PBR's elevated gross debt of $62.6B (+2.6% QoQ/ -16.3% YoY), we are not overly concerned, since it boasts growing adj cash of $17.9B in the balance sheet (+3.6% QoQ/ +45.7% YoY).

Combined with the growing profitability, the oil/ gas producer net debt to EBITDA ratio remains extremely reasonable at 0.85x, compared to its Oil & Gas E&P peers at 0.94x. This is on top of the declining financial debts of $28.8B (-3.8% YoY), with the balance mostly attributed to operating leases.

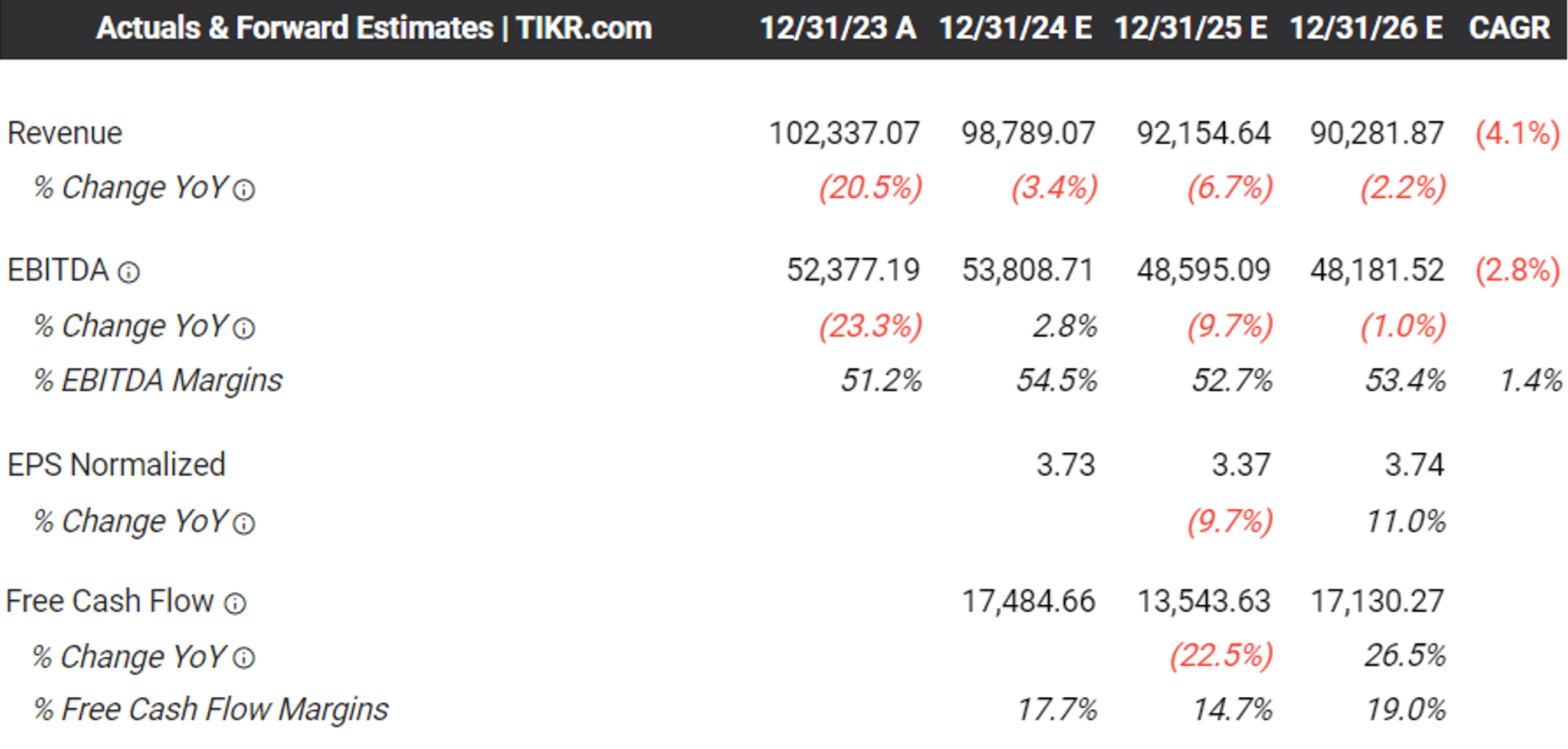

The Consensus Forward Estimates

Tikr Terminal

For now, the consensus has moderately adjusted their estimates, with the impacted Free Cash Flow mostly attributed to PBR's intensified capex projections of $18.5B in FY2024 (+22.5% YoY) and $21B in FY2025 (+13.5% YoY).

As a result of the significant investments, it is unsurprising that the management has also prudently dialed down their dividend payouts to the minimum, in order to better preserve capital.

If anything, readers must also note that PBR still holds approximately $9B surplus in the capital reserve account, with a future disbursement as extraordinary dividends still a possibility at the right moment.

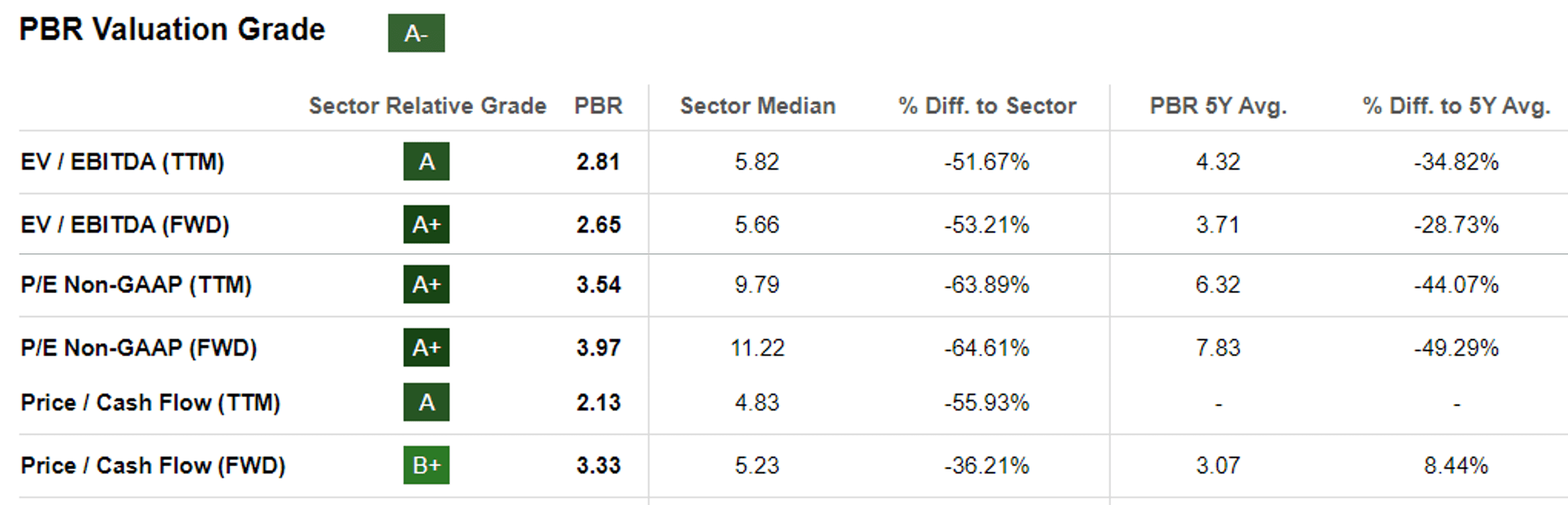

PBR Valuations

Seeking Alpha

As a result of these developments, we believe that PBR is relatively undervalued at FWD EV/ EBITDA of 2.65x and FWD Price/ Cash Flow of 3.33x, compared to the sector median of 5.66x/ 5.23x, Exxon Mobil (XOM) at 6.28x/ 8.13x, Chevron (CVX) at 5.74x/ 7.46x, respectively.

This is especially due to PBR's rich EBITDA margins of 51.2% in FY2023, thanks to its low breakeven point of $25 per barrel, compared to XOM at 22.4%/ $35 per barrel and CVX at 24%/ low $50s per barrel, respectively.

While it is unlikely for PBR's FWD valuations to be upgraded nearer to its peers, attributed to its state run status and Brazil's volatile political scene, we believe that these discounted valuations offer income oriented investors with a relatively rich dividend investment thesis.

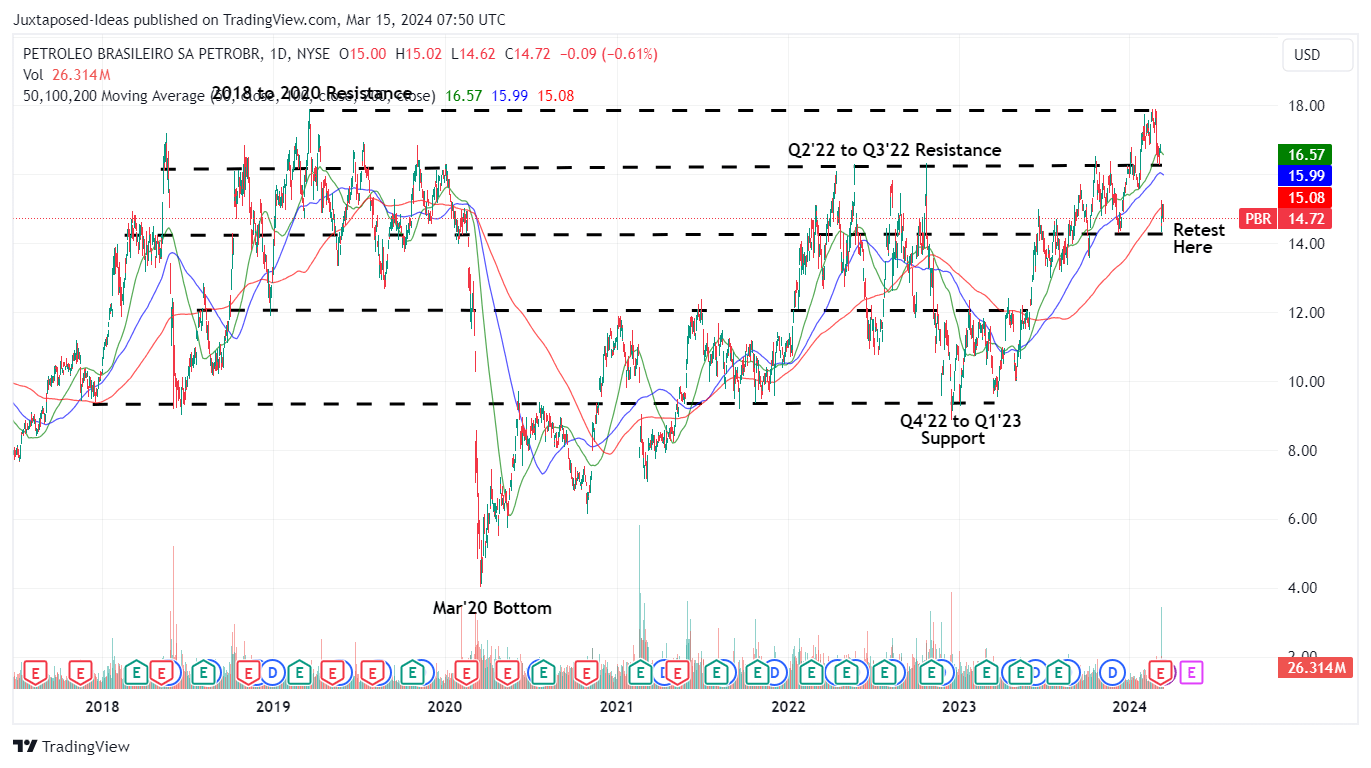

PBR 5Y Stock Price

Trading View

For example, the recent correction has triggered an expanded forward dividend yield of 11.9%, based on the annualized FQ4'23 dividend payout of $0.22 per share and further aided by the doubled dividend payout due to the NYSE ADR ratio (one ADR comprises two Brazilian shares).

Despite the decline from hyper-pandemic yields of over 20%, readers must also note that PBR's yields are notably more attractive that XOM's at 3.47%, CVX's at 4.24%, and the sector median of 3.66%.

As a result, we believe that the recent pullback presents a great buying opportunity for income oriented investors whom are comfortable with variable payouts and moderate volatility.

Combined with the EIA projection that Brent may remain higher at approximately $84.80 by 2025, compared to the $60s reported in 2019, we believe that PBR's dividend investment thesis remains robust, no matter the near-term volatility in the stock prices.

We are maintaining our Buy rating for the PBR stock here.